Big numbers of owner-occupier new borrowers are opting to go for floating rates, the latest Reserve Bank monthly figures show.

For those opting to fix, there's been a huge surge to the one-year terms.

The RBNZ's C71 data series, which was introduced only fairly recently and has data going back to 2021, differs from other monthly series in that it shows mortgage figures for after the mortgage has been uplifted (while other series highlight mortgage figures for when the mortgage has been committed to). (The RBNZ summary of the latest data is here.)

The C71 data therefore shows the flow of the money and into what rates as and when it happens.

And the latest figures, for October, shine the spotlight on a new trend that was also visible in the recently released S33 data for October that highlighted the total mortgage stock by times to next repricing.

The data is showing that there's a new-found popularity for floating mortgages.

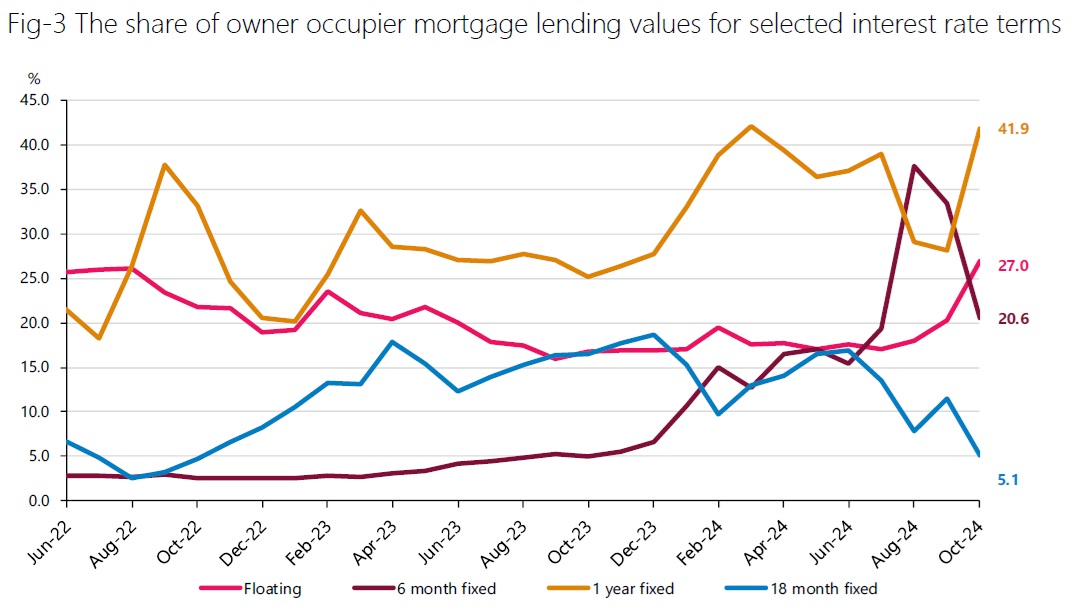

According to the C71 data showing new mortgages taken out in October, some 27% (nearly $1.5 billion) of the $5.335 billion for owner-occupiers was in floating.

That was a very sharp rise up from just 20.3% in September and the 27% figure is the second highest percentage for floating since the start of the data in April 2021 and it was only bettered by the March 2022 figure of nearly 28%.

Since pretty much the start of this year borrowers have been going shorter and shorter with their terms in anticipation of Official Cash Rate (OCR) cuts from the RBNZ - which subsequently began in August.

This trend among the borrowers has seen the previously unfashionable six-month term rise to prominence, peaking at a 37.6% share of new owner-occupier mortgage money in August. The share fell to 33.4% in September and then to 20.6% in October.

As the six-month term has declined in popularity, then so the more traditionally-favoured one-year term has stormed back to prominence. In October the one-year term took 41.9% of the owner-occupier mortgage money share, up from 28.2% in September.

The $2.234 billion worth of owner-occupier mortgage money put on one-year terms in October was the highest monthly tally for this term since July 2021.

Some 89.4% of the owner-occupier new mortgage money in October was either floating or for a one-year or shorter fixed term duration.

At times the two-year terms have been the most popular but they are currently right out of favour. Just 3.5% of the owner-occupier mortgage money was put on a two-year term in October. In October 2023 some 24.3% of the mortgage money was on two-year terms.

The trends are very much the same for the investors.

In October 29.3% of investor new mortgage money was floating, while 44.6% was fixed for one year.

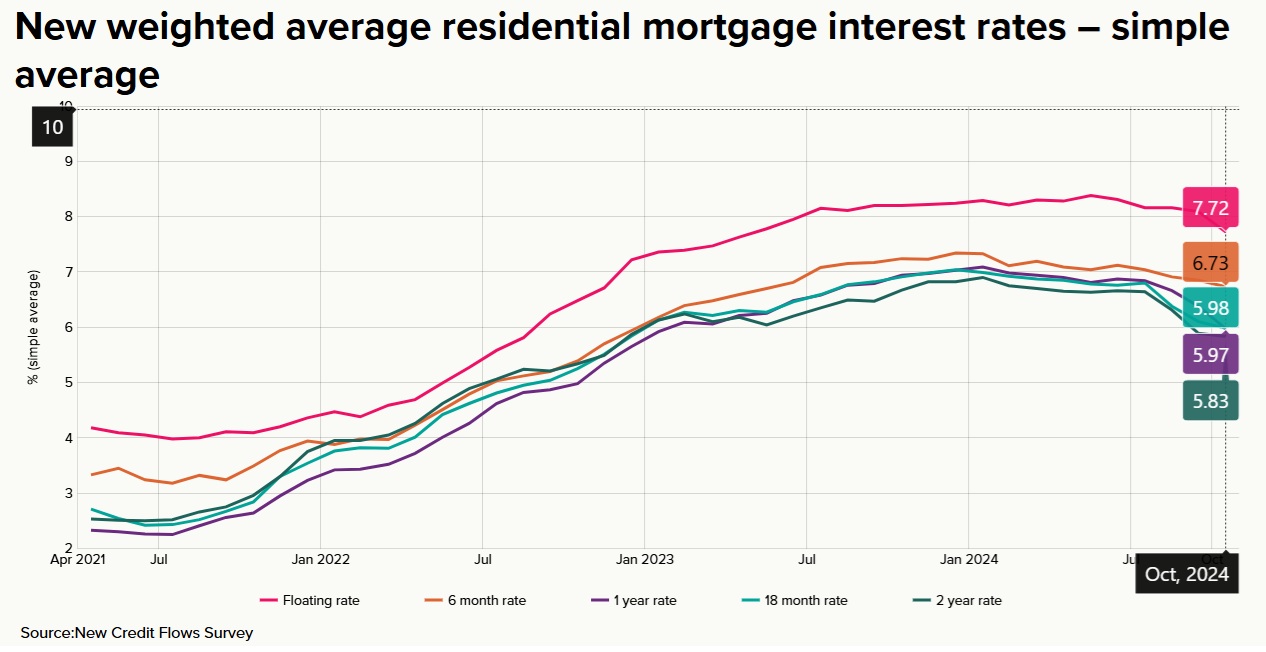

Separately, a new RBNZ monthly data series highlights the actual weighted averages charged by the banks on new lending. The RBNZ says the purpose of this data collection "is to better understand the provision and pricing of credit in the economy".

The data shows that the biggest drop in October was on one year rates, with a 41 basis-point fall to 5.97%. Not far behind were the floating rates, with a 37 bps fall. But the average rate on floating, at 7.72% was still much higher than the fixed rates.

17 Comments

It’s not going to be helping spending with such a significant amount of people on floating.

My floating rate goes to 6.95% with Westpac next week so it’s still rather painful (mentally, not financially).

Rates are going to have to cut in an attempt to get the whole curve down.

Not sure why, as there's a big gap between floating and the 6-mth rate. Perhaps there's a tidal wave of houses about to go on the market?

I'm curious how you come to that conclusion?

It's not a conclusion, just a guess. To me, there are two main reasons for keeping your mortgage on a floating rate. 1) You think that the OCR is about to plummet; or 2) You're thinking about selling.

So the alternative perhaps is a tidal wave of OCR cuts?

Yes.

Just done ours (late October) at 5.79% for one year. Interest rates will probably drift lower over that period, at least I hope so. It's a two-edged sword though, rates are only reducing because they've strangled the economy. You love them then you hate them. Or should that be the other way round?

I am starting to get more nervous that we aren't going to see any rates drop below 5% in the next year or so. Is this roughly as low as it's going to get?

I am pretty confident they will get to less than 5%. The economy is dire, and the CPI is under control.

OCR to 3% or less by mid winter.

OCR at 3% with a fat 2% bank margin is 5%. So either margin has to drop or the OCR has to go lower than 3%. Will it happen? Maybe, but not by much I think if it does

Except the fixed rates are not generally OCR + Margin. It may be that for floating to a degree, so then a 5% floating rate?

The average floating rate is more like 3% above the OCR at the moment, so 6% floating at 3% OCR? David C seems to think that swaps have bottomed out for now, so they won't help much going forward

They will drop to under 5% without doubt.

There is no way they can have people not buying property as the housing market us the biggest industry in the country.

If interest rates stay as high and the rent returns are not attractive to investor’s then rents will increase and there will be even less houses built.

This flows on to tax take being less, people unemployed and business going go the wall.

Very interesting times and the Banks do not want prices stagnating.

Probably down to 4.99% but I can't see them going much lower than this

Goddamn your housenomic reckons are a stretch.

Survive till '25?

More like wheatbix till '26.

Except for bank executives of course.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.