I have sympathy for anybody faced right now with the need to refix their mortgage.

Trying to figure out exactly where interest rates are going is a bit of a head-exploder at the moment.

But look on the bright side - at least all the angst now is about how far rates will DROP rather than how far they will RISE.

So, relief is on the way. It's just how much relief can you get, and when? And, wow, that's a tricky one at the moment.

The situation is incredibly fluid. I'm mindful that whatever I say now could be quite out of date even by the end of a week that, amongst other things sees us getting the June quarter GDP figures and (most crucially) finding out if the US Federal Reserve is going to jump, and how far (IE will it cut, and will it cut by 25 basis points or more?)

The Fed decision will matter for a number of reasons, but not the least will be what it does for wholesale interest rate pricing and what expectations will be placed on our Reserve Bank (RBNZ).

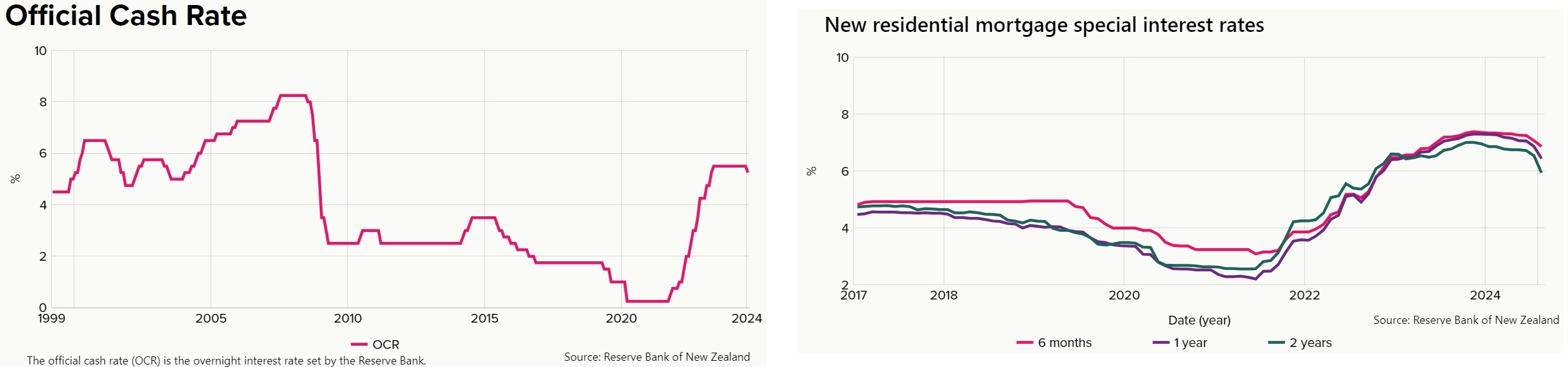

As we know the RBNZ has just commenced what we presume will be an 'easing cycle', dropping the Official Cash Rate (OCR) from its cyclical peak of 5.50% to 5.25%.

The RBNZ, which is charged with getting inflation back into a 1% to 3% range, with an explicit target of 2%, forecast in its August Monetary Policy Statement that annual inflation as per the Consumers Price Index (CPI) would drop from the June quarter figure of 3.3% to just 2.3% as per the end of the September quarter we are in. That figure, by the way, will be out on October 16, which rather inconveniently is a week after the RBNZ's next (October 9) OCR decision.

Early indications from Statistics NZ's monthly Selected Price Indexes data (covering around 45% of the CPI components) are that the headline annual inflation figure for the September quarter will indeed be well under 3%, for the first time since mid-2021.

But it's good news-bad news potentially because we are currently seeing things like weak petrol prices (well, comparatively!) - but such internationally priced items are beyond the control of the RBNZ and its monetary policy. What the RBNZ can control is the so-called non-tradeable inflation that is notionally generated domestically. And that's still 'sticky', with the annual rate being a still-elevated 5.4% as of the June quarter, while the RBNZ reckons it's only going to fall to 5.1% as of the end of the September quarter.

So, while the 'markets' might see a rapidly falling 'headline' inflation figure and may be looking at the US Fed starting to tuck into some serious rate cuts, our RBNZ is still being cautious. And if it stays cautious it might not cut as fast as people would expect or like - and maybe some of the current bank mortgage rate cuts are being overly presumptuous.

Skinny margins for the banks

On that, it is interesting to view what the differential, the gap, is between bank retail rates and the OCR. At the moment it is skinny. If we use the country's biggest bank ANZ as an example and look at its one-year and two-year 'special' fixed mortgage rates these are currently 6.35% and 5.79% respectively.

Well, that compares with an OCR of 5.25% right now, today, as opposed to what we think it might be, or would like it to be! And that means the gap between the OCR and ANZ's two-year rate is just 54 basis points, which is real skinny historically. Here's a graph of the OCR since inception and another graph showing six-month, one-year and two-year market average fixed 'special' mortgage rates since 2017. (Click on the little magnifying glass for a bigger version).

What that shows us is there tends to be a gap between the OCR and popular mortgage rates of between two and three full percentage points - and sometimes a bit more. So for the gap in one instance (IE the ANZ two-year rate) to be currently only about half a percentage point is very unusual and tells you that the banks won't want to see such a gap for long.

At the moment of course the banks are short of new mortgage business because of the lack of activity in the housing market and there's keen competition for 'switching' of existing mortgages.

But be sure, our gallant banks will want to see their lower rate crusade followed in short order by an OCR that 'falls into line' - IE comes down plenty.

So, will the OCR come down by plenty?

In its August Monetary Policy Statement (MPS) the RBNZ - and I'm taking some liberties with this because of the imprecise way the forecasts are notated - indicated the OCR could be 4.75% by the end of this year.

Cutting till it bleeds

There's two OCR reviews left this year, on October 9 and November 27. Therefore a 25 basis point reduction in each of those reviews would see the OCR at 4.75% by year-end 2024.

However, at time of writing - and due warnings must again be given about volatility - the financial markets are fully pricing in an OCR of 4.50% by the end of the year, with a better than 50-50 chance that the OCR will actually be as low as 4.25% by the end of 2024.

No wonder then that the banks are firing on all cylinders with the mortgage rate reductions.

Throwing the timeframe out a bit, the RBNZ is essentially signalling an OCR of 3.75% by the end of 2025 and 3.00% by the end of 2026.

To summarise, this suggests the RBNZ right now sees a further 50 basis points of cuts this year, another 100 bps next year and 75 bps in 2026.

The markets say no. They say at least 75 bps more of cuts this year - and very possibly 100 bps. And they see the OCR being 2.75% by the end of 2025 - which is 100 whole basis points lower than the RBNZ is forecasting.

Somebody could end up being disappointed.

Of course, as the RBNZ has been quick to try to stress in the wake of its ill-starred 'hawkish shift' in May its OCR forecasts can tend to be over-analysed, and they are based on assumptions.

In other words the RBNZ can and it will change its mind. And it most certainly has done in the past and indeed very recently after the May 'hawk attack'.

We can't be sure that the markets are 'wrong' therefore.

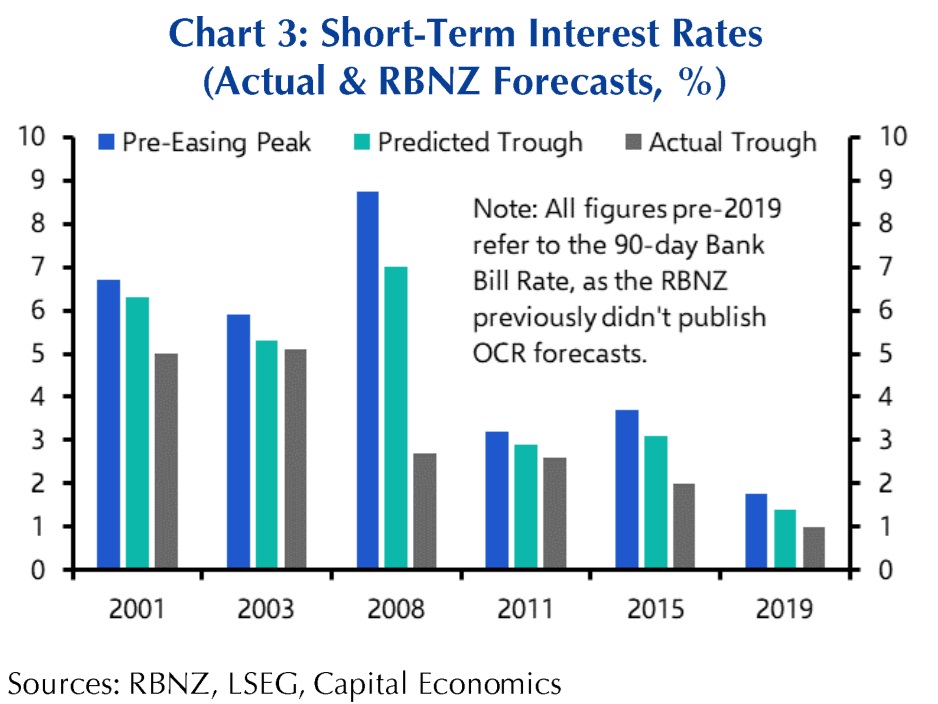

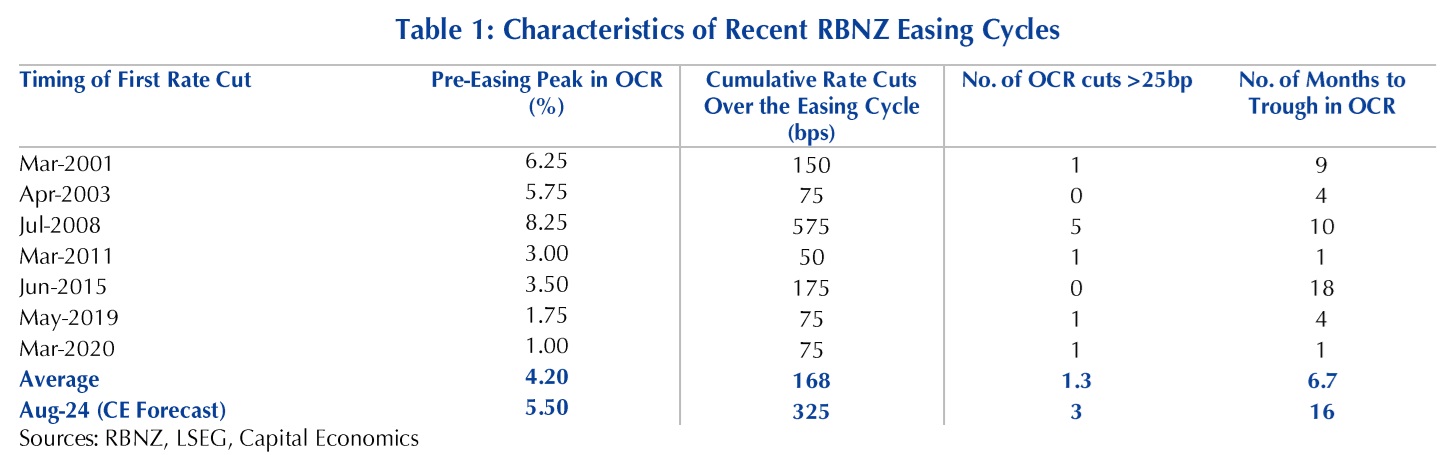

I was interested in a recent piece of, I think excellent, analysis from outside of New Zealand on the whole issue done by independent economic research firm Capital Economics.

They will cut more than we think

Having a look at what folk outside of the country can be a very good idea and gets you out of the 'NZ Inc Group Think'. And this was thought-provoking.

Abhijit Surya, Australia & New Zealand economist for Capital Economics, is predicting that the RBNZ will cut the OCR to 2.25% by the end of NEXT YEAR. Which would be a game changer if it happened.

"All told, we expect spare capacity in the economy to keep rising over the next couple of years," Surya said.

"As the incoming data make it clear that the risks to the RBNZ’s current inflation outlook are tilted to the downside, the Bank is likely to embrace a more aggressive approach to policy easing."

He also points out something else: "The Reserve Bank of New Zealand has always ended up cutting interest rates by more than it anticipated at the start of previous easing cycles. We think this time won’t be any different..."

He provides this evidence:

He also produces evidence to back up his suggestion that the RBNZ will cut faster than most other central banks, resulting in it getting the OCR to 2.25% by the end of next year.

"...The analyst consensus thinks rates will bottom out only towards end-2026, making the current easing cycle the longest one in modern history. What’s more, most analysts seem to be expecting the RBNZ to only move in 25bp increments. However, we doubt that the Bank will shy away from larger 50bp cuts, as evidenced by most of its previous easing cycles."

Now, that is just one opinion. But it is an international opinion and our rates of course will be affected by the international perceptions and trading patterns.

All of which doesn't make the job of trying to work out just how quickly rates will fall any easier.

I suspect the release of the inflation figures on October 16 is going to be pretty huge. If those figures do indeed show a 'headline' inflation figure well under 3%, but, more crucially a domestic inflation figure that is starting to drop meaningfully, then the lights are flashing bright green for aggressive rate cuts.

At that point our stressed mortgage re-fixer might have a clearer idea of what really is a good term to fix for. At the moment - well, good luck.

*This article was first published in our email for paying subscribers. See here for more details and how to subscribe.

64 Comments

I suspect the release of the inflation figures on October 16 is going to be pretty huge. If those figures do indeed show a 'headline' inflation figure well under 3%, but, more crucially a domestic inflation figure that is starting to drop meaningfully, then the lights are flashing bright green for aggressive rate cuts

That's exactly whats going to happen cos RBNZ uses over a year old data to decide what to do going forward. Which is batty in modern economies.

I am picking two 0.5% rate cuts by the RBNZ by the end of the year. And even then they will be 2% above likely inflation. So their last one may be a doozy and cut by more.

What year old data does the RBNZ use in it decision?

The headline CPI figure. It will drop around 1% in the September quarter simply because inflation (largely from the fuel tax resumption) over a year ago drops out.

CPI data isn't a year old, it's updated quarterly (not enough, should be monthly) and with the time it takes stats to compile itvit is often getting towards 6 months out of date, but not over a year old.

Anyone suggesting that the RBNZ doesn't look at the quarterly figures and only looks at the annual figure in their decision making is being disingenuous.

The quarterly figure was well within their target in December last year and every quarter since. So they don’t appear to look at it considering it took so long to start cutting back towards the neutral rate. In that time many people have lost their jobs and businesses for no reason at all. They took us from a soft landing to who knows what.

It feels like they only just realised annual was always going to be back in target this quarter when 1.8% dropped out. Almost like an “oh crap” moment, “we gonna look pretty stupid with these high interest rates and inflation at 2.3%”. Too busy doing surveys and useless predictions to see the obvious...

Who knows what .........- Millenials know from Mortal Kombat - The Spiky Pit FATALITY

If you ignore the September quarter last year (with the one-off fuel tax resumption), these are the quarterly figures. It took them until August 2024 to realise inflation was trending down in 2023 and within target from December 2023 (0.25% to 0.75% per quarter). They could have started cuts in January IMO, and certainly in April after the March quarter was released.

Dec-22:1.4%

Mar-23:1.2%

Jun-23:1.1%

Dec-23: 0.5%

Mar-24: 0.6%

Jun-24: 0.4%

within target from December 2023 (0.25% to 0.75% per quarter). They could have started cuts in January IMO,

Do you also want the RBNZ to whip the OCR up based on a single quarter of out of band CPI? Or only on the way down? A single quarter is not price stability.

If they lowered the OCR significantly, inflation started increasing over a few quarters, and then we had a quarter where inflation was above target, then yes I think they should consider increasing the OCR right then.

I agree January would have been a brave call (they would need a full employment mandate for that call), but by April it was pretty obvious they would be within the annual target by September.

You end up with oscillation if you base control outputs with 12 months lag on shorter-term inputs. If you hike the OCR based on one quarter's data you risk an overreaction from the markets who may assume a hiking trend. Same in the other direction. At least changing gears between hike/hold/drop they need to be really sure they're not going to be going the other way again within, probably, years. Market stability and predictability trumps perfect inflation control.

If you've ever implemented PID control for an oil fin heater you'll understand how this works.

They certainly seem to have a bit of an integral windup issue in current settings,

I want the RBNZ to use its freaking brains, not be solely reliant on rigid timeframe data. In an environment where there are slow changes to inflation, then its fine, use 4 quarters. In an environment where inflation is changing quite dramatically, use shorter term figures. It's not rocket science.

Kind of like if your weight fluctuated up and down over a few years, you wouldn't be overly concerned and would just make small changes in your diet/exercise to go back to normal. But if you suddenly added 20kg, you would take immediate action to stop it. You wouldn't average out your weight from a year ago and say "well the average over the year still doesn't look too bad". You would take immediate action because you would realise the difference between stable environments and non stable environments and change your behaviour accordingly.

Yes, it is. The headline figure takes into account the last 4 quarters. And 4 quarters ago they were collecting the data in July/Aug 2023 to come up with the figure for Sep 2023. Thats more than a year old data that is influencing decisions of what to do next... which is silly, particularly when we know that inflation conditions a year ago were really strong, but now aren't strong at all.

considering the CPI figure we see now is a result of the OCR 12-18 months ago, so RBNZ doesn't actually know what current inflation is or will be.

Global economies appear to be on the verge of a crash - people may say this is just another doom goblin warning. But this isn’t, there are so many economic signals right now saying we are on the edge of a very significant economic recession. Time to be extremely cautious in my view - for the next 6-12 months at least.

Recession usually occurs pretty soon after the US10-2yr yield curve normalises, which it has just done. Although this time could be different....

IO ......got the dry powder all ready for AFTER the US election (won't be buying NZ residential property - sorry Wingman), while you and I know the entire world economy doesn't give a rats about the NZ residential property market.

Unfortunately, so many here, being so far away from everything, have formed over these latter years that "She'll be right mate" - shout out to Peter Cape !

The NZ economy will go one of 2 ways :

1. Interest are reduced out of panic by the RB, that they have "overcooked" the increases - then the kiwi peso will devalue, creating further inflation, so back to square one.

2. If interest don't decrease enough, as the "market" wants, more businesses will go to the wall - and things will just grind on. unemployment will rise, recession follows ......

This is all a result of too much debt in the system, sucking the life blood out of the economy, as private debt in NZ is 138.26 % of its Nominal GDP (Mar 2024)

While the USA is forking out a trillion dollars a month, just to pay the interest on the 35 trillion of their debt - more than the defence budget....

Yes agree - I think a lot of people are underestimating how much trouble the US potentially is in. It seriously needs to address its deficit spending, but that same deficit spending is the only thing keeping their economy afloat!

its why the left imho are not the right option for the USA, right now.

Question on point 1: Will the inflation increase that much with a decrease in value of the NZD considering that many countries we export to would be impacted by a global recession. Why would importers keep importing goods i the price for consumers went up so much it wasn't palatable? Or is your point more focused on the contagion effect of higher cost of importing fuel? I wonder on that front, if the USD drops as well from a sudden event, would we then still have such an increase in fuel cost that it would have the inflationary effect we think?

@interesting1234 ....in Point 1 I am referring to oil prices, as this is an "essential" to keep everything truckin' along (pardon the pun)

While the NZD v USD will stay around 0.59 - 0.62 atm and unless something really drastic happens (your sudden event) it should stay about that level - been watching this pair since 2011 ...

Even in bad times there's green shoots. You just have to find them.

I'm sleeping extremely soundly, which probably means I've got it right.

I've heard it all before, several times. The 1987 stock market crash was a doozy. Guess who got rich?

Those who bought at the bottom.

1987

when we had 40 years of globalisation and financialisation ahead of us and population ponzinomics ahead of us

Not to mention untapped resources

Not this time

Unfortunately for you the cat's been let out of the bag.

The notion that we'll all go back to the 60's where everything ( like exchange rates) was run by extremely incompetent gubbermints will never return.

I specifically remember asking the Minister of Energy, about 1977, Bill Birch, why NZ petrol prices were controlled by the government. He replied that government control was best.

CH: "1. Interest are reduced out of panic by the RB, that they have "overcooked" the increases - then the kiwi peso will devalue, creating further inflation, so back to square one."

Dropping NZ interest rates will NOT result in a lower NZD, because other countries will also reduce their interest rate. What matters is the interest rate differential between countries, not the rate per se.

"Global economies appear to be on the verge of a crash ...."

Evidence please.

The interest rate inversions are not enough to justify such an outcome on their own as every central banker's economists (except the RBNZ's) are well aware of them.

So what overseas commentators are saying is that the NZ economy is in such dire straits that the RBNZ will be implementing emergency rate cuts?

That sounds promising for the employment and housing markets, right? Right? ....

Like chemo to a cancer patient?

When Q1 GDP is revised negative from the reported +0.2% and Q2 comes in negative as expected. NZ would have been in technical recession for an entire year. The fact that we get to find out in the 3rd month of Q3 is a national disgrace. The standing army of Stats NZ is a clown show.

When do they revise Q1 GDP? At the Q2 release?

In December last year they revised Q2 GDP (up) at the same time as announcing Q3 GDP.

If NZ housing market was the Titanic story, this is when the Quintet performed on the deck while the people was waiting for their lifeboats.

Jeez that’s bold, love the conviction behind the call but you’re saying she’s absolutely sinking with zero chance…might be right, I still think they’ll kick the can…maybe later next year, 12-18 months after that we’ll be back into the same dumb cycle…not with ‘21 style jumps but it’ll rise on the back of cheap lending and removed restrictions

No animal spirits during redundancy rounds

Your house is worth nothing if nobody will buy it

I would argue it is worth the cost of alternate accommodation.

Your house is worth a dry, warm place to live and raise your family in. Sure is worth more than sleeping on the street.

And to think, just a few months ago, the RBNZ, economists & commentators here were believing that they would hold the OCR at 5.5% until the end of 2025 lol...

Whaddya mean... 10% by Xmas, gurunteeed!

And incomes will outperform inflation, jobs are secure, and a nice 3 beddie in mission bay will be $200k.

I'll be rich, I tells ya

If you look carefully at the economic data being published...

...you'll realise RBNZ are using a vibe driven decision making process.

It's pretty simple, David.

(1) Inflation has trending coming down for months, (2) the economy is going backwards for months, (3) and the RBNZ has the OCR in a seriously contractionary setting for months.

Seriously, this is pretty damn simple.

The RBNZ has seriously overcooked us all and will now need to OVER COMPENSATE to right the ship !!!

If the government continues with its austerity measures then won’t that potentially force the RBNZ to cut even deeper to try and get things moving?

Yep!

It is virtually guaranteed.

But ...

1) Is guvmint now being as austere as they pretend?

2) Will guvmint be able to continue to be as austere as they pretended they'd be?

The answer to both is probably not.

The RBNZ has seriously overcooked us all and will now need to OVER COMPENSATE to right the ship !!!

I like how you keep thinking a soft landing was ever on the table.

I have never - not once - suggested this RBNZ would deliver a 'soft landing'.

Perhaps not exactly, but you keep making noises as if ensuring continuity should be their primary agenda, and not cutting rates last November is a mistake by them.

You're trying to wargame when they should've zigged then zagged, but it's not even with the same aims and objectives.

Creative destruction and financial reinvention are some of the only few cards they have to play.

I watched the Ray White live auctions for the North Shore. It’s safe to say in classic spring style the green shoots have finally sprung! 8 out of 14 properties sold under the hammer. The Ponzi is starting to churn back into gear. We have reached the bottom ladies and gentlemen

Yeah. I saw a swallow a month ago.

Might want to delete that from your browsing history then

Trying to figure out exactly where interest rates are going is a bit of a head-exploder at the moment

It's not that hard, the NZ economy is in really bad shape, and interest rates are going down faster and deeper than the RBNZ predicts

Throwing the timeframe out a bit, the RBNZ is essentially signalling an OCR of 3.75% by the end of 2025 and 3.00% by the end of 2026

OCR of 2.5% - 3.5% by August 2025, cuts will come in bigger sizes than 0.25%. Fix your mortgages short.

Oh look, the Fed just cut by 0.5%. I can only repeat the above:

"cuts will come in bigger sizes than 0.25%. Fix your mortgages short."

The downward spiral started a long time ago......

National sold of the power companies to increase competition.... the same companies have now, over the years, played the system to such an extent that our exporting industry are struggling and shutting down, the companies that we will rely on for export income to get out of this mess...

The minorities ( and resource management act) had it their way and hindered renewable energy infrastructure from being built ( which helped to protect the income to power companies) and kept power prices high

So to make it look good they fuelled the housing market..... theres always somebody out there that will lend you money, and once you are in neck deep debt they got you

Increased productivity is not cutting 10 minutes of a 1hour trip , its by increasing the value of the products you export, not killing off industries...

RBNZ cant fix this,no matter what they do with the OCR, when the politicians are fundamentally incompetent on both sides.

We are gonna be Greece of the south pacific... .

For the sake of businesses alike I hope they cut 50 and 50 to get this market moving again

I think we're heading into a bigger shitstorm and our own domestic economy is going to be insignificant.

Falling like dominos.

I hope your wrong, landscape is not looking promising

Out of all my B2B clients, the ones acting most paranoid and with their wallets most shut are the multinationals. I think we're so engrossed with restaurants closing, slow construction and flat retail sales, to see how grim things are globally.

Our internal woes are small potatoes.

I love reading all this bullshit about how C19 was the cause it just so happen to come around at the same time the world markets were shitting themselves. Lets print 80 billion dollars lower actual interest rates to never seen levels and then say inflation is only going to happen gradually.

Well I know something I buy gold . silver and houses

Bring on hyper inflation

Me too! I'm sure that economic lock downs and subsidizing the entire countries wages would have happened even if covid didn't happen.

Nice lol

I've been reading posts like yours from goldbugs for 20 years.

My dog knows more about economics than goldbugs. When was there last hyperinflation in NZ?

The fed just went -0.5%. chances of one of the two OCR cuts before Xmas being a double just increased massively, and some were already saying one would be a double... Are we going down a full percent by Xmas?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.