The number of first home buyers getting into a home of their own is on the rise. But the average price they're paying, and the amount they're borrowing, are declining.

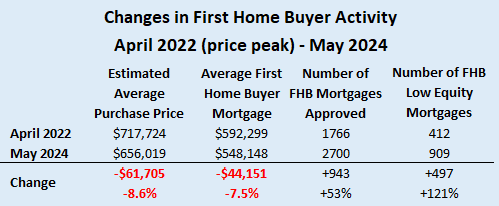

Interest.co.nz estimates the average price paid by first home buyers was $656,019 in May this year, compared to the market peak of $717,724 in April 2022.

That means on average first home buyers were paying $61,705 less to get into their own home in May this year than at the top of the market just over two years ago.

There has also been a corresponding decrease in the average amount they're borrowing over that time.

According to Reserve Bank lending figures, the average size of mortgages approved for first home buyers when their prices peaked in April 2022 was $592,299. By May this year that had dropped to $548,148, reducing the average size of their mortgage by $44,151 (-7.5%).

Over the same period, the number of mortgages approved for first home buyers has jumped from 1766 in April 2022 to 2700 in May this year.

However, there has also been a jump in the number of first home buyers purchasing their first home with less than a 20% deposit.

At the market peak in April 2022, just 412 (23.3%) of the mortgages approved to first home buyers were higher risk, low equity loans.

In May 2024 that number had more than doubled to 909 (33.7%).

So the number of first home buyers with less than a 20% deposit has risen from roughly a quarter to a third over the last two and a bit years.

So to summarise, over the 25 months to May this year, more prospective first home buyers were getting into their home, and on average they paid significantly less to do so and were also borrowing less.

But more of them, both in terms of their absolute numbers and the percentage of buyers, were buying with less than a 20% deposit and were taking out higher risk, low equity mortgages to seal the deal.

- The comment stream on this story is now closed.

•You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

142 Comments

Great news. Well done Chris Bishop.

Chris "tobacco man" Bishop put interest rates up?

Did he campaign in lowering house prices?

No he did not.

By all intents, the Nats were going to save the Rapacious Landlording class from losing their gold chalices and top 10% social class.......

Now the landlords are being chucked to ravages of the housing crash wolves and their riches are no longer the mega-minting presses they believed would be and enabling riches forever forward.

Oh well, a much better NZ WILL EMERGE, FROM THIS EPIC HOUSING MARKET CRASH.

National will gain more voters when renters start to gain more independence.

Do you thank your clock for making the sun set at the end of the day, and for making it rise in the morning?

Gotta hand it to them... taking credit for a collapsing economy.. like it was always their goal.

Next they are gonna say they WANT us to have nice warmer summers .... thus climate change is a target.

Dunedin wanted to change their town logo to

Climate change , Bring it ON !

or so the story goes....

No, it always was going to collapse, but what they hopefully will be able to take credit for is increasing supply without getting a corresponding speculative rise in prices.

That still has some course to run but if you look at the median multiple Median Multiples | interest.co.nz it has been tracking steady, with no dead cat bounce, but there is enough waste still to be trimmed in the system for it to decline further and then remain stable over the long run.

Surely this is a joke?

Yes!

The flop, flips

Good on them, buying a house, getting on with life and not whining on about it on here for the next 10 years.

wow i couldn't have put it better

How should people in their 20s/30s think about buying a home?

https://www.youtube.com/watch?v=b9g9LBMRVHc

All FHBs should watch this 3 mins of wisdom from Prof Galloway & Morgan Housel

It would certainly help them avoid rookie mistakes

"Don't put off till tomorrow what you can do today" Benjamin Franklin.

You could spend your whole life waiting... make a decision a pursue it.

The time to buy is when you can afford it.

Learn from your own mistakes.

Old Uncle Benny also said:

"An investment in knowledge pays the best interest."

lf you're buying now because you think you are wasting money renting, you really haven't got a clue

He also said

"Well done is better than well said"

actually he has a lot of quotes...

But let's acknowledge that many posters on here have never seen a real bear market, in anything. They haven't experienced how terrifying it is when a market gaps; when there are no buyers for what you have to sell, at any price. It's only then, they realise that no wise saying from the past helps in the slightest.

hold hold hold.

I hope no one gets to the point they are forced to sell, of course there are situations.

Some people have to. They have no choice. And when that happens, it affects the price of all other properties around them. Example: A new-build property in a number of similar properties is defaulted on by just one contracted buyer. The developer assumes the property back, and sticks it on the market to clear it from his books at 20% less than the original contract price; keeps the deposit, in other words. Those other buyers have to go to their bank to get finance. Guess what price the banks use to assess the lending? And that's when it snowballs, and some can't hang on.

Yeah... there are always reasons to have to sell... divorce, death, work relocation, finances.. and as you say that sets the new price for similar houses.

Got to ask you Rookie, how old are you ? You sound like you are in your 50's so if you are only in your 30's you have really got it together with your thinking.

My guess he's one of the spruikers who got banned reincarnated under a different persona to try to reinflate the spruikers narrative. TTP was caught out doing this a while ago. Sounds very much like HW2 to me.

100%

HW3

Honestly I don't know what a spruiker is, I don't really care.

I don't care about narratives OR useless comments.

And I don't know who either of those people are, think what you want

Honestly I don't know what a spruiker is, I don't really care.

I don't care about narratives OR useless comments.

And I don't know who either of those people are.

I'm 31.

Thanks Zwifter! Personally think I have a long way to go.

It's good too see some people on here with different opinions

A very large proportion of New Zealanders have never seen a proper bear market. And I would say more than 90% of people never thought there would be one, whether they are spruikers or not. And of course all the vested interests, economists, media and spruikers have continuously pushed the narrative that there could never be a true bear market in NZ property.

"A very large proportion of New Zealanders have never seen a proper bear market. "

Prior to Nov 2021, almost all New Zealanders had never seen house prices fall more than 10% and believed it could never happen in NZ. Numerous reasons were given by those with their vested financial self interests. This belief led many to buy residential dwellings using high levels of debt and led to the largest asset bubble in NZ when house valuations peaked at $1.76 trillion. The loss in market value in the residential property market is more than 150% of the value of the entire NZ stock market.

Yet those with their financial vested self interests continue to refuse to acknowledge the asset bubble (due to the continued vested financial self interest).

Has there been any mention in the main stream media in NZ of a housing price bubble?

House prices in Auckland and Wellington have met high profile property promoter Ashley Church's definition of a house price crash.

You could reword this as "Don't do due dilligence or make financial decisions based on logic, use your emotions".

"Don't do due dilligence or make financial decisions based on logic, use your emotions".

Many buyers were using logic. However it was their assumptions that subsequently proved to be incorrect.

A reminder of the reasons why house prices won't crash - the reasons given seemed to be logical, rational and plausible at the time and they also proved to be wrong. What did they not see? What did they miss?

1) May 2021: Ashley Church: We're deluding a generation of Kiwis with talk of house price crashes

https://www.oneroof.co.nz/news/ashley-church-were-deluding-a-generation…

2) Nov 2021 - Here's why it might be fruitless to pin your hopes on a house price crash

https://www.stuff.co.nz/business/300449314/heres-why-it-might-be-fruitl…

3) Dec 2021 - Tony Alexander - 19 reasons why there's no crash

https://ndhadeliver.natlib.govt.nz/delivery/DeliveryManagerServlet?dps_…

4) Feb 2022 - Ashley Church: Don’t expect higher interest rates to crash the housing market

https://www.oneroof.co.nz/news/ashley-church-dont-expect-higher-interes…

5) April 2022 - Ashley Church: Four reasons the housing market won't crash

https://www.oneroof.co.nz/news/ashley-church-four-reasons-the-housing-m…

6) May 2022 - Ashley Church: Do we now have evidence of a housing market crash?

https://www.oneroof.co.nz/news/ashley-church-do-we-now-have-evidence-of…

7) July 2022 - Catherine Masters: Why the New Zealand housing market is nowhere near crash point

https://www.oneroof.co.nz/news/why-the-new-zealand-housing-market-is-no…

It's funny how after the fact many claim FHB that bought at peak should've done their due diligence and homework. One would do so by seeking out the commentary of "subject matter experts" I would've thought?

The very subject matter experts that you have listed in your comment. I guess if you look close enough, you'll see "Comment and Opinion" as one of the many hashtags on Ashley's articles.

The time to buy is when you can afford it.

Rookie investor living up to their name. If they could have afforded it in 2021 would that have been the time to buy. I suppose if you don't mind overpaying by at least 30% then that is all good.

It's funny though, I've never heard a successful investor say buy when you can afford and lock in 30% loss. Rookie must be onto another secret winning investment formula.

"The time to buy is when you can afford it."

That line of reasoning is potentially financially fatal under conditions of record low interest rates (i.e 2020 - 2022 period).

That is how many of the highly leveraged buyers of that period are going to get caught out with mortgage interest rates rising from 2.25% to over 7.00%.

Agnostium

hhhhmmmmm! maybe you've never heard of Warren Buffett?

https://awealthofcommonsense.com/2020/03/even-warren-buffett-cant-nail-the-bottom/

Also you don't lock in a loss unless you sell.

"hhhhmmmmm! maybe you've never heard of Warren Buffett?"

As a long time follower of Berkshire Hathaway, it is extremely unlikely that Warren Buffett or Berskshire Hathaway would be buying any residential real estate at current market prices in any geographical market in NZ.

he bought stocks that dropped more than 30%

"he bought stocks that dropped more than 30%"

That's an interesting interpretation on why he bought.

Keep learning RookieInvestor. Your comment shows that there is a lot that you don't know that you don't know.

he bought because he saw value in it, and to him it was worth more than what he paid.

LOL

Do you think Buffet was giving advice about the NZ housing ponzi during the largest and fastest interest rate increase in 30 years?

And the longest yield curve inversion in history?

While sales are at a 14 year low?

And while sale stock is at a 14 year high?

hhhmmmmmmmmm!

This is a useless comment as NZ housing is not a ponzi, survival of NZ housing does not rely on the next person paying more than you did.

Although that does happen, just becasue the prices go up does not make it a ponzi. start thinking for yourself on stop just copying what other people say.

discounts!

New account but same blind faith housing trolling if the face of blinding reality unfolding. #ignore

must be striking some nerves since they are the least ignored comments.

Maybe its HW2, the Spruikers look stupid after they say buy then the market falls 10%, so they start a new account. I reckon we will only have to put up with rookie for 12 months, he will have blown his load every month and have not credibility by then.....

what was your view on property this time last year , the year before and the year before that? why did you not buy back in 2021?

HW2?

This is my 1st account i can assure you.

No I bought last year in July.

I have been trying to buy for 6 years but could never afford it, maybe i think housing is affordable because i managed to get something i considered cheap? IDK

I'm a FHB

I don't mind having no credibility here, there is no reason to try impress people here.

I'm here to open myself to new ideas and perspectives so i can form new opinions.

Its just some people here have stupid opinions and some have good ones, its just trying to filter who actually knows and who is following the crowd.

"I bought last year in July."

Just out of interest:

1) in what area?

2) at what percentage discount to the registered valuation?

3) financed at what LVR?

1) hamilton

2) 8%

3) 80%

What is the debt to household income ratio?

Does that include a spouse who is non working and needs to look after the children?

DTI is 4:1

Single income.

"Single income."

Good for you.

Have you also got some flatmates / boarders?

Did your mortgage broker suggest to you to put down rent from flat mates, boarders in your mortgage application?

Good for you.

Thank You!

I have a flatemate.

I cant remember if they suggested it. but I specifically asked for that not to be included in the application because i wanted to make sure it was affordable without it.

I may disagree with you on some things in terms of now being a great time to get into property, but it's good to hear that some are still getting a 1st house at a manageable price in the current climate. Congrats on the house.

That's fair, I can see how its much less affordable for people with children.

I do love a good argument.

I appreciate it!

Also congrats, I've been following your comments and they're consistent re: your age, that you bought on a single income and you bought outside Auckland. I was also looking at houses for sale in Hamilton the other day and they weren't as expensive as I expected given Hamilton's proximity to Auckland. I had one more question, feel free not to answer it though, what field do you work in or what is your salary range, as I say, happy to mind my own but just interested on how a single FHB does it, but well done.

Thanks,

I'm a mechanical engineer on 95K.

The hardest thing is building a big deposit.

Kiwisaver is the most important.

Kudos, your family must be really proud of you. Thanks for providing context around your first home purchase. You'll pick up some valuable information and opinions from this forum from those who have been around the block a few times and you'll work out which posters it's best to be sceptical of. Good point about Kiwisaver, it helped us also, although being able to access it to buy a first home has probably helped to push house prices up too.

And you too!

Yes it is debt to household income.

RI, don't bother. These sad, negative people struggle to believe that there is more than 1 person thinking differently than them. So they try to convince themselves that you must be someone else they didn't agree with in the past. How pathetic.

The more people who are scared to do anything and haven't achieved anything meaningful in life, tell you that you're wrong, the more you know you're on the right path.

It's just like the anger at people that have investment property, it's only jealousy.

The time to buy is when you can afford it.

Is surely a nonsense statement ...

The time to buy the most expensive asset most will ever buy should depend on a host of factors some specific to the individual and some to the market conditions.

For most people it has to be a balance of buying at the right time, in the right place, with the right risk, at the right price, with the right lender.

Your statement is kinda like boeing saying the time for their starship to take off is when it can actually reach the space station without accounting for the risks of not being able to return to earth.

Nonsense.

If your car dies and you have no other means to get to work, if you can afford it would you purchase a new one or start renting one, in case the prices come down?

Id buy one

This might be your worst take on interest.co.nz

A house is a speculative asset which you make a decision on buy or rent based on your projected gain or loss, plus the cashflow impact and externalities such as quality of life.

A car is a depreciating asset which you buy based on your requirements and financial means with the understanding that it will be a guaranteed loss, which is covered by the value it brings in the form of ease of transport and access to employment and pleasure.

The analogy of a car purchase is completely unrelated to a house purchase.

Also, you could just catch the bus if you want to be pedantic, which would be the actual reasonable option until you buy a car. Why would you rent a car to save money instead of public transport? Mind boggling. It's like saying you'd airbnb until the property market has gone down.

you could catch the bus, or bike.

some people choose not to because a car provides freedom, it comes down to what you want, and if the situation is suitable for you.

and can you afford it?

You're picking at minor details.

It was an idiotic analogy and they called you out on it. That's not picking minor details.

Well said

If you get turfed out of your rental because the landlords are selling up would you simply go and load up on debt and buy a house at 8x DTI when the mortgage would be more than the rent? No, you would find another rental.

you couldn't afford a DTI of 8:1

I suppose it depends on what is available to buy, what price and one's personal income level. Who would buy at 8x DTI currently when prices are slipping away.

Here is another car analogy, if Toyota gets more people wanting to buy a new car, do they keep supply the same and let prices rise, or do they increase supply and hold prices level?

They increase supply of course as they know one of the very reasons people were buying their car was based on the price and by increasing supply their margins are improved by economies of scale.

That is why if the Coaltions housing initiatives are allowed to succeed, then as demand increases, supply will more easily be able to match, and thus there will be no speculative unearnt gains.

But there is easily another 10% to 15% that could be trimmed from the present prices without affecting the amenity value.

Hey look I can afford to buy a Lambo. Guess I should just buy one right.

If that's what you need to live your life. And you CAN afford it. Do it

I could.

Wait FHB's or you to will see an erosion of your equity over the next many months.

Owning a house is not mutually exclusive of having the desire for affordable house prices in NZ.

Your comments around house buying should come with a disclaimer Zwifter: deposit given by parents and also given money to pay off mortgage.

What does that matter ? Anyone with parents that got ahead and paid off their house in the 1970's will usually give you a head start with a house. My father was given an even better head start, he was given a house in the UK. Just because I was given money doesn't matter, you can give an idiot a million bucks and in less than 5 years he will be broke again. I could have pissed it all up the wall and spent it all on hookers and blow, I know someone who did that, he is still renting.

It matters because your comments often show a lack of awareness of how much easier it was for you to buy because you were given a house deposit. Your parents were also there to bank roll you if you got in to financial difficulty, not everyone has those same advantages. Also, and importantly, what year did you buy your first house and how much did it cost? It was likely a long time ago and you would have borrowed a fraction of what FHBs need to borrow today and your risk was so much less because your parents were your back stop.

"not everyone has those same advantages. "

A single relative who is in their mid 40's, without any children and a university graduate is unable to afford to buy in Auckland despite a relatively frugal lifestyle (they are a saver)

1) they rent their current accommodation and do not live rent free from family so it takes longer to save for a deposit.

2) their borrowing power as a single person does not allow them sufficient amount to finance a purchase in Auckland.

3) their parents died without any assets so there was nothing from their estate to use as a deposit on a purchase of a residential dwelling.

If the previous commenter was in the exact same situation, would they be able to purchase at current market price levels?

"If the previous commenter was in the exact same situation, would they be able to purchase at current market price levels?"

No. I seem to recall that in the past, he's tried to spin some yarn about how he didn't earn too much, saved x% of it, and was able to buy a house.

Another commenter ran the numbers through a "what could I borrow?" calc and pointed out that the amount he could get with a similar income wasn't even half of what many young people are asked to spend today...

Zwifter: are you suggesting ranting on the comment section here, posting 25 times a day, huffing and puffing is not a productive use of one’s time. Maybe actually doing something is a better idea.

You may have a few of the dedicated, strongly disagreeing.

Zwifter : “Good on those people for buying a house and getting on with life and not whining on here about it.”

RookieInvestor : “wow I couldn’t have put it better”

Zwifter & RookieInvestor : have now purchased their first homes and continue to spam the comments whining about people that haven’t purchased yet or have opposing views to theirs.

I never whine about people who have purchase theirs, I would encourage them.

I would also say don't rely on government to allow you to afford it, there are other ways you can get started.

I hope that anyone who has a goal can achieve it if they work for it

I will argue with people that oppose my views, as does anyone, if you change my mind... well done, your opinion must be valid.

it would seem house prices ARE affordable.

average sale price 656K

Assume 10% deposit

Average household income 120K

DTI's are under 5:1

How many FHB earn around 120K themselves?

Probably not many... thats why average household incomes are referenced. 2x 60k incomes- sounds about right for a FHB

If any. How many dudes you know got the skills to go and rock a show like this?

Most.

Assuming a 10% deposit means you need to assume a higher interest rate and servicing costs than a standard 20%, so your DTI of 5:1 doesn't translate to the same affordability you would typically expect.

Deposit 20% with DTI of 5:1 has lower interest rate than deposit 10% with DTI of 5:1.

If you have a 600 grand mortgage and earn 120k, your life is very bad.

Rookie is like all other speculators in denial - not considering the wider economic picture at play. Cherry picking data and finding generic quotes to fit the narrative that now is always the best time to buy.

Get on with your lives, stop whining, buy now, look affordability is great!

it would seem house prices ARE affordable. Average sale price 656K. Assume 10% deposit. Average household income 120K. DTI's are under 5:1

🤡 What sort of DTI calculation are you making up to try to determine affordability? Average household income against average mortgage sold to FHBers?

It's spruikers like you HW2/TTP/ whatever alias you're using this time that are responsible for suckering the FHBers at the peak. Please stop.

"It's spruikers like you HW2/TTP/ whatever alias you're using this time that are responsible for suckering the FHBers at the peak. Please stop. "

They're unlikely to stop.

The property promoters need to earn income for their business and to pay for their living costs and put food on the table. It's a case of business and personal survival. Its the vested financial self interest motivation, and as a result of that motivation, there will always be collateral damage.

With the levels of negativity on these forums I’d doubt any property promoter would waste time trying to convince FHB’s here…head over to some happy clappy facebook page would be a way better spot for them…half the jokers here are determined the ole box of sticks is going to be lucky to be worth a cow & magic beans in the coming months 😂

"I’d doubt any property promoter would waste time trying to convince FHB’s here…head over to some happy clappy facebook page would be a way better spot for them"

Easier to persuade uninformed, uneducated, ignorant, miseducated, misinformed, financially illiterate potential buyers to transact. Here are the commonly repeated marketing phrases used by property promoters:

1. there is a housing shortage so house prices will continue to rise

2. population growth drives house prices, and population growth will lead to more shortage of houses / immigration will lead to house price growth

3. property prices double every 10 years

4. house prices rise faster than inflation / real estate is a hedge against inflation

5. property prices always go up in the long term

Some other beliefs about investing in real estate:

a) Buy land, they're not making any more of it / there is a finite amount of land

b) Time in the market is more important that timing the market

c) Landlords grow rich in their sleep

d) Owning a home is a keystone of wealth

e) Don’t wait to buy real estate, buy real estate and wait.

f) The best investment on earth is earth.

g) 90% of all millionaires become so through owning real estate

h) Everyone wants a piece of land. It’s the only sure investment. It can never depreciate like a car or washing machine. Land will only double its value in ten years

i) Buying real estate is not only the best way. It is the quickest way and the safest way, but the only way to become wealthy

j) Real estate is an imperishable asset, ever increasing in value. It is the most solid security that human ingenuity had devised. It is the basis of all security and about the only indestructible security

k) Land monopoly is not only monopoly, but it is by far the greatest of monopolies; it is a perpetual monopoly, and it is the mother of all other forms of monopoly.

l) The best time to purchase a house was 20 years ago and the second best time is now

m) No one has ever regretted buying property / have you met anyone who has regretted buying property?

n) you can never lose with property

o) you never go wrong with bricks and mortar

p) house prices always go up / never go down

q) rent is dead money

r) people should own their own home over renting

s) everyone needs somewhere to live so property will always be in demand and property prices will rise

t) there is an underlying housing shortage so property prices will not go down by much

Which is why I prefer the following 10

1. never trust a real estate agent

2. housing is a long term investment that provides secure housing first and foremost

3. always do significant due diligence (including builders, engineering, geotechnical & waterway reports) and never trust others reports

4. covenants will always be more damaging in the long run to living needs, lifestyle & future development

5. always have insurance or money built up for significant unexpected costs (e.g. re-roofing, modifications, rewiring, interior design elements e.g. gib & carpet replacement when needed etc)

6. never consider CV or RV an actual value or close to market value, always get at least a simple analytical appraisal

7. never consider market values as money you have or have earnt

8. don't buy in areas that have significantly dysfunctional councils or councils hostile to living needs, resiliency & access. Long term this often makes it more problematic to live in an area.

9. keep up with exterior maintenance to prevent leaks

10. never leave your property empty and unchecked for a long time

Jeez it will be the next economic cycle by the time I’ve finished reading that 😉…it will be fascinating to see how the next 12,24,36 months play out. If lending becomes more affordable & businesses get more confidence giving people more job security then I struggle to see the almighty collapse happening (well, worsening considering prices have had a pretty hearty drop already). But, maybe they don’t cut & things do get worse & prices continue to fall, I’m not sure. Personally, I’d love to see lending become more affordable again to keep the wheels turning but with tighter DTI’s, especially for “investors” to try & limit price growth.

Bishop stated he want houses to be in the 3-5:1 range.

That is literally what DTI is, DEBT to INCOME

Debt = 600K right?

Average income for a household is 120K.

5:1 debt to income ratio.

Sorry i had to explain this to you....

"Average income for a household is 120K."

For the record:

The new housing minister has set a target of having homes costing just three to five times household incomes

Average income for a household is $120,000 (based on the number provided above)

Homes costing $600,000 (5x household income)

20% equity $120,000

Mortgage: $480,000 (this is a debt to household income of 4x)

does that mean the median house price of 600K or that there are homes available for that price?

"does that mean the median house price of 600K or that there are homes available for that price?"

Ask the Minister of Housing for clarification of their statement.

What do you think champ? One house available at 600K and suddenly we have affordable houses. 🤡🤡🤡🤡

there are plenty available for under 600K. pal

But not where there are jobs and median household incomes of 120k.

I guess those 120k median household could just commute to Auckland from Taihape every day.

Ofcourse there this! Maybe if you looked outside of your small.... box

Travel near the distance of half the island there and back again... been there, would not recommend it long term on a daily basis. I take it this would be ok if the work was truck driving and you could sleep on the road at stops (like the second defacto partner's place) before the return trip.

With all the shitty townhouses being built, median will be 600k in no time

No he is quoting this: Median Multiples | interest.co.nz

The median household multiple is lower than the DTI ratio for obvious reasons but the DTI is useful for banks because they are the ones lending the debt.

FYI, throughout NZ, the following geographical areas have a house price to income ratio of 5 or below:

1) Invercargill (4.35x)

2) Timaru (4.70x)

3) Whanganui (4.78x)

Yes, I am very familiar with the median multiples.

The real point is that incomes in these places are close to the average, and the cost to build is very similar anywhere in NZ, then the difference is caused by the land price in these areas. Which can easily be checked by going on Trade Me etc.

The reason is that there is plenty of supply, which the council is keen to promote given they want, not only the extra rateable population but the development levies they receive to help upgrade failing existing services. The councils never say these subdivisions are not paying their true costs, they are grateful for the money they invoiced for.

Having developed also in small towns, a common extra the developer had to pay was an upgrade of a local pump station with way more capacity for the new subdivision, which then allowed the council to better support failing existing infrastructure.

Yes great news for the current and aspiring FHBs.

The better news, is the much longer they wait, the much, much cheaper it will get.

Good on minister Bishop for pursuing cheaper land and building costs!

What a Rockstar!!

Cheaper housing prices and lots more housing options will give the NZ economy real growth into much more productive business into the future.

The Rapacious rentier class won't like it, tough tities.

Even in a share market crash, there are buyers all the way down

Would it be fair to say that a share market crash would disporportionately impact the higher end of the property market, FHBs wouldn't be as likely to hold share portfolios.

Basically everyone with a Kiwisaver has a share portfolio, and many FHBs are planning to use that as part of their deposit. Even a conservative fund will typically have 20% or so in equities

I understand that, but if you are ready to purchase a house or close to it would be reasonable to expect you are not in a high growth fund/high risk fund and as a result largely not invested in equities.

In contrast, a wealthy individual would more likely hold a large portion of their wealth in a portfolio of equities relative to said first home buyers.

Cash doesn’t and returning 6% for a while now

Servicing costs still painful.

Don't mention about that party crasher guy, Unemployment!

2 incomes required to pay mortgage = double the risk of SHTF re. loss of job

and no offspring allowed = no ####.. Life is fun when you are a FH owner!

I’m largely invested in property and work in the property industry but I’m happy to see prices coming down and FHB’s getting a look in. The market seems to be adjusting (albeit slowly) to the new interest rate environment.

Personally I think we might continue to see prices drop another 5-10% until interest rates start heading down. My view is the bottom will be found over the next 6 months.

JamesM

What are you seeing in your property activities, particularly on the lending side?

From memory, a little while ago you were seeing commercial property owners facing cashflow stress and debt covenant stress with their lenders.

Have you considered diversifying your investments given that your entire livelihood is exposed there?

Some of us encouraged FHBers to wait to buy and borrow less as the marked turned in late 21. It looks like the reversal has some time to go as evidenced by more stock on the market and less sales. Renting a bit longer will mean you borrow less when you eventually buy. Paying interest is equivalent to paying rent to a landlord. When you buy a home the Bank is your landlord who has amazing rights as the mortgagee. The less you borrow the lower your rent. Paying rent to a landlord for a while longer is chips compared to the savings if you eventually borrow less by the tune of tens of thousands of dollars.

Yike!

Bought last year for 1.23 m, now asking 1.199..If I was a serious buyer I wouldn't want to offer anywhere near the asking price as starting point!

https://www.trademe.co.nz/a/property/residential/sale/auckland/auckland…

Bought in Nov 2023: 1,270,000

Listed for sale in March 2024: 1,199,000

With the photos, and short ownership period, this seems like a property trader trying to sell? If so, would be a loss due to renovation costs, holding costs and selling costs.

Did this property owner buy in Nov 2023 because they believed that house prices had bottomed and house price momentum was positive?

Here's another property being listed for sale within 3 months of their purchase date:

Nov 2023: sold by mortgagee sale

Feb 2024: listed for sale

July 2024: still unsold

A clifftop mansion snapped up for $9 million at a mortgagee sale last year mysteriously reappeared as a live listing three months later and is still on the market for sale after passing in at auction this week, OneRoof can reveal.

It was picked up in November by a vendor who did not wish to be named for just below CV after being listed as a mortgagee sale with Barfoot & Thompson agents Philip Davis and Rocky Liu.

In February, the property hit the market again, with the new listing on OneRoof with Bayleys agents Gary and Vicki Wallace declaring: “Vendor wants sold!”

https://www.oneroof.co.nz/news/mortgagee-mansion-snapped-up-for-9m-reli…

Showing my age here but I remember the share market crash in 1987 which led to lower house prices through to 1991 of more than 25% where we lived. It was worse in other places. And it wasn't much fun. We got out of it in 1995 by the skin of our teeth, but it was a long tunnel.

Agreed. The root causes of 87 were over valuation and excessive debt in shares and housing. Debt unsupported by income.

Sounds familiar.

"I remember the share market crash in 1987 which led to lower house prices through to 1991 of more than 25% where we lived. It was worse in other places."

Thank you for sharing your lived experience. Just out of interest, what suburbs are your referring to?

Reality for many places is that prices are stable and in fact are not dropping in NZ.

We are buying and selling currently in ChCh. and I can assure you that the market has not dropped in Chch, there are fewer cashed up buyers, than what there was a couple of years ago.

Auckland prices were always going to come back at some stage as they were grossly exaggerated for whst you actually got, so yes it is good for buyers in the long run.

Just as WGTN was grossly over priced compared with AKL, or indeed Turangi is compared with Taupo...

I don't mind CHCH as went to Uni there and have fond memories ... as any 21 year old would... very happy people!

earthquake damage and water pipes freezing in Chch are a bit of a bugger though.

Ok true. All HIGH PRICED - "property purchasing errors" can be solved, if you want 15 to 20 years.

Much longer than 20 years, if you see the huge Japanese 20 YEAR BEAR HOUSING MARKET.....

I understand that Auckland prices drove up prices in other centres as cashed up Aucklander's left and bought cheaper properties and set a new psychological baseline on what a reasonable prices to pay was. I would expect the reverse to happen as prices in Auckland fall.

It never went up. Big mistake in missing out on Auckland.

Bishop knows house prices are going to fall.

There is nothing the NACTF can do about it.

A smart politician would claim it is their policy ... So to be proved right.

(Simple ... when you know you're being conned. How many know it? Apparently ... Very few!)

100% the Landlords got played and conned by the NATs. Plain as day.

Bishop and the NATs are pinning their tail on the property crash and taking credit for it. Well played.

While its really the fundamental economic market forces causing this reset (valuations still way too high, as of July 2024) It's the market crashing the still massively overpriced NZ property market.

The Nats are just pushing it much faster, over the next ledge, downwards,

House prices went up more under Labour so if that was their goal by voting they voted for the wrong party. I keep trying to explain this to family who think that by voting National their market value would be improved. It is often not even that; there often is no direct relationship to who is in govt to house price shifts e.g. see 2011 major movements.

Townhouse/apartment is not a house, it's a box.

A 40% discount for a nice house, anyone interested?

https://www.realestate.co.nz/42601546/residential/sale/22-library-lane-…

Hahahahha

Its wonderful at a $290,000. price.

The transaction price history is interesting

1) March 2022: 730,000

2) March 2024: 705,000, -3.4%

3) July 2024: listed for sale at 459,000, -34.9%

So from peak to current asking price is -37.1% in just over 16 months.

Notice how the marketing by the real estate agent is trying to create fear of missing out to potential buyers to try and create urgency to transact.

"This is the perfect first home for someone with a limited budget who wants to get on the ladder before interest rates start to reduce and values start to rise again."

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.