The home ownership dream is likely well out of reach for typical first home buyers on average pay in most regions of the country, despite significant house price falls over the last 15 months.

The Real Estate Institute of New Zealand's national lower quartile selling price peaked at $670,000 in November 2021 and has since fallen back to $565,000 in February this year. That's a decline of $105,000 (-15.7%).

In Auckland, the country's largest housing market by far, the REINZ's lower quartile price has dropped back from $966,000 to $779,000 over the same period, a decline of $187,000 (-19.4%).

The lower quartile price is the price point at which 25% of sales are below each month and 75% are above, representing the lower end of the market which is of most interest to typical first home buyers.

Although the recent price falls at the lower end of the market have been substantial, they have only retreated back to where they were at the beginning of 2021. And first home buyers are likely to be significantly worse off now then they were then because mortgage interest rates are much higher.

In February 2021 the REINZ's national lower quartile selling price was $565,000, exactly the same as it was in February 2023. But the average of the two year fixed mortgage rates offered by the major banks back in February 2021 was 2.53%. By February 2023 that had risen to 6.45%.

That means a 20% deposit on a home purchased at February 2023's national lower quartile price would have been $113,000, unchanged from February 2021. And the amount that would need to be borrowed for an 80% mortgage would also be unchanged at $452,000. But the amount of money that would need to be set aside for the mortgage payments would have increased from $413 a week to $656 a week. That's up by $243 a week (+59%), leaving first home buyers significantly worse off than they were two years ago.

Interest.co.nz estimates that the combined, median after-tax pay for couples aged 25-29 who are both working full time was $1739 a week in February 2021. That means the payments to service an 80% mortgage would have eaten up just under a quarter (24%) of their take home pay.

Two years later in February 2023 and interest.co.nz estimates the median after-tax pay for typical first home buyers would have increased to $1871 a week. That's up by $132 a week (+7.6%), which means mortgage payments would now be chewing up 35% of typical first home buyers' take home pay.

Their situation would be even worse if they were unable to scrape together the $113,000 needed for a 20% deposit.

If they had $56,500 for a 10% deposit, they would need to borrow $508,500 for a 90% mortgage, which means the borrowers would almost certainly be paying a significantly higher interest rate for a low equity loan.

That would have pushed the mortgage payments on a lower quartile-priced home up from $542 a week in February 2021 to $832 a week in February 2023, up by $290 a week (+54%).

Which means the amount of their take home pay typical first home buyers would need to set aside to service a 90% mortgage would have increased from 31% in February 2021 to 45% in February 2023.

Those figures are bad enough, but they are based on buying a home at the national lower quartile price.

The situation is considerably worse for typical first home buyers in centres such as Auckland, Waikato, Bay of Plenty, Hawke's Bay, Wellington and Nelson/Marlborough, where house prices are significantly higher.

In Auckland, the amount of money that would need to be set aside to service an 80% mortgage on a lower quartile-priced home has increased to $904 a week in February 2023 from $604 a week in February 2021.

That has increased the amount of take home home pay that would be gobbled up mortgage payments for typical first home buyers in Auckland from 32% to 47% over the last two years, assuming they had a 20% deposit.

If they only had a 10% deposit and needed to borrow 90% of the lower quartile price in Auckland, the mortgage payments would have increased from $791 to $1148 a week over the same period, taking up 60% of their take home pay in February 2023, up from 45% in February 2021.

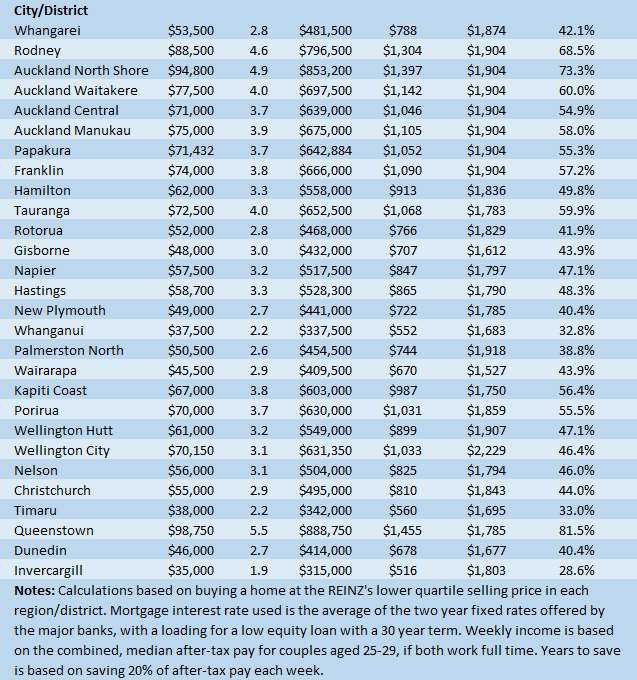

The tables below show the main affordability measures with both a 10% and 20% deposit for all of the main urban districts throughout NZ.

These show that in spite of recent price falls, the amount required for a 20% deposit on a lower quartile-priced home in February 2023 was more than $100,000 in all regions of the country except Manawatu/Whanganui, Taranaki and Southland while Otago was exactly $100,000.

This leaves typical first home buyers on average wages between a rock and hard place, because if they opt for a low equity loan with a 10% deposit they will be unlikely to afford the resulting mortgage payments.

So they are caught between trying to save enough for a deposit which is out of reach, or take on a mortgage which is beyond their means, something the banks are unlikely to agree to.

Unfortunately, that means home ownership in much of the country but in the upper North Island and Wellington in particular, is largely the preserve those with access to a decent amount of cash, perhaps with the help of mum and dad, or the highly paid.

Those on average wages who don't have a helping hand to stump up a 20% deposit are likely to be left out in the cold.

The comment stream on this article is now closed.

- You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

159 Comments

The ancient Greek mythology tale of Tantalus is an apt depiction of where NZ first home buyer hopefuls are at, and have been too, for quite a while

I read this as good news - as prices will continue to fall then until they are within reach.

Stay firm fhb's ...the squeeze is on.

Particularly with investors on the sidelines. Falling prices means investors have less equity (especially with reinstated LVR). Rising interest rates, and changes to interest deductibility, lowers what they can afford to pay.

So at this point prices need to adjust to what FHB can afford to pay.

Credit where due. The Govt interest deductibility rule changes leveling the playing field between home owners and landlords is playing it's part.

More tax flowing in form the landholding class as we speak - after decades of interest free gains.

National take note - we want this.

Agreed. This is the reason I wont vote for them. Have message my last couple of Nat MPs over this and you guessed it....no response.

Yes it is a major obstacle for me as well. Thinking of the young people, not myself,

I'm sure the mathemawizards are trying their very best to balance policies of tax cuts with fixing any real problems. Rewriting the curriculum is their next big thing, will be a very expensive term for any government imo. So we should expect big tax hauls.

Another mathematical truth is that even if Nats reintroduce interest deductibility later this year, you may still remain underwater due to new LVR rules.

Let's say you bought a $500k property during a time with no LVR restrictions with a 10% deposit and borrowed $450k. If the property's value fell by say 20%, you would now be underwater to the tune of $50k. With your equity already vapourised and further losses looming, you would have two options: sell the property at a loss and move on or foolishly stay put. If you stay put and at some stage, choose to refinance or banks get nervous, they could (possibly would) ask you to fork out an additional $120-$150k in equity. That puts you in a difficult position where it may seem impossible to recover from your paper or real losses in the foreseeable future. This cohort was labelled geniuses in 2020!

Just as some brain candy on this:

- I believe 46% of rentals have a social housing element involved (I.e. either supplemented or totally paid for by the state). So around half of rentals are still interest deductible.

- Unemployment should rise significantly over the coming 12-24 months.

So the number of non-viable private rentals due to the removal of interest deductibility is already low, and will likely decrease over the coming years.

Basically unless housing supply gets a significant level of intervention, little will change.

Pa1nter - there is no interest deductibility where the renters receive the accommodation supplement. It only applies if the rental property is leased to a govt agency or a community housing provider specifically for social housing. Interest deductibility still applies to new builds. So relatively few rentals will be elegible.

See: https://www.ird.govt.nz/property/renting-out-residential-property/resid…

Banks cannot insist on an equity top up if you keep the payments up, its not in the contract. You do raise an important issue however which Banks will factor in to future borrowing.

They can, including calling the mortgage altogether. Something that hasn't occurred doesn't mean they can't do it directly or cause it indirectly.

This was my concern, now alleviated, had the US banking failures jumped the ditch to us, and our banks started calling in their chits to build up cash, once all the deposit accounts had been drained of course.

Fortunately it didn't happen, but as you say, doesn't mean it won't.

Rumpole- unfortunately they can and do. This happened to a friend of mine during the GFC, who had several properties, and had borrowed against them to fund a business, which was not doing that well. The bank just rang her and told her she needed to put more equity in to her mortgages with them. I had no idea that could happen. Banks can also just take funds you get from a house sale and apply them to reduce your mortgage/s on other properties.

Many private landlords will be using their personal homes as equity so they should meet the LVR requirements. Furthermore, the LVR restrictions only apply to new lending (see https://www.rbnz.govt.nz/regulation-and-supervision/oversight-of-banks/…).

Accordingly, many landlords will try and ride out the high interest rates and push for a National/Act government to get some interest deductions so they will only pay tax if they are making a profit.

If you refinance, it would be treated as a new mortgage and 40% deposit would bite. And you're right, rich would be able to ride out pretty well one way or the other.

Wrong.

See clause 12(1)(b) at page 10.

https://www.rbnz.govt.nz/-/media/project/sites/rbnz/files/regulation-an…

You're wrong. Firstly, the clause starts with "may". Secondly, RBNZ sets policy on the highest value a bank could lend, not the lowest amount they must lend.

A commercial bank is under no obligation whatsoever to finance 60% or for that matter any amount at all, if in their judgement they're not satisfied with a borrower's creditworthiness or any aspect of collateral. So, with falling property values, if you were to refinance, they are absolutely justified to review if they are happy with the new LVR they're advancing

Your original claim was LVR restrictions apply to refinancing. The RBNZ document clearly states that they do not (i.e. "may" means the bank "may" treat refinancing as exempt from LVR restrictions - do you get that?).

Your new point is that a bank "may" decide to not refinance if they are not happy with the borrower's creditworthiness. That is a completely different point than whether the LVR prevents the refinancing (which you claimed above).

Do you understand the 2 different claims you are making?

I don’t have time to waste on you. Keep you head stuck ostrich

We want this

Do you also want the hangers on getting first choice of the rentals. Thats whats happening. KO are incentivising private landlords to hand them their rentals and they are. Which means there is less now for others

Apparently we need paper "rich" cash poor people to leverage mortgages into houses that already exist because it provides much needed rental stock for all those aspiring FHB that were outbid.

Not sure why we don't just run a home owners lottery, pull 200 names from a draw and revalue their properties with a 10x multiplier so they can dump that equity into deposits for rental properties. Then we can put them up on a pedestal for providing a much needed service to society and swoon at how savvy they were for no dollar down investing.

Give me an RBNZ Lotto draw each Saturday and Weds with 10 mortgage-paydown winners each time - on the proviso you can't leverage the house the borrowings are against to buy another house if you want to accept your winnings.

It's only slightly less insane than the circumstances that got us here.

You cant be very good at maths. Interest rates have doubled. 100% tax deductibility of 3% interest rates is EXACTLY the same as 50% tax deductibility of 6% interest rates. There is no new tax revenue flowing. It is likely that there is less tax flowing as landlords exit the market and stop paying income tax completely.

KW - And Grunter and Orr didn't see this coming - incompetence or an agenda??

Landlords and tax in the same sentence...stop it. Tax rinse and tax free capital gains were the primary reasons for most.

...I've seen plenty paying more as a consequence, but get your point regardless - though the adjustment is tax advantageous to the State however you like to read it .

Strongly agree.

Dont forget BLT ... the brightline test forces some to keep holding, and not selling.

The investors I know are in for the long term... forever.

Oh...you mean real long term. So do you mean a coffin..?

Many will die before they see Nov 21 values again

Hi HW2,

All these acronyms like "BLT" create so much confusion. How can we expect first-home-buyers to make sense of the housing market and get their own roof over their heads??

For instance, I always thought "BLT" stood for: "Bacon, Lettuce and Tomato".

Another example: "LOMBARD" used to be a finance house. But my niece uses it to describe her last boyfriend: Lots Of Money But A Real Dick.

At least "DGM" still stands for: Doom and Gloom Merchant. (Some things never change - or go away.)

TTP

Yes, some acronyms may even cause offence such as when you tried using acronym (POW) to advance your murky agenda. With tail between legs you exited the thread after a member grilled you on links to historic and selfless wartime sacrifice.....

Hi Retired-Poppy,

I was referring to you with "POW": Problem Of the Week. 🤭

That you are a "murky agenda" is not my problem. 🧟♂️

TTP

Lol! I remember your anger when at the time it was suggested it stood for "Person of Wisdom" 😇 Correct me if I'm wrong but when referring to you it might well mean a right "Piece of work" 😆

'TTP' is another good acronym, one of the best imo

I doubt it. Tax on a profit is better than no tax on a loss.

So at this point prices need to adjust to what FHB can afford to pay.

The marginal buyer sets the prices.

It's amazing how the 20% or less fhb's think they are the most important, the price setters.

No they are just the loudest.

80% of the voting population own property already (no voters and no hopers don't own property, owning property makes you far more likely to vote as you have skin in the economic game)

Can't wait for election time!

I disagree. The FHB segment is where the most crucial buyer is for setting future price direction. Thinking that the boomers and existing property owners can trade among themselves without new market entrants is little more than magical thinking. It would be little more than a circle jerk.

"owning property makes you far more likely to vote as you have skin in the economic game..."

Its the only game in palmy, unless you are a member of the squash club.

Correct. Its a repeat of the Uk in the early 90's. FHB's dictated the price, leading to house sale chains waiting for a buyer at the entry level.

Nah!.. us " greedy baby boomers" cash buyers with few conditions are ready to pounce!!

Thanks Jacinda, Hipkins and Orr...

You're incompetence is Awesome

👏👏👏👏👏👏👏👏👏👏👏👏👏

47 votes is probably the highest I've seen. Well done rastus

Don’t forget the WAR will you children.

Wow - there is no way the economy is not going to stall as people roll over mortgages.

In akl going from $604 to $904 a week mortgage repayments, an increase of $300 a week ( $15,600 a year) is about a $22,000 pay rise to offset this. Which if you take the med salary would be a 15.3% annual pay increase - i know most people are not getting these salary increases at the moment.

Add on food increasing 12% YoY.

So the most likely way to offset this increase to mortgage repayments is to reduce expenditure on non-essential items.

This will test peoples budgeting skills.

TimeToPrepare

Add to that the possibility of companies restructuring and layoffs this year.

test peoples budgeting skills

Tough times make people look at the options.

So where is the harm in that.

As a future FHB (Wellington), I’m more hopeful than ever these days despite rising rates. House prices have a ways to fall until FHB can more easily enter the market (imo).

Edit: For reference, I’m currently pre-approved for $500k, but realistically only would borrow $450k max. With a $150k-$170k deposit, I’m looking in the low $600k’s to buy, or $550s for a fixer-upper 3-bedroom with good layout and decent bones. Seems like the Hutts have some homes in this price range already, but I’m looking in a specific part of Welly. I need to move out of my rental by Jan (homeowner wants to sell), but I think winter/spring will provide some opportunities.

All the best for your search. I've been keeping track of the properties in certain Auckland suburbs on offer over the last couple of years using the same set of search criteria, and over that time I've gone from "They want how much? For that? Who would buy that?" to, more so in the last 2 months, "That looks ok, I can imagine living there." Affordability won't improve overnight, but at least now you won't find yourself overstretched and stressed having purchased at the peak.

hang in there - they'll start to look even better as we move into '24

You will see better prices soon given the amount of inventory.

Who's to say your landlord will be prepared to meet the market at that time. Be patient hutt prices are waiting for rest of country to catch up before taking another big drop

What part of Wellington are you looking in? There is the odd listing currently in the $550-650k range but you'd be looking at some serious cash to get them livable so being patient or flexible on location will help for sure. Good luck!

I’ve had my eye on west Karori for a while.

Can recommend. Ever younger demographic, no motorway travelling. Has great access to mountain bike park, swimming pool, library, supermarket. Genuinely takes me 25 minutes to cycle home from Terrace and I am 50 this year (be 15 on an ebike). That biking infrastructure also slated to improve. Buses are unpredictable at peak times but you'll get a seat at W. Karori in mornings. If you can find somewhere slightly lower in the Karori bowl, wind decreases markedly. Summers hot because its a bowl but equally winters are a degree colder - so if you want a really nice life, get central heating. 13k incl boiler for me. An investment you will never regret.

Cheers, Uncle B!

Wellington is a a disaster for poor infrastructure and pending large earthquake.

When the big one hits you will not see a cent from the EQC/ govt money and the insurance companies will rort you!

Slash has nothing on a big quake in wellington.

They need to move the capital to Northland! Or anywhere safe!

You started Happy Hour early today Hemi?

Reality sucks sometimes.

Ch Ch and Welly are high risk areas...

I put an object suspended from the ceiling. (Tall building). Every time there is an EQ, everyone looks at it to see how big it is.....

Whats a FHB?...

1. Kids with rich parents subsidizing the whole house purchase?

2. Kids with a mortgage.

If I was a young person I would be in Europe earning euros and saving big $$$.

Com back in 3 years and double your money .. but why come back?

NZ has sold it's mojo to the leftie costly idiots!

Second this - I recently moved over the ditch and I wish I had moved earlier.

Most kiwis I speak with average 25/30% pay rises when moving within the same industry..

Even within the same company.

I did a secondment a few years ago and I couldn't believe the wage/salary difference compared with NZ.

Buying now is madness.

The market has a fair amount to fall yet.

I suspect its madness to buy now because it wont drop much further but rates will pause briefly then head up again as inflation gets a boost from bailouts and war.

Massive risk levels at the moment to commit big money (yours or banks).

I concur. Reserve banks have been too slow and too scared with rises so far. Russia/China likely to drag out war and find ways to fuel western inflation and banks runs. If the fed blinks and pauses then money will flow quickly driving prices up. The us has 200+ banks not stress tested etc that may be at risk and i hate to think what their corporates are still hiding (likely many heavily indebted and zombie companies ready to drop). Europe has least one dodgy bank left ànd in the uk we face a terrible propsect of a labour govt. France stilll has riots

In NZ teacher and other public sector pay rises to come, flood insuramce payout to spend on rebuilds/infrastructure rebuilds and food damage, building materials another boost, pension and benefit increases, election yr spend and wage rises will fuel inflation locally a lot... let alone baked in rises to come. And interest rate rises havent bitten enough yet.

Theres trouble at mill. My gold nuggets are safely stored under the pillow (in my beds in the bunker and the ark) for a couple years.

I wonder what the typical demographic of FHBs are, vs that lower quartile property suitability.

IE., how many families are waiting till they can afford houses, vs single/childless purchasing townhouses?

We're in the former category, not even close to tempted by the offerings atm (the houses that would suite our family are still asking double what we can afford - and we earn well above average).

From what I've seen at open homes is people mid 30's and above. Some bring children and most others look like they have children. We have large family, income above $200k.

look like they have children? You can tell from the bags under their eyes lol

The car seats are usually a dead giveaway..

Along with dribble stains and vomit.

It's not really "affordable" if you're still borrowing 10x your deposit to get a house.

Yawn, property ponzi, hope it collapses.

Yeah, its hopeless. I am a humble renter but I suspect there is plenty of cash lying about to pump things up again soon. Maybe spring. Even though the numbers don't make sense buyers will be there anyway. This has years to play out, and the ponzi black hole still has plenty more to fèed on.

Not for a few years. Inflation is still way out of check and it looks we like need a recession and some decent unemployment figures to stop the wage growth. Expect more ocr increases and a lot more house price falls.. there will be a lot less cash lying around by the end of the down cycle so prices wont go up quickly at the start of the next boom..

So the national median lower quartile selling price will need to drop a further 39% from $565000 to $340000 to equate to 3.5 times the median income for 25-29 year olds (Feb ‘23). Would be great if it could happen. Certainly increase the happiness factor for our young folk.

So either be a bagholder with a house that's dropping through the floor relative to the servicing costs of what you borrowed to pay for it, or sit on the sidelines trying to save in the meantime while your living costs explode and your savings are being eaten by inflation.

Or.... Queensland.

You've got to count the cost. No feijoas in Queensland, and aircon there is only just catching on.

So I move to Queensland, start a business importing feijoas as a premium item that is dirt cheap in NZ to get hold of and live like a king in an air-conditioned mansion? Sounds legit.

These numbers show why there is so many sales occurring for fhb even in this slow market.

A new fhb on 20 percent deposit went from 32 to 47 percent.

Thats roughly the same as low equity buyers were paying 2 years ago (45 percent).

So where's the problem that doomie gloomies have with new fhb entering the market. Sure its a higher cut of their take home pay but it is do-able for them.

The numbers don't lie

I dunno man, maybe it's the $155k deposit they were never able to save for?

Despite the obvious truth that for aspiring FHB's, fiscally responsible home ownership remains out of reach, for Spruikers it all sadly comes down to colors. The insightful amongst us say its white, heavily vested HW2 says its black - just for the hell of it. Its best FHB's steer well clear of this market and let the over leveraged fall over en-masse first.

by redcows | 22nd Mar 23, 12:31pm

... dribble stains and vomit.

Compliments to you HW2. At least we can count on your communication being primitively consistent :)

Much as I would vote National this time round I cant with their plan to reinstate the interest deductibility

I deplore National for prioritizing speculators and landlords over the welfare of society.

The welfare of which part of society? The middle class FHB or the low income/welfare dependent who can no longer even find a house to rent that they can afford and are now waiting on the Govt to spend billions of taxpayer money in building them a brand new house?

A society where the rich get richer simply because they can deduct the interest on their mortgages as investors and speculators, while regular people cannot. Nats are proposing exactly that, which is not acceptable to me.

This sounds exactly like the voices in my head.

- SMG.

Exactly.

Potential Fhb's are a tiny fraction.

Most renters are life long renters and are hurt by labour's attack on investors.

Labour trying to please the 20% at the expense of the other 40% who will never buy or remaining 40% who are providing the private rentals that the govt can never afford or be capable of providing

Simon - If you didn't have such an amazing name, I'd be angry.

Instead I laughed out loud at your take that potential FHB's are a tiny fraction (I am a young person, no young people own homes, what are we then?).

Then I fell off my dinosaur when I read that 40% of people are providing private rentals (literally 1/6 of properties in NZ are owned by investors/greedy boomers that own 20+ titles)

-SMG.

80% of stats on the internet are made up on the spot didn't you know??

Anyway - search NZ elections and show me a government that held power during house price declines.

Last time 2008 labour lost to Nats.

Voters like house prices to not fall at a minimum even jacinda knew that (maybe why she jumped ship)

not maybe, this is exactly why

That has definitely been true in the past, but the thing about concentrating property wealth in the hands of fewer people over time is that their collective voting power gradually shrinks.

The ground has been shifting and the boomer generation's grip on power is becoming more tenuous. It would be good for political parties to take note of that.

Seventeen percent of the survey’s respondents are worried about falling house prices, but 48% feel neutral about them, while 32% are optimistic about them.

Among the 18 to 24 and 25 to 34-year-old groups, optimism was particularly pronounced, at 53% and 43% respectively.

In contrast, 83% of respondents are worried about the rising cost of living, while 76% are concerned about high inflation.

(Edited to include more from the article.)

Simon, I wonder what else happened in 2008 that could've had an effect?

Here's a source for you to decide whether or not it's made up :)

Mega Landlords: Over 22,100 homes owned by small group of very large investors | Stuff.co.nz

Now do you have 20+ properties or do you just hate young people?

- SMG.

Can it be both?

Either everyone should have it or no one should have it.

Agreed either option could work , but the option of interest deductibility for all would be administratively clumsy, so no one getting it seems more straight forward

Ok .

On that logic every owner occupied home owner then should pay TAX on the equivalent income they are earning by not renting the place.

See how basic it is?????

Or maybe the property investors enjoy the rent benefits without declaring it as earned income as per the owner occupiers?????

No. Because I cannot rent a property from myself. There's no transaction taking place to capture as income. IRD gets a bit wound up if you start inventing things when you claim expenses, so I'm not sure the logic should work the other way either.

You just answered your own question as to why owner occupiers can't claim interest as an expense (or maintenence insurance or rates!!!!!!!! Hell why stop at just finance expenditure???).

Painful. . .

I know the answer. I also know the same house in the same hands of a tenant shouldn't give rise to a tax deduction despite it being used for literally the same activity, because that's absurd :)

Why should investors be allowed to deduct rates and insurance and maintenence?

When owner occupiers are not?

Place be clear when you explain why this is currently allowed.

Thanks.

Sorry, I wasn't aware I personally had to justify the status quo of our current tax system. I didn't write it, btw, so you might be asking the wrong person.

Why should there be a distinction between income from property vs income from salary or wages?

I derive an income from having a roof over my head, and the required maintenance that goes with it, otherwise it'll be awfully difficult to function at work if I am living under a bridge.

I just bought a car on a 20% loan, no deposit.

The car rental firms can all claim their interest expenses on their fleet of cars they rent for income, why the hell can't I???????!!!!!

I'm outraged!!!

No wonder I can't afford the latest Tesla!!!! Beaten by all the car rental firms!!!!

/S!!!

...

Business interest rates?

You mean the risk based rates the market/ banks set based on the security of the loan?

They always have.

"Unconventionalview" said "Ok so long as property investors pay business interest rates".

Then deleted it after my reply which made them look economically illiterate (could they be Grant Robertson himself? Good chance!)

Simon you are being simple. Renting something short term is different than renting a roof for life. Renters are paying for the home - yet the landlord gets to own it.

Hiring a car is not a lifetime activity for most. So your brief rental doesn't buy the car and the purchase is paid fr by multiple short term users

Renters are financing a home and the tax system allows ownership to go to the landlord who had leverage and tax advantages.

This is not okay.

So you want to compare hiring cars and equipment with houses. You're better doing a rent to buy scheme if that is your goal.

Then if the market tips over just post in the keys. That way you get all the reward and none of the risk

Simon you are being simple. Renting something short term is different than renting a roof for life. Renters are paying for the home - yet the landlord gets to own it.

Hiring a car is not a lifetime activity for most. So your brief rental doesn't buy the car and the purchase is paid fr by multiple short term users

Renters are financing a home and the tax system allows ownership to go to the landlord who had leverage and tax advantages.

This is not okay.

Rastus - would you prefer landlords provide only short term accommodation at $250 per night as per car rentals of that term?

Also - explain my tax "advantages" V if I ran ANY other business in NZ?

The government makes whatever rules up that it wants to get the best outcome for most people. For examples they put extra tax on selling alcohol because of the negative effects of that product on society. The more they dis-incentivise people owning other peoples homes the better IMO. It is an industry that has far outgrown it's purpose of providing flexible accommodation, and has moved into the realm of speculative overpricing of the most expensive thing people ever need to buy. Effectively taking away the security of housing of many families growing up, while greatly increasing inequality.

Most house sales are by people upgrading homes.

The idea of buying a first home, doing some cheap DIY, seeing it go up in value over time (and incorrectly thinking it was all because of that awesome illegal deck you knocked up), then buying a more expensive home is what fuels the upward pricing in NZ housing.

Price rises breed price rises - every time. And unless the govt goes after the little home owner that does his house up and waits for the market to rise before paying more for an upgraded house, then nothing will change and the next time a 2% price rise happens that will again get amplified by this dynamic into a 5%, 10%, 20%, 30% until everyone again looks around at each other and thinks "gosh that's a lot of money".

Property investors play no role what so ever in this dynamic. They are the classic red herring.

By targeting property investors all you do is hurt renters as 90% of rentals are provided by private landlords.

A correction of 20% after 150% gains from the dynamic I described in paragraph 3 above was always going to happen.

What's the "real fair value" of NZ property? First, look at the cost of replacement. Provided population increases then at the margin a new build house becomes the price setter - or the "buffer zone" that kicks into gear to respond to any increase in demand (any population growth intrinsically provides for a degree of increase in demand) - It only kicks into gear once existing stock price justifies building new. That's how/why the new build price sets underlying local house prices of all existing stock.

I bet you do own a Tesla though ;) gimme a place to live ya rascal boomer landlord

"You must be this tall to ride."

That's what it feels like anyway, a year waiting in a queue for a roller coaster. Watching the test run as it swoops and toils. Interesting how many still see a +0.75 rise, with all the noise about a stall. We will follow all the way up, but I don't think we will be as hasty to follow back down. Opportunity for NZ lies in strengthening the dollar off of a FED pivot - maybe that's my naive opinion.

But this 'fhb today worse off' would only apply IF the 2021 fhb was still on the same low rate.

But how many of them still are.

Most will have or just about to roll over onto the newer higher rates.

Relatives have spent 6 months living with us. Sold but couldn't find a buy at right place right price. Finally have, and made a cool $100k or so by being able to be patient. A number of sellers lost an opportunity because they couldn't see the market.

It's a great market for fhb to be patient and make heaps by not jumping . Of course not possible for everyone.

So you're saying buy now. Congrats to your family

US Banks have a collective 620 billion hole in their balance sheets. The securities they are holding to maturity are currently worth 620 billion less than their balance sheet value if they had to be sold tomorrow. Smaller US banks are now offered the chance to hand their securities to the FED and be given loans at a convoluted interest calculation. But call it 4.5%. But the loan is only for one year. In one years time they have to take ownership of the securities and the problem again. If the FED funds rate is still 4.5% in Q1 2024. Then those securities are still only worth 75% of face value.

So short answer is the FED needs 1 more year to get inflation down. Then cut rates to stimulate out of the recession they caused. Then all those long term securities held by banks will have their value restored a lot closer to par.

Only a $620b hole? I'm sorry, but these days unless a problem is worth trillions it looks to me like a comparatively small deal, a few months of brrrrrrr....

Thanks. Its something else to factor in as/when Fed/RBNZ review OCR.

I believe that the house market is falling way faster and there is more desperation than what is shown in any media so just wait!!

We were looking to buy in the pre-pandemic times but it was a real nightmare, you would be viewing any open home with an army of people and the agent would not even talk to you. During the pandemic craziness we decided not to get into the frenzy so we just waited. Last Sunday, after lunch we went for a ride to check a couple of nice houses just to have a feeling for the market (three rooms, garden, good location). We were the only ones doing the viewing, the agents were really nice and insisted that the owner would consider any offer. Both houses are in the market for a price that is between the 2016-2017 QV price. The agents called me the following day asking if we were still keen on the houses. I told them that we are just waiting for the market to carry on falling (as it will keep on doing for the next two years) The first house went down that day by 50K. Is this experience just anecdotal o do you think that it is the norm? Has anyone got a similar experience in the last month or so?

As stated elsewhere. I'm seeing, Auction > PBN > Fixed Price > Reduced Price > Further Reduction to price > Withdrawn without sale.

Tumbleweed because agents are telling Vendors porkies to get the listing.

Iv'e seen this but also Auction > PBN > Fixed Price > Reduced Price > Further Reduction to price > Sold (Price TBC)

Hi Jaoquin

not sure where you are. Prices here in Wairarapa still listing at high levels…. Close to market height. But same experience as you, went to two open homes…. No one else there, then agents of each rang the next day. I get the feeling that buyers have now gone and agents are working with a very small number of interested parties. As with you we will wait a bit before buying.

There's some desperation coming through in my Ray White mailings for Wairarapa. For the past 2+ years the subject line has not changed every week. "Weekly Listings Update" and the odd "How is your local market performing?".

A month ago they've changed to a much more emotive "BEST VALUE properties are right here!".

Yes, in my area where I am looking back in Oct last year a 4 bedroom house was going for 1.35 to 1.4. Now, a similar house is now 1.2-1.25.

So in a little under 6 months prices have fallen by up to 150k. Luckily I didn't offer a higher price at the time. This is in a new subdivision too.

I think this winter will be a great time to pick up a "bargain" for investors. I am guessing easily another 50k lower which means going from 1.4 down to 1.15 for a brand new 4 beddie!

In the last few weeks 3 banks have fallen over, one a giant systematically important one...... Does this erode confidence, is this normal... no there is a serious recession coming, and the only way stretched vendors will sell is to meet the bid.

I look forward to scooping up a cheapie!

FHBs need to think smart & pull their heads in. The goals should be:

1) stop paying some else's mortgage (i.e. rent)

2) accumulate capital as fast as possible

The answer could be a 50-60sqm, 2-bed inner city apartment (or the like).

In Auckland these can be had for $350k in a building of average quality but still with an okay view.

A 20% deposit is some $70k (the bank of M&D and Kiwisaver can help here.)

That leaves a mortgage of $280k at 6.5%.

Now the trick is to structure it right. You want to start with the first payment being at least 1/2 capital repayment and 1/2 interest. If you can't manage the repayments at 50/50 then keep saving and get a bigger deposit.

Using the full function mortgage calculator on this site a $280k mortgage at 6.5% over a 11 year mortgage - yes just 11 years - will need weekly repayments at $685. This is way within the typical dinkies (double-income-no-kids) capabilities.

By year 5 they've accumulated $103k in capital. By year 7, it's $150k. Add back their deposit and its $173k and $220k.

But wait ... there's more ... What say interest rates fall closer to their long run averages of 5.0% but they keep up $685 weekly payments? Or what say they "fix long" when rates are below long run rates? Say 4.5% for 5 years. And if they increase their repayments in line with annual salary / wage increases? Or maybe take in a boarder for the 2nd room at $220 per week?

Suddenly they own it outright in less than 7 years! Suddenly they have $350k for their next deposit and by being smart again they buy their next place with using the same 50/50 rule and ... :)

The full function mortgage calculator on this site is just brilliant. Show your kids! (Because the banks never will!)

Ashley, I thought you had gone awol?

I don't know where to begin with this. I could live for free in a local park too. And there's zero chance it will leak on me, drop in value AND there's plenty of space for me to park my car. FHBs should just aspire directly to homelessness tbh. Anything more than that and they should "pull their head in".

lol

Funny that the replies thus far do not offer up anything of substance by way of rebuttal.

Are they amongst the following groups:

- Landlords who simply don't want people doing anything except renting their houses and paying their mortgages?

- Banks who want to you to leverage yourselves to the hilt and keep paying a mortgage for 20, 25 or even 30 years?

- Embarrassed homeowner who didn't do this so ridicule anyone that doesn't make the same mistakes they did?

- Wealthy older people without mortgages who believe everyone should return to the 60s?

Did I miss any other groups?

I should confess this is exactly what I did buying my first property. In London as it happened. I rented it after 6 years when I bought a bigger, better house using the collateral and using the rental income to augment my own.

You're not wrong, but you missed a large part of the problem - for the last decade, the vast majority of FHBs simply couldn't do it without tapping back into the ponzi via Bank of Mum and Dad's increased equity. Property has been out of reach (caused by the inability to raise ever-increasing deposits, NOT an inability to service the mortgage) for almost an entire generation of young people.

A lot of those young people (and you see this in the anecdotes about who is attending open homes) chose not to have their whole life revolve around purchasing a property, so generally went and got on with their lives, even if this meant having kids in rentals. Your proposed solution simply doesn't work for them - at least not in NZ.

If NZ apartments weren't total shitholes aimed at either the student market or retirees, it might be different - but here the apartments you're referencing are either tiny little boxes with a kitchenette and shared facilities, or a village of geriatric nimbys who really don't want the family with the noisy kids on their floor, no thank you! (or the future gardenless slums of Hobsonville, ye gods).

The kinds of apartments that suit this particular cohort simply don't fall within your proposed budget, nor are they differentiated very much [yet] from the general property available in NZ due to the compression that occured at entry level properties due to the activity of specuvestors. As I've explained before, this is why many FHBs were forced to go with new builds, despite the risk of failure/sunset clause/etc. - because that was where they could outbid investors (thanks, government grant!) and get something suitable for their family.

It worked for you, and it will definitely work for others. But it won't work for all.

Will you also confess to getting a London level salary, and not an average NZ one, I wonder?

Although the recent price falls at the lower end of the market have been substantial, they have only retreated back to where they were at the beginning of 2021. And first home buyers are likely to be significantly worse off now then they were then because mortgage interest rates are much higher

I actually don't agree with this. I'd much rather be paying a higher rate of interest on a smaller principle than a low rate on a larger principle, even if the repayments are higher. I can't influence interest rates, but at least I have some control over the principle I owe, and can be fairly confident it's not going to double in the space of 6 months like interest rates did.

agree.

lock in a low price - the money is made when buying - the time is ripe.. In only a few months we will likely see interest rates plummet with the next global financial crisis and banks lock up shop completely so now is a pretty good time to buy if you can

Best time to buy property? yesterday.

Next best time? Today.

So you depend on real estate commissions then Simon.....

Even Blind Freddy can see that your statement above is plain stupid.

The Best Time to Sell Property was Nov 2021 when people where paying stupid money

The Best Time to Buy Property will be when the 6 month moving average of the Monthly average price turns positive.

There is a clown along every 5 mins on this site telling you to buy now, and has been for the last 12 months...... Ignore them, care in the community has just gone a step to far.

for only 12 months??!! haha.

young fella.

10 years ago I won a bottle of red from Matt Gilligan from GRA by claiming Palmy would beat Auckland in cap gains. Still waiting for that bottle matt

Relatives in Palmy are saying that the housing market there is very soggy. That they expect prices to drop a lot more even from where they are currently at. Just like Wellington. They are both windy holes and got vastly overpriced for what they have to offer lifestyle wise.

Priced in NZ Dollars????????.?

You'll find it's actually a bargain

👌

Bullshit!?

depends on your circumstances and your sell time.

if its your family home you flip in 2 -5 years then buying in the bottom or just in the up cycle is key.

Anybody who brought in the last 3 years , in the up,and is selling now will think today is bad as is tommorow!

If your buying today to sell in 20yrs?. Ok?, But 5 years... dodgy?, 2 years ? Crazy!

People need to wait until 8 months time, the way price’s are falling could be down another 15% by then and the falls could continue for most of next year. The one thing that will not is house price’s going up for a number of years .

Or could simply miss out on right house right price

As above, Redcows relatives searched and finally found what they wanted after 6 months looking.

HW2 if a FHB had purchased this time last year as per your recommendation they would be in negative equity and now be refinance in a terrible financial position. Not sure if you understand basic financial information why do you keep pushing purchasing properties when the market is crashing.

Correct!

Interest deductibility needs to be reinstated ASAP otherwise there will be a shortage of rentals in 12 months and the new government will wonder why.

Its not good that mum and dad investors who have been trying to set themselves up for retirement are getting shafted by a knee jerk reaction by a govt with a communist philosophy. End result is a cashflow negative but paying tax - what other business has that!

How many other businesses have a single asset, trade at a loss for years and then only ever generate some kind of return when they sell the underlying asset for what was a totally incidental and apparently unintentional capital gain?

Are you sure you want to play this game?

Epsom - that is just not true. There won’t be a shortage because fhb will be buying them, leaving the place they are renting vacant. There are also still heaps of new builds being built and rental prices are now static or falling. Most Kiwis are happy with this because it’s good news for their kids, renters and society as a whole. The only ones complaining are specuvestors who are finding that their gravy train is no longer working for them. Well sucky boo, they have had it so good for so long, let young people have a turn.

Spot the overleveraged.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.