The kiwi dream of moving on up the property ladder remains well within reach for those people who have been able to haul themselves up onto the ladder's difficult first rung.

Interest.co.nz's Home Loan Affordability Report is well known for tracking how affordable (or not) the dream of home ownership is for first home buyers throughout the country.

Interest.co.nz also tracks how well placed first home buyers who purchased their first home 10 years ago would be to take the next step and buy a more expensive home now.

The results suggest the housing market has been very kind to those first home buyers, even with the difficulties that have plagued the market in the second half of the last decade.

Those first home buyers should have built up a significant amount of equity in their first home, enough for a substantial deposit on their next home. And the mortgage payments on that should take up less than a quarter of their current after-tax pay, provided they are earning at least average wages.

Which means moving out of that first home and onwards and upwards into their next home should be well within their reach.

This is how those numbers look.

Ten years ago in September 2014, the Real Estate Institute of New Zealand's national lower quartile selling price was $279,500.

At that time, the average of the the two year fixed rates charged by the major banks was 6.13%, and if the home had been purchased with a 10% deposit, the weekly mortgage payments would have been $399 a week.

That would have eaten up about 27% of a typical first home buying couples' take home pay, assuming they were earning the median rate of pay for couples aged 25-29.

So 10 years ago, home ownership was a pretty affordable proposition, even for people on average wages, although things were just starting to get tight for first home buyers looking to buy in Auckland with a low deposit.

Ten years on, in September 2024, and the REINZ's national lower quartile price has increased to $595,000.

If the home was resold at that price, it would leave its first home owners with net equity of around $369,942, after they had repaid the outstanding mortgage and paid agency commission on the sale.

That's $90,442 more than they originally paid for the house.

If they put all of that equity towards the purchase of another house at the September 2024 national median price of $781,000, it would mean they would be buying it with a cash deposit of 47%. So no low equity fees for them.

The mortgage payments on that would be $562 a week, and because the former first home buyers are now 10 years older and hopefully wiser, they would also likely be better paid.

That means the mortgage payments on their new home would probably take up just 24% of their take home pay, if they were earning the median rates of pay for 35-39 year-olds, making it a very affordable proposition.

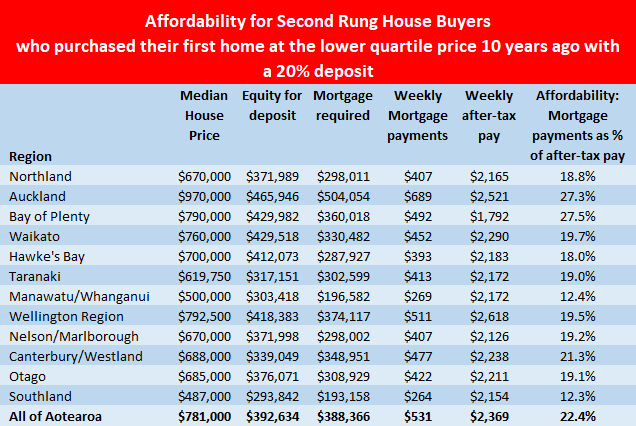

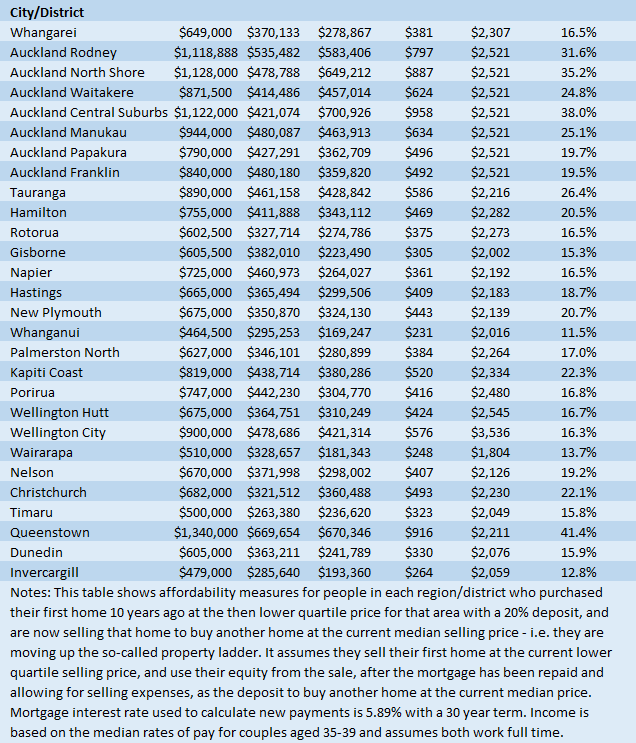

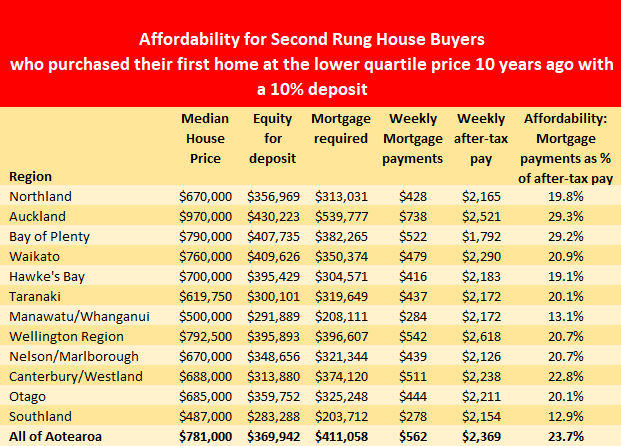

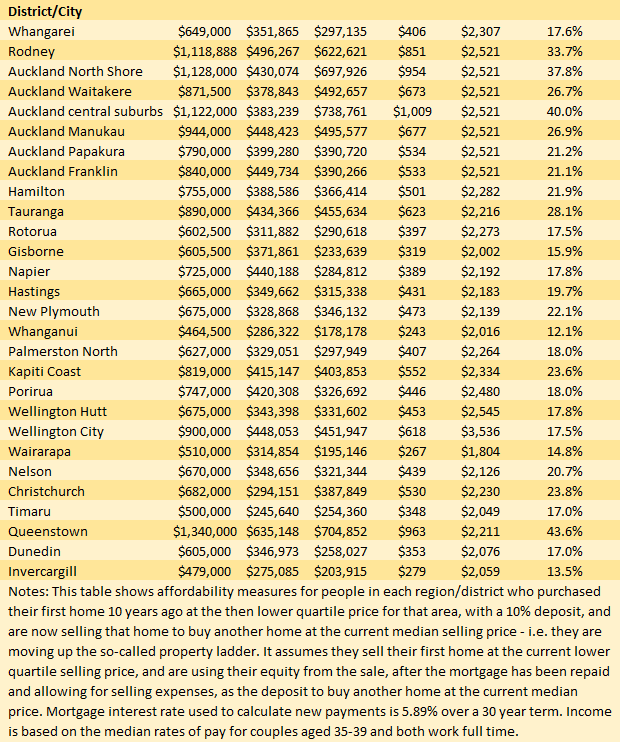

The two sets of tables below show the main regional and district affordability measures for first home buyers of 10 years ago looking to jump up into their next home, depending on whether they originally purchased that first home with a 10% or 20% deposit.

They show that the only place that typical first home buyers would struggle to move up the property ladder after 10 years is Queenstown, which claims the title of having the country's most unaffordable housing.

However, there are a couple of points worth noting in the figures.

They assume the first home buyers did not top up their original mortgage.

If they did, they would have less equity to put towards a deposit on their next home and the mortgage payments on it would be higher.

It also assumes they have not made lump sum payments on their mortgage, or otherwise altered its terms.

However, while the first home buyers of today may be facing a struggle to get into a home of their own, those who took the plunge 10 years ago should now be sitting pretty.

The comment stream on this article is now closed.

You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

100 Comments

It'll be interesting to see the same comparison for 2021 vs 2031. I can wait.

What strikes me is that the difference in commitments for moving "up the ladder" is very similar regardless of the deposit laid down 10 years earlier.

Those in a hurry to buy, I think should consider this. It speaks volumes when the capital gain hungry react angrily to suggestions that FHB’s take the time to patiently mitigate personal financial risks associated with owning property today before buying. It’s nothing more than an agenda to spread fear – the fear of missing out. As others suggest this glut of unsold overpriced homes is about to run out, they say, “FHB’s should shrug off thoughts of personal financial risks, rush out and snap up a house before it’s too late. Yet - somehow, despite still stretched fundamentals and rising job insecurity, they say house prices are poised to sustainably rocket higher at a rate far beyond one’s ability to save a substantial deposit. All these insightful revelations are simply based on cheaper money. The truth is that the market remains highly speculative, over-valued and vulnerable to risks on multiple fronts. A growing number of people are waiting on the sidelines for the first sign of real strength so they can relist. Note: 3000 unsold listings a month are currently being withdrawn due to ongoing market weakness - here. Why shouldn’t FHB’s seriously consider if they’re fodder to the many bag holders who are desperate for a financially dignified exit?

Becoming an owner occupier should be a life changing decision for all the right reasons. Steer clear of anyone who says you should hurry as they are more than likely suffering Emotional Dysregulation.

Houses are for living in and not speculating on. As a country, the longer this asset class is pumped as a pathway to growth and prosperity, only increases the likelihood of tears.

Becoming an owner occupier should be a life changing decision for all the right reasons. Steer clear of anyone who says you should hurry as they are more than likely suffering Emotional Dysregulation.

Or they've just seen repeatedly the outcomes from people who've talked themselves into thinking things will get any easier.

Houses are for living in and not speculating on

That costs money. Less of a problem if we're talking about a blender or new pair of shoes, but when you're up for the reality of decades of investment and commitment, and a working career that gets shorter each time the sun comes up, you can't be as complacent.

Curious phrases you use there, RP.

"Fodder" for "bag holders" who are "desperate" for a "financially dignified exit".

The article shows that first home buyers made a good choice in 2014 to purchase a home. However, if you go back to 2014 the market (particularly Auckland) was considered overpriced, and no doubt many people such as yourself whould have been telling people "don't buy now".

telling people "don't buy now".

Wrong, I'm not saying that at all.

Each night, Retired-Poppy goes to bed and dreams about ownership of an avocado.

TTP

You had been saying big crashes coming, just wait for a while.

Now you're saying what, the economy doesn't stack up and things look bad?

If we wanted to believe that was a certainty that'd happen tomorrow, probably begs the question about why so many of us bothered to get up and work today.

Financially speaking, the more time invested in the preparatory stage greatly increases the chances of a favorable outcome. Metaphorically speaking, would you want a car painter to rush the preparation stage restoring your classic, just so you can have it back sooner?

Really, not necessarily. There's a fine line between going in blind, and the diminishing returns of trying to make things perfect - because things can never get totally perfect.

If I restore your bungalow, there's a price to get it to "good", and then the cost and time to get it perfect is going to be many multiples more. Most people can't rationalize perfect.

Probably depends on what you're prepared to live with. I'm in a "close enough is good enough" camp. Different story if we're doing something like making a high precision aircraft engine.

Ahh - yes, the convenient introduction of extreme comparisons like "high precision aircraft engine" and "perfect", why am I not surprised - LOL!

Deep down, you must think old school methods that involve patience suck and you'd rather no school - right?

Que another contrary......

I put the aircraft engine example there to satisfy the pedants. For much of the rest of life, I stand by my philosophy. Perfection very often gets in the way of good.

If someone's buying a house, my advice is to know your market, and the numbers around what you can afford with some space for life happening. But it's not something that should have a super long run up.

Much of what I do is a hybrid of old and new school. New sometimes is faster, but there's older methods new hasn't surpassed. Most clients though, don't want to pay for perfect. Although they desire perfect at the price of good, so I'll give them both options. Perfect might get chosen 5% of the time.

"Those first home buyers should have built up a significant amount of equity in their first home"

And that Equity isn't real. It's a revaluation based on current prices, that can disappear in a heartbeat. How much equity would those buyers of 10 years ago have if the resale price of their holding falls below what they paid? None. In fact, less than none.

Can't happen? "Property always goes up, as this article demonstrates!" It has before and can again.

but the shrinking size of that mortgage after paying 10 years is real.

Presumed already not doubled down on leverage, paying a decent amount of principal throughout, and haven't thrown anything else on the mortgage when money was going cheap.

Indeed. paper equity is just on paper. It is not the same as money sitting in the bank having been extracted from someone else via sale though bank lending assumes it is similar.

paper equity is just on paper

The physical act of putting a roof over your head is only getting more expensive. Until that reverses, the cost of any roof over your head gets to increase.

Why do property prices fall? All sorts of unexpected reasons. For instance, here's a post from just a year ago, and today those same properties have probably halved in price, for now obvious reasons.

"How insane are real estate prices in Beirut?! Would anyone spend half a million on a two bedrooms appartment!? I am not talking downtown as these go for million +, ...But I mean the whole country might blow up any minute - prices don’t make sense at all."

And it has blown up.....

Also you or I could be dead by tomorrow. So, why not enjoy life while we're alive, and not be scared of every unlikely bad thing we can imagine.

Exactly!

Why tie up the capacity to get out and live life to the full by having a noose of Mortgage Debt around your neck?

That's the problem. Mortgage Debt has now consumed much, if not all, of the Disposable Income of those just looking for a roof over their heads, as they look to create a family, and so they can't enjoy Life.

So as we might now be seeing more and more, they are saying," I could be dead by tomorrow. So, why not enjoy life while we're alive"

But my point is, those in Beirut didn't expect what has happened, to happen, even though it was likely (as written in the post above). Just as many on here don't expect prices to fall, even as the possibility of much higher Debt Rates looms.

Why tie up the capacity to get out and live life to the full by having a noose of Mortgage Debt around your neck?

Because one day, you'll be old. And your ability to enjoy life, and pay for it, gets harder.

People just need to be smart about it.

Not if you get early dementia, cancer, or any other illnesses, or if you have an accident that effects your mobility permanently such as someone having a medical event in their car and head on colliding into you on an idle Tuesday heading gone form the supermarket. Life is full of risk, but don't plan everything riding on your retirement and older age, there has to be a balance.

not be scared of every unlikely bad thing we can imagine

This was exactly the point: in Beirut the risks were not 'unlikely', but quite predictable

Transposing to NZ, downside risks for the market have been predicted by IMF and OECD reports for quite a while now (at least 5 years). Sure, they haven't materialised. Similarly to how risks in Beirut had not materialised until a month ago

Sure danicriss, you make your decisions about buying a house in NZ, based upon what happens in Beirut, Palestine and Ukraine, it's your choice. Good luck with that.

In the context of the "Beirut real estate crash" example, how do you think those same factors of escalating wars in the Middle East/eEurope reflect on NZ real estate prices? The obvious reply in my opinion is that far away countries such as NZ might become even more attractive if the world will enter a period of escalating global conflicts (which is actually happening right now). yes, conflicts are inflationary and that might mean that interest rates could increase again instead of going down, but I think that the rising demand from unprecedented immigration might counter the effects of rising interest rates for NZ real estate

Moral of the example is that everyone thinks they are really smart in seeing the 'signs', but as history proves, we can all be spectacularly wrong, regardless of which 'signs' we focus on.

First Home buyers of 10 years ago are now sitting pretty

And that's the only point. You don't buy a house for 2 or 5 years. Through the ups and downs, over time, you will be OK, and you will end up with a mortgage free home, it's that simple. Don't listen to the fear mongering.

"you will end up with a mortgage free home"

Again. That's not guaranteed.

Terry Serapisos had lots of property and still went broke, even though that property is today probably valued a twice what it was when he lost it......to insolvency, first.

In the many downturns in various property markets across the Globe, being able to afford to 'hang on' when the unexpected hits is key. And being mortgaged to the hilt before that happens (as Terry now knows) can be dangerous.

We have no buffer built into our present system - anywhere. And that is, well, Dangerous.

Divorce of course is also very common these days and that can really affect the ‘mortgage free at retirement’ scenario.

When I asked Yvil what a mortgagee sale was the other day, I thought his definition would have been something along the lines of 'an imaginary situation when a house is sold out from under you'.

bw, just stop the nonsense. Did Terry Serepisos, whom I know personally, go broke by buying his own home ? Of course not, Terry made and lost his money through very high risk property and business ventures. It has NOTHING to do with FHBs buying their own homes. Your post is pure fear mongering.

From my comment above

It speaks volumes when the capital gain hungry react angrily to suggestions that FHB’s take the time to patiently mitigate personal financial risks associated with owning property today before buying (especially today)

It’s nothing more than an agenda to spread fear – the fear of missing out.

Yvil, enjoyment alludes the many who followed your flawed philosophy. They also rushed out to "enjoy life", borrowed heavily from tomorrow just to have something overpriced today.

Yvil, enjoyment alludes the many

In the context of all home owners, you actually mean the few.

Pa1nter, fair comment :) It's my personal view that the odds of a poor outcome for FHB's has greatly increased.

As they are for all of us.

Pass on regards from Michelle H, my ex-sister in law, who went out with him some years back. But that aside, the last I read he didn't own his own home? It was conveniently owned by his mother? And the point remains. High Risk or Low Risk, being mortgaged past a point of loan serviceability (many FHBers today and the last few years?) is dangerous.

Life is dangerous bw, actually, some say we will all die one day. Until this day, forgive me if I choose to live the best life I can, without being scared of every imaginable thing that could possibly go wrong.

What's leverage?

In other news, "Sun rises in the east".

I was thinking 'water is wet', but both would be more honest as a title.

Moving up the ladder normally involves more debt and sometimes that extra debt taken on can be substantial. How many young couples would currently be able to obtain the extra debt and be able to or want to service it.

.

Noted that Retired-Poppy quickly removed his lengthy post immediately above - which was yet another word salad of ranting and raving.

His comments on this site are notoriously misleading and deceptive.

Further, his various predictions/ forecasts over the years have an atrocious record of accuracy. When asked about his abysmal forecasting, Retired-Poppy ducks and dives and refuses to give a proper answer. Typically, a smart-ass response is all he can come up with.

TTP

More to the point is what the community thinks about someone who is greedy enough to commit fraud, dumb enough to get caught and cowardly enough to deny it.......

by tothepoint | 3rd Sep 24, 11:39am

Who will pick the beginning of the next market upswing?

by Retired-Poppy | 3rd Sep 24, 11:47am

Personally, I think Spring of 2025 but it will be more the appearance of a sustainable floor than an upswing. I think any sustainable upswing in prices won't be apparent till Spring 2026.

Your turn...

With this Tim ducked for cover and ran away......

I love that you're 'replying' at length to a full stop.

Tim is angry at what he read. I simply moved the post to the top of the thread as I felt it was more relevant in response to general comments post.

I appreciate you have take 2014 - 10 years back - as a logical timeframe, and there is no ulterior motive to use that date to concoct a ‘good news’ story. However, I think it’s still worth pointing out that 2014 was the start of a circa 3-4 year price boom. And that the picture, in terms of equity, will generally look nowhere near as rosy for those who bought after 2017.

and the last 10 years also include the biggest falls in house values for the last 40 years… Again, as per my post above:

"You don't buy a house for 2 or 5 years. Through the ups and downs, over time, you will be OK, and you will end up with a mortgage free home, it's that simple"

Yes. But the key point of this article is ‘climbing the ladder’ off the back of equity gains. It takes 2014 as a point in time. My point is that if you looked at 2017 or after, equity gains look nowhere near as good

They look worst if your sample size is buying at the peak and looking at today.

Will houses be cheaper to supply in 10 years time? We'd have to be making some much more serious moves today.

Very unlikely indeed.

"My point is that if you looked at 2017 or after, equity gains look nowhere near as good"

Yes, and if you cherrypicked the date the values were the highest until now it would be even worse, and if you cherrypicked 2019 to 2021 the gains would look ridiculously high. That's why looking at the last 10 years, which encompass both the crazy gains and the biggest losses in 40 years, is a good, balanced timeframe.

It looks even better if you take the beginning of 2012 as the point in time.

Home owners who bought their first house a decade ago are now well placed to move up the property ladder

What a stupid title. If they're looking to move up (I assume bigger/better located property) then these people would be much better placed if prices were still at 2014 levels!

First home buyers of 10 years ago are now sitting pretty

Still a stupid title because it's untrue if they are intending to move up the property ladder compared to if prices were still the same as 10 years ago. Will they be sitting more or less 'pretty' if the children in the photo want to buy their own home in the future and have a family if prices were still at 2014 levels?

Disclosure: I still haven't read a single sentence of the 'article'. I will however read the comments, so why not charge for them to be made because there is well established causal relationship between the quality of a comment and a green tick.

Sorry Murray, but if you haven't read the article, you shouldn't comment on it.

"Disclosure: I still haven't read a single sentence of the 'article'"

That's really shallow of you, Greg explains with detailed number why the owners are "sitting pretty". Read the article before making assumptions!

I have enough information to support my statements about the titles given house prices have risen in the last 10 years.

I made no comment on the article contents.

You appear to be saying that the title and contents are at odds - dishonest even?

Having read the article, are you able to refute any of what I've said about the title or are you only able to call me names?

PS: I enjoy our discussions and no offence taken; I hope you don't mind me challenging you either.

If they're looking to move up (I assume bigger/better located property) then these people would be much better placed if prices were still at 2014 levels!

Yes. You are 100% correct. The price of something going up over time doesn't necessarily represent greater value.

People are better off if they can get greater value over time for the same amount of effort exerted and time expended.

Ten years ago in September 2014, the Real Estate Institute of New Zealand's national lower quartile selling price was $279,500.

I think 0% down payment or 5% down payment was still available then.

Yes. LVR restrictions were introduced in Nov '14, and applied indiscriminately from ~May '15.

Let's see the statisticians actually FIND a statistically significant number of 2015 FHBs next year to check against? And for those they do find, ask how many beat the 500% deposit increase without the help of Mum & Dad?

Let's be careful here. The period from 2014 to 2019 saw a trend of decreasing interest rates in Aotearoa, culminating in historically low levels by the end of 2018. This environment was characterized by low borrowing costs, which aimed to stimulate investment in the Ponzi and consumer spending - continued suppression of the cost of credit amidst global economic issues stemming from the GFC among others.

If I were to use gold as a benchmark to pay the entry level price for the Ponzi (comparing Sept 2014 to now), it would suggest that the purchasing power of the Kiwi peso has fallen by approx 20%. It makes sense that the declining value of the currency impacts the lower socio-economic demogs more. So the 'moving up the ladder' paradigm only really works if incomes are increasing at a rate far greater than than the decline in purchasing power of the currency.

Furthermore, if I'm moving up this property ladder, I need the equity gains to propel me into a different property bracket.

Great comment

Has to be said. The period that I indicated includes some of the lowest debt servicing costs in history. Throughout the Anglosphere in particular, you would have seen some of the largest money expansion (correlated with suppressed debt cost servicing) ever seen before we even reached the unthinkable scenarios we have now. for some reason, people think of 2014 up to Covid as "normal", but it was anything but. By the way, it's not just incidental that 2014 is now being accepted as a critical point in recent economic history as this is when gold hit lows.

No, it's not, sorry JC. It's very one sided. JC mentions the big drop in interest rate which is true, but he conveniently ignores the subsequent equally big increase in interest rate, leading to the biggest drop in Re values of the last 40 years.

I hear you Dr Y. I consciously left out the Covid years as the 'all hands on deck' cost of credit operation was even more ridiculous than the period leading up to it.

Yet we moved to ‘high’ interest rates that are effectively average by historical standards. And his point was a historical perspective

"Let's be careful here. The period from 2014 to 2019 saw a trend of decreasing interest rates in Aotearoa. This environment was characterized by low borrowing costs, which aimed to stimulate investment in the Ponzi and consumer spending"

Let's be careful here. The period from 2021 to 2024 saw a trend of increasing interest rates in NZ, . This environment was characterized by the steepest increase in borrowing costs, which resulted in the biggest drop in RE values over the last 40 years.

How about we stay balanced JC and we look at both ? That's why 10 years from today is a great timeframe, encompassing both, a crazy upswing in values, and the greatest drop in values of the last 40 years.

My ‘reckon’ is that future upswings won’t be anywhere near as significant, and we will get more dips. Hence my point stands that the 2014-2024 period, which still shows pretty big rises overall despite the drop of the past 2 years, is unlikely to foreshadow post-2017 ten year price trends

Pretty weak troll skit Dr Y. Anyway, suppressing the price of money has implications in more ways than one.

Let's give it some context.

Assume the equivalent entry house price in 2014 of $295,000. Assume that was a purchase of gold instead. The value would be closer to NZD900,000 today.

Similarly for rat poison, That NZD290k would be worth approx NZD23 million.

The owner's portion of that $295K would only have been 10% (or 20%), so the equivalent return on the gold would be $90K/$180K.

BTC would of course look much better at $2.3M/$4.6M, but not many had the cajones to throw their life savings at BTC in 2014.

The owner's portion of that $295K would only have been 10% (or 20%)

What about the interest payments over the 10 years..

Big congrats to them, well-deserved, I’m sure. Remember you’re in charge of your own journey. Success isn’t waiting for anyone.

This is a great piece and it was about time something balanced like this went to print. Anyone who buys now will be in the same position in 10 years time.

This is a great piece and it was about time something balanced like this went to print. Anyone who buys now will be in the same position in 10 years time.

You could always print it out Z and put it in people's letterboxes. Use it as some kind of 'evidential' business case for your prophecy.

How easy is it to get a 30 year mortgage at age 40?

Easy, if the financials are ok. 40 yo is not a barrier to getting a 30 year mortgage.

Thanks.

Genuine question- are you considering buying a residential investment property in the next 12 months?

No

HouseMouse : "How easy is it to get a 30 year mortgage at age 40? "

Seriously?

Do you expect to any sage advice from here?

So what’s the answer? I wouldn’t know. Yvil seems to think it’s possible. And the article implies it is possible / likely.

Yvil doesn't think it's possible, Yvil knows it's possible (provided the financial stack up, of course)

Oh thx

so they assume someone will still be working age 70

at what point do they draw the line on 30 year mortgages then? 45? Or do they not care as they assume some will just sell if they stop working and can’t afford repayments

It's possible, but it gets exponentially harder after 40.

"so they assume someone will still be working age 70?"

Most likely there is a re-structure planned before the 30 years is up.

Banks are quite happy to lend at 30 years to older (40+) people - so they make heaps of interest - while the mortgagor gets the minimum repayment - once they know that after 20 years the mortgagor has a plan, e.g. lump sum from an inheritance, sale & downsize, refinance to a shorter term after 5 years, Kiwisaver cashed up at 65, etc. etc.

One wonders how many kiwis will choose to move 'up the ladder' using their net equity of around $369,942,

Given how our woeful tax system operates, many will choose to do that other 'most kiwi of things' and buy a rental property instead.

And there, in that last sentence, is why housing is so un-affordable in NZ.

(And is why I build my rental property investments. My conscience is clear. I sleep well at night.)

Most people think that the choice under all conditions is between:

1) rent vs

2) buy their own residential dwelling (house, apartment, etc)

However under certain conditions, the choice becomes:

1) rent (and preserve savings which could be used as a deposit to buy a house) vs

2) buy their own house (and risk losing their 500% - 1000% of their deposit, risk losing their own house, and still owe the lender money after the house is sold)

Under some conditions, it is better to rent than buy.

Under some conditions, it is better to buy than rent.

Future potential near term upgraders and downsizers should also learn the lessons here:

https://www.oneroof.co.nz/news/homeowners-loan-requests-rejected-they-h…

Most people forget the commonly repeated investment warning - past returns are no guarantee of future returns.

People who fail the learn the lessons of history are doomed to repeat them.

The choice for owner occupier buyers is between:

1) the fear of missing out on potential residential property price gains

2) the fear of potentially losing 500 - 1000% of your potential equity deposit (and potential life time of savings)

People are free to choose, however they are not free to choose the consequences of their choice.

Each owner occupier buyer is in a unique situation and has to make their own assessment with respect to their circumstances and the conditions of the geographical market which they are looking to buy vs rent.

Remember mortgaged owner occupiers have to continue meeting debt service payments under ALL conditions.

Owner occupier buyers: CAVEAT EMPTOR

Most people forget the commonly repeated investment warning - past returns are no guarantee of future returns.

People who fail the learn the lessons of history are doomed to repeat them.

This is a contradictory statement.

"This is a contradictory statement."

The second statement is unrelated to house prices.

Why does housing get excluded?

History is the most reliable means of assessing the future.

In this instance, some of the most important questions are:

- do we think central authorities will stop importing people, thus allowing us to depopulate and free up housing supply?

- will central authorities stop juicing the money supply and asset prices?

- are councils likely to make housing consents cheaper, or more expensive? If yes, given their dire financial states, why would they do that?

- will building a new house get any cheaper?

About the only scenario we will see things going seriously south for a prolonged period would require a massive economic upheaval few will be insulated from. This is going to happen, what we don't know is when.

It's not contradictory at all. History provides numerous examples of how past performance was NOT an indication of future returns..

In terms of your pertinent questions, in a roundabout way I think the answer to most of them will be yes, although not by design. I think they will run out of options, question is just when?

I think extending mortgage terms through "multigenerational lending" is pretty much a given at this stage, so I'm not too concerned about negative equity and the sky falling in when I buy. There'll be a few more cycles of engineered house price inflation. But banking on downsizing and using equity in the house to retire on in 30 years time is an incredibly stupid strategy at this point.

Workings need to be explained/outlined better.

How did you come to $369,942 equity?

Does that factor interest paid over 10 years? What about maintenance costs?

Fairly hard to define.

Probably more illustrative would be the net worth of people the same age, who didn't buy a house 10 years ago.

This will help ...

Equity (in the example) = Sale price in Sept 2024 at $595,000 - outstanding mortgage balance (see calculator above)

Maintenance costs, and all other costs like rates, insurance, etc., are paid from other income.

It seems most commenters are not interested in facts. Greg uses real numbers to substantiate his claim that FHB who bought 10 years ago are now sitting pretty. Yet, so many posters here fight Greg's conclusion and warn of apocalypse in the future. Some (like Murray Falconer) haven't even read the article. How shallow is this? It's more alike a sporting event, where posters blindly support team blue over team red, beyond any reason or facts. No wonder so many struggle to make good decisions when they can't see (don't want to see) reality.

That’s all fine Yvil, for what it’s worth as a ‘one point in time’ revelation. The problem is, it’s probably quite unlikely that 2014-2024 will be replicated moving forward. As above, how will FHBs who bought in 2017 etc be placed in 2027 etc in terms of equity? Unless we see an unlikely boom in the next 2-3 years, nowhere near as well as the 2014-2024 example in the article.

I think it’s important that people understand that.

This fixation with house prices ... While ignoring all else ... I found quite disturbing.

Is that who we are?

My longterm predictions for 10 years time:

House prices will rise 30%.

Rents will be up 50%

Interest rates will have averaged 5%

RP will still be telling FHBs to wait.

Sounds about right, maybe rents a bit less say 35~40%, and perhaps house prices 40%

nowhere near double

"House prices will rise 30%."

But ... but ... but ... "House prices double every 10 years". ;-)

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.