More first home buyers are taking out higher risk, low deposit mortgages, although that doesn’t appear to be affecting the average price they are paying for a home of their own, or the average amount they are borrowing, which are both relatively flat.

The latest mortgage lending figures from the Reserve Bank show that total lending to first home buyers (FHBs) was flat over winter, with 2445 mortgages approved to FHBs in June, another 2201 in July and 2481 in August.

However FHBs taking out the higher risk, low equity mortgages (where they have less than a 20% deposit), has steadily increased for five consecutive months, rising from 27.4% of mortgages approved to FHBs in March to 32.4% in August, almost certainly as a result of the Reserve Bank easing lending restrictions on low equity lending by the banks (see the first graph below).

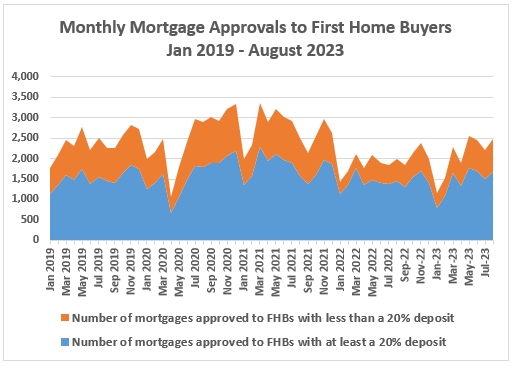

But so far, that does not appear to have pushed up the prices FHBs are paying for their homes and consequently, the average amounts they are borrowing.

In fact the reverse appears to be the case, with interest.co.nz estimating that the average price paid by first home buyers declined from $682,000 in June this year to $661,000 in August, which was its lowest point since February this year and still well below the peak of $718,000 in December 2021.

Similar trends are evident in the average estimated prices being paid by both low equity borrowers and those with a 20% deposit, and in the average amounts they are borrowing.

The second graph below shows the estimated average prices paid by first home buyers each month since January 2019, according to whether or not they had a minimum 20% deposit.

Just under three quarters of the low equity loans approved in August were to first home buyers.

What these latest figures suggest is that the recent loosening of LVR mortgage lending restrictions by the Reserve Bank has probably increased the number of homes being purchased by first home buyers, but does not appear to have increased the prices they are paying for them.

The comment stream on this article is now closed.

- You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

131 Comments

If they are buying at the peak of interest rates, then it should get better over time as their pay goes up and rates settle. Its better than buying when rates are low and prices are higher, they then feel it when rates rise.

And what about when rates are low and prices are lower? Since that’s very much on the cards.

It is not always about the price.

Prices typically go up as rates fall.

My mistake, you’re absolutely right. If I look back at major recessions against asset bubbles, of which there are many, I definitely do see asset prices shooting off as rates are slashed. Oh wait, no. No, that’s never happened. Name one time.

Generally the destruction happens after the first cut, so you’ll have time to react don’t stress.

What happened when rates were slashed after Covid? That’s right. But oh wait “ This time it’s different”

Listen carefully!! WEEE ARRRE INNN A BUUBBBBBLEE.

Bubbles burst. The burst is still to come.

Problem with the bubble now days is that it is a digital bubble so it is hard to pop.

Nah, one line of bugless code:

Bubble = Bubble * 0.5

Deoending on the language, you're missing a semicolon, and the interpreter could continue infinitely looking for the end.

Sigh. Yes, yes alright, a potential severity 1 bug OK I stand corrected. Ship it and maybe we'll be lucky in Prod. That is what we are doing with the Bubble.

I was (clumsily) attempting to extend your comment into a metaphor of a prolonged deflation, no harm no foul.

I'm also keenly aware I had a syntax error in my statement, no wonder it failed...

Fully agree.

Tradies, retailers, cafes etc are all struggling badly and will def start to lay off staff in bigger numbers soon... for retailers they will see rubbish xmas sales too which is most their annual revebue and profit.... We havent seen those key parts of the process yet. Families losing their main income already struggling with mortgages will be forced to sell with no buyers. We havent seen that yet which is the tipping point normally. Excess stock and low demand combined with high rates will quickly kills prices

This will lead to pressure on the govt to cut immigration to leave jobs for kiwis... and that will cut off the only life support for the house market.

I wouldnt be hanging out for a govt bail out no matter who gets in. The bubble looks pretty nasty from all directions.

The good news is that some businesses and professions will thrive as the market shifts... for some its a great opportunity.

People will always drink

House prices already rising according to Trade-Me property but you go ahead and keep yelling at clouds.

In Ireland they introduced DTIs. Spain were building 1 million homes per year when their market crashed. For a population of 47m that would be like NZ building 100k+ homes a year. In Japan they had a tapering (and now falling) population.

Denmark mortgage rates fell from 1.2% in 2016 to 0.56% in 2019. Their House Price Index rose 20% over that period.

https://www.statista.com/statistics/614979/mortgage-interest-rate-denma…

https://tradingeconomics.com/denmark/housing-index

Back with the Ireland obsession. Just dont forget the immigration and population gain factor in Auckland at least.

Ireland is a great case study. They implemented DTIs, turned out no one could afford to build or buy new houses.

And home values dropped 60% in ye olde IRE.

Yeah, because they had almost a total economic collapse.

Today, house prices in Ireland are now well above what they were when the bubble "popped". No houses to rent, few options for FHBs. This is because of the realities of trying to build in high wage economies, we only feel wealthy if we're buying goods made in Bangladesh by 3rd world child labour.

Ok so Ireland is what will happen here then.

IRE took 16 LOOOOONG years to reach the heights of 2007 again.

Ireland Residential Property Prices - August 2023 Data - 2005-2022 Historical (tradingeconomics.com)

So by 2037, NZ will surpass the 2021 average valuations. This is a long, long wait for the SpruikerClass!!!

I can see why the Spruikers are wanting a National Party led "momentary blip" to pass the bag and exit the land of the overleveraged. Quick.

Ok so Ireland is what will happen here then.

I don't think NZ is in the same state today as Ireland was in the mid 2000s for it to experience the same sort of economic demise. That said, the world is a fairly different place, so who knows.

I'm more pointing out how DTIs won't make property magically fall to the level the set DTI says people can afford.

It will have an impact. Spec crowd needing real vs.vapor equity to buy the next rental would need to adjust their models to actually declaring a profit and paying tax and saving the next deposit. At current expectation compared with rental income that's going to be circa 70-80% equity requirement.

Spec is usually referred to the actual construction of a rental house though (at least in building circles). Such construction will drop off with a DTI imposition, so you will have buyers fighting over whatever housing stock already exists.

So maybe a dip, with a big climb after a few years.

"IRE took 16 LOOOOONG years to reach the heights of 2007 again"

That assumes that the mortgaged owner could hold on until prices recovered. Many lost their jobs and were unable to continue meet their debt service payments and may have had to sell.

Unemployment rose from 100,000 to 350,000 at their peak.

Remember that Ireland's population is similar to that of NZ.

This example was written in May 2020 (before the peak of Nov 2021)

Let's take a look at the situation for an owner occupier buyer in Dublin in late Jan / early February 2007:

a) Property prices in Dublin have been rising from 1900 to 2007 - that's 107 years of historical data of house prices rising. Based on that, the owner occupier believes that property prices will continue to rise, or not fall by much

b) They read that property market commentators are saying that there is a housing shortage in Dublin and read the following article in the local newspaper on 25 Jan 2007 - https://www.irishtimes.com/news/dublin-housing-shortage-to-continue-1.8…

c) They proceed with a house purchase in 2007 using high amounts of leverage.

Details of purchase:

i) Property price: 162,000

ii) Mortgage @ 80% LVR - 129,600

iii) Equity value saved and used to buy the house - 32,400

Value at 2020 (13 years of ownership)

i) Property price: 137,000 (fall of 15.4% from purchase price - AFTER 13 YEARS of ownership)

ii) Mortgage @ 80% LVR - 129,600 (assumed to be interest only for illustration purposes)

iii) Equity value - 7,400 (77% decline from original equity to buy the house)

House price data - https://tradingeconomics.com/ireland/housing-index

That 7,400 in equity may be used to either:

1) upsize (into a bigger house by younger owners for children), or

2) downsize (into smaller house for retirees)

(Remember that there still payment of sales commissions which would reduce the 7,400 equity value even more - say 3% on 137,000 sale price or approximately 4,100 in sales costs which would result in net equity of 3,300). Haven't even included interest costs in any of the above calculations.

Now how is that 3,300 going to be sufficient for a 20% deposit for a new house (either for the upgrader, or downsizer)? That 3,300 is now only 2.4% of the median house price of 137,000 in 2020.

The owner occupier's financial security had experienced a real set back. These people will have less to retire on. All because of that one decision to purchase a property in 2007.

Now that scenario assumes that the owner occupier was able to hold on. What happened if they were unable to continue debt service payments (such as lost their job, experienced lower weekly wages, etc) and were forced to realise those losses?

This is the potential situation that owner-occupier buyers today are facing. I don't believe that hard working owner-occupiers buyers who have taken years to save their deposit to buy a house should be potential collateral damage as a result of a large presence of speculators in houses. Owner occupier buyers should be fully informed of potential property price risks and make fully informed decisions, rather than accept blindly the highly promoted viewpoints of those with huge vested financial interests.

Yep, do the Math. As an aside math is honest has no vested interest unlike some other things.

Maths is amoral so honesty isn't really a question there.

Humans on the other hand, are much more complex.

The expectation that the roof over your head is an appreciating asset is a massive issue. We need to get back to reality. It's a roof over your head. I like the way families live in South Pacific islands. Once you start burying your forebears on the land its kind of a hard sell.

The expectation that the roof over your head is an appreciating asset is a massive issue.

Greed is a part of human nature. Here are some other objects of speculation throughout history:

1) beanie babies

2) tulips

3) commodities

4) stamps

5) toilet paper, face masks, hand sanitiser - during COVID

6) art

7) rare books

8) rare wines

9) athletic footwear, sports memorabilia

10) entertainment memorabilia

11) rare cars

12) non fungible tokens

13) jewellery

It's the kids I feel for. Bangladeshi child labour unemployment rates are hovering at a tad over 95% already, a serious global downturn could put them all out of work.

Maybe slow down and read my comment, you'll probably find it aligns with your view. I was highlighting the reasons why their property markets didn't take off post bubble burst and low interest rates. Denmark dropped their mortgage rates from 1.2% to 0.56%, and prices rose 20% in 3 years.

If NZ introduced DTIs, or were building 100k homes per year, or had a population decline, then Malamah would probably be correct. But their comment ignores our dynamics.

Just dont forget the immigration and population gain factor in Auckland at least.

You're either more honest or more intelligent than any of our current politicians. I agree demand is relevant for housing affordability.

Yep, housings way cheaper places people don't want to live, or if everyone there is broke.

"Just dont forget the immigration and population gain factor in Auckland at least."

In order to persuade people to buy so that they can earn their commission, the property promoters cite population growth causes house prices to rise. This is the commonly held conventional belief and certainly seems logical. Here are some data points for people to think about:

1) Japan

a) Population - a RISE of 3.6%

1991: 124 mn

2009: 128.5 mn

b) House price index - a FALL of 46.5% (over 18 years)

1991: 182.7885

2009: 97.708

https://fred.stlouisfed.org/series/QJPN628BIS

2) United States

a) Population - a RISE of 5.2%

2006: 298.4 mn

2012: 313.9 mn

b) House price index - a FALL of 27.3% (over 6 years)

2006: 184.6

2012: 133.997

https://fred.stlouisfed.org/series/CSUSHPINSA

3) Ireland

a) Population - a RISE of 5.1%

2007: 4.399 mn

2013: 4.624 mn

b) House price index - a FALL of 54.5% (over 6 years)

2007: 153.973

2013: 70.09

The context of all your examples coincides with wider economic calamity though. You'd have to be silly to think an influencing factor like population increase somehow makes asset prices invulnerable from any other eventuality.

If the economy really does hit the skids as many are saying, then quite rightly asset prices will fall, even if more people move to NZ.

" You'd have to be silly to think an influencing factor like population increase somehow makes asset prices invulnerable from any other eventuality."

Many people believe that population increases result in a continued upward movement in price, or at least that house prices don't fall by much. Property promoters are continuing this narrative to persuade people to buy today - saw one repeat this argument just the other day with inward migration.

Here is a list of reasons that were given as to why house prices in New Zealand won't fall by much or would continue rising. This list was highlighted before Nov 2021 against a backdrop of continued rising house prices in NZ. (It might be seen in a different light given the house price changes since Nov 2021)

These are some reasons given in the mainstream media, property market commentators, property market promoters, bank lending promoters masking as bank economists, real estate agents, property market mentors & other sources as to why property prices in Auckland will not fall by much and that there is a low probability that property prices will fall dramatically:

-

during the GFC, house prices in Auckland fell only 7-10%

-

over the past 50 years, house prices in Auckland have averaged 7.2% per annum (or commonly referred to as house prices doubling every 10 years). This trend can be expected to continue into the future - https://youtu.be/Agp9xFWoBX4?t=172

-

there is a shortage of underlying housing in Auckland, so property prices won't fall by much - https://www.interest.co.nz/property/97513/auckland-councils-chief-econom...

-

there is a growing population which means that there will be more demand for houses - https://www.stuff.co.nz/business/106883553/house-prices-have-fallen-but-...

-

we have inward immigration which means more demand for houses

-

Auckland is an attractive city with an attractive lifestyle - that makes it desirable and attracts foreigners to move to Auckland and hence raise the demand for houses

-

Low interest rates were also forcing retirees and those nearing retirement to look for investments that would produce income, such as rental property. "Plans of the baby boomers to retire and live off a conservative yet well-yielding portfolio have evaporated with low interest rates," he said. "[They] are seeking assets and buying investment properties. They are also seeking assets they can hold and live off of for three decades in retirement rather than just 15 years given advances in health and medicines." - https://www.stuff.co.nz/business/84322204/all-predictions-of-an-auckland...

-

we mustn't forget either the vested interests in ongoing stability. No government, central bank or trading bank with mortgage exposure wants materially lower house prices. Nor does an incumbent Beehive want falling house prices going into an election campaign https://www.stuff.co.nz/business/110499233/think-house-prices-are-going-...

-

the economy is doing well, with low unemployment - https://www.stuff.co.nz/business/110499233/think-house-prices-are-going-...

-

there has been insufficient construction of new builds to meet the housing shortage - https://www.stuff.co.nz/business/106883553/house-prices-have-fallen-but-...

-

there are high construction costs to building a house. House prices cannot fall below their construction cost. - https://www.stuff.co.nz/business/106883553/house-prices-have-fallen-but-...

-

people don't sell their houses at a loss - https://www.stuff.co.nz/business/106883553/house-prices-have-fallen-but-...

-

continued inflation means that house prices will continue to rise in the future

-

The fact is, debt levels have barely changed from the beginning to the end of those 10 years, compared to GDP levels, compared to household assets, compared to household disposable incomes. And much more importantly, debt servicing is very much easier now, an item that is almost universally overlooked. We are not pushing out to unsustainable levels now, and even if they creep up a little, we are far from that point. https://www.interest.co.nz/opinion/95894/if-you-think-new-zealands-house...

-

in aggregate household debt servicing is low in New Zealand - currently at just under 8% of disposable income of households - https://www.rbnz.govt.nz/.../key.../key-graph-household-debt

-

property market participants & commentators who have been correct in their predictions about recent property price trends have more credibility and hence their predictions of upward prices are believed by a wider audience (such as Ashley Church, Tony Alexander, Ron Hoy Fong, Matthew Gilligan, etc). - https://www.stuff.co.nz/business/84322204/all-predictions-of-an-auckland...

-

previous warnings about a house price crash have been wrong - property prices have continued rising upward significantly since these warnings were given, so there is little reason to believe these warnings.(such as Bernard Hickey) - https://www.stuff.co.nz/business/84322204/all-predictions-of-an-auckland...

-

its unlikely Auckland prices collapse. I think the main two reasons though are:a) Affordability has been this bad, and worse, in the past and it only resulted in about a 10% drop. b) The number of homes built over the last decade has been too low and will take some time to recover - https://www.interest.co.nz/property/100670/housing-market-continues-hibe...

-

real estate is a hedge against inflation so I don't see house prices in Auckland falling much further.

[https://www.propertytalk.com/forum/forum/property-investment-forums/new…]

" You'd have to be silly to think an influencing factor like population increase somehow makes asset prices invulnerable from any other eventuality."

Here is what Tony Alexander was saying in Dec 2021, when house prices were at their peak.

19 reasons why there’s no crash

5. 165,000 migrants

https://ndhadeliver.natlib.govt.nz/delivery/DeliveryManagerServlet?dps_…

Note that this article has been removed from his own web site and can no longer be found there.

Much of this reasoning is sound, all things being equal.

What no one is really capable of, is predicting the future in its entirety. It does seem like we are heading for some larger negative economic times, which will over-ride your list of attributing factors to house prices.

But if everyone acted as if the sky was going to fall tomorrow, no one would bother doing much of anything. Plant a garden, get married, get a job, etc.

What's the saying, "feel the fear, and do it anyway"?

"Much of this reasoning is sound"

Much of this reasoning SEEMS sound to many people. These were the common conventional beliefs / assumptions as to why house prices couldn't fall by much. These were the beliefs that led to a fear of missing out by buyers. These were the beliefs that led to many house buyers believing that a highly leveraged investment in houses was as safe as houses. These were the beliefs that led to the elevated house price levels and elevated house price risks in NZ.

Then house prices fell significantly from their 2021 peak - or as ANZ recently described it - "the house price bubble of 2021".

all things being equal

This part you left off is critical. Obviously multiple factors have the potential to impact house prices. Population growth will drive up prices all else being equal (i.e. same number of houses available, same interest rates, same credit polices from banks etc). A massive move in any of these will shift the market even if other factors are moving in the opposite direction.

So, it is possible to find an unexpected correlation between two specific variables for a period of time (population and house prices for example) because one or more of the other variables had a larger impact i.e., not all things were equal.

Yes I hear you, each of these has its own set of unique causes, but a similar theme. Bubble, followed by a failing economy, and monetary stimulus to soften the blow.

I do think there’s a chance property could go up significantly, however likely followed by a secondary pullback. The boat is going to rock a fair few times if that happens.

My pick is really an L shape. I don’t think we’ll see those 2-3% market rates again for a while. But ultimately the covid stimulus hit at the top of a boom, the downturn which slowly showed in 2019 was erased by a secondary peak. Now we have much tighter regulation going forward, overpriced assets everywhere and upside on rate margins. The game has changed slightly. It would take a lot to hit 2021 highs in the next few years, not impossible but not likely imo.

This is what these people fail to understand, if rates start getting slashed in this climate, it’s because something has gone seriously wrong.

They better hope rates stay higher for longer and achieve the mythical “soft landing”

But no.

rATe CuT dUriNg buBBLe, meAn aSSetS gO MooOoON!

Exactly. A severe economic shock would be required to justify cutting the OCR aggressively down to below 2% again. And that shock would create severe headwinds for housing which would counter the stimulatory effect of rate cuts. I guess the govt could pull out another massive stimulus package as per covid.

Far more likely is we have significant economic weakness over the next two years, with low growth or mildly negative growth, and the OCR gradually comes down to circa 2.5-3% in about two years time.

Just to clear that up - I don’t think anyone sensible is expecting rates to be slashed. Atleast not me. It’ll be more of a “settling” but not down to 2-3%

Absolutely correct. Happened in both Ireland and the USA. The Fed first cut rates in September 2007, then the real collapse happened afterwards.

Prices down 10k per month July and august the downward trend is picking up pace,FHB should just wait as it is quite obvious the news recently saying house prices were climbing again is complete nonsense, with rates staying higher for longer and inflation well above target levels house price will continue to fall for next 18 months and could be far longer if recession hits larger economies.

Very pessimistic if you think prices will fall for another year and half. Maybe the next 3-4 months but we have definitely flatlined and rates aren’t expected to go up much. I think whoever bought in 2023 and early 2024 will likely look back around 2030 and realise that they bought in the dip.

Hasn't HPI been showing prices nudging back up across most of NZ for 3 months...

Exactly, not sure what this fella is on about, anything to put the gloom on.

You know it's bad when DTRH isn't advertising bullish house price discounts.

FHB house price 21k in two months I would say that’s a big drop for FHB. Let’s face facts NIfty 1 you haven’t got much correct for last 2 years, the house price’s have fallen 20% in real terms add inflation it would be around 33% all this time you have been saying price’s will start climbing again with rates staying at this level or higher and inflation well above target levels and NZD tumbling, even if you had a lobotomy you should still be able to figure out house price’s are going down for some time. Maybe you and pant1er could see a financial advisor together could be big help.

I forgot nifty1 and paint1er Take the pieman with you he really needs a few sessions with the financial advisor.

DTRH, I’ve invested well and would modestly class myself as reasonably successful. The amount of nonsense from you on the other hand is plain stupidity, I question your “advice” and credibility and the audacity to tell others to see a financial advisor. What a clown.

I think his rationale is if you don't agree with his many, many claims of X percentage falls, you can only be an over leveraged investor living precariously close to the edge.

So pretty much every seminar believer in the last ten years then...?

Iceman Your comment I cut down some trees and made a extra million gives us all a clue about you,most of your posts are huge nonsense you haven’t got much correct and with financial predictions for last 2 years your record is sad as house prices were crashing you would say buy now. You should be ashamed as If anyone taking your advice would have paid hundreds of thousands to much and would now be in negative equity if anyone is a clown it’s you bo bo stick to make balloon animals.

Haha what the heck are they you on about mate? My theme was that this is an overdue correction after the covid gains. You may have got people mixed up but don’t put words into my mouth. Perhaps early onset of dementia for you mate, get help. I more so think you are a sour muppet with a hint of tall poppy, as your last comment speaks for itself .

Iceman,you a Yvil are very similar almost like the same person if not it doesn’t change anything around the nonsense you comment daily. The fact is you always encourage people to buy property in falling market which could cost people hundreds of thousands if anyone took your advice negative equity is the place they would be, you seem a bit triggered by my comments.just facts everyone can see the truth, whenever any one pulls you up on the nonsense you spew or disagree with you, the insults start all a sign of insecurity bet you drive a large car 🚗

DTRH - you are similar to the DGMs who constantly maintain that "now" is never the right time to buy and that a 50% crash is incoming. And this is exactly the type of misinformation which mean that many hold off from buying thinking there is a "better time" and never get on the property ladder. I suspect that you are one of these renters waiting for the "right time". Never triggered mate, I'm comfortable in my position and share my beliefs based on facts (last 3 months HPI increase, rates flatlining, inflation at 6% - downward trajectory. It's a waste of time talking to idiots though.

The last 18 months would have been a terrible time to buy losing around 20% in real terms and 33% with inflation things will get back to a balance some time but not for a while as this article said FHB price’s have dropped 21k in two month this is increasing the pace of price drops.

No shit. Hindsight is amazing isn’t it? Or those people could have waited a few more years and bought for higher when rates are lower.

Iceman do you really think rates will be coming down again, if rates ever come down it would be because of a major problem and house prices would be the last of your concerns.

I said that rates will settle, not go back down to 2-3%. Perhaps you need glasses.

You could say the same thing about your oft repeated claim that the prices of things are dictated by average incomes. You know, instead of what they cost to produce.

Of course house prices are dictated by income’s look at history house price’s normally go up with inflation and average incomes only for the last 14 years with low or emergency rates has this got out of balance, that why the crash has happened and will continue as rates climb to normal levels. Hope this helps you Pa1nter.

The cost to build a house is high, for "reasons". If you cant afford the new house, those "reasons" don't all go away.

In lieu of a new house, you have to try to compete for existing houses. With the people still living in them.

It's not Swahili

If I am correct and rates stay around this level house prices will continue downward trend and many new build will be taking huge haircuts, maybe the government will buy them at cost from distressed investors and builders and rent out to homeless and overcrowded population and also put small selling fee of 1% on all house purchases this will help fund process.

If rates don’t go down - building activity is slowing and immigration is increasing rapidly which leads to demand. So should actually see small increases especially if interest deductibility is reintroduced.

Wasn't it Yvil that cut down some trees and made $1m in capital gains?

NZ Mortgage rates are about to spike much higher from here, then again higher and HOOOOLLD.

Those (average household incomes) - with mortgages higher than 450K will be lambs to the slaughter. Very Sad what the nefarious Spruikers have done.

FHBs - don't take the Spriukers bait, WAIT! Pay much less in 2024 to 2026! Wait!

The prophet was right and 10% is Guaranteed!

Alas! We have a prophet here who can time the market! 🤡

Its simple maths! Don't pay more than a DTI of 4-6x.

The Greedy spruikers would love to offload their ratboxes to new bagholders, for more than 6x DTI

Buyers be warned!!! The RBNZ will make lower DTIs regulation.

Don't pay today's prices - they are in a reset downwards, that has just begun.

You should walk into your local housebuilders office and demand a place on this pricing rationale.

"...would love to offload... for more than 6x DTI"

This comment doesn't even make sense and shows a real lack of understanding.

That could literally be ANY price, as dependant on the buyers income x 6 to get the figure.

The last, average household income was assessed at: 117K. Do the math's at 4-6DTi! Do you understand this ???

This is where the market is going, in a higher and holding interest rate world?

I may earn 200K so at 6 x DTI I could borrow $1.2m, whereas your average household can only pay maximum (using your figure of 117K) of 702K at 6 x DTI. Do you understand this?

Your comments make no sense. And the RBNZ has never indicated a DTI of 4-6. Even in their discussion paper they used an indicative example of a DTI greater than 6.

Excellent. We finally agree:

- So 468K to 702K is a good average range, to buy NZ property at.

Its resetting towards that now. It will accelerate at a much fast rate of knots, as mortgage rates reset past 8%

Yes I can earn 1M so can pay 6Million. How great is that! hahaha.

Average household income is irrelevant. It's the income of house buyers that matters, but we don't have stats on that.

DTI of 6 sounds ridiculous it should be 3 to 4. UK for us it was 3, in the past it was 3 for NZ. Six or more is nuts. Once interest rates changed even on a DTI of 3 the impact on our spending was huge. NZ has had higher then 3% increase on DTI than 7 not sure how people are handling this.

Again triggered iceman mr angry needs to calm down its not nice to call people clowns if they have a different opinion to you maybe making the balloon animals will have a calming influence.

They'll do fine as long as they are able to service the mortgage and ride it out. But will they? If they were close to their limit at 3-4%, and with other cost of living rises, and a flat-lining economy? Not so sure.

Price might not be going up in a meaningful way in the next couple of years but rent will.

$400 per room p/w Wi-Fi not included.

No they wont. As supply increases form distressed sales, the new landlord's will buy in at prices that work without rent rises. Can't get blood out of a stone.

The issue is - the DGMs are still holding out for these distressed sales and we’re factually past the bottom.

But How do you know we are ‘factually past the bottom’? We are for now, sure, and that’s factual, but it’s possible there will be another leg down, below the current bottom.

Look at the HPI for the past 3 months, it’s actually increased.

Are you familiar with the concept of 'local minima'? Downturns are not always a simple leg down followed by a leg up.

You may be right that a bottom has been reached, but you certainly can't say we're factually past the bottom.

I would say the effects of interest rate tightening haven't even been felt yet, here and internationally.

I would say they have been partly felt. But not felt enough to create too much damage. Yet. Give it 6 more months.

lol if you look before past 3 months, it's actually dropped. Just look at three months data is not how you determine "it's passed bottom"...

We will also see far less immigration as the economy and employment weakens, and potentially more young people moving back to mum and dad’s house, or moving in to mate’s houses for a mutual ‘win win’ ( support mate’s soaring mortgage payments, and maybe get a sharp deal on the rent for the room)

You speak as if landlords are still going to hold enduring power over renters.

The irony of renters bailing out their landlords via mortgagee / distressed sales may be a reality for many in the coming 12-24months.

Lol.

Why do you perceive it as “power”? Is it insecurity? Relax - I feel like the supermarkets rip me off, but I don’t see that as power over me.

Can the supermarkets kick you out of your house? Do you spend most of your pay at the supermarket? Does the supermarket manager come walking through your house and check you have been cleaning under the oven?

The supermarkets have little power over you. Landlords have a lot.

A better example is if I was renting a car and didn't own it - sure, I need to keep it tidy etc. It's not a power trip by the rental car company. Also with all the Pro tenant laws - you can't actually kick someone out in most cases anymore.

If someone was taking most of my pay for their retirement fund (and could ask me for more), could inspect my home, could decide to sell my home forcing me to find another place to live, I would feel like they had quite a reasonable amount of power over me. I would be nice to them, and try not to upset them due to the power imbalance. Whether I liked them or not.

To compare it to hiring a car, or buying a lettuce is laughable. Your kids don't need to change what school they attend when you change who you hire cars from.

I was trying to give you an anology as you sounded like you were taking it personally, but I understand the plight. You have to remember thought that most landlords want good tenants, and it's not that hard being good tenants - so generally there are no issues until they need to sell. Prior to the tenancy law changes, landlords didn't kick out good tenants for no reason. Issues only arise when tenants turn out to be a**holes.

I dunno, I've met some arsehole landlords in my illustrious renting career.

The landlord needs to give you notice of a minimum 48hrs prior to inspection. These inspections can’t be any more frequent than monthly.

Landlords want to retain good tenants. They make being a landlord a lot easier.

Finally, the tenancy.govt.nz site describes houses as ‘yours’ when referring to landlords houses. The tenant is simply the tenant.

Disclaimer: previously owned rentals which were regretfully sold. Hindsight.

Its the landlords house, but the tenants home.

The discussion was whether a landlord has 'power' over their tenants.

How often can the tenant inspect their landlords house?

A mans home is his castle, unless he rents.

The inspections are required by the insurance company or else the landlords policy becomes null and void.

Perhaps if the tenant was paying the insurance policy they would have reason to inspect the landlords house.

Inspections are in no way a power play by landlords.

I never said inspections were a 'power play'. I said landlords have the power in the tenant/landlord relationship. The landlord gets the rent and capital gains of the property and ultimately decides who can live in the house. The tenant pays the rent and hopes the landlord doesn't increase the rent or ask them to leave as moving is expensive and disruptive. Most people renting, especially families, would rather be living in their own house. Increasing property values and residential property investors limit the opportunity for that to happen. I get the feeling the 'power' word is triggering and we are talking cross purposes, so lets just leave it there.

Part of the reason why people choose to buy than rent.

“power over renters”?

Trust me, it’s a different story when you constantly having to turn down angry perspective tenants trying to offer you higher rent to secure the property.

Stressful not powerful.

So many people saying 'take my money', oh what a terrible burden.

“Trust me bro”

Yeah, no thanks.

You might be inundated now, I say enjoy while it lasts.

It is very risky right now to assume that rates will stay roughly where they are or go up only slightly. A spike to 10% or higher is a real possibility, depending on several global factors that are highly unpredictable at the moment and over which NZ has no control.

If that were to happen, a significant fall (another 25% or more) in our still massively overpriced housing market cannot be ruled out. This is not the time to be taking on a lot of debt/risk, in my opinion.

A spike to 10% or higher is a real possibility

It's possible, but not very probable.

10% Mortgages VERY LIKELY.

The prophet Guaranteed it.

We were wrong to cast out the Prophet. He saw the future with clarity and only spoke the truth.

Well, seeing as you wrote it in capitals

It's still not overly probable.

Floating rates going to 10% or close to it is plausible. Fixed rates going to 10% is extremely unlikely

Agree Floating will be the first to get written above 10%......

Talk in the US is now, what a 7% UST rate will mean for everyone.

It will mean that all the worlds Debts (ours much more so) get drastically more expensive. Those that get forced resets (1 to 5 year) will be BBQed.

The risk is always there. Those that choose to take on the risk - in the past, now, or in the future, will reap the rewards or the losses. That is the nature of the market.

What could possibly go wrong?

This scenario reminds me of that XXXX Beer advertisement in Australia, where they loaded up the ute full of beers and then one more Sherry bottle (for the shilas) and the ute collapsed!

Still here on Facebook! https://www.facebook.com/watch/?v=3423199264421915

Low equity less than 20% deposit...How much less equity ? 32.4% of new mortgages and rising .... Are we near sub-prime yet?.... I guess even with the higher LEM rates folk are still keen on having a nibble ... Many will be counting on valuation rises to counter the penalty rate... I hope everybody knows what they are doing....lol

Wow ! more than 30% are low equity mortgages?......that is a lot.

Reminds me of money pushers leading upto the GFC......the RE Agents and Mortgages brokers, loading up the unwary home buyers with massive debt burdens and laughing about it, all the way to cash in their commissions. Those Money Pushers made good money doing that, great job to have when you are without a conscience.

What could possibly go wrong in 2023/24/25 ?? ...... Yes all NZ is made up of the risky USA style Adjustable Rate Mortgages (small US mortgage portion are ARMs) that partly fed into the GFC meltdown.

(104) The buble in Florida and the mortgage brokers - The Big Short - YouTube

They are buying with a 5% deposit and the Govt guaranteeing their mortgages under the First Home Loan Scheme. Not a lot of credit checking going on either, as most of them are "new residents"

https://www.oneroof.co.nz/news/first-home-loan-scheme-is-open-to-abuse-…

Absolutely unbelievable.

What could possibly go wrong.

One interesting issue is that Kainga Ora is receiving a 0.5% fee to insure the high LVR mortgage.

"Each participating lender will have their own interest rates and fees. One of those fees is to reimburse the lender for the Lenders Mortgage Insurance premium Kāinga Ora charges to insure each First Home Loan. The amount of this fee is 0.5% of the loan amount."

https://kaingaora.govt.nz/home-ownership/first-home-loan/

This raises several questions:

1) Is this insurance premium adequately priced to cover the exposure that they're taking on? I have no idea on pricing.

2) what is the maximum size of their exposures that they're taking on relative to their net worth / equity capital? and if the losses get too large relative to capital whether there is any potential backstop / capital funding by the government.

Remember the credit insurers in the US in the GFC when the credit default risk was subsequently found to be inadequately priced and led to solvency issues? Remember AIG with the sub prime credit default swaps?

This is effectively NZ taxpayers insuring the housing speculation of largely new foreign arrivals, who just recently got a ticket to live in NZ.

Bloody hell! WE are on the hook for this risk for tiny premiums!!

So they can own potentially own multiple properties in the listed high volume application countries of the Philippines or India and get the First home Loan Govt Guarantee. This stinks. Smells like a wrought!

I know many great people from these countries, yet one of the reasons they left was because the lack of trust in the countries systems and rampant corruption.

Where is the investigative journalism on this potential major scam? INTEREST TEAM - PLEASE STEP UP. This is one reason why I pay the fee here!

When the property market tanks the next 15 to 30%, as interest rates get into further eyewatering territory......WE the NZ people will be left covering these potentially massive losses. The premiums for this risk must be much, much higher!! Not the back of the envelope BS calculation by some KO weasel.

But wait, there's more! Kainga Ora are also busy buying houses for First Home Buyers, through the First Home Partner Scheme (where they dont just guarantee the mortgage, they actually buy 25% of the house). "Changes were made in July to make it easier for buyers" so no surprise that there has been a flood of FHB. No mention of how many hundreds of millions of dollars are being spent on this scheme. It was so popular that its now oversubscribed and even KO has run out of money.

https://www.oneroof.co.nz/news/first-home-partner-help-for-first-time-b…

FYI, a property investor with 100 investment properties commented on potential impact of election result on house prices:

1) if incumbent government remain, he would expect a 10-15% fall in house prices

2) if there is a change in government, he would expect a 5-8% increase in house prices

Also said that if incumbent government remain, he would leave New Zealand, and sell his property portfolio

I wonder what kind of magic wand he thinks the Gnats have. Improving milk powder prices and stimulating tourism? Surely anything else is just fiddling about given our current account deficits.

If the economy goes into recession, the next government will very likely need to respond and provide stimulus. The size of the stimulus is contingent upon the magnitude of the recession. That will be regardless of whether the incumbents remain or there is a change in government.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.