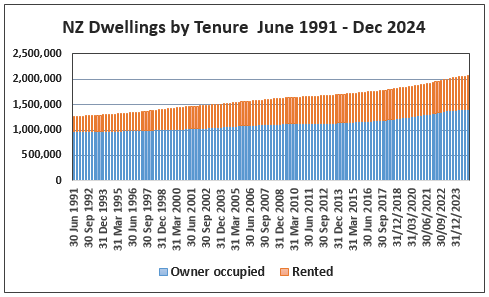

The number of owner-occupied dwellings was at a record high at the end of last year, although the overall rate of home ownership in this country is declining.

The latest housing tenure estimates from Statistics NZ (based on 2023 Census data) show that there were 2,027,700 dwellings throughout the country in the fourth quarter of last year, of which 1,354,500 (66.8%) were owner-occupied and 635,600 (31.3%) were rented - the figures do not add up to 100% because they exclude certain types of dwellings such as hostels and motor homes.

All three figures were at record highs at the end of last year but rented properties have been increasing at a faster rate than owner-occupied ones.

The percentage of rented properties has increased for seven consecutive quarters, from 30.7% in Q1 2023, to 31.3% in Q4 2024.

Conversely, the percentage of owner-occupied dwellings has declined over the same period, from 67.5% in Q1 2023 to 66.8% in Q4 2024.

Although recent changes in home ownership levels have tended to be small, with a slow reduction over time, the changes have been more dramatic over longer time frames.

The Statistics NZ data goes back to Q1 1991, when 73.8% of dwellings in this country were owner-occupied and just 22.9% were rented.

So although total housing stock has increased substantially over the period, most of that growth has come from rental properties - as shown in the tenure graph below.

The comment stream on this article is now closed.

53 Comments

It's such a pity... and people wonder why folks are leaving this country..

Housing is a curse for many, so if country were to change for the better, Housing has to be a focus from the government...

Housing has been a focus for this government. That's how they got elected. i.e. Tax cuts for landlords.

And you want more for landlords? Seriously?

Nat has a cat in hell chance of being re-elected.

Labour will simply need to be the other party. Nats have done nothing but the tax cuts and spending cuts... which have just made everything worse.

Geez, forest ,have you heard about inflation.

Most of that increase was covid printing party.

Had to end some time. Buckle up x get real ffs.

There’s going to be a lot of tears when Lux becomes a two term PM.

Why build housing , no return.

Christine, go for it yourself

Its a curse worldwide.

Get off your play station. Ffs

Joker, get off the drugs and your mind straight

Unnecessary assertion from you Dgm

The trend is not good. However, there has been a huge increase in retirement homes ( which are not in fee simple ) and I wonder if the statistics are skewed because of this phenomenon. Older people sell their house and buy a right to occupy. How is that reflected in the statistics ?

rented properties have been increasing at a faster rate than owner-occupied ones.

Its all those Kiwis leaving for Australia and renting their houses out while "waiting for prices to recover" so they can sell them.

Kw, if they think that the grass is greener in Oz and they will buy a cheaper home in the cities, then they are going to be out of luck.

Prices are far more expensive in Oz, and they are competing with so many more and immigrants pooling their money.

I will give you the tip, that Chch remains one of the best places to live and housing is still very affordable and opportunities are good.

Of the Aus cities, only Sydney has a higher median price than Auckland

Auckland is not the only place to live in NZ, and is overpriced.

It now is not a nice place to live, I hear it all the time from people who have got out and moved to ChCh.

Median house price in Melbourne is $774k - and falling.

https://propertyupdate.com.au/the-latest-median-property-prices-in-aust…

You would be wrong, have you seen the size of Melbourne ? People are hours away from the CDB its like including Hamilton and everything way outside of it into the prices. Houses are way more expensive in Australia for the places people actually want to live in.

That's just incorrect. I'm an Aussie and we sold a nice 4 bed house 9km from the Melbourne CBD when we moved to Tauranga in 2016. I then had to pay more for a 3 bed house of similar quality in Tauranga. Our household income was cut in half in NZ. Australia is a big country, with huge amounts of opportunity in every region in every state. Pay is better. The standard of living is better. The health system is superior etc. Superannuation system is far better. There's better beaches and more of them. NZ is a great place to live, but this myth that it is better than Australia is just garbage.

I'm a bit confused, why are you still living here and why is the second largest group of people coming to NZ to live Australians ? Maybe Tauranga is not so bad after all, personally I love it here. The only thing better in Melbourne was the vineyard tours, otherwise its just another city where it gets both too hot and too cold.

We live in NZ for family reasons. I agree with you, Tauranga is a nice place, but there's plenty of places in Australia that are just as nice as Tauranga, with cheaper housing options, better paying jobs etc. I'm sure there's plenty of people moving to NZ from Australia, but in my line of work, I know of 10 young tradesman that left for Australia in 2024. All of them now earning more than double what they were here for less hours per week, some even triple for remote work. These young guys/girls leave, and their companies employ foreign workers to fill the gaps. These young people are getting opportunities in Australia that just don't exist here. Why would you stay in NZ when you can earn double for the same qualification a couple of hours away?

that's median price, not median HOUSE price as you suggest. That's Melbourne's feature , it has a lot of apartments/units.

From the same table Sydney's price is $1,191,955 - if you believe you can buy a house in Sydney for that price then lol, please stay where you are. Maybe somewhere starting from NZD1.8M ?

Trust me, you can buy a house in Melbourne for 774k but that would be the area where you would not feel like you are anywhere near to Melbourne. However it is a lot of houses in that range and it is good, people can live in the house even though it is 25-35km away from CBD (e.g. Point Cook)

Additionally you would need to factor in things like Estate Body Corp Fees which plenty remote locations have , Stamp Duty, AUD3000 of title transfer govt fee on top of conveyancer and the fact that this is actually all priced in AUD (which is already 10% more expensive).

So your AUD774k can be easily seen as NZD902k so keep that in mind

Question is , can you buy 4x2 newbuilt house on 400 sq.m lot for 902k in the most remote parts of Manukau City? If the answer is yes than no point moving to Mel from Auckland. If no , welcome to Melbourne then !

"I will give you the tip, that Chch remains one of the best places to live and housing is still very affordable and opportunities are good."

Owner occupier buyers: there may be an undisclosed potential conflict of interest, and undisclosed vested financial self interest here.

CAVEAT EMPTOR

In plain english, the guy is a self interested fraud and making up a narrative for Chch to pump his deflating assets.

Ignore this clown.

Not a fraud at all.

Just need to have perspective and too many going on about Auckland market.

I point out that it is still possible for people to buy owner occupied and investment property in NZ

Your weather in Christchurch is terrible. A good reason why so many live in Auckland and very happily. Christchurch will always come second in terms of opportunities and popularity.

Weather certainly not flash for Summer this year!

Just shows you that this Global Warming is just scaremongering and a scam like Covid is.

Auckland is not like it used to be, that is all you hear from people coming South for a better lifestyle.

Just shows you that this Global Warming is just scaremongering and a scam like Covid is.

Tell me, is the Earth flat?

That is rich for someone coming from an isolated weather hit city destroyed by earthquakes and where another big quake could happen any time. I do not live in Auckland and never have but give me it’s better weather, its opportunities and it’s harbour every time over poor old Christchurch. Yes the weather is not like it used to be. I agree with you that climate change and covid are very real.

Not sure I need any more opportunities?

What I do know is that what we do in Chch would not work as well for us in Auckland.

Just do not like the way Auckland has deteriorated over the past decade, but each to their own.

Suppose it depends on what sort of financial independence and lifestyle you want.

To be fair the earthquakes in Chch have made people a lot of money and have provided opportunities.

Chch no thanks.

Keep spruiking Chch, while many leave to rent overseas and end up with far more in their pocket at the end of the week. Buying a house isn't the be all end all of life, but it would be beneficial for more to have the opportunity in NZ to do so at a reasonable price to income ratio as has been on offer until pre-2020. You don't even need to think the grass is greener there, you just need to do the math on the level of disposable income you'll be able to save and/or invest compared to the same job in NZ

K.W. : "Its all those Kiwis leaving for Australia and renting their houses out while ..."

Got facts for that? No? Sorry. I have no time for your reckonecomics.

There are a number of non owner occupier residential property syndicates operating to combine their financial resources to increase their buying power (and borrowing power) to outbid owner occupier buyers in the existing residential real estate market. (Remember, non owner occupier buyers are able to borrow up to 7x DTI vs 6x DTI for an owner occupier buyer)

To maximise the cashflow from the non owner occupier residential property, it has got to the point where these non owner occupiers are:

1) renting out residential dwellings on a room by room basis (rather than the entire dwelling to one tenant such as a family) in order to maximise the cashflow

2) renting out on Airbnb / Book a bach - though some changes on the Airbnb platform may now have reduced revenues and made this less financially attractive than renting out in the long term rental market.

3) adding rooms to rent out

4) adding other dwellings on the property to rent out.

This has been the impact of re-introduction of interest deductibility for non owner occupiers in the EXISTING residential dwelling market. Some non owner occupier owners are willing to go into negative cashflow for the potential untaxed long term capital gains (i.e after 2 year brightline test which was reduced from 10 years)

The buying advantages of non owner occupiers over owner occupier buyers in the EXISTING residential real estate market:

1) 100% financed purchases of residential real estate (due to equity release / deposit recycling techniques)

2) interest only financing

3) interest deductibility

4) combined buying power of residential property buying syndicates

5) 7x DTI vs 6x DTI for an owner occupier buyer

Owner occupier buyers (especially first home buyers in Auckland without assistance from or access to the bank of mum and dad, and an inability to take on "boarders" or rent out a room on Airbnb) are unable to compete with those buying advantages given to non owner occupier buyers.

Here is a comment on a Facebook group from an owner occupier buyer who was outbid by a non owner occupier:

"Annoying else dealing with this??? It’s so disheartening trying to buy something as a single mum when everything is getting snapped up by investors!! Sold 2 weeks ago, and straight up for rent

The rich just getting richer and those like me still struggling and saving as much as possible to even have a chance at getting a home of my own"

And yet, there are plenty of unsold brand new townhouses languishing on the market just waiting for someone, anyone, to make an offer on them. 60 of them in my immediate neighbourhood alone. So its unlikely investors are crowding out home buyers, when there is soooooo much unsold stock out there.

Those townhouses are available for a reason. Asking price is unrealistic. You're basically saying they should just buy the worst available option or not complain.

"there are plenty of unsold brand new townhouses languishing on the market just waiting for someone, anyone, to make an offer on them. 60 of them in my immediate neighbourhood alone"

I suspect developers are reluctant to lower the price as it will impact their profit margins. How long can these developers and builders hold on without sales, revenues and hence cashflow? A key determinant will be continued access to funding, particularly lenders - banks and non banks, and other sources of funding to keep the business alive - family, friends, investors, etc

Lower the price and there will be buyers. At a price of $1.00, there are buyers out there.

These properties may not suit the needs of owner occupiers - size, number of bedrooms, location, car parking needs, access to school areas, price point, proximity and access to work, etc.

It seems that these townhouses were built for non owner occupier buyers, rather than owner occupiers.

One common comment is that since interest deductibility is being reintroduced on EXISTING dwellings, new townhouses are less financially attractive.

Some stock no good, no parking, too tight to neighbours., 3 level. Noisy. Going to be dogs breakfast in a few years.

you have misunderstood the limitations for home owners and investors.

for home owners, income, or DTI is more of a limitation.

for investors it's the equity, or LVR that is more of a limitation.

"for investors it's the equity, or LVR that is more of a limitation. "

Yes for those that were at or near maximum LVR limits at the peak house price and house prices falling from peak. For those that had low LVR's at the house price peak, they will have untapped borrowing capacity and have continued ability to buy - the question is how many of these buyers are out there under current conditions?

Huttman: "for investors it's the equity, or LVR that is more of a limitation."

So you're saying the RBNZ has got their ratios wrong again?

I suspect your are bang on the money.

So who benefits? Could it be the landed rentiers second ... with the big Aussie banks the primary recipients? Golly ... I think you may be right. (But what do I know, ay?)

that is not what I was saying at all.

what I was saying is, there are limiting measures and controls by design, and they are different for home owners and investors.

Was it not late last year that it was reported that home ownership was rising?

Indeed. RNZ also reported on 5 October 2024 that it was the first lift in home ownership recorded since 1991 - 66 percent of households are homeowners, up from 64.5 percent in 2018.

The latest figures have been adjusted to incorporate data from the 2023 Census.

Governments come and go but the percentage of rentals continue to gradually grow. The same is happening in many other countries also. The silly thing is many governments in NZ plus those places we copy laws from like UK and Australia have been passing laws to make it harder to provide rental homes. Things like stamp duty, congestion charging, lending rules, and tenancy laws. All these poorly thought out impediments just help to push up rents and this traps even more people into being tenants for life.

Willful blindness.

MY RECENT RANT - IN THE YEAR 2025

INTRO - Warning, this is not uplifting, and not the least because of the completely new global financial territory where the U$ is losing its reserve currency status - also the fact that it will begin to lose its default currency status as well, as the true state of the economy and its currency is gradually revealed.

As the default status dissolves we will witness a currency failing upwards, before it finally reveals its true value. It will appear to be strong but only in regard to the other fiats which are all heading in the same direction, just at different velocities.

A cursory periodic glance at the 'rock relic' that has been an accurate measure of goods and services for some 5000 years will tell us how far gone they are - hint - all of them have lost more than 99% of their purchasing power - the remarkable thing is just how short that timeframe has been - until you find out how pitiful the average life span of fiats has been - more on that later.

Add to this the dozens of geopolitical flashpoints across the entire planet, and I would throw out 90% of the graphs and charts that we routinely use to make our forecasts and accept the fact that we are experiencing a brand-new global financial paradigm and entering uncharted territory.

So too the fact that the eCONomic mysticism is being exposed as the mother of all crocks, that all fiat currencies are in their inevitable debt-death final phase, that interest rate manipulation as an effective monetary tool for the control of inflation is being finally shown up as utterly farcical, and we have the makings of the mother of all shambolic years.

BRICS - this factor alone challenges all of the old rules

Note that Indonesia just signed up to BRICS and the list of countries has become so long that they have had to suspend applications to enable them to process the prospective members. Just to add to the volatile geopolitical mix, Brazil (the 'B' in BRICS) is also under attack by the Western financial/military hegemon which desperately wants to maintain its unipolar hold on humanity.

https://globalsouth.co/2025/01/13/brics-under-attack-in-brazil/

SOME PERSONAL OBSERVATIONS

#1 The latest U$ job reports point to a FIRE (Financial, Insurance, Real Estate) based economy in continual decline with the latest employment data showing jobs in manufacturing and construction flat, with most of the growth in service, retail, and govt. employment. The UE data has to be taken with a sack of salt anyway given that multiple part-time jobs are lumped in, plus people no longer looking for jobs and as such are not included in the data either.

#2 Two months into the latest U$ fiscal year (beginning Oct 1, 2024) shows a $624 billion fiscal deficit, which could run out to anywhere from a $2 - $3.7 trillion deficit by fiscal year's end.

#3 Will DOGE be able to trim Federal spending to even match the negative offset in revenue received from a floundering economy? - I doubt this very much. This strategy has been estimated to knock out around $2 trillion in GDP, or around 7% - but they were calling for a 3% growth rate before this idea - this nets out to a dismal negative nominal 4%.

#4 There are huge unrealised losses not shown on the bank's balance sheets because they loaded up on Treasuries and mortgage-backed securities when rates were 1-2% and now with rates at 4-5% they are trading at under 1% (down to 70-80 cents on the dollar). They will mature at par - but this is a gut punch because real inflation is at least 10% meaning these assets are losing value at a compounding -9% annually.

#5 As I see it, Dah Fed has only two options - (how would you like to die?) -

(i) Fire up the printing press like crazy and KILL THE DOLLAR.

It's 99% gone anyway - why not go for broke - this is historically the choice that those in the hot seat make.

A very simple calculation is to look at the price of gold in 1971, just before the U$ went off the gold standard - a 40 oz bar of gold cost $11,000. Around the year 2000 it was up to around $100k, and today at say $2,600/oz it comes to ~ $1.1 million for the same bar.

That, as near as damn is to swearing, amounts to a loss of 99% of its purchasing power in 53 years. Incidentally, as I have mentioned on this forum before, the average lifespan of all fiat currencies in history is only 35 years - it appears that king-dollar is already 18 years overdue for the great fall off the wall.

(ii) Cut back on everything, tighten the screws and KILL THE ECONOMY even faster - normally not the option chosen as the politicians don't want the implosion on their watch.

#6 As I see it, the risk-weighted organic direction for global interest rates, regardless of what tricks dah Fed and other CBs try, is upwards. That said, I cannot see IRs reaching the 7-10% territory without the entire fiat casino coming down like a house of cards - let alone even remotely approaching the territory during the Paul Volker debacle when the prime rate peaked at a mind-numbing 21.5% in 1981.

A MAJOR CAVEAT FOR #6 - IR manipulation as a monetary tool is a complete crock anyway - it is a sleight of hand designed to thieve from the real economy and to continually transfer wealth to the rentier* sector.

*(The term “rentier” refers to an economic agent or individual who primarily earns income through interest, dividends, and other financial returns from investments, rather than from labour or entrepreneurial activities. This class of income is often termed “unearned income” since it does not arise directly from productive work or business endeavours.)

IR (Interest Rate) hikes are directly and immediately inflationary, just as hikes in energy prices are too. Indeed it is completely farcical to even suggest that they could ever be an inflationary control tool - they are the 180˚ polar opposite of what they are dressed up as.

Historically, with the incorporation of the constitutionally illegal U$ Federal Reserve model, it became the precursor for the central planners to expand their theft from Mainstreet on a grand scale - all the while, the key private banking baron culprits remained ensconced behind the scenes as the puppet masters, busily tugging on the strings, and aided by all manner of smoke and mirrors.

The Fed is one of three 100% privately owned banks on the planet - the other two being Italy and South Africa. A private cartel monopoly ownership is the perfect model to enable the theft of a nation's wealth by a tiny group of plutocrats - as the trite saying goes - "the easiest way to rob a bank is to own it" - also, being their own in-house regulators, plus not being audited since 1953, makes this about as easy as stealing candy from a baby in a pram.

This coup was all about centralising money creation, but it was sold to Congress on the basis of the Fed being the mechanism that could step in and save banks in the event of a run on deposits. They did exactly the opposite, and in the 1930s, as a direct result of the pump-and-dump debacle that they themselves had orchestrated, there was a huge attrition of small banks, and of course, along with them the liquidity they provided for the real economy, and especially the rural sector.

The Fed sat on their hands and let these banks go under, whilst their biggest member banks gobbled them up for a pittance, and the depositors (read unsecured creditors) lost all their money. Worse still, the farmers were made to repay their loans to the big banks or forfeit their farms. This in turn, led to a massive plummet in agricultural production and abject starvation for much of the vulnerable sectors of the economy.

This was a huge coordinated land grab - precisely what they are gearing up for right now - the DTCC, and Cede & Co. wait in the wings like vultures hovering overhead for the next big land grab.

"The Great Taking", a very concise free PDF (in the link below), explains what they have in store for those of us who fancy that we own paper assets and mortgaged real estate.

WE DON'T - we are the last in line unsecured creditors - how is that going to pan out when the total nominal value of derivatives is between $2.5 - $3.7 quadrillion. In fact, we are merely discretionary beneficiaries in a giant shadowy trust set up without our knowledge - the 'T' in the DTCC acronym gives that away - it designates the word 'Trust'.

'Cede' means to surrender possession - TPTB love to taunt us with word games and labels on one hand, as they thieve from us with the other.

https://thegreattaking.com/read-online-or-download

Back to the global derivative debacle - IOWs it is 26 - 40 times the annual global nominal GDP. What makes this even worse is the fact that a huge chunk of the nominal GDP figure should never have been included in the calculation in the first place.

National income accounting (GDP tripe) harks back to the late 1600s when a couple of Dutch bankers ran the numbers in time for the launch of the Bank of England in 1694, and to try to arrive at a figure where govt. debt obligations could be reconciled accordingly - the system appears to be some 330 years out of date - time for an update perhaps?

Some of the individual bank's derivative books are outrageous too - from memory, Goldman Sachs about a year ago was roughly 1200:1 (Derivatives:Equity) - with Citigroup (the largest shareholder at over 40% of the New York Fed), a whopping 330:1.

#7 The more banking is centralised and the local community banks are restricted by regulation, the more money creation flows into asset portfolios - IOW existing assets, rather than Mainstreet's entrepreneurial sector, which is the engine of activities and sustainable societal wealth. Generally, within the status quo financial system, banks are in effect penalised if they lend for productive business purposes - this involves following the Basel, (Swiss-based) BIS (Bank for International Settlements) - NZ is one of the 62 member-bank affiliates.

As I have said before ~97% of money is created by these banks (NZ has a pitifully small number of banking entities) and is devoid of any window guidance whatsoever as to where the available liquidity is placed.

When banks lend there are 3 main scenarios...

(i) When this money is used for consumption it naturally leads to consumer price inflation because it adds to the money supply, but not to the supply of goods and services - more demand chases the same fixed supply of G & S (Goods and Services).

(ii) When this money is used for financial and asset purchases it leads to asset price inflation, with extreme examples like the Japan property bubble of the 1980s that ended up bursting spectacularly and only very recently regained the market cap ground that it had lost 30-something years earlier.

(iii) If banks conduct adequate due diligence in their lending for productive purposes, this by definition creates more G & S, creating sustainable income flows for the borrower to both service and repay the loans.

In an economy that has many banks, that are also backed up by non-banks making loans for productive purposes, then economies could be looking at sustainable real growth of 10-20% as opposed to low single-digit growth or even negative nominal growth, let alone growth that is inflation adjusted.

= LEADING TO MINIMAL CPI INFLATION OR ASSET PRICE INFLATION

Case in point - the EU - the ECB has killed off some 5000 banking entities in the last 20 years. However, the appointed (read unelected) financial European Commission executive, shills for the global financial plutocracy, and this situation can never be addressed without massive fundamental political reform.

Conversely, under the U$ Federation's Governance System, where individual states have constitutional monetary and fiscal policy autonomy, with a modicum of common sense this can be readily achieved.

In fact, from small beginnings with just one solitary, but spectacularly successful model - the 105-year-old Bank of North Dakota, we now see ~35 states moving towards implementing sound money, state depositories and Public Banking Solutions (PBS), so that they can begin to protect their locally generated wealth, and insulate themselves from the profligate federal financial casino.

With this number of states wanting to insulate themselves from the suicidal Federal govt's. 'policies' it kind of beggars belief that any Canadian, with more than half a brain, would even entertain the idea of their resource-rich country becoming the 51st U$ state.

I wonder (sarc) if the sales package includes the disclosure that the average U$ taxpaying citizen, when you include unfunded liabilities, has a total debt burden of between $1 and $2 million dollars? On the contrary, many U$ states are talking more and more openly about secession.

SUMMARY

The only certainty for me in 2025 predictions is that the year will be a hats-off wild ride - barely two weeks in and the geopolitical uncertainties compound on a daily basis, to the stage where it is very difficult to keep up. For the life of me, I cannot see us getting to the end of 2025 without a systemic financial meltdown.

Both the EU and NATO are now toast, particularly with Germany being rendered an uncompetitive industrial cot-case by its occupier - the one that also severed its energy umbilical cord from Russia. Theoretically, if the population can lift itself out of its current terminal case of Stockholm Syndrome, vote in a government that is devoid of an economic death wish, and begin looking East and South, not West, there might be a faint chance of some degree of modest recovery, otherwise, IMO Germany is gone for all money.

The two next biggest EU economies are France and Italy and they have monumental financial challenges too.

In the meantime I will be looking closely at the big European G-SIB institutions and their equity positions - these include HSBC/Barclays/Credit Agricole/Deutsche Bank/Groupe BCPE/UBS/ING/Societe Generale/Standard Chartered/etc.

A liquidity event in any one of those giant institutions could trigger a global domino effect, especially as the derivative positions unwind like a broken spring in a worn-out builder's tape measure.

Europe is the birthplace of the global private banking con - it may well turn out to be its nemesis too - poetic justice perhaps?

The scenes remain familiar - from Rome and Venice to Holland, Basel, the City of London, and the long shadow cast by the 'Old Lady of Threadneedle Street' - fascinating - a play that spans more than 300 years lurching into its final act - black comedy drenched in the blood of impending financial carnage.

Colin Maxwell

'The Federal Reserve is not a private institution ,it was created by Congress, operates under federal oversight, and serves a public mandate to ensure economic stability. Member banks are required by law to hold shares in their regional Federal Reserve Banks but these shares do not grant ownership rights or control. The Fed’s policies are set by a publicly appointed Board of Governors, and the majority of its profits are returned to the U.S. Treasury, affirming its public nature'.

Which part of dah Fed being a tool of a thieving private cartel do you not get, Rastus?

... quoted...

"When the next megabank blows up from its derivative exposure, you can add the names Jamie Dimon and Patrick McHenry to former Republican Congressmen Randy Hultgren and Kevin Yoder as four of the men who greased the skids for another derivatives banking crisis.

https://wallstreetonparade.com/2024/09/the-fed-just-kicked-the-capital-…

https://wallstreetonparade.com/2021/07/after-jpmorgan-chase-admits-to-i…

https://wallstreetonparade.com/2017/02/wall-street-banks-are-trading-in…

https://wallstreetonparade.com/2014/06/citigroup%e2%80%99s-dark-pools-h…

Your 'quote' is equally as intriguing as the reason for your defence of this completely unconstitutional racketeering crock that has been thieving from Mainstreet for 111 years.

Tell me, do you happen to have a source for this 'quote', Rastus?

Never mind, because I do - a DDG search located it in about 5 seconds - and guess what - it's turns out to be a butchered rehash of dah Fed's standard shite that it uses to obfuscate FAQs on its own website !!!...

Who owns the Federal Reserve?

"The Federal Reserve System is not "owned" by anyone. The Federal Reserve was created in 1913 by the Federal Reserve Act to serve as the nation's central bank. The Board of Governors in Washington, D.C., is an agency of the federal government and reports to and is directly accountable to the Congress."

Rehashed from ... https://www.federalreserve.gov/faqs/about_14986.htm

Honestly, Rastus - is this all you have?

That's what they tell you to believe.

That was a long read but it sounds like you said, it's not a silly idea to have a small allocation of bitcoin which is not owned or controlled by any one party and has no counter party risk. Not financial advice, you do you. Everyone else keep arranging the deckchairs and listening to the music. A debt based economy with fractional reserve can only go one way. It’s literally history, roman empire, coin clipping, gold\silver dilution etc.

This whole ‘rentier’/unearned income thing is BS, it’s designed to distract and divide, if you put money in the bank and get interest on it, that’s unearned, so that’s bad eh! You are being conditioned to think like that. think about it, isn’t the whole goal to be able to retire with some money coming in to cover your living expenses, is that evil? If so anyone with a KiwiSaver is evil, because you are getting unearned income from the shares that it’s invested in, that’s even less work than a landlord, shock horror!

Of course the boomers have all the money, it takes a lifetime to payoff a mortgage and acquire savings, and a whole lot of luck. I’m not saying it’s not getting harder for each generation, but compound interest takes most of a lifetime to gain momentum so lets try and keep some perspective.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.