The ability of first home buyers to save a reasonable deposit is likely to have a bigger impact on their ability to get into a home of their own than falling interest rates.

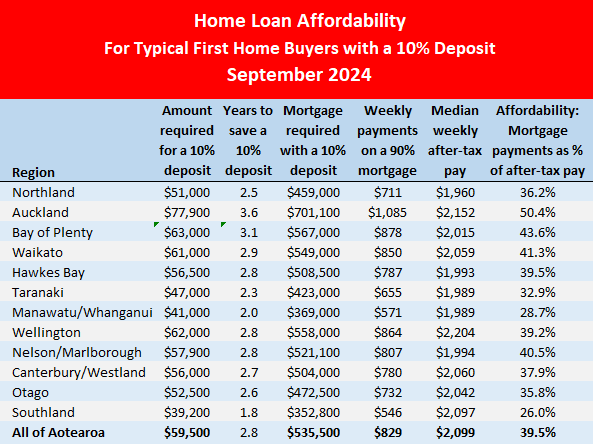

Interest.co.nz's latest calculations show typical first home buyers should be able to afford the mortgage payments on a lower quartile-priced home almost anywhere in the country at current interest rates, if they are able to scrape together a 20% deposit. However, that affordably drops away sharply if they only have a 10% deposit, particularly if they are looking to buy in the upper North Island. (See the note below explaining how the calculations are made).

We also measure how affordable the mortgage payments are for couples earning the median rates of pay for people aged 25-29.

At the national level, that would give a young couple a combined, after-tax pay packet of about $2100 a week, although there are regional differences.

Mortgage payments are considered unaffordable if they take up more than 40% of their take home pay.

On that basis, there are only three districts in the country that are considered unaffordable for first home buyers on average incomes if they have a 20% deposit. They are; Auckland's northern suburbs of Rodney and the North Shore, and the tourist mecca of Queenstown.

So in almost all of New Zealand, the problem first home buyers face isn't not being able to afford the mortgage payments, it's being able to get together a 20% deposit.

That will range from having to find $76,700 in Invercargill, the country's most affordable housing district, to $196,000 in Queenstown, the country's most expensive.

Across the Auckland Region, a 20% deposit on a lower quartile-priced home averages out at $155,800, which interest.co.nz estimates will take typical first home buyers seven years to save if they set aside 20% of their take home pay into an interest bearing account every week. That doesn't take into account any inflation in house prices that might occur over that period.

That will push many first home buyers to attempt to buy their first home with a low equity loan. But even that option will require a reasonable chunk of cash for a deposit.

A 10% deposit on a lower quartile-priced home will range from $38,350 in Invercargill, to $77,900 in the Auckland region and $98,000 in Queenstown.

The trouble with that option is a low equity loan is much more expensive than one with a 20% deposit, not only because more money is being borrowed, but also because banks charge substantially more for low equity loans to cover the extra risk involved.

And that pushes the mortgage payments into unaffordable territory for many parts of the country.

With a 10% deposit, mortgage payments become unaffordable for all of the Auckland region, including its most affordable districts of Papakura and Franklin on its southern flank.

Hamilton, Tauranga, Napier, Kapiti Coast, Porirua, Wellington City and Queenstown are also on the unaffordable list for low equity buyers.

So where is it still affordable for first home buyers on average incomes to buy a home if they don't have a 20% deposit?

Their mainstream options are likely limited to Whangarei, Rotorua, Gisborne and New Plymouth in the upper North Island, Hasting, Whanganui, Palmerston North, Hutt Valley and Wairarapa in the lower North Island, or anywhere in the South Island except Queenstown, although Nelson is marginal and Christchurch is at the upper end of affordability levels.

But if aspiring first home buyers want to buy into the main centres of Auckland, Hamilton or Tauranga, or in central or northern Wellington, they will need higher than average incomes or access to a big chunk of cash or both.

The comment stream on this article is now closed.

Note: How we calculate the Home Loan Affordability Report:

| Calculations are based on buying a home at the REINZ's lower quartile selling price in each region/district. The mortgage interest rate used is 5.89%, with a loading for a low equity loan (where applicable), with a 30-year term. Weekly income is after-tax and based on the median rates of pay for couples aged 25-29 and assumes both work full time. Years to save is based on saving 20% of after-tax pay into an interest bearing account | ||||||

55 Comments

"latest calculations show typical first home buyers should be able to afford the mortgage payments on a lower quartile-priced home almost anywhere in the country at current interest rates"

And the most important word in that sentence? Current.

If we should have learned anything from the last 3 years, it's that unexpected things can happen to change what % rate 'current' is. If it's lower than today, then all well and good. But there is very little to go if % rates, say, halve from here. But what if the opposite happens? % rates double, or triple or more. And that's the thing. As we've recently seen, the lower bound for all practical purposes is 0%. There is no ceiling; not 10% or 20% or even 100%.

Gold: NZ$4,517.58 ↑. NZ$ 0.6024 ↓.

Interesting to compare affordability with levels back at Nov 2021.

https://www.interest.co.nz/property/113833/prices-bottom-market-continu…

"the lower bound for all practical purposes is 0%"

Really? Do tell us more ... ;-)

"There is no ceiling; not 10% or 20% or even 100%."

And more on that assertion would be extremely interesting too ... ;-)

They should be able to afford to buy a lower quartile-priced home, but FHB should not be greedy and leave some stock for investors.

Despite what NZ Gecko says, the market is rising. Be quick.

Be quick? Agreed. Get out whilst you can; whilst there are still buyers about - at any price.

That's what lower mortgage rates are providing; a chance to sell.

this is Geckos (sheeps) other account.

@ bw - Get out now? And go where? Onto the government's emergancy social housing wait list along with the other 28,000 families waiting? No thanks doomsdayer. Bet you been waiting decades for the "great bubble burst" lol You missed multiple ones, including the one we've just had.

What is the "emergency social housing wait list"? I assume you mean the waitlist for public housing, if so, why would anyone selling a house need to necessarily go on a public housing waitlist, that's a doomsdayer comment right there. They could buy a cheaper property, rent, move in with family, share a property with friends, move overseas etc.

Also some areas in NZ hit their lowest level since their peak on the REINZ House Price Index in September 2024.

@ 26@Main - "They could buy a cheaper property, rent, move in with family, share a property with friends, move overseas etc."

Buying & selling in the same market = the same type of property at the same type of price point, unless the seller is downsizing. This means your selling & buying like for like. It's counterproductive. People typically don't downsize unless they're much older & their children have left home. Even then, empty nesters typically hold onto the family home for a lot longer, they don't generally immediately downsize as soon as their children move out. Downsizing would also imply that they sell and re buy again, not "get out of housing", but a change of circumstances leading to a change of property type.

Why would anyone selling want to go back to renting willingly unless its temporary in the short term until they buy again? If they've put themselves in a position where they have to sell & revert back to renting, its usually to do with a series of poor financial choices that they have put themselves in that position, & were likely never cut out to be home owners in the first place. This usually occurs when one maintains a renters mindset, where they don't budget for home owners additional expences such as rates, water rates, insurance, maintenance costs ect.

Move in with family can understand to a degree, if the family was sick or needed constant assistance in some way. Most well established home owners don't willingly sell up to move back home permanently unless this is the case. Ask most well established home owners how long they feel they could realistically live with their parents again on a permanent basis after spending so long out of home.

Share a property with friends? I doubt this is a popular option at all - "hey let's all sell our properties and live together". This sounds more like a rental situation, imagined by a renter themselves or someone who has watched too much Friends on TV. Ask most home owners if they actually like their friends that much that they could also permanently live with them, you'll surprise yourself with the resounding answer.

Moving over seas would be about the only logical reason to sell to "get out of housing", and again it's only temporary until they look to re buy again in the next location. So this is not really "getting out of housing" either.

Either way, to suggest "getting out of the housing market and go back to renting" as a logical solution makes little sense at all. It is usually suggested by tenants, expecting that if so many people sold up & walked a day in their shoes as a renter, they may have more empathy towards them, and at the same time current renters then may be finally able to afford a super cheap house to buy themselves. Because it's everyone else's fault why they can't afford a house deposit. It's a biased fantasy at best. Think it through. Regardless if you rent or you own, you are still part of the housing system. The ones who are exempt from this as I said before are the ones that are government dependant to house them. Yes, this is called The emergancy social housing wait list, or the wait list for public housing, funded by government.

The other options I suppose would be voluntary homelessness, or those living in caravan parks. Though to even suggest this would be a better lifestyle choice than owning shows ignorance of the highest level. Owning will almost always be the better option. It is the envious doomsdayers that incoherently advocate to "get out now while you still can". But they simply cannot logically answer "get out to what?" Homelessnes? Renters for life? Live on a boat? A campervan? A caravan? A tiny home? Are these better options than owning?

Overseas

Residential real estate at lower price points - non owner occupier buyers are outbidding owner occupier buyers

"Pointon said there had been an uptick in demand for houses in the sub-$800,000 price bracket in Hamilton, with first-home buyers now facing competition from investors, who until now have largely been absent from the market."

"One of his listings, a three-bedroom home on Howden Road, in Fairfield, had received seven offers within six days of hitting the market and sold to an investor who made an unconditional cash offer of $740,000."

https://www.oneroof.co.nz/news/latest-news/they-know-they-will-be-blowi…

Oh look another oneroof article driven by anecdotes.

Reality is inventory is increasing as are days to sell.

It's not that there aren't places that are affordable - they mostly just have no jobs available.

Also, saw an article on ?oneroof? A few days ago reporting the banks had hit their limit on low-equity mortgages. In which scenario affordability matters not.

It's not that there aren't places that are affordable - they mostly just have no jobs available.

Perhaps the owners can use them as places where they trade low-cap altcoin speccys into the day and night. Or some kind of WFH gig contracted to the public sector. Commute to Wellington for the monthly meeting. Worse-case is a Breaking Bad scenario.

incomes in many of the places that are listed as affordable are below the national average used to calculate affordability. So they are in fact….unaffordable for those living there!

That's not quite correct Speedmax. The income measures used to calculate affordability are regionalised, to take into account different income levels in different places, although the regionalisations are fairly broad.

There must be some kind of error in the data. According to the table the median after tax income in Southland is listed as only $55 per week less than Auckland.

A few months ago I was explaining to my two teenagers what mortgages were, the different types, how they were calculated, and the pros and cons of various permutations, especially the benefits of a bigger deposit & shorter terms. This calculator from interest.co does a great job in making sense of this for the common P&I mortgage.

A few weeks later I was discussing my 'flat mates wanted' analysis and the kids were listening in.

Well, the older of the two, who isn't exactly covering themselves in glory on the academic front, but they do have a well developed sense of cunning (most probably inherited from their mother) asked later ...

"Dad, can you please get in a border for my room when I leave and buy a house. You can use the board to repay the $100k that I'll need for my house deposit so I have as a big a deposit as possible."

Proud Dad moment? Anyway, my response was brutal, "So you want to understand how tax works? And how the weekly board monies will be taxed?"

Anyways, thanks interest.co.nz team. This a great monthly reminder as to what our children face.

Don't declare the boarder living in your place. As DJT says, 'fight, fight.'

I seem to be one of those people the IRD likes to send "please explain" letters too. (I can't think why ;-)

Works out better to be 100% squeaky clean as accountants charge a lot per hour.

Your kid is expecting you to pay for their deposit?

More "top up" their deposit so they can keep the term as short as possible. It makes financial sense. And I quite like boarders as I grew up in a big family (and my wife shouts at me less when they're around ;-).

The standard cost method for ird allows a cost deduction of $231 per week per boarder. If you let the boarder have his girlfriend in his room on the weekends you won't pay any tax.

Yup. But the 'standard cost method' comes with a definition of a boarder that doesn't cover the boarders I've had. So I have to use the other method (which sometimes works out better).

Could you explain the girlfriend reference? How does that affect things?

Just poking fun. If you were to argue that she was a boarder too on account of always being around you could double the $231 pw. Not legal advice. Bad joke.

.....meanwhile the overall standard of living in this country drops.

This is couples, singles left in the dust!

Also, it must drive the fertility rate down further if you have a mortgage and think one child is expensive enough.

You're right. And for many of us we lack the looks to secure a willing spouse without first having a house.

The unaffordability will doom many a hairy troll to lifelong loneliness.

You saying no house no spouse?!

not true, easy for singles who have any future planning to save a deposit if they get flatmates. and a job pay more than 90K ish.

Yes that's the route I took but most people are not prepared to compromise to that degree.

There are plenty of First Home Buyers looking in Christchurch now!

ChCh is the quickest growing city in NZ.

The reason being is that the happiest city has the the lifestyle that people want.

Thing is people are getting out of Auckland as it does not offer enough for Kiwis now for the cost of living.

The population in Auckland has grown over recent years by immigration from mainly the Asian countries.

Ch-ch has never appealed to me as a place to live, a bit too flat, characterless and dare i say it here, conservative. But that's just me and maybe I am wrong. I will give plenty of credit to it's location for access to incredible outdoor/nature options. I would kill for that living up here in Akl. To think I could live mortgage free in a decent home in Ch-ch. Maybe it's time to reconsider.

The beauty for cyclists and walkers is it's dead flat until you actually want a hill, in which case you are spoilt for choice. Decent array of cycle paths now, despite the heavy sprinkling of grit in the wheels of progress.

Don't come if you want to see native birds though - it's a wasteland as are most of the plains. We're working on it though.

Definitely flat but the port hills are on the doorstep!

Character is on its way back, at the same speed as the rebuild. By 2030 should be good to go! I will be moving back (after my stint here in AU).

Isn't Christchurch were the soon to collapse Williams and Wolfbrook are?

Lol, get back to “ The Man” when they miss paying a tradie or their shareholders!

Thing is you won’t be, sounder than any Bank!

Too fkn cold!

Might need some hairs on your chest then ;-)

The West Island

As of 2023, the median age for first marriages in New Zealand has risen to around 32 years for women and 33 years for men.

It hasn't been as low as Mr Ninness suggests since the 90's. Specifically, in 1991, the median age at first marriage was approximately 25 for women and 27 for men.

When an older person gets stuck referencing a specific period of time and seems unable to update their cultural or factual references, it's often referred to as "temporal bias" or "time warp thinking." This can also be linked to "nostalgia fixation," where an individual becomes anchored to a particular time in their life and views that period as the most relevant, leading to outdated references or anachronisms.

Maybe it's still the ages for 'common marriages'? Or 'shacking up' as it's also called.

My wife and I were onto our second house before we formally tied the knot. (I think she just wanted to throw a big party for her friends.)

The reference in our calculations is for couples, not married couples.

Respectfully Greg, as per 26@Main's comment below, your reference is incorrect.

But when do they start saving for that first home? They don't just start saving and buy one straight away, unless they win Lotto. In Auckland they'd need to have saved for seven years to get a deposit together.

The survey is nonsense, and the editors are too bloody minded to rethink their obstinate positions

I gave up on trying to get any sense out of them a while back

From a recent RNZ article:

The country's largest bank, ANZ, said the average age of its first-home buyers was now 35. BNZ said about 45 percent of its first-home buyers were early to mid-30s. Westpac said its average age for a first home was also 35.

Credit bureau Centrix said earlier in the year the average age of a first-home buyer was 37 - it had fluctuated from 37.6 at the start of 2018 to 35.7 years in the fourth quarter of 2021. That average is roughly ten years later in life than where it sat in the 1970s.

https://www.rnz.co.nz/news/national/530751/is-it-harder-to-buy-a-house-once-you-re-40

Yes I have raised this previously. Ignored.

The ship’s finally about to leave… what a thrilling moment.

PLEASE EXPLAIN...

Are your repayment calculations correct?

i.e. Take Papakura Auckland where you have an assumed purchase price of $675,000 with a 10% deposit of $67,500 (ie a mortgage of $607,500). Your repayments are apparently $941/week?

According to the BNZ mortgage repayment calculator weekly repayments on this basis are only $828/week?

If you were using the LOWEST available BNZ mortgage rate which is 5.59% fixed for 4 or 5 years then repayments are only $804/week

Am I missing something with these calculations? How did you calculate your repayment amounts because they appear to be significantly incorrect?

Low equity margin is applied for the 10% deposit table

So how much is the low equity margin because the difference in mortgage repayments of $113/week appears to be excessive... I mean that equates to a whopping $176,280 over the 30 years?

You can see the methodology used in the note at the bottom of the article, which also appears at the bottom of the 10% and 20% tables.

You are right about the low equity margin, it is substantial.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.