Our term deposit rate tables are changing.

With the Treasury and the Reserve Bank (RBNZ) working to introduce a bank guarantee for depositors, the Deposit Compensation Scheme (DCS), which will become effective some time in mid-2025, we need to prepare for that.

The DCS will cover depositors up to $100,000 per institution for any loss should an institution fail.

This cover is for more than banks.

The RBNZ regulates non-bank deposit takers (NBDTs) too, and those regulated institutions will also be covered. Apparently the RBNZ now has the power of on-site supervision for the purposes of assessing financial stability.

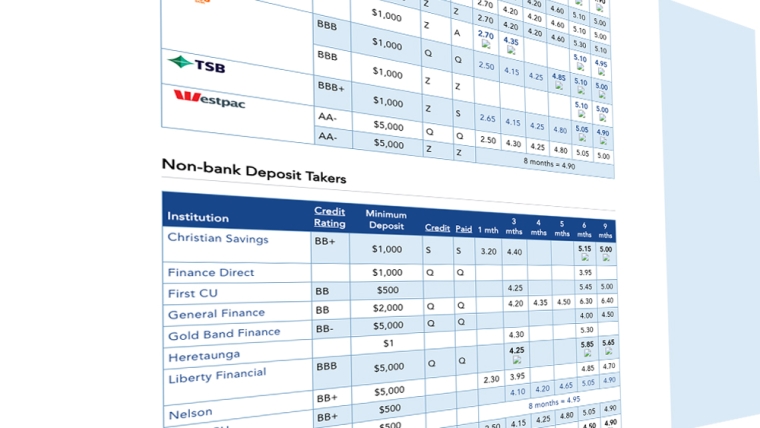

As a consequence, we have adjusted our savings and term deposit tables to identify the non-bank institutions to be covered by the DCS.

The risks to depositors will dramatically fall to be similar to banks when the DCS becomes effective. And that is because the taxpayer is making a guarantee promise.

Covered institutions (including banks) will pay a fee for the right to promote this protection to potential savers. That fee is to be "risk based" so will likely be higher for smaller institutions with consequent liquidity variations. And in turn, that fee cost will tend to restrict what they can offer for a deposit interest rate.

Because it is now about six months until the start of the DCS coverage, savers need to know who will be included. And that is why our rate tables now show a separate section for the NBDTs.

The current institutions registered as NBDTs are:

Christian Savings

Finance Direct

First Credit Union

General Finance

Gold Band Finance

Heretaunga Building Society

Liberty Financial

Mutual Credit Finance

NBS (Nelson Building Society)

Police and Families Credit Union

UnityMoney (Unity Credit Union)

WBS (Wairarapa Building Society)

Xceda Finance

11 Comments

Thanks for your proactive approach. It will be interesting to see how the market response to the higher interest paying NBDTs plays out when they have a Govt guarantee to $100k.

When introduced, I assume that the guarantee will cover existing term deposits not just ones taken out from that date. If so would it be a plan to, right now, take out a 5 year TD at 7% instead of 4.4% from a bank?

I haven't seen the legislation/regulation however I'd question that assumption: the offered rates will drop when the guarantee comes in.

"Covered institutions (including banks) will pay a fee for the right to promote this protection to potential savers. That fee is to be "risk based" so will likely be higher for smaller institutions with consequent liquidity variations. And in turn, that fee cost will tend to restrict what they can offer for a deposit interest rate."

Unless they fail in the next 6 months. Thus the 6-7%

I think you need a page for on-call transactional accounts. The banks are making it difficult to earn anything off everyday spending balances. It's easy if you have a mortgage hooked up to eftpos/visa but quite difficult for if you don't.

For all the complaints about fees, I wonder whether one should be able to opt to pay a transaction fee rather than forego interest? Those who have lesser transactions (eg put most things on cc and pay at end of month) are effectively subsidising those who do multiple withdrawals incl at ATMs. ?

Is this fee going to an insurance company who will absorb the loses or is the money for any loss coming from the government which effectively we pay for? Are we now bailing our selves out or still bailing out the private companies? I'm confused!

No deposit guarantee scheme in the world is protected by private insurers. They won't go near these risks. All are backed up by taxpayers, including the NZ one. Which is why people like me point out the moral hazard involved. It's just another subsidy for savers with money.

“The scheme will be pre-funded by levies on deposit takers and supported by a Crown backstop."

https://www.beehive.govt.nz/release/depositor-compensation-scheme-protects-kiwis%E2%80%99-money

I agree that a Crown backstop for the scheme is effectively the taxpayers subsidising those who get some funds back. However it seems the levies collected and the Crown is also effectively subsidising the deposit taker that got in trouble. Hopefully the deposit taker is forced into liquidation or is to be sold etc rather than being allowed to continue to operate. There would also be moral hazard if the deposit taker was allowed to continue to operate.

People could instead put the money into Kiwi bonds for not much less of an interest rate and get it essentially government guaranteed. But if people weren't saving in banks then our economy would break add it is needed for our housing economy. So a small cost for tax payers. It is crazy that NZ doesn't have one when almost so other OECD countries do

In which case the tax payer should be annoyed, look at a couple of the dodgy names on that list...

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.