Debt-to-income (DTI) borrowing levels may be starting to increase again after falling substantially in the past three years, the latest quarterly release of DTI information from the Reserve Bank indicates.

But we appear to be some way off yet seeing the official DTI limits - which came into force on July 1 - having any impact. (RBNZ's summary of the latest figures is here.)

Ahead of the rules coming into effect, the RBNZ had indicated they would not be 'binding' in their initial phase. And this is very much the case. The DTI policy allows banks to lend:

- 20% of their residential loans to owner-occupiers with a DTI greater than 6 (that's a loan over six times annual income); and

- 20% of their residential loans to investors with a DTI greater than 7.

The RBNZ's now been compiling DTI information on a monthly basis - but releasing it quarterly - since 2017. We've been tracking it from the start.

Generally the trend was for DTI levels to fall in the 2017-19 period before then rising very strongly and hitting high levels in 2021.

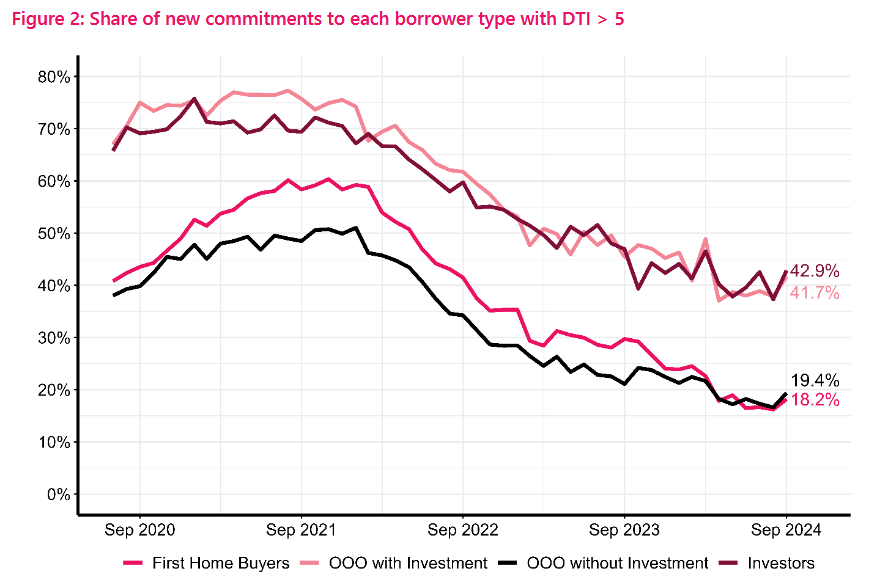

While the official limit has been initiated at a DTI of over 6 for first home buyers and other owner-occupiers (without property collateral), the RBNZ has had something of a focus on DTIs of over 5, so, we are continuing with our table showing the percentage of DTIs of over 5 times. We focus on the latest month (September) and compare that with June of this year and September in each of the past two years.

The table below shows the percentage of new mortgage money for first home buyers and other owner-occupiers that is on debt-to-income ratios of over 5 times:

| Group | Sep 24 | Jun 24 | Sep 23 | Sep 22 |

|---|---|---|---|---|

| FHBs nationwide | 18.3% | 16.5% | 29.7% | 41.4% |

| Auck FHBs | 25.5% | 26.3% | 44.2% | 57.3% |

| Non-Auck FHBs | 12.7% | 9.5% | 17.5% | 27.9% |

| Other owner/occ nationwide | 19.4% | 18.2% | 21.1% | 34.2% |

| Auck other owner/occ | 27.2% | 23.6% | 28.8% | 45.3% |

| Non-Auck other owner/occ | 13.9% | 13.9% | 15.3% | 25.2% |

As you can see and as the below graph indicates, there's been a bit of a blip up again recently following sharp falls.

So, that's all quite interesting. But if we look at where the new rules actually kick in - the DTIs of over 6 - we can see that recent new borrowing is still well below the 20% level mandated by the RBNZ.

The table below shows the percentage of new mortgage money for first home buyers and other owner-occupiers that is on debt-to-income ratios of over 6 times:

| Group | Sep 24 | Jun 24 | Sep 23 | Sep 22 |

|---|---|---|---|---|

| FHBs nationwide | 2.4% | 2.5% | 6.3% | 10.9% |

| Auck FHBs | 3.9% | 4.4% | 11.2% | 19.1% |

| Non-Auck FHBs | 1.3% | 1.1% | 2.2% | 4.0% |

| Other owner/occ nationwide | 6.5% | 7.6% | 7.8% | 15.0% |

| Auck other owner/occ | 6.5% | 8.6% | 9.4% | 20.4% |

| Non-Auck other owner/occ | 6.5% | 6.6% | 6.6% | 10.6% |

All very comfortable, for now. But this does look like we are very much at the low point of the cycle. And it will be interesting to see what develops from here.

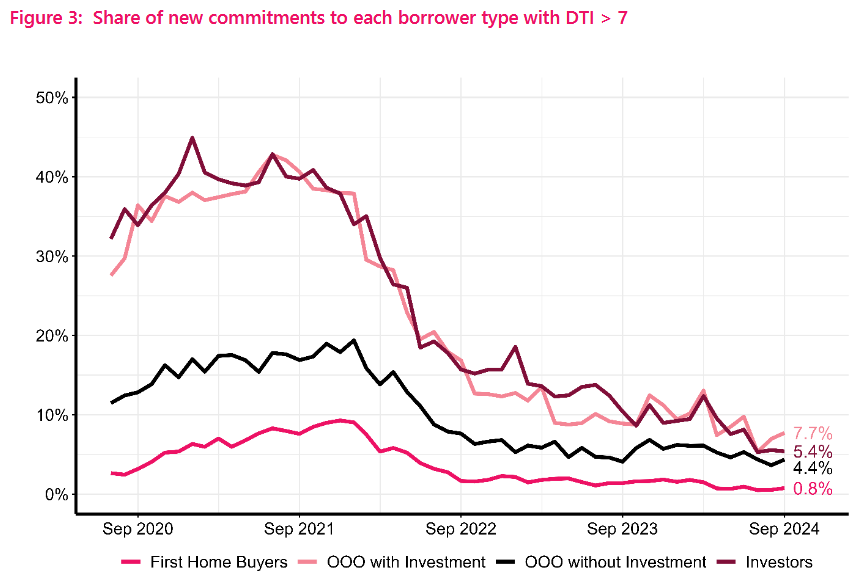

So, what of the investors? This is a grouping that has largely been on the sidelines in the past couple of years but there are now perhaps tentative signs of more interest. The figures below show there's plenty of room for investors to get more involved.

The next table shows the percentage of new mortgage money for both investors and owner occupiers that have investment collateral that is on debt-to-income ratios over seven times:

| Group | Sep 24 | Jun 24 | Sep 23 | Sep 22 |

|---|---|---|---|---|

| Investors nationwide | 5.4% | 8.1% | 10.5% | 15.8% |

| Auck investors | 4.5% | 6.5% | 12.1% | 20.3% |

| Non-Auck investors | 6.3% | 9.8% | 8.9% | 11.6% |

| Owner/occ + investment collateral nationwide | 7.7% | 9.8% | 9.1% | 16.9% |

| Auck owner/occ + investment collateral | 6.7% | 10.2% | 9.6% | 21.7% |

| Non-Auck owner/occ + investment collateral | 8.4% | 9.4% | 8.7% | 13.4% |

So, there we are. All very comfortable at the moment. For now the banks have nothing to worry about. No need to 'ration' the lending based on DTI numbers.

21 Comments

Semi pointless as should be lower. The only thing it will stop is runaway pricing like in 2021.

I was just thinking how low the numbers were of people over a DTI of 5. Plenty of those FHB must be earning decent money and have scraped together big deposits.

FHB, single income DTI is 4.6, mortgage is 43% of income at 6.91% interest rate.

The thing is, at a DTI of 5, an interest rate of 6% means 30% of your pay is on interest only - let alone the other 3-4% on principle. Factor tax into account (and don't even think about student loans) and that's a significant portion of their income on the mortgage.

To pay the debt service payments, many are taking on other sources of revenue:

1) boarders, flatmates, foreign students homestay

2) rent out spare room on Airbnb

3) rent out additional dwelling to long term tenants or on Airbnb

4) co-ownership with others - family, friends, non owner occupier buying syndicates

Many have no option but to do so.

Totally doable. I knew someone who took on 3 flatmates, basically they were paying the mortgage.

5) sale of spare kidney

The RB Act needs to be cancelled it’s holding kiwis back

Not cancelled.

But radically changed would be great thing.

Alas. It won't happen. Our MPs are too stupid. And voters? Just a tad more stupid.

We're stuffed until the shit hits the fan ... hard.

So you're saying, David, that the DTI's should be lower than the RBNZ has set them?

Yes. I wholeheartedly agree.

Our DTIs - thanks to our 'independent' Reserve Bank - are way, way higher than other comparable OECD countries.

Why? Could it be because the big banks, like they do in the US, have far too much influence?

100% agree. Threshold is to high. Let speculators use tax paid capital rather than just boosting global banking profit.

They don't need to be lower. The banks do not care as long as you are paying the mortgage. I was out of work for a long period, never even told the bank, they don't care as long as you are still paying the mortgage.

The banks are slack, so we should remove regulations on them?

Yes the RBNZ was a bit gutless setting the number, unless they plan to wait until home loans get lower and then set a more prudent number.

That feels like a sensible approach. Incremental

Current DTI settings are far too high to be useful

Only currently useful in preventing the crazy highs of the next boom at current settings.

That is exactly the point. Stopping the debt frenzy exploiting young workers from getting security of home ownership, and then relocating their future tax payments to Aussie.

Lower please.

When is HPI out?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.