The national median days to sell hit 50 in August, the highest it has been in an August month since 2008, the Real Estate Institute of New Zealand (REINZ) says.

Meanwhile, the national inventory level surged 30% year-on-year in August, reaching 29,579 properties on the market. This was, however, down 977 from 30,556 in July.

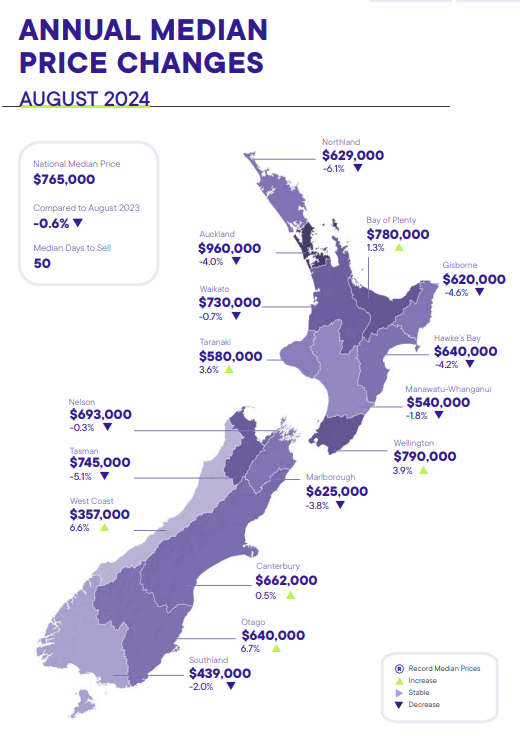

REINZ says the national median price dropped $5,000 to $765,000 in August year-on-year, but rose $12,000 from $753,000 in July.

The total number of properties sold fell by 40 to 5,685 in August year-on-year, and by 307, or 5%, from July.

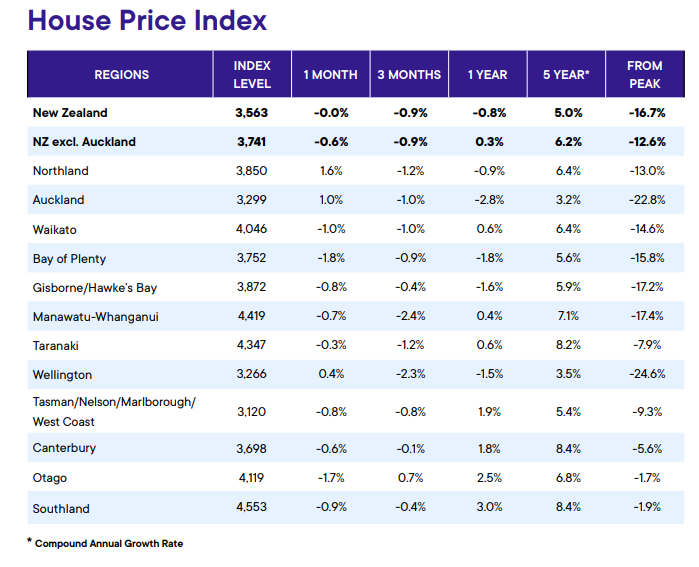

The REINZ's House Price Index, which is adjusted to account for changes in the mix of properties sold each month, weighed in at 3,563 in August, down 0.8% year-on-year, and unchanged from July. The HPI is 16.7% below the market peak reached in 2021.

In terms of the national median days to sell, it's the first time this has reached 50 since 2008 when it came in at 57. Interest.co.nz records show there've only been two other August months since 1992 when it has reached 50 or more.

At 50, it was up eight days from 42 in August 2023, and up one day since July.

'It would be an overstatement to say that we are at a turning point in the market'

"We continue to see an increase in the average number of properties listed. Although the inventory is down slightly compared to last month, the volume of properties for sale continues to provide a lot of choice for buyers," says REINZ Chief Executive Jen Baird.

"This month [August], we saw further signs of a change in market sentiment, with local agents reporting increased confidence in vendors and purchasers, the return of investors, and increased activity, particularly at open homes over the last two weeks of August. They attribute this change to the decline in interest rates. However, it would be an overstatement to say that we are at a turning point in the market - we merely have our indicators on. While there is a rise in optimism and confidence, we are hopeful that better times are still ahead," Baird says.

In Auckland the median price rose $10,000 to $960,000 in August from July, but was down $50,000 year-on-year. At 1,801, Auckland sales volumes were down four from 1,805 in July, and down 18 from 1,819 in August 2023. Median days to sell came in at 51 in Auckland, up 10 year-on-year, the highest in the city since 2001, and well above the 10-year average of 39.

REINZ says August standouts include Northland's 23% year-on-year increase in sales volumes to 173 sales, 13 regions recording an increase in new listings year-on-year, with Gisborne's increase at 69%, Marlborough's at 41% and Manawatu-Whanganui up 40%. Just six of 16 regions had a median price increase year-on-year, with Otago up 7% to $640,000, and the West Coast up 7% to $357,000.

Days to sell - REINZ

Select chart tabs

*The map and table below come from the REINZ.

143 Comments

What was going on 16 years ago??

interest rate dropped like a rock, and house prices only gone back to peak prices 5 years later.

House prices grew in the mid-2010s, as John Key himself pointed out, largely due to a combination:

- high net migration (more importantly, net outward migration of Kiwis hitting very low levels - ~3k a year in 2016 & 2017)

- cheap global energy commodities

- low interest rates

- China importing record volumes of dairy from NZ

So, on top of interest rate cuts, we need to lift export income, stem the outflow of skilled Kiwis and bring down energy prices for Kiwi businesses and consumers. Easy peasy, eh?!

Oh, and a minor detail: revert the foreign buyers ban

Spring and early summer were much colder in 2008. Seasonal climate is the number one driver for property sales.

If you were to overlay temperature/rain charts over property sales charts there'd be a direct correlation.

I was drinking 20 for $20 Double Brown cans at Year 13 leaver parties, and trying to hold it together the next morning at my Saturday job.

I think the economy was also in a bad shape ... something like that.

Is that you No.2 son?

GFC

Yep although things were deteriorating before the GFC with high interest rates, collapse of mezzanine finance sector etc

I can't remember yesterday let alone 16 years ago.

The global financial crisis.

Great news. Want to sell, drop them prices.

My mum is one of the many. Wants $900k plus. Personally thinks is actually only worth $500k tops, but expect it would go for $750k.

$500k is what they built it for 15 years ago.

Saw a post about a property asking for $550k with a rent appraisal of $870 per week (dual unit). Net cashflow deficit of $15k if 100% leveraged.

Basically, the price would need to either drop to $320k or interest rates fall to 3.5% to make it stack up investment wise. RV in 2017 was $230k for reference.

or rent increase.

Are you sure you calculated that right? 550k * 5.89% / 52 = $622.98 a week in interest. Or do you mean the amount you have to put in to pay the principal, if so that is not exactly a loss.

There are a lot of investors who would be prepared to accept a deficit in anticipation of interest rate decreases and eventual rent increases.

Maintenance, insurance, rates etc.

If you can pay cash for it or have a big deposit it's possibly worth buying though, although I note the 2017 RV which is low. Do you know where this property is and what condition it is? It doesn't seem legit.

Here you go. It's 8% gross so yes if you put cash down then it might make sense, but how many investors do that? Everything is about leverage.

And sorry, RV was $225k not $230k.

https://www.realestate.co.nz/42607073/residential/sale/98-pembroke-stre…

https://homes.co.nz/address/carterton/carterton/98-pembroke-street/q7NDX

Cheers, I see the CV as $400k (land value $215k) and it was last purchased in 2022 for $443k. It's awful it's come to this in NZ that we pay so much to rent and buy property, especially when like this one it is very old and in a small place like Carterton. Unfortunately renters there don't look to have a lot of choice and rents are high, there will be landlords taking advantage and it sucks.

The market in Wairarapa went a bit bananas from 2017 to 2021. The half decent rail service allows people to work in Wellington and live regional.

I bought my first home, an 80sqm 3 bedroom on 700 sqm for $200k. Traded up in late 2021 and sold it for just under $600k. Was up for rent a few months back asking $580 per week.

.

If they built it for 500k 15 years ago it will cost $1m to build today

And there in lies a real problem. Not just the inflation but the expectation of inflation. Inflation is not a good thing

More $750k today. (And could be less.)

"If they built it for 500k 15 years ago it will cost $1m to build today"

House prices in the existing dwelling market can and do sell below current construction cost / current replacement cost.

Then there's the well-kept properties built from native hardwoods which you could barely build the same these days due to lack of the same resources.

Depreciation. It probably needs lots of work.

Those who have been in property for many years/decades aren’t phased about the current downswing in the cycle.

After the longest upswing in living memory, a sustained period of falling property values was inevitable. The road to recovery was bound to have its twists, turns and gradients - but the underlying enthusiasm for property remains unabated…… One only has to consider the numbers coming here each day - in their relentless pursuit of property ownership and the long-term prosperity it brings.

TTP

Japan enters the room….

Amokk.

The big difference between Japan to NZ is you and I cannot become Japenese citizens we can't male a life there we have to leave at some stage. Even the Korean comfort women (and their children) who were taken from Korea in WW2 weren't allowd a passport or granted citizenship meanwhile here if you qualify you can become a NZer and build a life.

This is nonsense.

Article below about buying in Japan due to the recently introduced digital nomad visa that allows stays of up to 6 months. Not sure if her father's permanent residency played a part in her being able to buy though. Two especially interesting points in the article:

The ongoing costs - "fixed asset tax (rates) of around NZ$390 and insurance around $840". "Kininmonth-Deans says it is unlikely she will rent the house out. I would have to pay two lots of taxes, in both Japan and New Zealand.” Perhaps we could implement similar taxes?

https://www.stuff.co.nz/home-property/350321923/kiwi-buys-stunning-holiday-home-japan-123000

"Perhaps we could implement similar taxes? "

New Zealand councils charge these taxes on dwelling owners. They're called "rates".

Sure, but I read it as the rates (similar to our rates) are $390 (first quote). I assume (perhaps wrongly) that taxes may be applied in Japan as a disincentive to renting property out, I don't know, but the Japan National Tax Agency says "income from renting out real estates located in Japan is considered to be income from domestic source. If a non-resident is renting out a property, the amount of lease multiplied by the tax rate of 20.42% will be withheld as withholding tax". Maybe we could apply a tax like this to non residents like Australians who own property here. A quick Google finds residents are subject to capital gains tax on sale of a property and inheritance tax when a property is inherited, maybe we could learn something from the Japanese?

"If a non-resident is renting out a property, the amount of lease multiplied by the tax rate of 20.42% will be withheld as withholding tax"

How about this one?

"If a non owner occupier is renting out a property, the amount of the lease multiplied by the tax rate (subject to some related ownership expenses such as rates, insurance and maintenance being tax deductible) is payable" - that was the policy of the previous government in the existing dwelling market.

"maybe we could learn something from the Japanese?"

From a housing policy perspective (not a tax policy perspective), it might be better to learn something from the Singaporeans and apply it to the existing dwelling market :

https://www.propertyguru.com.sg/property-guides/additional-buyers-stamp…

Total nonsense, yes. The rule in Japan is the same as here: 5 years of residence to apply for citizenship.

The BIG difference is you can't have multiple citizenships in Japan, you need to drop the other one(s) you have.

Been to Japan lately? They have opened their doors to let young people to become PR and eventually Japanese Citizenship!

Been to Japan lately? They have opened their doors to let young people to become PR and eventually Japanese Citizenship!

Partly correct. Relatively easy to get PR, but Japanese citizenship is harder. If you're not fluent in Japanese language, you probably won't get it.

PR is far better. There's not much you can't do except vote.

So property investment as the hero's journey basically

@Three Veg - I would not say "hero Journey" however it worked for me - bought my first house @2011.

Today Gross = $3.25 Million & Net 1.2 Million (equity) Cashflow - $60k per annum on interest of 6.89 when interest drop to 5.5 Cashflow will get to -$12k.

Now if property prices grow at a modest 3 - 5 % per annum for the next 10 years well who knows that might be heroes journey? I am not spruiking just saying it does work. IF you know how to make Net 1.2 million in 13 year lettuce know.

bought my first house @2011

The key question is will the owner occupier buyers of today purchasing at today's prices experience the same level of house price growth and returns as the buyer in 2011 experienced?

The highly leveraged buyers of the 2020 - 2022 period expected that they would experience similar house price growth rates and returns of highly leveraged buyers in preceding 50 years.

For those that are unable to see the mathematics between the Peaker and the Buyer Today (BT).

For owner occupier buyers: CAVEAT EMPTOR. Beware of those with their vested financial self interests.

1) Peaker

The median house price at the peak for Auckland was $1,300,000

With an 80% LVR, this is a mortgage of $1,040,000

The 20% equity is $260,000

2) Buyer Today ("BT") - Aug 2024

In 2021, the buyer who waited, deposited the same $260,000 equity into a bank deposit earning interest. Also BT would rent an equivalent house and have still saved money due to the rental being below the monthly P&I mortgage payments of Peaker - in 3 years the savings would have been about $20,000 annually. So a Buyer Today would have an amount of $340,233 to use as a deposit.

The current median house price for Auckland is around $950,000

Equity deposit of $340,233

The mortgage at this purchase price would be $609,767 (an LVR of 64%)

The Peaker has a mortgage which is higher by $430,233 (mortgage of $1,040,000 for Peaker vs $609,767 for BT). BT's mortgage is 41% lower than Peaker's mortgage.

Assuming BT, pays the same exact dollar amount each year that Peaker pays for their mortgage, as a result of that additional borrowing, Peaker is paying $1,232,229 more over the 30 years than BT (This is due to higher borrowing amount of $430,233, and total interest on this of $801,996 over 30 years). BT is mortgage free by the year 2037, whilst Peaker continues to pay their mortgage until 2051 (14 years later) - so after the year 2037, BT can save all that money that Peaker continues to pay on the P&I mortgage.

Assuming same incomes, and same living costs (food, travel, etc except mortgage) , BT can save the total $1,232,229 in payments that Peaker is paying. If BT invests the annual P&I payments that Peaker continues to pay after the year 2037 at 4.0% p.a, then in 2051 this amount will grow to $1,401,500.

Remember that at the end of 30 years, the house price will be EXACTLY THE SAME for Peaker and BT.

BT will have more money available for retirement than Peaker. Conversely, Peaker will have less money than BT at retirement.

That single decision to buy in November 2021 would have cost $1,232,229 extra to buy the exact same house for Peaker compared to a Buyer Today.

For those who haven't noticed, the situation for Peaker

1) Nov 2021 purchase

The REINZ Auckland median house price was $1,300,000

With an 80% LVR, this is a mortgage of $1,040,000

The 20% equity deposit was $260,000

2) Sept 2024 situation

The REINZ Auckland median house price is currently $960,000, a price fall of 26.2%

Mortgage outstanding of $1,040,000 (assumed to be interest only for sake of simple comparison). The LVR is now 108%.

The equity is NEGATIVE $80,000

They are in negative equity, with a loss of 131% of their initial deposit, which is likely to be their entire life time savings. In less than 36 months, their entire life time savings has evaporated.

Can they hold on? If they are unable to hold on, then the loss may have to be realised (and they may still have an amount owing to their lender)

@CN New i bought two houses in Palmerston north in 2021? They have performing really well? Capital Gains and cashflow ..... One of them was a free standing house for $455k (now worth $645k as per homes) rent is now $600? once again not spruiking its just facts - how many thumbs up will I get for this probably negative 4? As mentioned not spruiking its in my best interest people don't buy and keep renting - If you want to make a move do it............

Out of interest, did you use equity for those two house purchases?

@26@Main - yes i did

Just to understand you more clearly.

So you borrowed against your existing property to use as a deposit to purchase the 2 properties in Palmerston North?

On your 2011 property purchase the current LVR is 63%.

"Today Gross = $3.25 Million & Net 1.2 Million (equity)"

@CN new the property i bought at 2011 is part of a porfolio now. portfolio value is 3.25mil -

now worth $645k as per homes

,,🤣🤣🤣🤣

i bought two houses in Palmerston north in 2021? They have performing really well? Capital Gains and cashflow ..... One of them was a free standing house for $455k (now worth $645k as per homes) rent is now $600

Each geographical property market has its own local and specific drivers.

Just out of interest did you rent out to community housing providers in the long term rental market to take advantage of the tax rules on interest deductibility that were in effect in 2021?

Or perhaps you rented out as student housing or Airbnb and able to claim an interest deduction in 2021?

Will you subdivide the land and build another dwelling on the site in future?

@ CN - a combination mostly I rent to working population as of late however, I have had community tenants.

(now worth $645k as per homes)

Homes.co.nz is in no way a fact peddling site, but glad to hear it is working out for you nonetheless. Wellington can only build out so much more so the lower north will all continue to get more an more connected and grow the smaller towns and cities as time goes on. With the new road completion between Wairarapa and Manawatu, smaller locations will become more attractive also.

@interesting1234 - thanks for the message i appreciate it - further more I notice see kiwirail commisioned (or is busy to commission) and inland port between palmerston north and bunnythorpe? work starts in 2030 it is a massive site of 2,4 kms connecting all Cental and lower North island freight in one massive hub with rail to wellinton and Tauranga i feel Palmy is going to really rocket along - disclaimer "i am just stating what i read" https://www.pncc.govt.nz/Council/What-were-doing/Strategic-initiatives/…

Whether it comes to fruition will be another thing, but fingers crossed. Rail connectivity and affordability would make life so much better, so says everyone living in the Wairarapa and Kapiti who can work in Wellington or from home multiple days per week with Wellington salaries.

Wellington salary here. Commuted for a few years from Wairarapa, but now I work from home 4 - 5 days per week.

The train was a $400 per month pass, easily offset by cheaper housing costs. Just makes for long days if you're doing it often.

A $50,000 initial investment in an ETF and $60,000 annual addition over 13 years at 6% net average return (you would probably do better than that), would give you $1.3 mil over 13 years.

Your numbers might work with 3-5% average growth over the next 10 years, but those numbers absolutely do not stack up with todays purchase prices.. So your anecdotal evidence of past performance really doesn't work as an argument supporting potential new investors jumping in now.

@1harlow1 = then I would say that is also a good option - it was just not the route I took - however it seems like great investment

It might be true that todays prices wont work (i just bought in Jan again) however it might - thats what i am concentrating on.

FTE's might also work I just don't know - i am just not spuiking FTE's (or property for that matter)

Just responding to your question, you asked if anyone knew how to make 1.3 million dollars in 13 years. I was just providing a very low effort and significantly less risky alternative that doesn't rely on leverage.

Also has the added benefit of not blocking young kiwis owning their home for your own financial benefit. You might say it's a win win situation.

@1harlow! everything you say is true. I also love the ethical argument.(i gave you a thumbs up for it).... Can you do me a favour and tell those young kiwis to buy now because there is no investors in the market, as far as i understand there is allot of houses for sale, or are they to busy eating avo or buying cars or blaming boomers or leaving NZ. Some older kiwis i know are not buying either. I buy and get blamed those who do not buy ...... well they can find 1000's of excuse? ***not blocking anyone there is no one at the open homes**** The way I see it if i say buy now i am spruiking if i say dont buy i am blocking?? can you sort out my ethical dillema?

Why would they want to catch a falling knife?

@powerupkiwi - not suggesting to catch a falling knife - by all means try to time the market in the mean time keep renting. In my experience the market will pick up and then the oppertunity missed might be cutting deeper than the slow falling knife.

That investment would also be spitting out dividends today, rather than being a cash drain.

And it would never phone you at night because the toilet is leaking.

subtle difference between does work and did work (in retrospect mind)

"While there is a rise in optimism and confidence"

Whose?

The most false confidence I’m seeing is from desperate agents and the highly leveraged who need sales and increasing prices again for their own self interest.

The yield curve is just starting to normalise from an inversion that is comparable in depth and duration as to just prior to the 1929 crash and subsequent depression. To be highly confident about the future given this would be delusional ( in my opinion) - but those who are highly confident right now probably don’t even know this inversion has occurred, nor what it could mean for how the economy functions of the next 12-24 months - and the impact it could potentially have on asset prices in the near future.

The history of yield inversions and comparisons to today might make for a highly educational article on here interest.co.Nz editors. Increase the financial knowledge of your readers who haven’t been educated in this area.

I would be interested in reading this. Have not had much exposure to the particulars of yield inversions.

Not all yield curve inversions resulted in a recession.

https://wolfstreet.com/2024/09/08/the-yield-curves-steep-inversion-now-…

All the more for an article I say to explain why the depth and duration of this inversion is quite significant viewed over a 100+ year time frame.

TA, OneRoof, the real state agencies...you name it 😅

oh dear, are we comparing now with 2008 already?

We must have already exceeded the price falls from 2008 and the recession hasn’t hit yet - it’s still ahead of us the next 12-24 months.

considering this cycle is engineered, it will all depending on how quickly OCR drops to neutral level.

If only the world was this simple.

I know, if only that

Yeah maybe we will see OCR cuts with a rapid end to the recession and a reinvigorated property market?

I feel the many hundreds that have lost their jobs or are currently facing job losses would beg to differ. My gut feel being one of them, is that we have pain to come.

Don't tell the spruikers and bankers that.

Lower for longer house prices are the trend.

I agree 100%.

The hurt locker door is ajar.

The realists like IO are wary.

The spruikers, who told many to buy in COVID highs are, are amongst us cheering on the OCR .25% as a landslide victory.

The fat lady isn't even at the auditorium

Carnage is coming. I see some of those areas with massive increases in inventory are areas with loads of holiday homes. This indicates mortgage stress of primary residences so the Bach needs to be offloaded before the bank sells it. We also have loads Homes just being completed off plan, that are worth 25% less than the owner signed up for in 2020-2021. This is probably going to get very ugly……and it’s just starting.

Surely people only buy a bach if they are in a good financial position

It’s the Bach they bought when they thought they were in a good position. Remember 2.99% interest rates forever.

Just like the cars, boats and other flashy toys people bought when they thought they were in a good position. Some excellent private sale bargains starting to filter through.

I need a jet ski and Polaris if you can point me to a distressed seller.

A fool and his money are lucky to ever be in the same post code...

People do stupid things with their money all the time, which is why the majority of people are not rich. The degree of leverage determins the outcome of the stupdity in terms of long lasting consequences.

Prioritize well being and happiness over material possessions...wise words indeed.

Golly. I'm doing something right.

Leverage can make you rich.

"Leverage can make you rich."

That statement is incomplete, so let's complete it. "Leverage can make you rich OR poor."

Leverage amplifies both the gains AND the losses. Many people are now discovering the latter part of that - the part that is frequently omitted by property promoters.

Some high profile names have recently been reported by mainstream media outlets.

"When the tide goes out, you see who has been swimming naked"

Haha or it can bankrupt you!

Haha or it can bankrupt you!

Reposted here as an example:

For those who haven't noticed, the situation for Peaker

1) Nov 2021 purchase

The REINZ Auckland median house price was $1,300,000

With an 80% LVR, this is a mortgage of $1,040,000

The 20% equity deposit was $260,000

2) Sept 2024 situation

The REINZ Auckland median house price is currently $960,000, a price fall of 26.2%

Mortgage outstanding of $1,040,000 (assumed to be interest only for sake of simple comparison). The LVR is now 108%.

The equity is NEGATIVE $80,000

They are in negative equity, with a loss of 131% of their initial deposit, which is likely to be their entire life time savings. In less than 36 months, their entire life time savings has evaporated.

Can they hold on? If they are unable to hold on, then the loss may have to be realised (and they may still have an amount owing to their lender)

"Haha or it can bankrupt you!"

Does anyone have a soft copy or link to the April 2012 issue of Property Investor magazine?

https://www.thepaepae.com/wp-uploads/2012/04/Dean-Letfus-NZPImag-Apr201…

{kind=link}

AirBnB allowed them to be able to afford to have a holiday home. With the AirBnB collapse, its no longer financially viable.

From what I have seen a "good" financial position can go to a "bad" financial position very very fast, especially at this current point in time.

"From what I have seen a "good" financial position can go to a "bad" financial position very very fast, especially at this current point in time."

"Everybody has a plan until they get punched in the mouth." - Mike Tyson

If they [believe they] are in a good financial position.

Once upon a time that might have been the case - when a holiday home was an expense. For some time now a holiday home has been the opposite due to rapid capital gains - hence many more second home owners that couldn't afford one in the past stretched themselves to 'invest'. All unraveling now of course...

There are also a lot of properties bought as AirBnBs - either wholly, or used partially to fund the holiday home use. Adding 15% GST on to the price has killed the AirBnB market, and they are too cashflow negative to be converted to long term rentals or the owners dont want to continue holding it if they cant use it as a holiday home. So they are being sold.

Adding GST has indeed killed the Airbnb market and along with it the income tax revenue the govt was collecting prior to this change.

I suspect adding GST to AirBnb was mostly about MPs favours for mates in the hotel industry.

Data from MBIE recorded international visitor numbers in 2023 at 76% of pre Covid levels, it's likely numbers increased this year but less international tourists will also factor in to less stays in Airbnb. I think anything that can reduce stays in Airbnb is a good thing, we've lived near properties that were taken out of the long term rental market and put on Airbnb permanently and that shouldn't happen.

@delboy. Was it ever a good idea to convert long term rentals/housing stock into short term rentals? All the evidence from around the world points to no - it wasn't. It was great for tourists, but we all know that tourism doesn't actually provide the amazing benefit to wider society that MP's and news outlets like to peddle.

Hotels and motels are exactly where tourists and travellers should be staying, Hotels full or busy then result in more being built.

The only areas that short term rentals should be allowed are places where there are no hotels or camp grounds. And yes - they should have GST attached.

With it taking so long to sell, the poor RE agents are barely making $1000/day on their commission. The poor wretches.

keep the bad news coming to fuel the rate drop.

It won’t make any difference. You have loads of people coming off low fixed rates in the 3-4 range, under water, who cannot afford even 5-6%. The situation is getting worse and interest rates will not go low enough to save them. There will be people coming off these low rates for a few more years, myself included. I have a 3% rate until the end of 2026. Between now and then loads of over leveraged under water property owners are going to face what is coming.

Link to the numbers for "loads of people " please?

Front page news a few days back where a RE estate agent was explaining how this exact same thing happened to him 250K loss, not able to settle, had to get second tier financing to finance the loss. He specifically talked about the fact that this was becoming more and more common as these developments are settled, the house is worth 20-25% of what they signed on for and they cannot pay. He explained the media are not reporting it, but it is common, and will ruin many peoples lives. To me that means there are loads of them around. I'm sure you can find the link, it was in the herald, on stuff and a few other outlets. I have seen similar stories, but not front page news.

Off the plan buyers getting caught out at settlement date.

Here is the article

https://www.rnz.co.nz/news/business/527578/wellington-real-estate-agent…

Mike Robbers of Lowe & Co Realty told clients last week that he and partner Socheata had signed a contract for a three-bedroom Wellington investment property which was not yet built in 2020.

At the time, ASB was offering a 1.9 percent interest rate for new builds and the expected rent would cover repayments.

"The market was booming, our incomes were solid and we expected that by the time it was built, our townhouse would be worth considerably more than what we agreed to pay for it."

But by the time the house was built and ready for settlement, almost everything had changed.

"Interest rates hadn't just doubled, they'd quadrupled. Rents had tanked by more than 30 percent - unprecedented. The townhouse was no longer a viable investment and completely unaffordable for us to consider keeping. But property prices had dropped so much, that the property was now worth less than the remaining balance required to settle."

He said, with their incomes also down, he was not able to get bank finance to settle.

"Whilst this sounds like a diabolical financial position to be in, it is one that many, many people found themselves in, caught by an unprecedented change in circumstances on multiple fronts. We ended up using a second tier lender to settle on the townhouse, then did some painting and styling and got it sold within four weeks for around a $200,000 loss."

He said the end result was that they had a bigger mortgage.

"This is such a common story at the moment, but you don't see it mentioned much, or the actual impact discussed. If 5000 New Zealanders did something similar to us - perhaps a conservative estimate - that's a billion dollars in equity wiped out over the last 24 months - if the properties have now been sold again at a loss, none of this is recoverable.

That's it. Thank you. He says many many people. I say loads. To me they are the same.

I read a tale the other day of someone's settlement date coming up, and they'd just got their notice they are being made redundant out of the blue (this does seem odd admittedly to come as a shock). They were due to see a broker about insurance for redundancy the following week, which now they can't get. There must be more like this around, but as we know, people don't tell you about their losses, only the wins.

Yup there have been 2 posts in the last couple of days on the FHB Facebook page. One just after signing the S&P agreement and the other recently bought in Auckland and is a single person paying the mortgage.

Must be nice to live in deliberate ignorance….

Rate cuts won’t be the saving grace you think they are in this climate, but by all means fill ya boots.

Days to sell now worse than 2022.

Remember what happened in 2022?

Best thing I did was cash out of the Auckland market in 2020 and get into Queenstown market - good quality houses are always selling in good time frames, the cheap stock on the fringes does ok due to high rental yields, there is always opportunities in the market regardless of conditions of the day - interest rate swaps trend averages indicate at least a 2% drop by Q425, I am picking a sharp 3.99% rate for 1 Year this time next year to spark the next cycle of recovery, until then steady as we go.

Arent the yields worse over there unless you are doing BNB

What? buyers returning yet again?

by wingman | 14th Jul 23, 5:11pm

NZ had a net migration gain of 65,000 in the year to March.. Many of them will want to buy, and many of them will be looking around Auckland.

He's been drinking too much of the fermented stuffs - the thirst-quenching Koolaid will be next..

Whoever counts on net migration gain to increase the number of buyers in the market is completely detached from reality. Only a tiny fraction of that 65k people would be cashed up straight away and meet the visa criteria to able to buy - I'd say not even 1%. For the rest, only a fraction will remain in the country long enough to become buyers and the ones that do stay will take years to have a deposit. Consider that most migrants come from countries with currency weaker than NZD, so whatever savings they have will reduce significantly if brought here. Then you think of how many of those who start from scatch would be able to save $30k+ per year to be able to have a 20% deposit in roughly 5 years.

Buyers return exclusively to Riverhead

Riverhead is up 5.8% in the last 12 months. (Since I bought there)

You wanna be rich.... or not?

Riverhead is up 5.8% in the last 12 months. You wanna be rich or not?

Riverhead Median sale price August 2023 = $1,499,659.00

Riverhead Median sale price August 2024 = $1,367,127.00

-7.5%

https://www.realestate.co.nz/insights/auckland/rodney/riverhead

Does this mean you're a bullsh-tter?

Depends if you're comparing YoY median sales values for a month, or the median sale price in the last 12 months compared to the 12 month's prior. I think that website uses the latter.

Change the chart to 3 years and you might see the discrepancy. There's a blip up from October 2023 to April 2024, so the median sale is probably in there whereas the previous 12 month's median price may be somewhat more subdued.

No. +5.8%. The SALE price is what counts.

https://www.realestate.co.nz/insights/auckland/rodney/riverhead

Where I bought, the signs are down because it's sold out.

No one ever got rich sitting on the sidelines yelling out "the sky is falling".

Every section comes with a commercial pump.

There’s a new subdivision called berryfields out of Nelson like this. So close to the water table the developers had to raise the ground by 3or 5m (cant recall the specific) and each section has a pump. I’m just waiting for a wee shake so i can break out the popcorn when the concrete block foundations crack, they develop plumbing issues and start subsiding 🤣

The graph within your link shows the median SALE price has declined over the last 12 months (as RP states).

Take a another look at that yellow line...

Go for a drive out West and check out what's going on.

All the way from Westgate to Waimauku. People get rich taking risks, but you're not amongst them.

You certainly took a risk… but it looks like you’re -$132,873 since your purchase.

I’m very familiar with Westgate and try to avoid it 99% of the time.

Wouldn't think so. I've owned lots of properties, I know what I'm doing.

I bought my property in Riverhead for $325,000 less than CV. The whole area's exploding, huge industrial subdivision over the motorway at Westgate, massive Kmart, Asian supermarket opening, SH16 widening, huge new residential subdivisions, traffic jams, thousands of cones, you are right, it's pretty chaotic, I'll give you that.

https://www.nzherald.co.nz/business/new-zealand-retail-property-groups-…

"I bought my property in Riverhead for $315,000 less than CV"

What percentage discount is that to the 2021 CV?

Around 24%.

.

If you think NZ prices are starting to look cheaper, have a browse at the quality and prices of property in well-to-do non-anglo saxon countries. e.g. away from the resorts, you can get a modern 4 bedroom house in a high demographic provincial french, spanish, or italian town with a pool and acreage for 600k. I'm not suggesting you move there, but does it really make sense to pay more than twice as much in NZ, when we are operating in the same global market with free flow of capital and the same standard of living? (try https://www.french-property.com/ or https://www.idealista.it/ for example).

The good news and good data continues to pile up. Pointing towards hope for future generations in relation to owning a home.

Auckland central HPI up 2% on the month.

Who knew lolz 🥂

Demand for apartments. (low prices make for low / short mortgages and faster equity accumulation - some FHBs understand maths)

You are obviously a genius, so you'll know that Auckland Central also comprises suburbs such as Westmere, Gay Lynn, Ponsonby etc.

You'll also be well aware that the HPI adjusts for compositional elements.

Cheers!

What you say is true. But my statement is also true.

Oh the glass one eight full man is back.

Auckland central medium was down 14.5% last month , not much of a bounce

Agents clutch at straws to justify above market prices.

eg they say interest rates are falling whereas the average interest rate on all loans hasn't peaked yet and is still going up due to existing loans coming off low rates onto higher rates. I hear about it at the office water cooler about once a week of people refixing. We are still paying for the mistakes of the Reserve Bank Governors decisions in 2020 and 2021 unfortunately.

Links to REINZ property reports here:

https://www.reinz.co.nz/Web/Web/News/News-Articles/Market-updates/REINZ…

The REINZ House Price Index for Lower Hutt has reached new lows.

From the peak, it has fallen 30.4% (before the impact of inflation). After adjusting for inflation, the REINZ house price index for Lower Hutt has fallen 39.1%.

For property buyers on a 80% LVR at the peak, they are now in negative equity.

An example:

1) At peak

Peaker nominal house price: NZ$1,000,000

Mortgage at 80% LVR: $800,000

20% equity: $200,000

2) current situation:

Current nominal house price: $696,000

Mortgage:$800,000 (assumed to be interest only for sake of comparison)

Equity: NEGATIVE $104,000 (loss of over 150% of their equity)

Friday the 13th horror!

the map shows Auckland a 4% fall but the table chart say 2.8% fall

making it crystal clear the Auckland medium

In Auckland the median price rose $10,000 to $960,000 in August from July, but was down $50,000 year-on-year.

implying that the August 2023 price was 960k + 50k or 1010k

960k vs 1010k is a 5% fall

So there you go, keep the report till Friday then hose numbers, who cares its happy hour

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.