Considering the amount of publicity given to people facing so-called mortgage stress, the number of homes facing a mortgagee sale remains surprisingly low. Perhaps this is in part due to a secret weapon the banks have when dealing with home owners who can't make their mortgage payments.

It goes by various names but is most commonly referred to as either an unauthorised overdraft or unarranged overdraft. For the purposes of this article we will simply refer to as an overdraft.

According to the Reserve Bank, it generally works like this:

"When a customer has a standard loan facility [mortgage] with payments linked to their current account, and there are insufficient funds to cover a loan payment, most banking systems will not mark the loan as in default.

"Instead, they will automatically place the current account into an unauthorised overdraft."

This means the full amount of the regular mortgage payment will be paid from the overdraft, and any shortfall arising from what the customer can afford to pay, accumulates in the overdraft account.

So in simple terms, say the regular mortgage payments are $1400 a fortnight but the customer can only afford to pay $1200.

The full payment of $1400 is made from the overdraft account, and the shortfall of $200 remains within the overdraft.

Over time the shortfall would continue to accumulate within the overdraft, but the mortgage payments would be up to date.

However for the borrower, this brings with it problems of its own, because essentially they are paying down debt with more debt, and are also partly replacing relatively cheap debt (on the mortgage) with very expensive debt (on the overdraft).

Debt managers spoken to by interest.co.nz, who have asked not to be named, say the interest rates charged by the banks on so-called unauthorised overdrafts can be around 22%.

To be fair to the banks, you would have to say that such arrangements carry a very high level of risk, and the interest rates charged reflect that.

The advantage of such arrangements is that they provide a little bit of breathing space until a permanent solution can be found and that avoids having to proceed immediately to a mortgagee sale.

Interest.co.nz monitors the number of residential mortgagee sales coming to market and these are currently running at around a dozen a week.

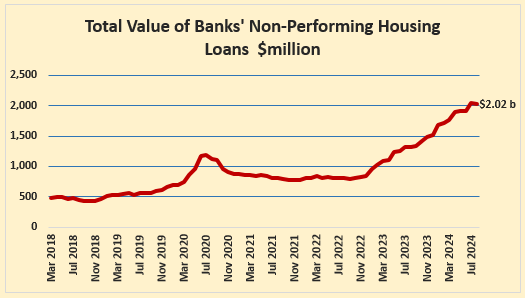

That's a drop in the bucket considering that according to Reserve Bank figures, the total value of non-performing housing loans was $2.02 billion at the end of August (see graph below).

That figure includes mortgages with the type of overdraft facility described above.

According to the Reserve Bank, when an overdraft is put in place to cover a shortfall in mortgage payments, the mortgage is classified as "past due' and after 90 days this becomes "non-performing."

So eventually the piper must be paid and as well as finding a way to meet their ongoing mortgage commitments, the borrower will also need to pay down however much has accumulated in the overdraft under such arrangements.

But hopefully they should still have their house.

The comment stream on this story is now closed.

*This article was first published in our email for paying subscribers. See here for more details and how to subscribe.

22 Comments

Better to use a revolving credit facility (which would need to be setup well before financial troubles start) or possibly ask the bank to increase the fixed term loan.

Most would already have a revolving credit facility I think, and the situation described would happen once that's been tapped out.

In our case our ANZ flexi (a revolving credit) covered mortgage payments. Once it hit the limit, it just kept going. So yeah. You can have an unarranged overdraft on a revolving credit facility!

Banks have an offset product. Not sure how this is categorised in the above or is the above unrelated and is an unauthorized overdraft?

An unauthorized overdraft is certainly an indication of cashflow stress by highly leveraged borrowers. A bank typically requires repayment of an unauthorized overdraft and there are high interest rates as well as additional bank fees.

At what point does the bank say enough is enough and the borrower has to be up to date on their payments?

At what point does the bank say enough is enough and the borrower has to be up to date on their payments?

They rise at the point when the market picks up and sales can be made ... either encouraged, forced or mortgagee. I shudder to think how many could be out there. Probably not a huge number in the grand scheme of things, but some of the current listings will be in this situation. Banks could be stricter if they wanted too but it's really not in their interests at this time - rolling snowballs have a habit of getting larger. There's still some ways to go to out of this slump. Patience is warranted.

It depends on the level of client communication with the bank. if a person has lost a job, and getting another job will resolve it, I think the bank has a position of care to give the situation a chance to resolve.

"if a person has lost a job, and getting another job will resolve it, I think the bank has a position of care to give the situation a chance to resolve."

How long will the bank give to an unemployed person before asking for repayment?

For a owner occupier household with a high LVR (e g more than 90% at current valuations), the lender may allow a shorter timeframe?

What about a owner occupier household who is currently in negative equity?

As I understand, the banks are more willing to work with owner occupiers than non owner occupiers owners and the financial constraints and criteria vary to each category of owner.

They have a much longer hardship process now days

From what I am seeing, the extra rope allowed on the gallows, is only stretching for another three months.

I am in Wellington in a lending role, although a very conservative one, having seen a few of these cycles before.

This time feels harder to me, a little more public, a little more mainstreet.

Another commentator today was talking about manufacturer payrolls going sideways if they were lucky and down more often than desirable.

Buckle up people.

"Banks could be stricter if they wanted too but it's really not in their interests at this time "

What does the bank do to owner occupier borrowers in the following situation?

A) an owner occupier borrower who is

1) high LVR at current market valuations say 90%

2) in negative equity (i.e LVR >100%) AND

B) unable to continue meeting mortgage payments due to a loss in houeshold income due to job loss or fall in income (e.g lower commission income)?

How long will the bank work with the owner occupier borrower to give them time to find another job or for their earnings to recover to sufficient levels to meet mortgage payments? 3 months? 6 months? 9 months? 12 months?

If there are a sufficient number of these borrowers, then there could be more owner occupier borrowers receiving notices from banks with deadlines for mortgage repayment and under a time constraint to sell before the banks step in with mortgagee sales.

Slightly off topic, unauthorized overdraft fees are a peculiar thing. I got caught out with one once many years ago, I think it was a $3 fee, despite having sufficient funds in my other accounts. My bad!

At the time I was not aware the bank changed my Cheque account to allow EFTPOS transactions to go negative, was used to being declined at POS. Would be interesting to see what costs or losses that $3 fee actually covers.

I got caught at by those overdraft penalties back then too. I think the charge per transaction was more like $20 and I had made several transactions expecting they were OK as they hadn't been declined - I always carried cash just in case. Back in the 80s (I think it was) that was a lot of money. They changed their policy without informing customers and I believe it was a sneaky way of making money for nothing. I complained and got the charges waived. I'm guessing a lot of people just paid up. It have never trusted banks since. Which is probably a good thing. They are only in it for themselves. Of course. As many of those who haven't been able to meet their mortgage payments are about to find out.

I always had a transaction authorization denial on my account until I spotted the $3 fee in my statements. Early 2000's. I check my statements every month religiously.

Complained to the bank, I believe they waived it. Just would've been nice if it wasn't done by stealth, because I don't necessarily mind the convenience factor. Their app now gives me a notification if my balance falls below a pre-set amount which is nice.

When BNZ almost failed Ron B proposed to buy BNZ, using money borrowed .... from BNZ.

Looks to me giving it a good push to get last juice out.

Greg, I know for a fact that major banks all but turned off unarranged overdrafts because of CCCFA. Regulation says banks must carry a full financial assessment before extending someone's line of credit, so unarranged overdrafts would be a breach. Not sure what minor players are doing though.

I believe the reason for low mortgagee sales is bank's efforts to help customer manage stress (special payment plans, interest only, etc)

Not my area of expertise but was this one of the CCCFA requirements the coalition revoked?

Full financial assessment is still required, banks just don't have to scrutinize as much anymore by going through the details of someone's statement - basically they can trust expense info provided by customers more than before, but banks still have to ask the questions and somehow calculate if customers can afford what they're asking

Did they do a full financial assessment when stress tests were only ~5% and interest rates at 2.99%? They will do all they can to prevent the panic stage of the cycle kicking in by increased numbers of mortgagee sales, which could potentially trigger more vendors to list and sell before the mayhem ensues. Easier to take a hit for a while at least and allow time for the mortgage holders to sort things out and get back on track with payments, and kept the stats looking ok for the non-performing loans which again, could slide things further towards panic.

But one thing is for certain, the brunt of the pain will be shouldered by borrowers who foolishly trusted the banks to make sound financial assessments for them. You know, the subject matter expert institutions with access to a wide range of data and people who do this for a living and should have their customer's best interests in mind.

Some cashflow crunches are temporary so giving homeowners more time to wriggle through seems like a good thing.

Anyone who ground out the last 12 months can fix interest rates for 1.5% lower than before. If they can cover their costs now then it was well worth the grind.

Why is it that banks encourage some owners to over extend and then get to penalise them when under stress? This feels unfair.

Some equalising of the shared nature of risk is needed.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.