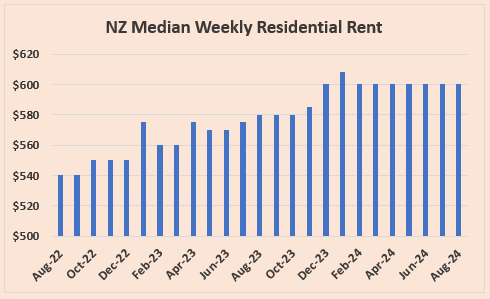

The housing market has seen little if any rental growth this year, according to the latest bond data from Tenancy Services.

The national median rent has remained unchanged at $600 a week for seven consecutive months between February and August.

In practical terms the national median has been flat since December last year when it hit $600 a week for the first time. It briefly popped up to $608 in January before dropping back to $600 in February, where it has remained ever since.

While there are regional variations in rental growth, for the main population centres rents remained reasonably flat throughout the country in August.

In the Auckland region the median rent has fluctuated between $650 and $660 since September last year. That's apart from November 2023 when it briefly dropped to $645, and May this year when it popped up to $670 for the month. This suggests rents have been more or less flat in Auckland for almost 12 months.

In the Wellington Region the median rent has bounced around between $600 and $623 a week since March, and settled at $620 in August, suggesting rents in the Capital are reasonably settled for the time being.

In Canterbury median rents have remained within a narrow band of $540 to $550 a week since November last year. They were at $540 for the second month in a row in August, also suggesting a settled market.

A more detailed quarterly analysis, to the second quarter, of rent movements in all major urban districts is available here. It will be updated with third quarter data next month.

The table below shows the national median weekly rents for each month over the two years from August 2022 to August 2024.

The fact rents have remained stable for so long suggests supply and demand for rental properties is reasonably balanced overall.

The comment stream on this story is now closed.

You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

45 Comments

But bu but but…. Rents are going to boom with all the immigration!

whoops

the huge number of townhouses being completed no doubt is playing a major role in keeping rental inflation at zero. Well over 800 townhouses for rent in Auckland on TradeMe

No locally born person wants to live in these. Heck even immigrants are turning their nose at them.

I listed my house for rent about 3 weeks ago and got flooded by people in the first week wanting to escape outta their sh*tboxes and into a proper sized home. We had it rent for $750 odd a week within a week and had to turn down about 30 good applicants.

Much like the sales market, good quality housing is holding price, but sh*tboxes are diving quickly as people dont want to live in them. Rentals no different.

The majority of townhouses, terraced houses and apartments in NZ are designed and built with no regard for the occupants and purely for investors to speculate on. The developers and their architects play a game of Tetris trying to fit as many of these shoeboxes as possible on the smallest footprint.

There is an acute shortage of well-designed townhouses with decent outdoor spaces and carports/garages, and these tend to be highly sought-after by renters and buyers alike.

Very much this. These newer build places tend to bake in the sun (especially upstairs), have the most naff garden/patio areas - if any - all lined up so you don't get much privacy at all, and seem to fall to bits within a few years.

However, they seem to be purely a 'vehicle of speculation' by which investors can leverage equity in their home/portfolio to buy more new build property and rent it out to the latest arrivals. I recall a client of mine who has purchased 3 Williams Corp units in Chch without ever seeing them. He was very frank about it being the easiest way for him to buy the most amount of property for the smallest amount of real cash down.

Occasionally there is some hapless owner occupier who manages to find themselves inevitably wedged between two Air BnB party houses.

For disclosure, I live in one of your latter category townhouses.

However, it was built post-quake (Chch) but well before the likes of Williams Corp and Wolfbrook came to prominence. There is adequate off street parking for two cars, a proper double garage, and a very private courtyard garden area. The neighbours had grass laid in theirs and it's a genuinely nice, bona fide backyard. Freehold section too which is nice. There are four townhouses in our 'row' (two pairs, in effect) and none of them has ever struggled to sell or be rented.

The only modifications we've made are having LED lighting installed, and an upstairs ducted AC system which has been a gamechanger.

That's because they are only designed for people who arrive with nothing but a suitcase. There is no storage for anything, the kitchens are designed for people who don't cook, no garage for a car/bike/tools, no backyard for kids or pets, and the walls are so paper thin you can hear your neighbours toilets flushing.

The one down the road from me was advertised for rent on the 8th August. Its still listed, and vacant. In a premium area as well. In contrast, since NACTNZ changed the interest deductibility rules there are a lot more older units for rent - ones with backyards, storage, garages, and full sized kitchens - all for $100 a week less than the new townhouses. I know which one I would be renting.

Landlords have been honorable in doing their bit for people struggling through the downturn by keeping rents at reasonable prices.

Kia kaha! 🥂

Is it really landlords' goodwill, or more about renters' willingness and ability to pay which dictates rent prices?

Disagree that theres any honor in it all... and with the lower OCR the proof will show when rents continue to rise despite lower rates ....

https://www.rnz.co.nz/news/business/520050/renting-is-very-expensive-nz…

This is clear evidence the many loss making Landlords are unable to defray holding costs. It always was and IS about the capital gains.

As a loss making Landlord, commenter "safeashouses" has already attested to this.

I am a loss making landlord at the moment that is true - and my assets are depreciating - however that is the game I am in- so when the wheel turn I can hopefully recoup some of the loss' and make a profit - this is the way business work.

Yeah nah.

Real businesses do better than that.

@redcrows - fair enough - when I do make a profit as I have before pls make a note to say well done:)

redcows

Definite nah on that.

Stas NZ say 63% small businesses are gone-burger after two years . . . only 37% survive beyond that.

Are you trying to reinforce my point about real businesses.

It really isnt, my business is 12% down in sales from last year, we just hired a new person to put us closer to the box seat when the wheels eventually start to turn again. We will still be profitable and paying tax this year. We are not reliant on asset appreciation to justify our existence.

Only 12% down? You're doing well.

@sluggy well I hope it picks up for you and best of luck. the thing we have in common is waiting for the turn. Yip also paying tax. Also all loss' of mine is ringfenced so not getting any tax back just fyi (there is not such thing as negatively gearing)

Ring-fenced or not, your losses can be offset against any taxes on future incomes.

Can owner occupiers do that? Nope. Renters? Nope.

Level playing field? I think not.

I don't see the clear evidence or know how you came to that conclusion based off this article.

all you are saying is rents aren't going up so landlords must be struggling.

What it does tell me is property yield is increasing, average price is coming down but rates are staying the same.

Here you go Rookie, evidence of 50,000 Landlords who enjoy topping up holding costs with their wages;

https://www.rnz.co.nz/news/business/529846/more-than-50-000-property-in…

i imagine most businesses make a loss in their first few years,

You can believe what you like however the reality is that a large proportion of Kiwis are growing increasingly fed up with the greed driving our housing market. As more people recognise the need for change, it’s clear that policies prioritising affordable housing and cracking down on speculation are on the horizon. The status quo won’t last much longer; a fairer, more sustainable future is inevitable.

People have been saying that for decades, all that’s changed from your perspective is that you are now one of them.

If landlords can cover costs - and most are more than covering costs - then they do very well indeed......

Capital appreciation over time is phenomenally good for residential property in New Zealand. And with mortgage interest rates now in sharp decline, the outlook for (net) rental yield is improving by the month.

The real concern is not for landlords - but for those with bank term deposits whose returns are now drastically falling. (Sadly, many of these are elderly folk who rely on the interest for their livelihood/wellbeing.)

TTP

Sadly, many of these are elderly folk who rely on the interest for their livelihood/wellbeing.)

Indeed, you're right - many do. Given there has been no relief from fixed cost of living pressures, this cannot bode well for retailers either.

Can I fix a bit that post for you TTP?

"Capital appreciation over time was phenomenally good for residential property in New Zealand."

It remains to be seen whether it continues. And I, for one, say it won't.

For example, I_O put up a good graph on NZ's private debt growth to GDP growth from 1991 until today. We hit a ceiling back in 2008 and it hasn't risen since. Thus, one could conclude that capital appreciation won't grow unless GDP does too. (take care with that statement btw)

Add to that constraint my favorite one - which is new density rules will facilitate many, many more dwellings to be constructed in desirable areas - and the fate of past capital appreciation trends is sealed.

If you can't do better than the above word-salad for a response, Chris, then no wonder you're of no fame. ☹️

Property is well-placed as an investment.

TTP

You forgot the caveat ... "under NZ's current tax system".

Re word-salad? Yeah. I'm sorry I don't have the time to make it better. Nobody pays me too. Unlike some accounts on social media.

We're nearing a tipping point where more Kiwis will see that this so-called altruism is nothing but greed disguised. Property investors may cling to their inflated profits, but the truth is becoming harder to ignore. The number of Kiwis who recognise the need for change far outweighs the few driven by greed who resist it. When the tipping point hits and the public demand can no longer be ignored, we’ll see policies that crack down on speculation and prioritise fair, affordable housing. It’s not just about protecting investments anymore—it’s about ensuring a sustainable future for everyone, not just a self-serving minority.

Maybe ex-renters have been buying some of those townhouses I see popping up everywhere.

I wouldn't own one of those for all the tea in China, in a few years time they'll be hovels. There's loads of them in Hobsonville, many with washing hanging over the balconies...like Hong Kong.

Let them eat cake! - Riverhead Boomer.

Preservation of capital begins with purchasing a desirable property in a promising area. A do-up even. Not a possible future slum.

Nope. Rents are steady because incomes are steady. Rents track incomes. Supply / demand makes a marginal difference unless there is an abundance of housing (Chch 2015) or a sudden population surge (Wellington 2019, Auckland late-2023). Check out Govt's rental affordability index - it's a flatline.

It appears that Infometrics has "discovered" that there are differences in incomes and rent affordability:

"Traditionally, housing affordability estimates use overall average household incomes. However, Census data shows that renting households have significantly lower household incomes than owner-occupied households. This difference means that using overall household incomes can overstate the ability of renting households to afford rents or to save a deposit to buy their own home.

Nationally, we estimate the mean household income was $133,800 over the year to June 2024. However, for renters, we estimate a mean household income of $104,800, which is 22% below the all-household average household income. For owner-occupiers, we estimate household incomes are slightly higher than the all-household average at $148,900. This makes a big difference to affordability calculations"

- Infometrics New ways of exploring local housing affordability, 25 September 2024, Nick Brunsdon.

I might also add that that $600 is paid out of pocket while Income figures are pretax. That does make a difference too.

I worked out the effect of the OCR cut on my modest property portfolio (most of which I built) and the effect is trivial. This is because the sum of all repayments are > 65% capital rather than interest. Which is turn is due to a) the age of the original mortgage and the b) the shorter terms I prefer (i.e. < 20 years).

So no rent increases for any of my tenants ... which makes it over 3 years since I increased rents.

I guess some will say that makes me a nice LL but a terrible investor. Maybe. But if you choose to label me a terrible investor, be aware that every property enables a substantial on-call overdraft while providing re-insurance capacity on which I receive a small stipend. ;-)

The humble brag is strong. Basically you got in when it was cheap to buy a property and subsequently cost to service is cheap. I'd like to think anyone with a moral compass would do similiar in your position.

Whats the size of your property portfolio and debt?

"Basically you got in when it was cheap to buy a property and subsequently cost to service is cheap."

The last place I bought was a few years before covid-madness. I buy, develop, then sell some, keep some. It's a hobby. I enjoy creating new stuff and the intellectual exercise involved in doing it well. And it distracts me from stressing about other less active activities. (Frank will understand. ;-)

I wouldn't label you a terrible investor. A know-it-all maybe but not a terrible investor ;)

It actually makes sense to reward good tenants with lower than market rents. The difference between landlording being a passive income stream or an every other weekend pain in the neck is perhaps $25 pw, or a two week longer vacancy rate looking for the right tenant. It's got nothing to do with being a nice guy.

That has always been my philosophy as a landlord and I'm a self-absorbed douchebag.

Thanks?

The nugget I dropped in has been missed by all thus far.

I really think the stall in median rent growth is down to an alteration in the pool. Since AirBnB now pay GST many of these cheaper out of the way baches are now in the rental pool. The return of interest deductibility has meant older houses with cheaper rent are being leased again after being on the sideline. Interest deductibility for new houses only skewed the rental pool to newer more expensive houses.

RP is entitled to his opinion, but I speak with A LOT of landlords and I am yet to meet a single one who has lowered his rent for a specific property. I'm sure it exists but for the most part, rents are increasing to match the increased maintenance, debt servicing, and rate costs.

I feel like there are so many different drivers affecting rental prices that it's impossible to attribute any single change as the driving force. There are probably other factors but, from a glance it seems like we have a few factors contributing to the flattening of rental increases, wages flatlining, immigration on a downward trend whilst emigration is going up, as well as interest deductibility bringing some older properties into the rental pool. All of these will have an effect but hard to say which one is the most impactful.

"I feel like there are so many different drivers affecting rental prices that it's impossible to attribute any single change as the driving force."

Keep it simple. There really isn't any mystery.

Incomes establish residential rents.

It's largely the same everywhere in the world. Has been for yonks.

Bingo

Incomes establish residential rents.

E46 is closer to the mark. Supply of and demand for rentals has the largest impact on price. Not everyone decides to spend x% of their income on rents. When rentals are plentiful the same person may bargain and play off multiple landlords. When there are multiple prospective tenants 'fighting' for a single rental they will pay asking even though their income hasn't changed. The percentage of a tenant's income that they're prepared to pay changes based on their perception of competition - not their income.

"The percentage of a tenant's income that they're prepared to pay changes based on their perception of competition - not their income."

Your "original research" is noted. Some will find it very valuable ... But ...

It's basically your opinion, right?

You've no hard, nor soft facts, to back it up? Right?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.