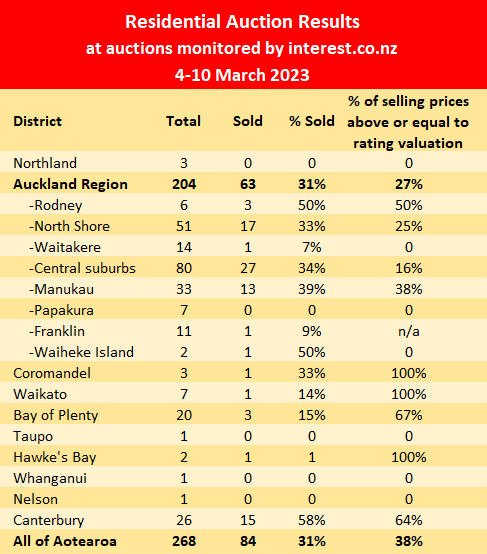

There was a slight decrease in activity at the residential property auctions monitored by interest.co.nz over the last week (4-10 March).

Interest.co.nz monitored the auctions of 268 residential auctions around the country, down from 293 the previous week.

Of those, 84 were sold under the hammer, giving an overall sales rate of 31%, down from 37% the previous week.

The main reason for the decline in total auction numbers was fewer auctions in Canterbury and several provincial centres compared to the previous week, while auction activity was up slightly in Auckland.

Prices remained soft, with just 38% of the properties that sold fetching prices above or equal to their rating valuations, while 62% sold for less than their rating valuations.

At the major auctions prices appear to have been firmest in Christchurch and weakest in Auckland's central suburbs.

See the table below for the district-by-district results.

Details of the individual properties offered at all of the auctions monitored by interest.co.nz, including the selling prices of those that sold, are available on our Residential Auction Results page.

The comment stream on this article is now closed.

- You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

111 Comments

As someone posted yesterday, there's a lot For Sale in the relatively small suburb of Rolleston (400?). And in that wider area of Selwyn, 893. And just 26 went under the hammer in all of Canterbury where Trademe tells me there are 5,107offering of all types available?

Auctions don't make too much sense for vendors in a market downturn - unless the property is highly desirable and (fairly) unique.

Remember that houses "passed in" at auction carry a red-flag if/when they go back on the "open to offer" market. They're very much in the "also ran" category, ripe for picking up low-ball offers.

TTP

I disagree TTP, I think they have already demonstrated a lack of understanding of where prices are... don't waste your time.

In all honesty, it doesn't really matter what happens in the New Zealand property auction sector.

It's what happens in the global financial markets from now - given the SVB episode (it's spreading. See below). I know it looks like an isolated case, but either fear of counterparty lending drives interest rates up or the Central Banks decide to press on and ....drive interest rates up. The alternative is for CB to ease back to defend The System, and that will drive Inflation up which will....you guessed it ...drive interest rates up. Pick your poison, so to speak.

https://www.reuters.com/markets/companies/FRC.N/

Agreed. A large chunks of the bbq bragging speculative have no idea on the stuff that really matters. Rates up much higher for much longer is the future.

Was talking to a property developer yesterday. His thoughts on residential investment at the moment were .... "a financial suicide mission"

My property investor friend tried to convince me yesterday that I need to start looking to buy now otherwise I’ll miss the next upswing - lots of bargains out there he says. When I said prices are accelerating to the downside and interest rates and still going up and will stay higher for longer than expected, he replied with certainty that property doesn’t go down much in Auckland and I need to get ready otherwise I’ll miss out. Oh and he’s an economist…

This Ponzium spruiked hard by the paid commentators AC and TA on the likes of Granny Herald and Onewoof is ingrained and hard to break for the addicted.

Another good solid interest rate rise, bad property loan instigated bank run, will put paid to it?

We are on a wild ride though. We might be looking at the start of a series of bank runs in the US, and the Fed will surely consider this when it does it's next interest rate review on March 22nd. The runs could pressure rates down.

The ultimate trajectory is reduced asset values and standard of living for most of us, but the route is twisty turny.

Any percieved delay/pause/fear in stepping up rates to combat inflation will mean rates may have to go higher in the long term - causing worse problems.

Fed has no choice.. they know there will be significant fallout. The better option is to go higher earlier

Sheeple keep the faith untill they are living in a cardboard box under a bridge.

Usually that's when faith is stronger.

Never took a shine to the word sheeple. It's like a religious person who thinks every other religion is nonsense apart from theirs.

Certainly agree, NZ property is the most lagging of indicators, the news to watch is elsewhere.

Re your FRC link: Another west coast stock with a collapsing share price. Part of the unfolding picture of high risk tech being the hot potato everyone is trying to drop. I wonder if we will be able to scoop up some US IT workers to fill some gaps?

By lagging do you mean it’s taken 15 years to get the downturn from the GFC that everyone predicted?

And all it took was a global pandemic for people to feel like geniuses.

I think the property storyline won't be as popular over the next 12 months. In an interview the other day with Powell he tentatively agreed that unemployment in the states needs to get to around 10% or more, in order to bring inflation to where they want it.

The 15 year lag was global can kicking by Monetary Policy, which made a bigger crappier can.

The lag I'm talking about is between inflation in major economies driving interest rates and now finally poking NZ in it's debt bubble.

A lot of web chatter this morning about this. Expectations that small banks will suffer runs, and any good assets they still have will be canibalised by big banks, leaving bankrupt husks.

SVB seems like a storm in a teacup. A “bank” that invests in a single vertical goes bust when that vertical has a downturn is hardly a sign of market contagion.

Nevertheless, something like US's 18th biggest bank. Apparently quite a big teacup.

TTP, That's not what my property brokers agent told me for the recent auction campaign....

Prices remain soft?? That's is incorrect.

The auctions remain soft because the vendors are expecting unreasonable prices.

Prices are really really strong and they are in expensive territory where only a few like top 5% can afford it.

As one article mentioned a few days ago, No one else in the world will touch with a barge pole. Now whether that's paying interest rate on mortgages or the price of houses.

The market needs to come in realistic and reasonable category where an average earner can buy it and live a life too.

Yes....this collapse will run to a 40 to 50% loss, back to the early 2010s prices.

Is this the time to score a house? This teen buyer says yes | Stuff.co.nz

https://i.stuff.co.nz/national/131397209/is-this-the-time-to-score-a-ho…

This story must be fake news

Your son 🤡?

He was probably too young to take out a mortgage in Nov-21 - right? The naive are good at teaching those with patience what not to do ↘️

Hopefully, he can get some flatmates so he can stop doing 100hrs each week. Or find a job that has overtime with penal rates.

Why not work 168 hours per week?

When he reaches 50 he can be on stroke anticoagulants and fed through a straw. NZ's obsession with houses as the primary means for gaining financial security, while backed by disturbing levels of debt, could wind up contributing to the undoing of our social fabric. Which do we really value more? Lets take greed out of the equation and then ask ourselves the question....

Our social fabric is already buggered. It's running on the fumes of shared religious identity and held together by an almost illusory legal framework.

At worst greed and debt were the shotgun shells as poor Bessie got led round the back of the barn.

You're at your most insightful at 3am Mr P.

Hearing Winston on 'best of the country' was also insightful. One four letter word he mentioned was 'work', something I am about to go off to, Hi ho hi ho

by HW2 | 12th Mar 23, 6:07am 1678554452 - "Hi ho hi ho",

Having to work on a Sunday, which one are you? Grumpy or Dopey?😣

Leveraged perhaps? Banks need their interest... I don't mind working a Sunday, if the terms are right of course

Imagine back in the day if there was a sabertooth Tiger attack at 10:30 on a Sunday.

"No Mr Tiger, didn't you get the memo? It's mandated there's 3 breaks a day and only 40hrs a week. We'll have to do this tomorrow sorry"

Yes, a lot of occupations have their contractual "claw" backs... 🐯 😆

Dad joke.....

Plus overtime

Instead of a house he should be leasing or buying his own machinery and contracting back to his employer and other farms.

He can then work as hard as he likes to grow a business - but with his strong work and saving ethic, and some mentoring he could set himself up financially for life by 35 or 40.

Instead he's been sucked into the property ponzi that needs fresh capital by those with vested interests

“Real estate agents reckon in three years time the prices will be high again, everyone is saying it is a good time to get in,” said Thomas.

He needed to stay home where Mum cooks all his meals and does all his washing.

After a bit more experience surely.

You don’t get those hours lost working ever! Life is all about balance and working 100 hours a week is not healthy either physically or mentally no matter how young you are. All you are doing is working eating and sleeping. Should someone be operating heavy equipment 100 hours a week from a H&S point of view? In my day I worked 45 hours a week max, my wife never worked as there was no need to and my biggest house loan ever was $100k. We have only had 3 family homes and the current one is worth $3m or so as agents say. Property has certainly got ridiculously expensive in Aotearoa.

I wonder how many families could get ahead on a single income max 45hrs a week these days.

That’s my point

When all the other wives' wanted to have a life outside of kids, the relative value of labour declined so eventually households had to work well more than 45hrs to get to the same place.

Life's changed a lot in 50 years.

Housing is expensive tho. Although for way more reasons that the most commonly cited culprits on this fair site (greed and boomers).

Th term and mentality in NZ of 'getting ahead' is the issue. Everyone feeling they have to 'get ahead' of others, like the obnoxious people needing to get on the bus first to get the 'best' seat.

I guess it depends on your take of getting ahead. Many young couples are in a position where they are fearful of their financial position if they decide to have children. The ability to keep their head above water with a chance of owning their own home is now ambitious.

Just shows that despite their fake ‘socially conscious’ facade, Stuff are just as complicit as Granny Herald.

They have a "homed" section, where half the articles are just advertisements for houses for sale. Shows their journalistic integrity

This just in: most news media is paid advertising in the form of infotainment.

Dp

Housework’s you never fail to give me a giggle with your eternal spruiking but this is desperate even for you.

Thanks mate. But not spruiking, observing. It gets the doomers triggered doesn't it.

Na, it doesn't mate. Just shows how ignorant you are

So you have pretty much admitted right there to being a troll, which was pretty obvious. It would be good if this website could ban trolls ie. people who are intentionally trying to trigger people.

Haha you're joking

You just cant stomach my POV which beats yours

Sounds like a mint life for a 20 year old. Work arse off, live like a hermit.

Great epitaph.

Losing all that deposit will be the icing on the cake.

Most of the 20 y/o I know that worked like that are now 40 and work part time and play golf and fish the rest.

The 20 y/o I know that "made the most of their youth" are now 40 and neck deep in mortgage and are looking at another 15 to 20 years of slog.

(And I'm sure there's everything in between).

A bit like having kids, we had ours young and are now enjoying a few drinks with them and their mates from time to time. Most of our friends are still dropping their kids at kindy.

Each to their own.

Little disappointed no data for wellington, oh well I've stopped going to open homes for now. Vendors looking for far too much. Rents are still unbelievably high (we looking at $800/w) if we go renting. Might look at buying again end of the year, hopefully, will have saved an extra $50k by then anyways.

If you are Wellington-based I would wait and see what happens with the election. If National win and have a major cull of the public service that could add further impetus to price falls.

As an aside, what happens to all those who get culled? Do they become unemployed driving up the cost of Welfare Payments? Emigrate? Work for less somewhere else and drive down wages? Get rehired as permanent Public Servants and keep the cost to the taxpayer similar to today's?

Good question. Depends how big the cull is. There is every chance National’s cull won’t amount to more than a tinker, so maybe it’s not a big cause for concern.

If I was dictator for a day I would smash the Wellington bureaucracy. I think you could easily chop 25% of the bureaucrats out, who are working in the highly wasteful policy space, and fundamentally restructure things. Don’t know what that means in terms of people, could be 2000-3000? That would be a saving of circa $ 200 million per annum

Maybe it’s a possibility if the Nats need Act - which they probably will to form a government.

As to what those people would do, who knows.

In Hitchhikers Guide to the Galaxy they are given the honour of leaving on the first colony ship.

Of course, there was no second or third colony ship, which was odd...

For either party, a cull is already in motion and has been for months. These things don't happen overnight but also nothing is set in stone.

National will likely thin the herd more, we'll see if and when. Maybe I will get caught in the crossfire and will be on the market so to speak.

Although National will give property investors a 33% income tax cut (from 33% to 0% providing you keep loading it up with debt) and a 100% capital gains tax cut (for those that sell between years 2 and 10).

I think they'll loose more votes than gain on that particular issue. Surely if you're running a business that invests in property the interest is deductable as an expense anyway? Loss in capital this FY also offsetting profit? Haven't checked this out though tbh. Maybe I'll do a degree in accounting, probably need to at some point anyways

Houses I look at in Auckland.....I tell the RE Agents that Im only interested in a potential return/yield of 8% now......so come back to me when they cut the price by 40%.

It wont happen quickly, but it will. Higher interest rates, for longer, will demand it.

Dont be in a hurry and walk away from most that are not near 8% earners.......or your deposit could well dissolve as the yield becomes king.

Underwater homeloans must be so demoralising!

PS...scullerious RE agents hate you talking yield, as they know you cannot be duped by their slick willy but misleading sales "safe as houses" spiel.

You will be waiting a very long time, possibly forever.

As every day passes another property owner/home-owner is going to be trapped with their holdings.

One way or another lenders will keep their loans regular, but those owners will be unable to move. The sale price will not discharge the loans outstanding, but the payment will still be met. So they'll be kept in limbo, and why prices aren't budging at the moment - they can't.

Only those who have sufficient equity will be able to drop their prices (all the way to $1 if they own outright). But many, if not most, of the buyers for their offerings will be those trapped with what they already have. They can't sell so they can't buy.

The number of qualified buyers and market velocity is going to plunge as prices 'ease'. And so as time passes, the prices will keep falling.

Once a significant number of trapped owners become entrenched, it's mighty hard to change that if % rate have little room to move down. And given what we've got, and have had for the last 15 years, that room for movement is very limited. Inflation is telling us so.

Thats just the greedy ignoring reality, and the banks avoiding a 1987 like reality check. Potential buyers continue to wait, or immigrate.

End of the day NZ is a tiny dot in the ocean of global money. If something like another Lehmans happens, and there's is plenty of noise about bank problems out there, then we will be carried along with the impact and fallout.

We are not special, we are riding in the last wagon of a global train that has lot of derailment opportunities ahead.

Unfortunately for the leveraged, the losses whilst sounding small so far….are actually multiplied by that leverage.

So a fall of 2% in sales prices is actually a fall in equity of the 2% times 5,6,7,8 or 9

Aren’t leveraged interest only investors losing equity at a rate of 10,12,14,16,18% ??

Twelve months of this and many will be out the back door

I get a sense this is going to break like a tsunami on our economy……everyone’s watching the tide recede but don’t realise what’s coming.

by Zachary Smith | 11th Mar 23, 11:21am 1678486881 - You will be waiting a very long time, possibly forever.

Zachary, absent the capital gains, the risks matter more now and will more than likely be reflected in yields. If it didn't, sales volumes would already be rising as the investor tide would be turning. This would give the impression there existed a floor to this rout. With 6% gross yields on offer from banks with little effort, suddenly vandalism, missed rent payments, doubling of insurance premiums, soaring rates and diminished tax deductions really do matter.

Do the sums.

We will just have to wait and see.

Good answer. I think the longer deposit rates stay at these levels the more likely this scenario of higher rental yields will play out.

Note: the above graph does not represent all auctions!... Only a few select auctions.

Take the 3 in northland . That must be one agency's total! Because yesterday I watched 5x auctioned at RW bream bay... And again they were all passed in.

Smoke and mirrors.... Defined data set of info being put up here.💥💥💥

...and I noticed it represents A O T O Rower. Not New Zealand .. Woke!

A lot of these comments around housing sound like "it's different this time". I have been round long enough to know it is not different. It is the same as previous corrections. It will be followed by a return to growth.

The boom always lasts longer and the rebound comes sooner than you think.

Its a concern we have yet to witness the fear and reset in equal proportion to the epic greed. Selling houses to each other at ever increasing prices is not a sustainable pathway to economic prosperity. In 2-3 years time, lets see what it all looks like in the rear vision mirror. What label will society then attach to it? I think regular flat lining price periods are healthy and are necessary to reign in peoples unrealistic expectations. Now that the price of debt has gone skyward, our "prosperity" is now highly vulnerable.

Ireland took 15 years for their house prices to recover to their 2007 peak. But that couldn't happen here.

We sold our property in Thornlands, Brisbane (Upper middle class suburb) in early 2008 for 557K, it sold in 2018 for 568K (same condition). When we sold the market was strong, but it was not bubbly.

Are you saying something about the new owners or about the market, its not clear

Just that the property we sold in a nice suburb in Brisbane, did not appreciate any amount of note over a 10 year period. Even though the Australian economy was doing well, and interest rates had reduced. The property was in the same condition. Single level brick and tile, in a nice quiet cul-de-sac.

Sure there will likely be a return to growth. But how much growth? My view is the next growth phase will be subdued.

Retail Interest rates will need to return to circa 3-4% to generate a significant lift in prices again. This return to 3-4% could happen in two ways:

1. The economy really really tanks this year and inflation subsided. The OCR is cut back to circa 1.5-2% by mid 2024.

2. We have economic weakness for a couple of years. Inflation gradually subsides. We get back to an OCR of circa 2% by late 2025

In Scenario 1 there is a LOT of collateral damage. Even though the OCR comes back down again quite quickly, high unemployment, bankruptcy etc etc negates anything other than a slight tick up in prices from late 2024.

In Scenario 2, the economic damage is much less but there’s still prolonged malaise. Prices start slightly ticking up in late 2024 as well - interest rates aren’t as low as scenario 1, but the economy and employment is somewhat more robust

There are more scenarios but I think these are the most likely ones.

3. Inflation is persistent, economy is weakish but not as weak as scenario 2. Inflation gradually subsides, OCR returns to circa 3.5 by circa mid 2024, prices start ticking up late winter / early spring 2024.

In all three scenarios prices aren’t ticking up until late 2024.

Here’s scenario 4, quite unlikely:

4. Although economy is weakish in 2023, it starts a moderate rebound in late 2023. National has won the election and property investors are emboldened. High interest rates mean there is still a strong handbrake on house price growth, however changed sentiment sees a slight tick up in prices in the summer of ‘23/24

I welcome anyone to have a go at refuting any of the above, with reasoned argument, rather than trolling spruikerism (or trolling DGMism)

https://www.newshub.co.nz/home/money/2023/03/economist-cameron-bagrie-r…

Do you notice how proper economists like Bagrie never put figures or dates on any of their predictions? They admit no one knows.

Unlike Tony the Comb who told the sheeple middle of last year that there was only another 5% to the bottom.

I’m in the Bagrie camp - the falls don’t stop until investors get back in the market - and why would you buy a rental for a 1-3% net yield when you can get more than that on TD - and passive.

HM, my only scenario is 2024 will be worse than 2023 - I think we’re at the end of the beginning

I think there is such a lag - it’s taken 12 months for most to accept the NZ property market is not bulletproof and prices can fall.

The levee has broken. That’s a game changer - so anything can happen from here.

Thanks for your views

I have doubts OCR will go back that low within next 2 decades... Surely everyone will point out that look what damage it caused so recently. 20 years most people will forget OCR and blame the virus

Surely everyone will point out that look what damage it caused so recently.

Probably not, they'll look at 15 years without any significant recession and concur the 2% inflation policy is the golden rule.

Whats happening recently won't be viewed as derivative of monetary policy.

Here's another scenario 3% is the new 2% inflation.

-previous 20 years in NZ, nil goods inflation (1/3 of CPI), so only had services inflation (2/3 of CPI) adding to inflation. So with goods inflation now present, we immediately go to 3% CPI as opposed to 2% CPI. Upside services inflation risk with all the pay parity, and me too pay claims.

So 3% CPI, 1% margin for term deposits above CPI, 1% for bad debts, 1% for bank margin. Base mortgage rate is 6%. 2021 property prices are not exceeded for 10 years plus.

Thanks.

my base projection is peak 2021 values are not exceeded for another 6-7 years.

HouseMouse, the very fact we are talking various plausible scenarios shows, that as a debt ridden nation, we have limited ability to mitigate the economic pain. We have little control over the fallout resulting from local and foreign policy missteps. It seems like we are now between a rock and a hard place forced to borrow and tax just to repair our damaged infrastructure.

We have little control over the fallout resulting from local and foreign policy missteps.

Haha, yeah, it could all have been avoided with some clairvoyant decision making skills.

We can borrow and tax for that damaged infrastructure, sell down some assets, or liquidate sovereign wealth funds. Each scenario has ups and downs, and unforseen bills always suck.

I actually think there are a number of factors that make this time quite different, in some ways at least.

Yes, for example, some things aren't cycles, like progressively burning the most cheaply extracted oil. Then it's gone...

This is what I have been saying for many months, half completed developments abandoned. Just like the place next to my parents’ house in the mid to late 1970s:

https://www.nzherald.co.nz/nz/eyesore-half-finished-auckland-apartment-…

She said it is not easy in the New Zealand economy at the moment for people to get projects off the ground.

Reporting negative news only contributed to lowering confidence and making it harder, she said.

Keep up the good work IT GUY

Agree Comrade HW2, Lets just report the good news..... I see that one of the big stable coins had about 10% of their cash with SVB, not sure why they where not holding this in short dated treasuries themselves?????

It all depends on perspective. Yours is good news for those who see it as such. Comrades know how to make money on almost any market

good read about Otara being effectivly down 30% on the most trusted channel in NZ ONEROOF

Demise of the Otara millionaires club: ‘Owners are kicking themselves’

House prices in South Auckland suburb are on the slide after unbelievable peak.

12 Mar 2023

Share

Read more:

Architect gives his Grey Lynn villa an uber renovation

Otara's shopping strip. The suburb has seen a slide in property values after they rocketed during the post-Covid boom. Photo / Getty Images

Otara properties that were fetching dizzying $1million-plus prices at the height of the market have plunged to around $700,000 with some owners kicking themselves they didn’t sell earlier.

The average property value in Otara has tumbled more than 20% ($193,000) in the last 12 months to $751,000, OneRoof-Valocity property figures show.

Ray White salesperson Adrian Chhour recalls bringing an auction for a property on Clayton Avenue in Otara forward one day to beat an OCR announcement in December 2021.

The property sold to a developer for a “crazy” $1.1m and the next day properties in Manurewa that would have fetched between $1.1m and $1.3m were only reaching $800,000 and $900,000 at auction. “Literally the next day properties changed overnight,” Chhour said. “We beat the timing of it by just one day.”

Start your property search

Find your dream home today.

ADVERTISEMENT

In the last year property prices have fallen around the country and Otara has been no exception with Chhour adding houses that would have easily got $1m two years ago would now only sell for about $700,000.

“Most of my clients who are still in Otara are kind of kicking themselves that they didn’t sell in the peak of the market.”

Read more:

- Auckland for under $1m: Number of affordable suburbs more than doubles

- South Auckland home suffers near-$1m hit as resale losses grow

- $1 fire-sale home in South Auckland ends up selling for $661,000

He knows of a property owner who purchased a property when prices were high with the intention of doing it up and flipping it, but who would, in the current market, struggle to get what he paid for it even after the renovations.

But there are traders who are now back in the market looking to snap up some bargains from investors who were selling properties they have owned for more than five years due to the rising costs, Harcourts agent Alex Dunn said.

“Property traders pick them up at a pretty good price and they don’t need too much work to them as they’ve got solid bones so they can do a quick renovation on them and get them back to the market for first-home buyers.”

A home on Antrim Crescent, in Otara, Auckland, has just sold for $735,000 after a full renovation. Photo / Supplied

They would then test the market with the renovated property to see if they could sell it and if not they would rent it out usually getting a good income from it, he said.

Dunn sold a three-bedroom home with a double garage on Antrim Crescent in Otara for $570,000 in January which he estimated would have fetched the early $900,000s at the peak of the market.

“I know there’s one across the road that they are wanting big dollars for, but it’s just sitting there.”

Not everyone is prepared to meet the market, he said.

A property at 30 Franklyne Road is also being marketed as “a development opportunity not to be missed” and already has resource and building consent for five five-bedroom houses on the 986sqm site.

The property has an asking price of $1.55m and last changed hands in September 2021 for $1.585m after the auction attracted interest from eight developers.

Other listings such as a house at 1 Luke Place and another at 50 Cobham Crescent are appealing to developers by highlighting the fact that the property is zoned for terraced housing and apartments or mixed housing urban zoning.

Ray White Manurewa salesperson Tom McCartney said the price drops in Otara are in line with what's happening in the rest of the South Auckland market and it's now the owner-occupiers who are probably likely to pay more than the developers.

And while the prices have pulled back, a standard three-bedroom house on a 600 to 700sqm section that would have sold for $550,000 in early 2020 is still selling for around $700,000.

“So over a three-year period and you took out the big spike in between and you've gone from $550,000 to $700,000 then you would probably be quite happy with that return, but it's just the fact that in between a lot of them have gone up to $900,000 and a $1m that people feel potentially like they've lost money and missed out when there was just a short period of time in the market when it went crazy for a bit.”

Renovated properties or those in tidy condition are attracting first-home buyers or owner-occupiers looking to upsize from a smaller unit, while do-ups were being bought by investors or renovators who then spent time and money bringing the house up to a liveable condition and to the healthy homes standards.

Just this week McCartney sold a fully-renovated four-bedroom property at another Antrim Crescent address for $735,000. It last changed hands in December 2022 for $575,000.

Another property with a large home and smaller dwelling at 34 Waipapa Crescent is being auctioned by his agency later this month and would suit investors due to the property offering double rent or extended families.

It's abit rediculous copying & pasting an article in its entirety...

It's abit rediculous commenting on the messager not the message. But I expect nothing more when the MESSAGE SAYS SOUTH AUCKLAND IS DOWN 30%

I'm surprised it hasn't been deleted TBH, you even included "Advertise with One Roof" with hyperlinks lol.

Everyone knows why Otara has dropped substantially in value...it's a sh*hole.

IT GUY is horsing around and making a foal of us. He could even be aiming to stirrup some trouble, rein him in editor please

The Ray White comment is interesting but not surprising: "...it's now the owner-occupiers who are probably likely to pay more than the developers."

Really illustrates the change in motivation of market participants, with more of the sales going to people willing to pay a premium for somewhere to live, outbidding the people who do it as a business and can see it is not profitable.

The owner occupier bid is clearly 30% lower than developer bids where, even then IMHO time will show that these levels are still TOO high

A home on Antrim Crescent, in Otara, Auckland, has just sold for $735,000 after a full renovation.

Paid $710k in 2018. RV of $1m in 2021. 😭

https://homes.co.nz/address/auckland/otara/36-antrim-crescent/BEWKp

Amateur developers would have been battling each other at auctions for that 18 months ago.

my how times have changed…

A number of houses at the Auckland auctions this week appeared to get quite good bids yet were passed in. I am keeping note of these ones and will check further down the track whether or not that was a good decision. It's curious to get a bid for the QV estimate and around RV and well above what the vendor paid and yet not accept that in the current environment. One passed in property's bid was a few thousand under what the vendor paid only a year ago. A bit painful but fully to be expected surely.

Authored by Raghuram Rajan, op-ed via The Financial Times,

In his testimony to Congress earlier this week, Federal Reserve chair Jay Powell indicated “the ultimate level of interest rates is likely to be higher than previously anticipated” and “restoring price stability will probably require that we maintain a restrictive stance for some time”.

This was the tough Fed on display, and markets accordingly tanked.

Yet a few weeks earlier, Powell had set the financial markets off to the races when he said, “We can now say, for the first time, the disinflationary process has started.” Financial markets, used to years of easy money, celebrate at the slightest indication that the Fed will soften policy, making its task harder. Yet they are not the only market that is not currently co-operating.

Labour markets have, if anything, become even tighter, despite the Fed raising interest rates by 450 basis points since last March, and Friday’s strong jobs numbers did not alleviate concerns. While goods production is slowing after the pandemic increased consumption significantly, services, which are more labour-intensive, are now picking up strongly. Workers are hard to find, especially when it comes to hospitality and leisure. One reason is that the labour force is missing 3.5mn workers relative to pre-Covid projections. Older workers understandably quit during the pandemic, and many did not return. Retirements still continue at an accelerated pace. And tragically, as Powell pointed out, Covid-19 also ended the lives of half a million workers in the US, while a slower rate of immigration has led to about a million fewer workers than expected.

In addition, given the difficult nature of jobs in leisure and hospitality, workers have sought opportunities elsewhere in the economy. And perhaps as importantly, companies have been holding on to their staff precisely because hiring has been so hard. Until they are confident that the economy will slow down and they will not need these workers, and also perhaps until they see enough unemployment around them to signal that hiring will not be difficult in the future, labour hoarding may continue.

Other markets are also treading water. For instance, US house sales have slowed considerably, but property prices have generally held up, probably because there is not much supply entering the market. With mortgage rates having risen by so much over the past year, a homeowner with a 30-year mortgage at 4 per cent will have to shell out much more in monthly payments if she upgrades to a slightly better house with a new mortgage at 7 per cent. Because she cannot afford to buy, she does not sell. And because this is limiting the supply of homes on the market, there is only modest downward pressure on prices.

Finally, inflation has been trending down because pandemic-induced supply chain disruptions and war-induced commodity supply disruptions are now being sorted out.

Beliefs in a painless “immaculate disinflation” and soft landing lead to a self-reinforcing equilibrium, in which few believe the Fed will have to do much more. As a result workers are not being laid off, financial asset prices and housing are holding up, and households have the jobs and wealth to keep spending. But without some slack in the labour market, the Fed cannot feel comfortable pausing its efforts.

To get the job done, therefore, the Fed has to force markets to abandon their belief that disinflation will involve only mild job losses. Indeed a recent study by Stephen Cecchetti and others suggests that every disinflation since the 1950s has involved a significant rise in unemployment.

There are dangers in the Fed taking a soft landing with mild job losses off the menu of possible outcomes.

The first, evidenced by the questioning Powell underwent during his Congressional testimony, is that politicians will be irate if the Fed torpedoes a recovery they have just bought with trillions of dollars in fiscal spending. The central bank is not immune from Congressional wrath.

Second, the benign equilibrium may turn into a vicious one. The markets could have their Wile E. Coyote moment. Lay-offs may spur more lay-offs now that businesses are confident they can hire back if necessary. In turn, laid-off employees may be forced to sell their houses, depressing property prices and reducing household wealth. Unemployment and lower wealth may hurt household spending, which will in turn depress corporate profits. That will lead to more lay-offs, falling financial markets and financial sector stress, and yet more muted spending . . . We may end up with a deeper recession than currently anticipated because it is hard to get just a little unemployment.

Of course, the Fed could then revive the economy by cutting rates, but it will need to be wary of doing so until it sees enough slack build up in the labour market. If it turns too fast, markets will celebrate and the job will be left unfinished. But if it waits until there is sufficient slack, lay-offs could develop a momentum of their own.

The temptation then is for the Fed to be more ambiguous, keep a soft landing on the menu and pray for an immaculate disinflation.

If so, the Cecchetti study warns that the eventual unemployment needed to rein in inflation could be much higher.

The Fed’s only realistic options may be a hard landing and a harder landing. It may be time for it to choose.

Beliefs in a painless “immaculate disinflation” and soft landing lead to a self-reinforcing equilibrium, in which few believe the Fed will have to do much more. As a result workers are not being laid off, financial asset prices and housing are holding up, and households have the jobs and wealth to keep spending. But without some slack in the labour market, the Fed cannot feel comfortable pausing its efforts.

The temptation then is for the Fed to be more ambiguous, keep a soft landing on the menu and pray for an immaculate disinflation.

This seems to reflect the NZ view on the economy as well. Jobs still stable, money still flowing, hands off thought process and "inflation will come back down" while not many make changes to their spending habits around us. Still pondering how many more mainstream articles it will take, andmoretgages refixed at higher rates before we see any meaningful change.

Bit disappointed that a spruiker hasn’t commented on why my scenarios are wrong, and why a bullish scenario is right.

come on HW2, TTP or Nifty, have a go!

Interesting article in OneRoof about how "bargains can still be found in the wealthy Auckland suburb". A house with an RV of 2350K and a QV valuation of 1990K sold for "a super low" 1290K.

Yet if we look at the sales history we see that the house was bought in 2014 for 850K which means it went up about 440K in nine years which is about 4K a month.

This is still a fabulous return (5%) and way beyond what it should have gone up by, especially when you consider that you get to live in or rent the house out too and no tax on the capital gain.

be interesting to watch the future value of that house

Why are Wellington auctions excluded from your stats?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.