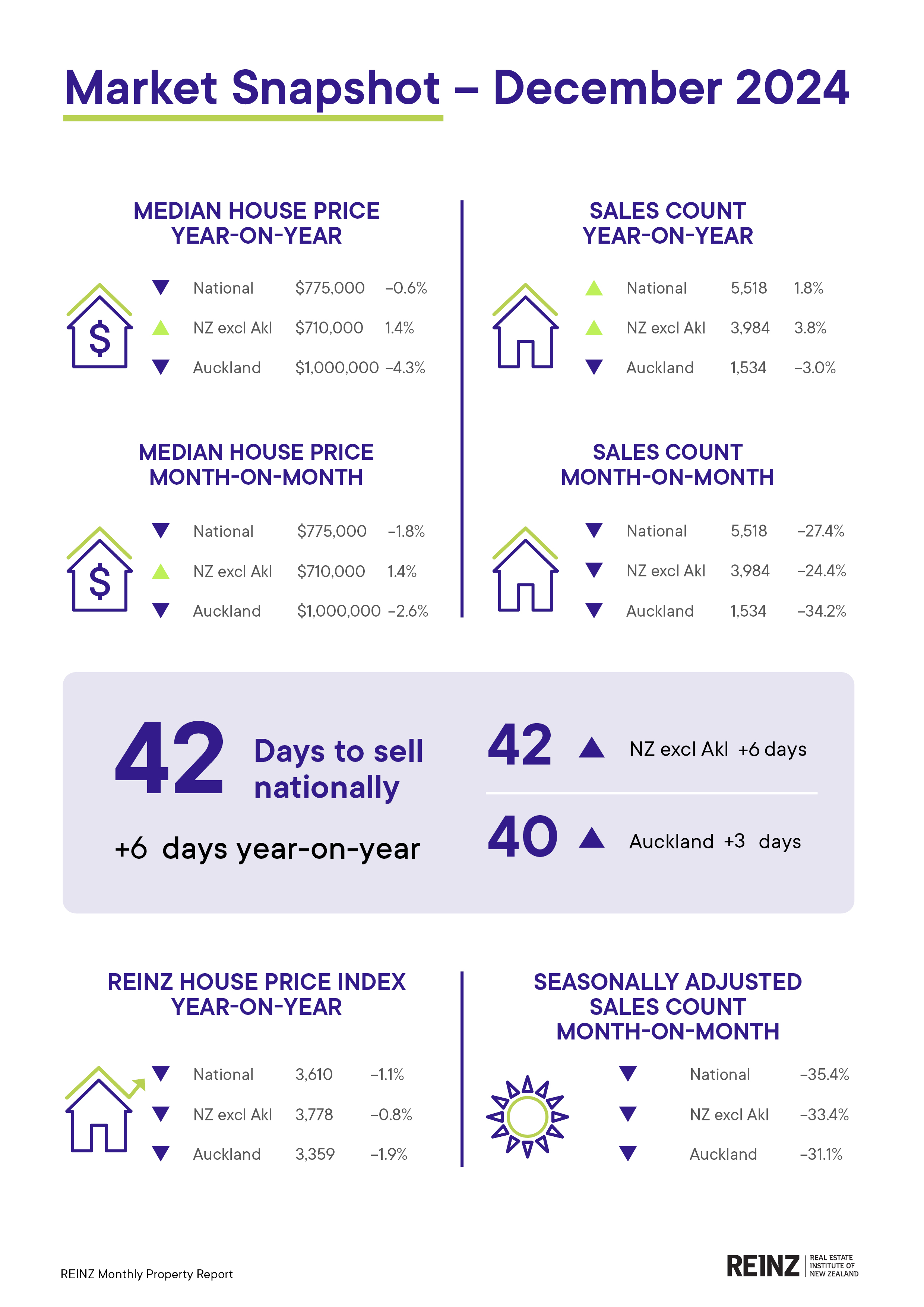

The housing market finished last year on a quiet note, with the Real Estate Institute of New Zealand (REINZ) citing "limited urgency in the market in December."

The REINZ recorded 5518 national sales in December. That was up 1.8% compared to December 2023. However, the market was particularly weak in Auckland, with sales in the region down 3.0% compared to December 2023.

The seasonally adjusted sales figures paint a particularly grim picture. Seasonally adjusted national sales in December were down 35.4% compared to November, with Auckland's seasonally adjusted sales down 31.1%.

"December is usually a quiet month for the housing market," REINZ Chief Executive Jen Baird said.

"For New Zealand, sales count was down 27.4% compared to November 2024 and up 1.8% compared to December 2023."

"When we adjust the figures for seasonal effects, we see that both percentage movements are noticeably less than expected, confirming that December 2024 was a particularly quiet month for residential dwelling sales," Baird said.

The national median selling price was $775,000 in December, down 1.8% compared to November and down 0.6% compared to December 2023.

In Auckland prices were even weaker, with Auckland's December median of $1 million down 2.6% compared to November, and down 4.3% compared to December 2023.

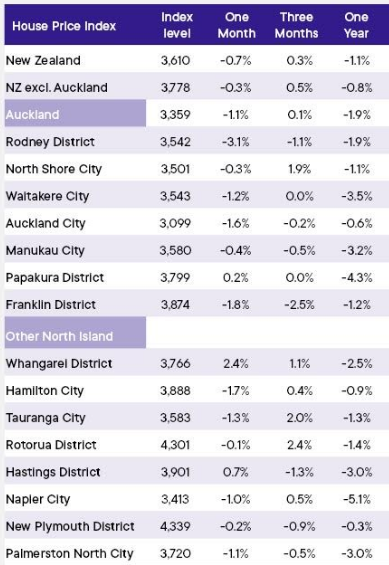

The REINZ House Price Index (HPI), which adjusts for differences in the mix of properties sold each month, was down by 0.7% nationally in December compared to November, and down 1.1% for the year.

The HPI for Auckland declined 1.1% compared to November, and by -1.9% compared to December 2023. See the table below for the regional HPI figures.

In December the national HPI was 15.6% lower than its peak in 2021.

"Sales have risen year-on-year, though we saw a larger than usual drop off in sales this festive season," Baird said.

"This suggests that December 2024 was impacted by the way the holidays fell, making it a shorter than usual December, with many people choosing to start their holidays early this year."

"Buyers had ample stock to choose from and many expected further interest rate reductions, so there was limited urgency in the market in December," she said.

National inventory levels rose 18.5% year-on-year to 29,478, REINZ said.

The comment stream on this story is now closed.

REINZ House Price Index - December 2024

Median price - REINZ

Select chart tabs

Median house price growth

Select chart tabs

Volumes sold - REINZ

Select chart tabs

Volume sales growth - REINZ

Select chart tabs

Days to sell - REINZ

Select chart tabs

176 Comments

RIP recovery.

She suffered a quick and pain free death.

I don't really see this data set as "RIP recovery", as if I had money on the sidelines for owner, occupied I would be moving quickly.

We bought mid-2024 and we've already made 3.9% paper profits via Valocity in six months. Much of this is the type of property we purchased at the price, but not all property in this slide is the same.

Had we not bought after selling in 2022, I would be very very nervous, as I have seen good property in Central Auckland starting to get back to eye watering prices.

Lots of anecdotes not a lot of substance.

All agents are telling me things are heating up but they also did 6 months ago and look where we are.

Only agent I know on a personal level has had to get a second job as in their words "you cannot live by only selling 5 houses a year".

So yeah the market is exceptionally weak.

Never and more accurate life Truism...."if the RE Agents lips are a movin, they are a lyin!"

Valocity! Homes! If you are relying on them you certainly have nothing more than paper profits.

If you bought mid-2024 and you 'made 3.9%', you are an outlier.

What are you going to spend your profits on?

Wafers to munch on while dreaming about those gains..

I picked a figure for my valuation and wrote it on a bit of paper here on the desk. Made 100% paper profit in no time! Obviously not all property is the same, but I'd be quite nervous sitting on the sidelines with these sorts of possible gains.

My point wasn't shouting from the roof tops about paper gains, more that these broad index tracking for a year on year basis wont be the best way to view the current state of the many unique markets.

The likelihood is we are going to see 100bps off the OCR in H1 2025 and things can change quickly.

But all the above comments are fair!

I love how Spruikers claim paper profits, but paper losses are not losses until you sell....

My point was more broad based numbers aren't truly reflective of what is happening on the ground in a massively diverse market.

This is especially true in a 12 month period where there has been huge change in the underlying factors.

Pricing momentum in freestanding homes in desirable Auckland, Christchurch and Queenstown suburbs, with weakness in Wellington and apartments can both be true. They are very distinct segments rolling into a broad index.

I'm personally hoping property doesn't have price increases mid term. We aren't investors and are hoping to upgrade in the mid-term, so that would be a good outcome for us.

But guess we'll know by next year's HPI January release to see the eventually outcome.

Also, my Valocity valuation is down 5.4% in a month, but it's fluctuated +/- 4-5% in the last year.

RIP housing market, going to take a very long time before it can resurrect..

Might be similar to Japan, wait for a couple of decades..

Market will be flat for 2 years and then take of in 2027/28.

"By now, sell in 29"

As the Rookiest of wannabe property tycoons would surely know, these once in a 100 year property crashes (as we have certainly now) take on average, 6 years to play out to the very long, scraping bottom.

So waiting for 2027, for a much lower priced ledge, that may eventually hold is in 2027, or possibly longer?

In the worst case, such as happened in Japan since 1991, it took 18 years to crash to a 47% loss, but it's much worse, if you account for it in Real Terms, with inflation adding to these massive losses.

Inflation has raged in NZ at a combined +20% since 2020, so if your property has not gone op at least 21%, you have effectively gone backwards in REAL TERMS in the last 5 years.

Property has been the worst of all major investment options, all told, since the never to be seen again high tide preposterous property peak of 2021. (ok maybe the 2030s, may see a new peak, possibly???)

Those insanely leveraged, talking foolishly about "the bottom is in" or "the time to buy was last month" or "the 2023 bottom has passed" look like totally novice tools, whose TA and AC - like, warped views and narratives, are not worth a garbage can full of stinking and rancid doggy doo.

Watch as the convicted cheaters, schemers and fraudsters in the Real Estate industry, try to polish this terrible, much delayed turd.

For anyone to listen to these professional "turd polishers" as abounds on the all-encompassing "Buy Now" Narratives on property pages of the Awful Oneroof and NZ Heralds......you truly need your head read and will be led into financial oblivion, by following such financially self-interested charlatans.

Buyers beware, offer only the 2015 previous price guide/RVs or lower, as 2018 prices are now being hit and seen in the sales reports and its declining at rates not seen, since the Great Depression.

Don't think Japan imports as many people in proportion to their population as NZ does.

"Inflation has raged in NZ at a combined +20% since 2020, so if your property has not gone op at least 21%, you have effectively gone backwards in REAL TERMS in the last 5 years."

FYI,

Estimated inflation adjusted REINZ house price index to Dec 2024 from peak:

1) National: -26.6%

2) Wellington region: -34.9%

3) Auckland region:-31.6%

4) Whangarei: -26.2%

5) Hamilton: -26.5%

6) Tauranga:-25.8%

7) Rotorua: -24.7%

8) Hastings: -28.6%

9) Napier: -30.12%

10) New Plymouth: -17.9%

11) Palmerston North: -28.6%

12) Nelson: -23.0%

13) Christchurch: -11.4%

14) Queenstown: -12.7%

15) Dunedin: -22.4%

16) Invercargill: -17.3%

Note that:

1) all are NEGATIVE

2) what happened to the commonly repeated mantra by property promoters "property is a hedge against inflation"?

Those old property mantras, often wheeled out like a rickety old wheelchair by Ashley Church, Tony Comb Alex, and the Oneroof radio show guests, are gone rotten, much like their general advice has.....poof! - like a fart in the wind.

The Property sector in general has been the worst hedge and the worst for the NZ Inc economy, in general. It has also been the most rapid evaporator machine for wealth since the 1930s/1970 crash events.

Tough life and financial Lessons will be learned the hard way, upto 2030.

"Tough life and financial Lessons will be learned the hard way"

Unfortunately there will be owner occupier households who will lose their entire life time of savings who will be collateral damage in the residential real estate market mania.

You'll have to account for the inflation effect of diminishing mortgage debt. Rapid wage growth has meant my debt: income ratio has shifted substantially over this 'peak-trough' period. Now that lower rates are back, ability to build equity by overpaying mortgage is strong.

Mid 5's aren't lower rates, historically they're just above average. The debt level is the issue, not the interest costs.

In a falling market buyers have all the time in the world. In fact waiting will likely get you a better price.

The best hope for sellers is that RBNZ keeps trimming.

Looking like another year of catch-up for incomes in relation to house prices.

so long as income increases isn't eaten up by inflation, especially with a weaker exchange rate...

…which will put upward pressure on interest rates….

Indirectly and with a gather-data-and-see-cpi-increase-before-RBNZ-decides lag

Interesting that there's static and negative growth in spite of recent interest rate falls. Lags or other factors?

Not really - as I've been hammering away at on here for a few years now was that falling interest rates does not always correlate directly with rising prices (in the short term)...even though the property bulls/vested interests wanted everyone to believe that as soon as rates went down, house prices were going to be back to high annual returns. This has not occured and is not a surprise to me - its the same as what happened in the USA when I lived through the GFC and falling housing market there.

The drops in rates we have had is only just holding the market in place - it shows just how weak the market really is. Business failure/unemployment etc haven't peaked yet (at least as far as I can see) so falling rates is only just countering those effects. Another external event that triggers rising inflation again could be really damaging to our economy (in my opinion). We are only just holding on with falling rates - let alone flat or rising rates again.

As the history of yield market inversions shows - it can often by 24-36 months after the inversion before you start seeing any real strength in a market. So in our case, that could be 2027 or even 2028. Of course history doesn't always repeat exactly but I doubt our market is going to be back to the moon anytime this decade - I more see flat or even falling prices for quite some time yet.

As I too, have been hammering away here saying that prices dont begin going up until the END of the interest rate cutting cycle, not the beginning of it. And if interest rates go on hold after February we may not see the END for a long time. Because we are in the "longer" part of the "higher for longer" bit.

The end of the cutting cycle may arrive within a month

I have to say they gave it a pretty good polish. Where I live which is a very popular NI provincial capital the market is dead especially over $1.5 m or so. I know of several taken off the market as the vendors are totally frustrated as over several months on the market they have not had a single offer. Thank heavens Christchurch is okay. I will sleep tonight.

Ex Agent, so you finally realised that Christchurch prices are still rising and they will continue to.

Christchurch has the largest number of houses being built for population, which is no surprise to me as it is the most popular city now in NZ.

Auckland has only grown thru immigration and from what I am told by those that have moved south, to its detriment!

All those new homes will put Christchurch house prices under more pressure than they already are. Another factor that puts a lid on Christchurch house prices and business growth is that immigrants don’t want to live there. The earthquake history, bad weather all year around, right wing inhabitants and lack of work and business opportunities compared to Auckland.

Ex Agent, with respect you clearly do not know ChCh at all.

Your negative comments about it just shows ignorance and not really worth debating with you.

As to immigrants, probably best not to comment.

Bad weather is news to me, unless you are unable to put on a couple of layers in the winter.

More sun and less rain the Auckland and Wellington, I've been biking daily for a decade without the weather getting in the way. I get wet perhaps one day a month on average.

Hows that rain in Aucklsnd going abloody scorcher down here. Blue bird day after blue bird day. And no traffic jams on the motorway just for a start.

"so you finally realised that Christchurch prices are still rising and they will continue to."

From the table - Christchurch City month on month HPI change: -0.7% (i.e NEGATIVE)

Beware the potential undisclosed vested financial self interest and potential conflict of interest

Owner occupier buyers: CAVEAT EMPTOR

Reminder (note that I have bolded the words for emphasis):

by The Man3 | 7th Jan 25, 2:20pm

I will guarantee you that prices in most parts of NZ will be up this year and ChCh minimum of 5%.

NZ house prices in many parts are cheap and will never be cheaper again.

Temu3 is as reliable, as some cheap internet purchase junk....promising all nirvana, if only you buy my "investment" off me, in the former swamplands of Chch, at stupidly elevated prices.

Soz Temo3 - the values are down and so with your investments......

Property developers, property promoters and real estate agents in the current environment can be summed up in this one line:

https://youtu.be/wYlptbR0Dkw?t=22

Otherwise they might end up like this:

1) https://www.1news.co.nz/2024/08/12/du-val-receivership-tradies-cleaners…

2) https://www.stuff.co.nz/business/350241770/work-was-drying-timaru-build…

3) https://www.stuff.co.nz/nz-news/360546664/home-building-firm-owes-credi…

4) https://www.stuff.co.nz/business/350240131/taxman-seeks-liquidate-two-s…

5) https://www.stuff.co.nz/business/132096262/auckland-construction-firm-w…

6) https://www.nzherald.co.nz/business/most-of-gurpreet-grewals-agency-cre…

7) https://www.nzherald.co.nz/business/tough-market-century-21-real-estate…

8) https://www.stuff.co.nz/business/350236906/weak-housing-market-blamed-r…

9) https://www.pressreader.com/new-zealand/the-press/20241221/282084872410…

Just became aware of this one.

The developer of upmarket Ōrākei apartments has had liquidators appointed after debts mounted to $3.76 million including $2.3m due to Inland Revenue.

https://www.nzherald.co.nz/business/developer-of-multi-million-dollar-o…

FYI,

Christchurch housing market keeping everyone honest - 'buyers don't have to overpay'

1000 more houses on the market for sale.

https://www.oneroof.co.nz/news/christchurch-housing-market-keeping-ever…

Correct, they will be up this year in most places, 2025.

"limited urgency in the market " LOL

Now, about those Foreign Buyers >$5M....

so the year ended with a 1.1% drop in the HPI, not exactly a crash. I expected a lot worse for 2024.

the past quarter showing improvements in most regions, including Auckland, the most inflated region.

Median house price, excl Auckland actually went up last year.

Classic - reverting back to the median house price to elicit your copium because the HPI doesn't fit your narrative

"the past quarter showing improvements in most regions, including Auckland, the most inflated region."

Auckland past quarter +0.1%

Auckland past quarter +0.1%

Not exactly the massive crash many here have hopium for.

Tell us Rookie, how long do you think a crash takes to play out?

Rookie is advised to research deeply and not base his life's investments on the property spruiking pages of the pro-property Oneroof......Pied Piper and cliff edge comes to mind here!

How long until this crash bottoms Rookie?? Japan styles???

Residential Property Prices for Japan (QJPN628BIS) | FRED | St. Louis Fed

we are by no means, anything similar to japan.

I know what you mean!! Our NZ DDDebts are higher and our economy is much more vulnerable!!

NZ is truly up the Karzi, worse than 1991 Japan problem styles.....

Maybe we will become a world leading economy like Japan too, yeah right mate!

there is no defined time, strange question.

If you can't define a time then what makes you believe the NZ property crash is over?

Your comment suggests that people were predicting a "massive crash" to happen in the final quarter of 2024. Can you provide evidence to this claim?

His personal necessity.

From another interest article.

"However we also haven't seen quite so many reductions this quarter in particular, which indicates that we're now at or very close to equilibrium in the market," Wilson said.

in 2022 we crashed 25% ish, since then the market has been flat, small increases and decreases. its been 2 years since the crash. the next part of the cycle is the recovery.

TBH i don't think the recovery will be fast, but i think the crash is over.

Ok so you’re getting your “facts” from what the QV operations manager is telling you. No surprises there.

And no evidence to share about the claim of a massive crash in the final quarter?

Who the f*** is Wilson?

Given Rookie's comments, that is feasible.

@Time Lord - if i may politey request - why do you care? - you stated your points - market is going down - Rookie (like me, apologies not speaking on your behalf Rookie) we hedge our bets and live with the outome - I have set sail and there might be bounty - if there is good if not well that is the choice I made - you miss 100% of the shots you did not take right ?? So don't take them - no-one is selling you anything - buy / dont buy / rent / don't rent - however just stop trying to proof that you are right (because you dont know)

Honestly SAH you’re doing yourself a disservice putting yourself in the same camp as the Rookie. Your comments are far less biased and more open to reason. Hence I’m questioning their posts and not yours.

Rookie uses this site to speculate on every property article regardless of the data and plays mental gymnastics to try and fool the reader (eg1: choosing alternative data to the article he’s commenting on. eg2: claiming people said there was a massive crash coming in the Q4). Is he/she doing this to try and entice buyers into the market?

I’m simply questioning his claims which is all it takes to see his logic fall apart. If you expect Rookie to continue posting nonsense, then expect others to continue responding with counterpoints.

you have no idea what you are talking about, you've never actually tried to have a discussion with me, so how would you know im not open to reason, the times im not open to reason is towards people who aren't biased themselves, i'm always open to a good discussion, so if you're willing im happy to indulge ;)

Median house price, excl Auckland actually went up last year.

So excluding the biggest market that is also the lead indicator of the national market. ,,🤡

Auckland has the biggest impact on the national figures, but i wouldn't exactly call it a lead indicator of the market the past year.

I know you wouldn't, because it doesn't fit your spruiker narrative. Doesn't mean it isn't.

Definitely noticing down here in Chch that properties are taking longer to sell (with some exceptions). I'm not talking about the rubbish Williams Corp/Wolfbrook townhouses either, or the 'there's always another one waiting' new subdivision builds but older houses in more established areas, or ones that have been purchased and done up to sell ... in fact there's tons of places I've seen where clearly somebody has bought, spent up on upgrading, and now cannot get 'what it owes'.

Interesting time for the dumbthoughts clan as there is a second child on the way, and the current house probably isn't big enough (owing to part of it being used for my business). Also not in a great school area.

There are a few places we've viewed where if the vendor would accept CV (and we would get CV for ours) the cost difference would be worthwhile but the vendors prefer to let the property sit unsold at 10-20% over the CV and the agents inform it's not even worth bothering to make an offer of the CV ... of course they are incentivised to say that but it makes the upgrading house process a total pain.

"vendors prefer to let the property sit unsold at 10-20% over the CV and the agents inform it's not even worth bothering to make an offer of the CV"

I would still push the agent to actually present your CV offer, don't listen to their spin

There was an article in the Press this morning that I think 6500 new homes were consented in Canterbury last year, the highest rate per capita in the country. They might be in for a long wait with so many new properties coming on the market

I frequently take my dog for a walk/run around the new 'wetlands' area in Halswell (can't remember the name of it, but it's heading towards the old quarry). It's incredible the amount of new houses being built out that way. You can get a very nice - by my standards at least - 4 bedroom for around $1 million but that still feels a lot to pay for a generic cookie cutter new build, when there is always a nicer, newer one popping up just next door. There are also clear congestion issues building up around there w/r to people travelling into town for work.

Te Kuru, nice place to go for a walk, run or bike, been there a few times, in theory it should prevent flooding in the area, but hasn't really had a true test yet. Both around there, and on the other side of Halswell, the Longhurst side there is a huge amount of development. Maybe in a decade or so houses will bridge the gap between there and Prebbleton.

If you're able to bike, the Sparks Rd cycleway means the city is only 30 mins away, regardless of the traffic. Hopefully they extend it through to Halswell proper and down Sutherlands Rd as it currently ends in the middle of nowhere. It will also be interesting to see what happens with the bus lanes being added to Halswell Rd, the southwest is currently underserved in terms of buses, but it is hard to get people out of their cars.

In a decade or so, Rolleston, Prebbleton, and Lincoln will have merged to form one large town. Then it will be interesting to see what happens to Council boundary areas as more CCC ratepayers discover they can live just outside of Christchurch and not have to pay for any of the facilities they use, or the multi-million dollar cycle lanes that hardly anyone uses.

They'll be in for a rude awakening. Road maintenance in urban periphery areas will sink them. Lower population levels mean lower rate take but higher road maintenance costs.

Cycleways are the cheapest and most sustainable transport mode, both to build and maintain. If you think cycleways are expensive dig out what percentage of your rates goes on maintaining roads (many of which are close approaching full rehab/renewal levels which means costs are about to increase even more). Try not to get sucked into the culture war nonsense designed to distract you from the real issue. We cannot afford to maintain current car level use.

cycle lanes that hardly anyone uses.

Not what I’m seeing:

https://www.odt.co.nz/star-news/star-christchurch/cycling-numbers-all-time-high-christchurch

Te Kuru, that's the one. Will be interesting to see what happens if/when then next big rain event occurs (lots of houses built very close to it).

I agree with your and KWs assessment that in the next 10-20 years that whole area will sort of merge into one, so Lincoln, Prebbleton etc will all form part of greater Chch.

Interesting comment KW makes about being able to buy outside of CCC zone, enjoy lower rates, and then still make use of the CCC ratepayer-funded amenities.

Certainly most of my friends have purchased nicer (spec/size-wise) houses in Lincoln, Prebbleton, Rolly etc whereas it's just muggins here who is stuck with a fairly small, freehold townhouse. Perfect for a couple or with one kid, but not really enough for a family. That being said I never get stuck commuting!

Christchurch does not have a lot of CBD based businesses, like Auckland and Wellington does. Most of Christchurch's big employers are located in areas like Hornby, Halswell, Sockburn, Russley, Harewood. And rapidly migrating out to Rolleston where rents are cheaper and there is more land for expansion. So commuting to most people's work isnt a problem, as you dont need to go to the CBD or through the CBD. Which is why no-one uses buses in Christchurch - they simply don't go where people need to go. Implementing a central city based public transport system as though Christchurch is the same as Auckland and Wellington, is just stupid. Then most of local Govt is run by stupid people.

As Rolleston becomes an even bigger hub for industrial businesses and manufacturers, more workers will migrate out there. Christchurch is going to shrink. There's only so many Ubers, massage parlours, and liquor stores that a city needs.

One of the reasons people don't use buses is because the city centre is flooded with cheap underpriced parking.

Buses and cycles in ChCh absolute waste of time.

Generations coming thru will not be interested in busing nor cycling as too time consuming.

ChCh the growth city of NZ.

Bus, I agree. Bus in Chch is rubbish especially if you have to go through the bus exchanges. I remember watching a documentary about the goings-on at the Chch bus exchange ... was called 'Black Hawk Down' or something. Also fares are rather pricey unless you are on supergold card or some other discount.

Cycling, completely disagree. Fastest way to get around town. I could definitely bike from Halswell to CBD faster at peak time than drive. I say this as a petrolhead who otherwise drives a V8 4x4 or a tuned up turbo sportscar ... my bike is the best form of urban transport in Chch by a country mile. Hence why I have an eBike and then keep the gas guzzlers.

Getting anywhere in Christchurch on a bus is a painful process. It takes me 7 minutes to drive to the CBD. If I caught a bus, it would take me 26 minutes. I literally could be there, and back, in the time it takes me to walk to the bus stop.

A 14 minute drive to the Airport, is 50 minutes by bus. A 24 minute drive to Sumner Beach is 1 hour and 15 minutes by bus.

Now lets say you live in Rangiora and work in Hornby - thats a 32 minute drive, or 1 hour and 45 minutes by bus. And the Council still insists on putting permanent bus lanes on Main North Road and Cranford Street.

The only way the Lefties/Greenies can make travelling by bus competitive is to slow down cars. Which is what they are doing by installing speed humps on all the streets, making everywhere 30 kmph (including on major arterial routes in/out of the town), and reducing double laned roads to single lane roads by installing a ton of cycle lanes and dedicated bus lanes that cannot be driven on regardless of the time of day.

Coming soon - congestion charging.

Buses in Chch are a $2 flat fare, and half that for kids, it may be the lowest public transport fares in the country. Price isn't the issue with buses

Going up to $3 a trip as soon as the new payment system is implemented. But after that, looking at $8 a trip fare coming up.

https://www.rnz.co.nz/news/national/535565/bus-fares-in-canterbury-may-…

I doubt hypothetical future increases have much impact on current demand levels

But it should impact hypothetical future demand simulations, which drives the implementation of turning car lanes into bus lanes - which now just carry practically empty buses all day. Back when they first opened the Northern Corridor, they made buses from Rangiora free to use - and the patronage was still an average of just 7 people per bus in peak hour. Now those bus lanes are permanent, and even less people use them.

Edit, KW's bus pulled up first with a similar comment.

I found the Christchurch bus network quite good when I lived there pre-2017.

My comment is not so much on the network ... just that with the proposed pricing increases it will be very expensive (and even at current prices, provided I can get a free park, I can drive from home to town for a meeting for less in fuel than a bus fare costs), and also it can be a bit 'dodgy'. Also as KW points out it's slow.

I remember checking the timetable and seeing that for me to bus from where I live to where I meet clients (if not working remotely) is more than 2x the journey time even when the bus uses the bus lanes.

Yeah biking is great!

Always have trouble carrying 10 bags of groceries on the handlebars though!

to be fair, biking is for those that can not afford petrol.

You da man. Buying 10 bags of groceries everytime you use the car, what a legend.

As you can see, the Man, is a big big spender and happy to throw money away, factor that into your thoughts when you consider his financial advice that CHCH housing is a good buy.

Where would you possibly bike to without having the need to be carrying something on the way to and back?

Young ones are not biking in ChCh nowadays and will not in the future.

The Council gas blown mega millions in putting in bus and bike lanes for very little use, as they got big handouts from the govt.

In the years to come the cycle lanes will be tossed out.

The obvious answer is commuting, which many people do several times a week and office workers probably don't need to carry much. Even if you do, bags exist.

I think you should get out on your bike and see all the youngsters out there enjoying the summer weather - might be just what you need to stop being such a grumpy bugger.

Yes I really don't understand the hate towards cycling (well I will say that I have an immense dislike for the road cyclists who seem to think it's cool to dress up in that tragic fake sponsor lycra, wear airpods while riding, and ignore all the road rules and ride in big groups). I've never had a single issue as a motorist with a "commuting" cyclist, however.

As I said, I'm a genuine petrolhead and love cars, but you just cannot beat bike as a form of transport - especially now there are so many ways to get around without going on the road thanks to the cycleway network. Get some exercise, get some fresh air, beat the traffic, you can do most things with a bike (I can fit a good amount of shopping in my backpack) ... love it.

Lol

He’s The Man THE THIRD

what kind of ego refers to themselves as ‘The Man’

😂

I'd love to see the number of people cycling out to Rolly to go to Costco (if it ever gets built, seems like there is a big impediment to expansion in this country unlike Australia).

Bulk buying is probably a reasonable use case for a car, once every few months.

Using half a ton of car to move yourself around a small flat city, or to transport a couple of litres of milk, is insanity. How desperate we are to avoid a little bit of fresh air and exercise.

With my pannier bag I stop off at the supermarket once or twice a week, works just fine for us. If I take a backpack as well I can pick up a couple of week's shopping.

I bike because it's quicker, more efficient, gives me some exercise. The fact that I save a bunch of money is a happy side effect - I'd still bike if I could drive for free.

We're saving up for a cargo bike. Solves the problem of moving people or goods.

Not settled if we'll sell the car yet

biking is for those that can not afford petrol

Or those who value their health and enjoy the winding up and down for the day of biking to and from work. I don't get the whole cyclist vs motorist thing, notwithstanding there are some horrible cyclists and also motorists when it comes to obeying the road rules. Live and let live folks, one day you'll be 6 feet under and not have a care, dollar nor house in the world to give.

Obvious troll, but I'll play along anyway.

I commuted on a mountain bike in Hawkes Bay for 7 years, starting about 15 years ago. I wore rugby shorts and a hi-vis t-shirt. It was only a 7km trip to work but it involved 70 and 80km/h zones. It took me about 12 minutes, which was a little quicker than it would previously take me to drive, park and walk. There was a shower at the office, and I carried my bike up a flight of stairs then "parked" it in a storage room. I carried a change of clothes, lunch, and laptop in a backpack. I'd put in one earbud and have the radio for company.

I rode in the rain, wind, 30+ heat and 0- cold, because I'm not immediately water-soluble, nor am I a wuss.

I lost 8kg, and built up leg muscles that I still (mostly) have today. My fitness and energy levels went through the roof. I had no problem keeping pace with the lycra-and-carbon crowd, which impressed some and annoyed others. A young lady at my office unknowingly described me to my wife as "that guy with the great butt." Awkward.

In all that time it cost me $500-odd for the bike plus maybe $30 in inner tubes. I could swap out a (rare) flat and be going again in 5 minutes. No gym fees, no parking charges, no door dings, no traffic jams, lower motor vehicle expenses.

I used the savings to upgrade one of my fun cars.

Halswell that ends well

Most of the new builds are in the Selwyn and Waimak Districts, with Christchurch locals moving out of the Christchurch area to buy cheap family homes, whilst family homes in Christchurch are bulldozed and replaced with 2 bedroom townhouses designed for those living out of a suitcase.

There's one down the road going to auction in a few weeks. 4 bedroom, top school zone, good street. 90's build - they bought it for $910k and then reclad and renovated it. 2022 CV of $1.24M. I'll report back on the outcome. Hopefully it will be before the commenting ability gets cut off.

Do you mind letting me know the property address? I might go check it out!

Part of the problem I'm finding is a lot of these done up places the vendors appear to have spent too much.

E.g. I've seen a nice property in Fendalton that would perfectly suit us. Vendor asking $1.35m after no sale at $1.4m, they bought in 2022 for around $950k. Clearly has had some tasteful work done (fancy kitchen, improvements to living areas, very chic outdoor area). Great schooling, and convenient to shops and other amenities.

However, when looking at the 2022 listing (found on Google) it's clear the property wasn't in terrible shape to begin with. In fact the upstairs bedrooms look largely unchanged, so you are paying $400k for what looks to maybe be around $150-200k of work.

So the vendor sits there saying "it owes me $X" but prospective buyers such as myself don't want to overpay for the work they have had done. If this property was around $1.1-1.2m I'd be looking a lot more closely.

Thus a standoff ensues.

If they got a place in Fendalton for under $1M then either its (a) got leaking issues or (b) its got earthquake repair issues. Both of which would probably have been covered up by the subsequent renovation. But not necessarily fixed. Buyer beware.

Personally, I would not touch a pre-2011 build unless it was just a cheap house close to its land value, so if it falls down it wont be such a financial loss.

Fair point. It's a 1990s house (so I'm guessing leaky risk?) - I just said it's nice based on external observation and if it were "sound" it would be a good fit for us. Agree that you normally can't get anything in Fendalton under $1m.

Its probably both. Fendalton was quite badly damaged in the EQ because of the three waterways that run through it (Avon, Waimairi, Wairarapa). However, the vendors and agents are probably plugging "water views" to out of town buyers who don't understand that post-EQ being close to water is a hazard not a feature.

Like this one. Last sold as an "As Is, Where Is" - back up for sale and now they want $6.2M for it. Previous sale price has been scrubbed from the online sites. LOL. Some unsuspecting buyer will be sucked in.

https://www.harcourtsgold.co.nz/listing/pi69597-29-garden-road-merivale…

"now they want $6.2M for it."

LOL.

"Previous sale price has been scrubbed from the online sites. "

Sellers want to reduce price transparency for market participants, keeping market participants entirely in the dark.

Last sold Sept 2021 for $2.9mn?

only possibly leaky if a plaster clad.

1990 houses were very well built generally

My ass they were!

many leakers, and if not leakers then poorly insulated and damp

60's and 70's baby. Still using heart Rimu framing, often overengineered to some degree or another and with appropriate maintenance, will last and last. You can't get that wood anymore in quantity, os keep the borer at bay, the moisture out and they'll last and last.

I’m curious dumbthoughts, you say that your house is not big enough, why not?

Honestly, some of it is 'necessity' and some of it is want.

Main issue is we have a 3 bed townhouse. One room is used to run my business (which is the primary 'breadwinner'). Master room is for wife and I, other room is for child 1.

Once child 2 needs his/her own room, I'll be out of the office. There is a small study nook but it's simply not appropriate for my needs.

So there is a need for an additional room of some sorts (ideally away from the bedroom area so little feet aren't tempted to interrupt me while I'm working).

In terms of wants, the downstairs living and kitchen is very modest. E.g. there is barely enough pantry space now we have to buy more food because we have more mouths than when it was my wife and I. The lounge area feels packed if we have even another couple of people in there as guests.

Outside is a usable patio space but no garden or much space for the kids and dog.

So the living space is more of a want of desiring something bigger to accommodate 2 children, friends bringing their kids over etc. The office issue is the pressing need.

I could look at converting part of the garage to an office but unsure if this is feasible or wise.

Fair enough, the reason I ask is at times it seems people confuse wants with needs. We need a bigger house because we need a spare bedroom and another toilet (teenagers) and another living area (get away from the kids) bigger bedrooms (for bigger kids). All things you don’t really need at all, and potentially very expensive to have. Fine if you’ve got money to get rid of, not so smart if you don’t.

forgot to blame the weather. Maybe that's being saved for the next set of results?

I always find interesting the 5 year average price increases, shown in the HPI report. So the five year average price increase for Auckland is now 2.8%. So to 'double every 10 years' prices they need to increase by 85% in the next five years.

The regions (NZ exc Auckland) have grown by 5.4%. What I believe is happening is that industry and population are leaving Auckland. The previous growth in Auckland was supported by poor targeting of accommodation supplement that made industry stay there, but can't afford to any longer.

However, Auckland supply has continued - still building at 15,000 houses per annum. So little chance of price increases in the future

And remember that even the 5.4% growth over past five years is probably less than the interest rate during that time.

So to 'double every 10 years' prices they need to increase by 85% in the next five years.

I think it's "double every 7-10 years" according to Ashley Church and the rule of thumb taught as seminars across Aotearoa. Lord Orr said housing was a consumption good one time - possibly trying to worm his way out of being responsible for the 7-10 yr prophecy embedded in the nation's belief systems.

Anyway, if the credit impulse works its magic, who knows what could happen.

Down, down, down the road,

down the ponzi-crash road.

There is no reason for the housing market to do anything other than stagnate or continue to fall.

The best and brightest are still heading offshore in droves and the replacements don't have much money.

Many people have been taught a valuable and recent lesson about housing bubbles and the personal consequences of reckless borrowing.

The job market is munted and government spending is still being bought under control.

The asking prices are still ridiculous by any metric. First world prices for third world housing.

These real estate types need a reality check. New Zealand housing is a dead horse.

Nailed it Brocky.

Bring on the much lower priced market and DTIs averaging around 4x in 2027.

Happy days.

"This suggests that December 2024 was impacted by the way the holidays fell, making it a shorter than usual December, with many people choosing to start their holidays early this year."

No, this year's result was just an aberration caused by the way the Christmas holidays fell. Back to 10% / annum growth without a doubt!

/sarc

With respect, you are deluded if you believe house prices are cheaper in Ozzie!

Quite the opposite, we are cheaper than over there.

NZ housing is more affordable than the Ozzie Cities and just as many opportunities.

Like for like, all things being equal, Ozzie is cheaper.

With respect, I don't recall mentioning the price of dwellings in Australia? We were discussing the future direction of NZ property.

But, since you brought it up, you are welcome to fact check yourself here: https://www.realestate.com.au/insights/proptrack-home-price-index-decem…

In general the housing in Australia is also more spacious and of a higher standard than NZ, thus better value for money.

Incomes are higher and just as many opportunities is demonstrably false.

"But, since you brought it up, you are welcome to fact check yourself here: https://www.realestate.com.au/insights/proptrack-home-price-index-decem…"

Some leading indicators for Sydney and Melbourne show potential residential dwelling price risks are extremely elevated and vulnerable.

You conveniently do not mention that the wages and salaries are much higher in Australia. So many kiwis have struggled to get a home of their own here and so off they go to Australia and in a couple of years or so they have bought their first home. Oh and they have super accounts that are huge compared to our pathetic KiwiSaver accounts. You obviously did not have the skills or nohow to make it over there.

Ex Agent, far too heavily taxed for what you receive in Oz!

Far easier to operate in NZ and you dont have to put up with Ozzies!

There we go, earlier on a little dig at immigrants and now slamming Ozzie's, TheMan happily illustrating that those hick Christchurch stereotypes are grounded in truth. Hopefully all the immigrants migrating there will loosen and lighten things up a bit.

Not many immigrating there. They nearly all go to Auckland as they know they can get ahead there. Better weather, more business and work opportunities, less right wing bigots and bigoted old farts like him and less chance of a big one.

2024:

NZ: The median earner paid ~$7,000 tax on their ~$50,000 income.

AU: The median earner paid ~$13,000 tax on their ~$67,000 income.

So the middle AU pays more tax than the middle NZ, but still takes home more in the hand than the middle NZ earns gross.

And just for completeness, a NZ on $67,000 (incidentally the 75th percentile) pays $12,320 tax. And an AU on $50,000 pays $7,300 tax. So comparable.

And we haven't even considered the exchange rate and relative purchasing power.

if you a slumlord/hopium/spruiker anything else (which I am) the worst look like it is behind us - also less properties on the market and lower interest rates - this slumlord spruiker (whatever you would like to call me had done it tough) however with recent drop interest and good tenants outlook is looking better. Would like to add I do hope this is a better year for all - so if you a DGM i guess you would like it worse?

You seem like one of the Diamonds in the Rough SAH, of a largely "Blood from a Stone" money grubbing, landlords.

Look after your tenants, consider their much lower in general/financial means and you will do well ......just may take a decade or two.

less properties on the market

Did you miss the bit about inventory surging 18.5% year on year?

@agnostium - no i have not - you might have missed the article on less houses for sale and market catching up - also there is inventory (like apartments and 3 high 3 deep townhouses ) that is classified as inventory - I am invested in free standing homes with a bit of land. Still desirable 1. for tenants with kids 2. buyers

Or so you say! The desperado from Christchurch and you are so desperate to convince us you have some investment properties and that the market is turning.

Fair enough, next time maybe explain that when you say less property on the market you actually mean less property of the small subset you are particularly interested in.

Auckland feeling quiet with low confidence.

It's pretty touch and go isn't it? Have we lost too many jobs / people / businesses for the economy to pull up? Is there a risk of an early 2025 slump back down again?

And, before anyone starts, yes, the housing market is our economy. If we are not increasing mortgage debt significantly each quarter (by around $5bn), then our economy will crash, jobs will evaporate, and we will be back in the mid-2024 doom loop. Every cog, pulley, and piston in our economy relies on private balance sheet expansion.

Until the government begins spending money again this doom loop will continue and I think it'll happen.... in the election year.

My personal view is that we are only halfway through this recession - but I’ve been wrong before - I just don’t see a path out of this until the current government wake up to the fact they need a massive stimulus program to get us out of this trend we are on - and that will take a political 180 and perhaps some significantly worse economic data to appear.

100 percent agree

you do realize stimulus means lower interest rates?

I think we have finally realized that the problem of our pile of maxxed out credit cards isn't to be solved by signing up to another one, but by sorting our shit out and starting to earn more as a country. Tho I have serious doubts of how successful we will be at this.

But hoping this government will kick the can and borrow and spend to allow us to consume our way to prosperity...thats just madness.

Pretty weird how the government gets compared to household when it needs to 'balance the books' and 'live within it's means'.

But many of those very same people suggest households should borrow to their tits, maximise leverage to buy a house to *checks notes* invest in their future.

The reality is that government borrowing per se is neither good or bad. It's what the borrowing is used to pay for. Tax cuts to landlords was a terrible thing to borrow for. Same with the massive gold-plated RONS.

New rail enabled ferries and a new hospital probably not too bad.

That's why Luxon is sinking in the polls. He is just really really bad at making the right calls.

To be clear, I am talking about NZ as a country. $1.30 of Imports for every $1 of exports. Keith Woodford had a good article on here recently about it. We have been constantly living beyond our means for far too long, selling our country off and borrowing from overseas to make up the shortfall. Just like a household that isn't sustainable, because ultimately our floating dollar devalues and interest on the accumulated debt will rise. That equals inflation and a much lower standard of living.

As you say agnostium, recent governments dont have a track record of borrowing for assets that actually pay their way. I think it will take a change of population mindset towards old fashioned ideals of work, thrift and efficiency before things even begin to turn around. It will probably take some form of crisis to get that mindset again.

"NZ as a country. $1.30 of Imports for every $1 of exports"

Fuel and vehicles are 28.5% of total imports and 8.4% of 2023 GDP. Note that the current account deficit to GDP ratio for 2023 was -6.9%.

New Zealand’s Top 10 Imports

The following product groups represent the highest dollar value in New Zealand’s import purchases during 2023. Also shown is the percentage share each product category represents in terms of overall imports into New Zealand.

- Mineral fuels including oil: US$7.3 billion (14.6% of total imports)

- Vehicles: $6.9 billion (13.9%)

- Machinery including computers: $6.8 billion (13.6%)

- Electrical machinery, equipment: $4.5 billion (9%)

- Optical, technical, medical apparatus: $1.7 billion (3.4%)

- Plastics, plastic articles: $1.6 billion (3.1%)

- Pharmaceuticals: $1.5 billion (3%)

- Aircraft, spacecraft: $1.1 billion (2.1%)

- Food industry waste, animal fodder: $886.1 million (1.8%)

- Articles of iron or steel: $868 million (1.7%)

New Zealand has had a current account deficit EVERY YEAR since at least 1981 (44 years). The smallest current account deficit was in 1988 when it was just -0.1% of GDP.

https://tradingeconomics.com/new-zealand/current-account-to-gdp

Agree.

Lower interest rates will only have a material stimulatory effect on the economy if they are sub 4% (retail rates not OCR). Possible but quite unlikely.

And given the government is being austere, the prognosis for the economy is poor

ignore the bank economist spruikers who say we will start seeing a moderate pick up In growth this year

As expected there was going to be a lot of hype and narrative around rate cuts and the summer selling season, but the data looks pretty weak so far. I am noticing some unsold stock reappearing as new listings this year but still dubious they will get the prices they are seeking, especially around Wellington with the job market. I have been to a couple of open homes recently and there does seem to be more people there, but it’s hard to know if that’s translating to sales. I expect it to continue to bobble up and down and then dive a bit further as it goes into winter. Without some kind of stimulus or policy to boost the market, it’s not looking like taking off anytime soon. It’s looking very much like the 70’s downturn still.

So there are over 60 empty, unsold, brand new townhouses within a few blocks of my home. How long do you think it will take the market to clear this stock? Asking for a friend.

KW, whoever the developer is of those units will not do too well, or deserves to .

Didnt do their homework as not too sure who their market for them being where they are floor plan.

At the end of the day the intelligent investors will do well snd the not so, will do poorly.

North Shore quartet up. 50% cut in Feb.

Probably waiting to hope inflation hides the real drop.

The crashing NZ property market looks so bad, when crystalized into the Council Valuations.....they will delay, delay and delay.

"When it's this bad, they just have to delay/lie"

I believe it will be an actual bigger screwup and show even larger property devaluations, as the sick NZ economy will ensure that values are again lower mid 2025 and end of 2025.

Leaving rates were they are is a blatant price gouge on Awklanders. To fund the largess of Council is the only reason its being delayed. Sack 20% of the do nothings and get on with reality. If they keep it up I would not be surprised to see a rates revolt.

RV has nothing to do with overall rate take. How many times does that very basic tenet need to be explained?

Amazing how people who are demonstrably ignorant about how council works are confident enough to stand up and spout shit about council employees being do nothings.

Yes Council rates increase every year, regardless of values up or down.

- Values just split the "always increase" somewhat proportionately.

I believe the Council know full well, that Aucklanders home values will show -15 to -25% declines since 2021 and the likely litigation volumes that this will bring on, scare them. All will still pay More Rates.

The Council need to grow a pair, send out the new valuations and let the cards fall where they lie.

The reason for the delay is the CV's have not taken into account that thousands of old houses have been fixed and upgraded after the floods/cyclones by insurance.

The person in charge has ordered that all those houses are identified and their CV's capital improvements values significantly increased to reflect the near new condition of the home following the insurance repairs.

Expect to see lots of bleating and pearl clutching in Granny Hearld from the folks that have essentially new houses (barring the framing and roof) following their insurance claims, thereby significantly increasing their rates bill.

In August 2021 Wanaka got down to 100 listings on Trademe. Right now it's 365 and rising.

Yep. Gotta say Lakes have avoided financial reality for a while, mainly due to Aussie, Overseas, and cashed up boomers. Reality will hit there. Aussie is having increased bankruptcy and boomers are struggling to cash out in other "crashing" parts of NZ. If constructions stop in Wanaka then circa 40% of everyone living there with a mortgage will have to leave as there is no other regular work there.

See what happens.

Also I know this is just one property but the below sold for $1.2m in December and the Homes.co.nz valuation this month is $1.64m. The neighboring properties are all the same build and two are for sale and have similar valuations on homes...

https://homes.co.nz/address/wanaka/7-meadowbrook-place/j4V75

"The neighboring properties are all the same build and two are for sale and have similar valuations on homes..."

FYI,

Homes.co.nz criticised for allowing estate agents to influence price estimates

https://www.stuff.co.nz/business/127537672/homesconz-criticised-for-all…

Ok but in this case shouldn't a sale of $1.2m adjust the value of it to that sales price? Then if there are properties exactly the same next door, they should also be adjusted to a similar value.

The current value on homes is 37% higher than it sold in December as stated on their site.

"but in this case shouldn't a sale of $1.2m adjust the value of it to that sales price? "

In other valuation websites, it should have an impact.

However on homes.co.nz, real estate agents may be attempting to influence potential buyer expectations of "market value". After all, there is a percentage of sale price commission earning sales person with a vested financial self interest involved here - the higher the price, the higher their commission.

Seen many valuations on homes.co.nz rise rapidly just before the property is listed for sale.

Well if that's what they are doing it's pretty obvious that something is very amiss here.

Last time I checked late Nov/early Dec, Homes was overvaluing properties by around 15%.

You could see, even when houses were sold the estimate stayed up, sometimes up to 30% above the sale price. Sometimes the estimate was up to 20% above the actual asking price. The real estate agents delay uploading houses that fetch low prices as they are then missed out from the algorithm when it re-baselines. Plus as CN says the real estate agent can put whatever estimate they want in, they keep it high to make people think they are getting bargain.

It's like Kathmandu sale prices, the sale price is the actual price, every now and again a NZ sucker or foreigner comes along who doesn't understand the pricing and pays the label price.

Property developers, property promoters and real estate agents in the current environment can be summed up in this one line:

https://youtu.be/wYlptbR0Dkw?t=22

CAVEAT EMPTOR

My daughter bought a home a couple of years ago where we live. The agent changed the existing estimated value on Homes from $1.7m or so to $1.95m when listing it. A sucker offered the asking price subject to selling an Auckland home which of course didn’t sell. The deal fell over and the agent came back to my daughter who paid a little over $1.7m for it. The agent changed the value on Homes back to the price my daughter paid for it. Talk about smoke and mirrors.

Wow, so many new listings coming on now in Auckland - add that to the record high existing listings which means ....

The tsunami of three years of pent-up vendors is starting to flow. BRACE BRACE BRACE

Wow, they obviously needed the extra day or two to create that Bullshit spin!!!!!

I take as much from that release as the first Poll of the year that puts hippy back in...

Subdued sales should be seen in context.

Basically, looking at Auckland, sales in 2020-22 (36 months) averaged 5,344 pcm

In 2017-19 (36 months) pcm average was 3,027.

That massive surge has to equate to a massive under-performance in order to revert to the mean.

Sales pcm in 2023-24 (24 months) averaged 2662 pcm

As anyone fair will acknowledge, the 2020-22 sales were based on a pipedream of eternal low rates. That will not repeat.

In addition, always left out of account is that the pop of Auckland has risen about 350,000 since 2018. Stats NZ don't do a very good job of estimating pop and housing stock in Auckland. However, it has to be acknowledged that a metric which showed sales per 50k of pop would give a more rounded picture. It is inaccurate and misleading to continue comparing sales over time if the denominator, in terms of total houses in an area, is also not updated periodically.

Auckland sales peaked in about 2004, when the pop was probably a good 500k lower than now.

Price rises are not good except for cap gains, not the "market."

A 40% rise in 2020-22 following the 29% rise in 2016, simply excludes more people from capacity to afford to buy. It also means that unless you have two earners on over $100k, you cannot buy without parental help. And if you do, the couple cannot afford for one to go off on maternity leave for 2-3 years.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.