Floating mortgages surged in popularity in November, according to latest Reserve Bank monthly figures.

Of the $7.556 billion worth of new mortgages taken out in November, some $3.579 billion was on floating rates. That's 47.4% of the total on floating - and its very much the highest percentage on floating since this set of RBNZ figures began being published.

The RBNZ's C71 data series, which was introduced only fairly recently and has data going back to 2021, differs from other monthly series in that it shows mortgage figures for after the mortgage has been uplifted (while other series highlight mortgage figures for when the mortgage has been committed to). (The RBNZ summary of the latest data is here.)

The C71 data therefore shows the flow of the money and into what rates as and when it happens.

And the latest figures, for November, show that the trend of going for shorter and shorter mortgage terms, very visible since the start of 2024, has now reached its ultimate point, with people starting to move away from fixed terms altogether in favour of - for now - floating rates.

The Reserve Bank started cutting the Official Cash Rate in August 2024 and this has fallen from 5.5% to 4.25%, with another 50 basis point cut widely expected next month. Mortgage rate falls actually started before the OCR cuts.

Clearly, mortgage holders are looking for further falls - hence the sudden surge in interest for floating rates, which according to separate RBNZ stats on average monthly mortgage rates, are more than 75 basis points higher than the shorter term fixed rates.

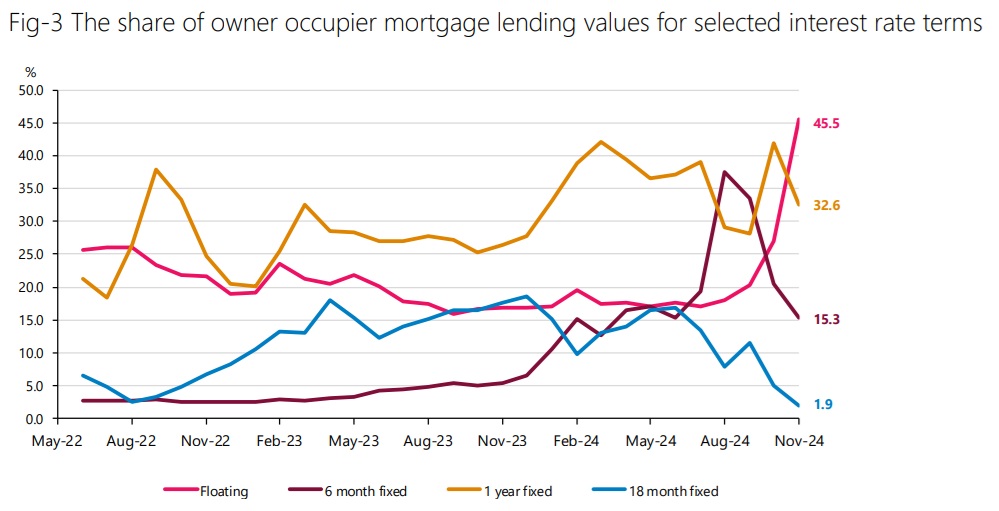

Of the $5.319 billion of mortgage money taken out by owner-occupiers in November, $2.421 billion was on floating. That's 45.5% of the total, up from 27% in October, and 20.3% in September.

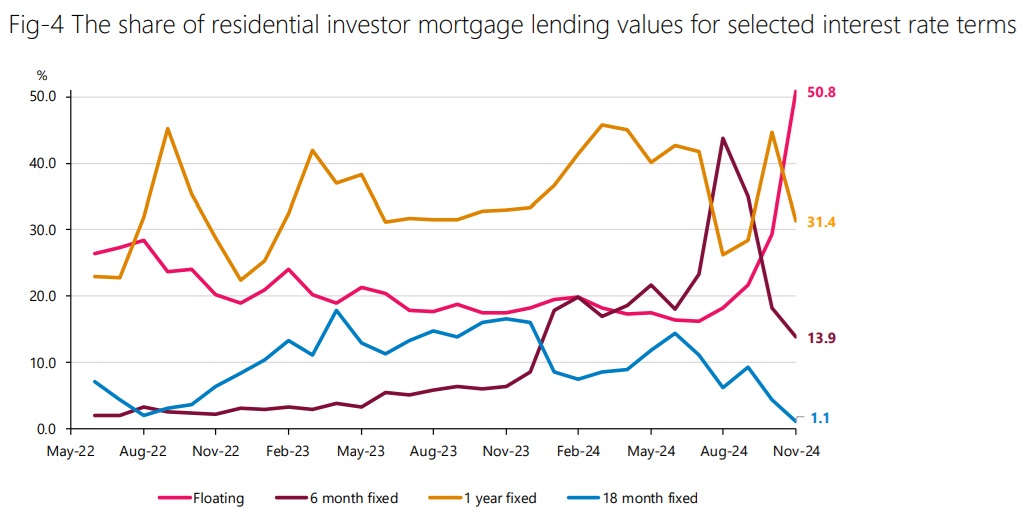

The investors have gone even more the floating way, with over half the money borrowed by investors in November on floating rates.

Floating mortgage rates became very popular for a time after the Global Financial Crisis, but in the past 10 years or so the preference has been very much for fixed rates. So, how long the new floating fashion will last for will be interesting to see.

The RBNZ reports that for the owner occupiers, the share of loans on floating and short-term fixed rates either for a year or of shorter duration represented 93.4% of new lending in November.

In November 99.0% of investor new lending was on floating or at fixed rates of two years or shorter duration.

33 Comments

People are incredibly optimistic when they probably shouldn't be.

swap rates and OCR forecasts are all on a downward trend.

Aren't the longer dated swaps going up now?

hard to say, 5 years + yeah, people don't float their mortgage rates based of long term expectations though.

5+ year swaps are irrelevant to residential mortgage rates. 1 & 2 year swaps are still heading down.

Given there is such a premium for floating in NZ, wouldn't most of these people probably been better off on a 6mth fixed?

yea i do wonder the reasoning behind it, especially the large percentage of people doing it.

The obvious thing to me is the expectation of a decrease soon? or being able to react to the change when it happens.

possibly waiting for the CPI figures, seems a bit long to wait for the OCR, the current OCR prediction for feb wouldn't change interest rates enough to float for 4months?

a low inflation figure on the other hand could change things quite a bit.

This is precisely why I favour 6 months rate. Because of the high uncertainty in NZ and international financial matters, floating is best, so one can react quickly to the changing situation. But it's too expensive. The 6 months rates are the next best thing.

6 month is expensive too though. 0.4% difference between 6 month and a year when I recently fixed. You need a big decrease in that 6 months to justify it.

Its probably all the people planning to sell up in 2025.

good point. i did notice a big decrease in listing leading to the end of 2024, i assumed a whole lot would come back in early 2025.

Those wanting to head to left wing Aus now that we have right wing NZ?

Australian Labor is not an extreme Left wing Govt, like the last NZ Labour Govt was. And its basically dead in the water at the moment with it looking like the Coalition will get back in come May. Its increasingly looking like a global shift to the Right post covid. The true test will come in 2026 when we see if even the Victorian's are sick to death of them.

Spot on. The world has finally seen that the left emperor/empress has no clothes.

True, their Jacinta has been a complete disaster for Victoria. Almost as bad as our Jacinda.

You have to be out of your mind to think that the last labour government were extreme left. Besides the identity politics bullshit, what social policies did they actually implement that were extremely left? No CGT, no land tax, a sensible removal of tax deductibility for the biggest beneficiaries of this country (landlords). They could and should have done a lot more.

Reckon it's a combination of that plus expectations that the RBNZ would cut 0.5% in February, which until the last few weeks or so were looking reasonably sound...

A very large move towards floating rates means many borrowers expect lower rates soon.

people following mortgage broker advise.

Yes, unfortunately.

I use a broker because I’m too busy/can’t be bothered liaising with a bank and going through their stupid disclaimers every single time. The broker cuts that out and I make them work for their commission because I don’t accept poor advice. I am very firm and very clear about my intentions making them effectively a secretary to turn my intentions into actions.

Precisely why I use one.

Yeah. In November.

In my own case, we fixed some for a year, and left 25% on a floating offset for cashflow reasons.

Nothing wrong with the floating but it could be crunch time next month and time to fix.

"When the facts change we change" could very well be Orr's words, in the next month or two.

Debt prices are rocketing around the world and while we are one, we cannot be an economic island V the mighty USD.

Those floating and on short fixes may very well get a good ole roggering in the financial meanstreets.

Offshore investors will expect premium returns for money risked into the NZ Ponzinomic economy.

I can easily handle 7 to 10% cost of funds, how many leveraged Kiwi would be in the dogs jaws by it? Most would be!

We all live in interesting times.

People still have plenty of time to fix for 2 years and kick that can down the road.

Don't why they wouldn't take the cheaper 6 month fixed option if they're only on floating for the purposes of anticipating further rate cuts.

Could be offset? We have about 1/4 of our mortgage in an offset and this gets more every year (as fixed terms expire) as our rate of savings gives us an effective interest rate of 0%. So it basically doesn’t matter what the floating rate is.

A lot can happen in 6 days, let alone 6 months in a volatile world....perhaps a doubling/halving of interest rates (or more)....it is not without precedent.

The NZ (Aussie banks) are so sticky though. In UK when the BoE reduces the cash rate , all bank mortgage floating rates come down that day. In NZ they just leave it. For example, last time i looked in November the margin between fixed and floating was at a two year high.

Going floating in NZ for more than a few days/weeks is dumb.

But I expect 'investors' are hunky dory with this as they see interest as an 'tax deductible expense' (when it should be seen as a cost !!!)

Banks in NZ never pass on OCR cuts quickly. (The OCR is good for forcing rates up quickly, or holding a floor under them, but down quickly? La la land.)

Why not 6 months? Fix for 6 months and be patient as our thoroughly uncompetitive banks adjust down as and when banks consider their profits are satisfactory.

my 1yr fixed 7.29% is coming off next week ..after I get some more equity out ...I'll be taking the 5.49% 2yr term .. great deal .., very foolish to expect COVID rates again that was a major reason why home prices spiked .. inflation is coming thanks to mad-dog trump

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.