Investors took their biggest share of the mortgage advances last month in three-and-a-half years, according to the latest figures from the Reserve Bank (RBNZ).

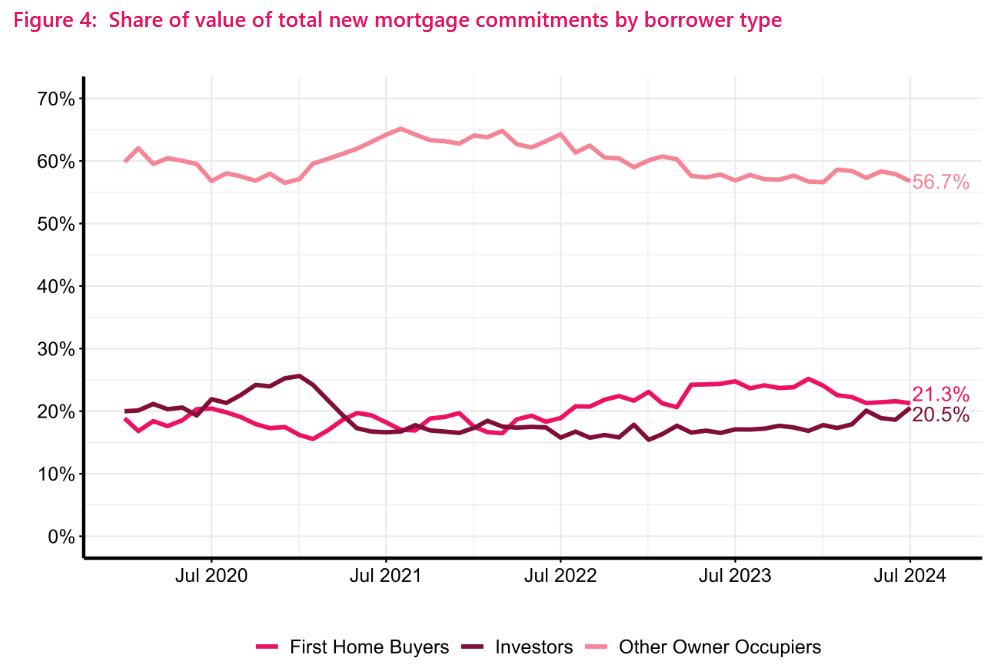

In a month that showed a bounce-back from a dire June, investors took a 20.5% share of the $6.652 billion in committed mortgage money.

This is the highest percentage for the investor grouping since the 21.8% recorded in March 2021.

And the $1.366 billion taken by the investors was the highest numerical total since November 2021.

For the investors this is all still a far cry from the days back in 2016 when this grouping was taking around 35% of mortgage money.

However, with more favourable conditions in place for the investors under the Coalition Government with restoration of interest deductiblity and a shortening of the bright-line test timeframe, economists have been looking for signs of more investor interest and what this could do to rekindle the housing market, in which prices have recently begun going backwards again.

With interest rates now going down quickly, the attitude of the long-side-lined investors will be key in setting the housing market direction next year.

While the investors have been on the sidelines, the first home buyers have enjoyed record shares of the mortgage money. In December 2023 the FHBs had a high-water mark of 25.2% of the mortgage money in that month.

However, since then the share has gradually been declining. In July the FHB share was down to 21.3%, while the $1.415 billion borrowed by this grouping was not much ahead of the investors - bearing in mind that FHBs have had a bigger monthly total than the investors every month since March 2022 - so, for nearly two and-a-half years.

In terms of the overall total of monthly mortgage money, RBNZ said that on a seasonally-adjusted basis it was up some 5.4% in July 2024 on the previous month - which as said earlier was a pretty dire one.

Compared with the same month a year ago, the July 2024 figure was up by about a third and it was the highest July figure since 2021.

In terms of numbers of mortgages taken out, the 17,442 in July was a big bounce from the very low 14,590 in June and was in fact the second highest monthly total so far this calendar year.

100 Comments

If there was ever a reason to want the market to crash this is it.

I wish they would just ### off and let those that pay the mortgage (the occupiers) own their home.

if the market crashes then there will be less people owning houses overall, not just investors.

that is bad news for families.

Good to see the market is showing signs of a recovery starting.

More of us are renting and for longer. Data shows home ownership rates have fallen across New Zealand as residential rental numbers hit a record. People can’t afford to buy a home. Renting is bad news for families stuck in financial hardship, as landlords plan their next cruise.

First home buyers are borrowing $1.415 billion. So clearly people can afford to buy a home. Not withstanding that Auckland is still way overpriced and unaffordable.

I consider auckland as a anomaly unless otherwise stated.

So clearly people can afford to buy a home.

Hmmm. Yea some can get approval for the immense amount of debt required to buy a home but many are having to forego a lot of the niceties like holidays/overseas trips, a second car, bikes, kayaks and often live pay check to pay check, unlike those that timed their births better and enjoyed the pleasure of having affordable housing and the toys.

Which is normal for most people taking on a mortgage, then a few years down the track when they have paid down the mortgage they can reduce their payments and enjoy holidays without paying for a rental and instead of rent increases, their mortgage decreases. This is how things work. People these days just want to have it all with no inhibitions to their luxury lives.

How much did your first house cost in terms of years of work? What were your housing costs as a % of your income?

The data says that today we are far worse off. New DTI limits are 6x income, yet the multiple for median income to median house price is even higher—that means a lot of hard working kiwis have been priced out. Rents are creeping up to 45-50% of take home for young renters, and almost no one can afford to rent a house on their own, you have to live with flatmates and have multiple incomes to just be able to afford shelter. Long gone are the days of the 1/4 or 1/3 income spent on housing rule. FHBs are having to rent rooms to boarders, kids these days are growing up in houses with flatmates.

You lived through good times made by strong men, ask yourself what kind of times you are making for future generations, because they sure as hell ain’t good anymore.

SKF

How much did your first house cost in terms of years of work? What were your housing costs as a % of your income?

Mine was 6x (two people's income) and the mortgage payment was over 50% of our income. We lived like paupers and got a flatmate in.

Our friends all thought we were nuts giving up the supposed best years of our lives paying a mortgage. Now they call us lucky.

Odd because even 30 years ago it was less then 4 times one persons income with an entry level job. Perhaps you brought a flash house with too many luxuries and did not work hard enough.

This was 20 years ago. And my better half and I were only a couple years into our working career, earning not great money. Nothing was 4x just one of our salaries, maybe at an absolute pinch a 1 bedroom shitbox unit miles out. We opted for a house in a better than lower quartile neighborhood.

Ah the halcyon days that no longer exist as options. Well they do but the equivalent now would be a nurse and an engineer move to Aus (because NZ is far out of reach near the same city they work) and they buy a house in a well positioned neighbourhood with good transport connections. A cautionary tale for us because there goes our medical care in retirement & functioning water and tech infrastructure, we really need to follow them soon if we plan to have medical and good infrastructure services in future decades.

Everything's relative, interest rates were up near 10% at the time. Now the minimum wage pays around $50k (back then about 18k) and interest rates are almost half (obviously higher the last 2 years). Actual affordability hasn't shifted very much.

The only significant differences today are a) some neighborhoods are now too gentrified, and b) the deposit requirements are higher.

Edit (to your edit): the nurse and engineer may leave, but their home ownership chances will not significantly improve because the country they're moving to has all the same issues and declining home ownership rates. Assuming you're talking about Australia, if they moved to the UK nurses are paid quite a bit less than NZ.

Our health system was never set up to cater for the consequences of the aging population we have. It was always going to be under resourced (but our governance has helped it be worse).

Everything's relative

Common trope. It's not

In 1995 bought our first "section", relocated a house on it, did most of the work myself, often working till 10 at night and weekends. Still live in the same house. At that time all our money went in the house, there were no extras. Our combined incomes was about 40k and our loan got to about 130k, but we did everything on the cheap with no extras. Interest rates were a lot higher, can't remember exactly now but we paid premium as land and putting house on was fround upon and only 1 bank would give us a loan. Times were extremely tough.

Your total loan was my down payment

banks being the big winner here

but without investors, where do you suppose rent the house from? and it's still cheaper renting than owning.

Nonsense.

Without investors the prices would be lower so the fhb could afford to buy.

I think you misunderstood me. if no investors, then no houses available for rent.

there will always renters in an economy, even some odd home owners need to rent in some occasions.

more importantly, housing market is not always about to make prices affordable to FHB.

This is true, there is a level of required rental properties, however there are far too many crowding the market and FHBs are suffering as well as renters due to systemic upwards pressure on rent coming from misguided ‘investors’ purchasing properties with low rental yields then aggressively attempting to raise rents to cover their poorly planned cost basis (which is why rents as a % of take home pay have consistently increased).

My wish is that, keep the house market stable, let the income grow faster than house prices. though, this might be just my little day dream.

The problem is that our smart kiwis in their 20s are leaving for Oz and other countries that offer far more in prospects, salaries and affordability (housing etc).

So for us all to make money ongoing and actually live somewhere nice.. we have to lobby to make housing affordable for the next generation. And right now that means to make intro policies to make it less attractive for specilators and investors to buy housing and for anyone to make our housing market into a ponzi again.

I keep reading people are finding it hard to find work.but in high skilled tech and other skilled industries it's increasingly hard to find anyone skilled to work for a decent salary.. they are all leaving

Ban short term rentals in cities (air bnb etc) that would free up loads of rentals

Catching a falling knife.

If it's any consolation, they're not nearly as bad as they were during 2013 - 2016.

July 2015 for example, there were 1,982 FHB @ $631m and 5,738 Investors @ $2b (RBNZ C31).

July 2024 it's 2583 FHB @ $1.42b & 2552 investors @ $1.36b

Agree. I'm a home owner with a mortgage, but I want to see it crash and burn. I am so angry and just sick of this country being run entirely for the richest 5%. Everyone seems to be just a-okay with that too.

People use houses to “park” their money because it’s easy and low-ish risk. We need tax reform that puts more pain into that behaviour and less pain into “parking” your money in businesses that actually make goods or provide services—incentivise productive investment over enabling economically damaging rent seeking behaviour.

"We need tax reform that puts more pain into that behaviour"

Singapore prioritises owner occupier buyers in the existing dwelling market.

FYI, here are Singapore's current rates of ABSD.

https://www.propertyguru.com.sg/property-guides/additional-buyers-stamp…

Let's incentivise non owner occupier buyers to buy new builds or to build new builds which adds the number of dwellings to existing dwellings and increases the number of dwellings.

Non owner occupier buyers continue to outbid owner occupier buyers in the existing dwelling market.

What would those Singaporean rates of ABSD do this behaviour? - https://www.oneroof.co.nz/news/return-of-the-land-grabbers-millions-on-…

Voters should choose policy makers who choose to prioritise owner occupier buyers over non owner occupier buyers in the existing dwelling market.

ABSD addresses this. Capital gains tax does not address this. Existing non owner occupiers will hold on - look at the impact of brightline test for non owner occupiers. Annual payments of Land Value Tax does not address this.

Home ownership rates in NZ are at multi-decade lows.

Policymakers should incentivise non owner occupier buyers to build new builds or buy new builds and add to existing dwelling supply in NZ. By re-introducing interest deductibility in the existing dwelling market, new builds are now less attractive, and more incentive by non owner occupiers to buy in the existing dwelling market over the new build market (and outbidding owner occupier buyers in the existing dwelling market)

Banks should be putting money into businesses that make goods, such as Rabobank providing loans to farmers. We also need more angel investors- not many here in NZ.

Banks are the primary beneficiaries of rising house prices (and down-sizers). It really is a con when you look into how counter intuitive “getting on the property ladder” is.

The house you actually wanted was 800k but you could only afford 500k? “Just get on the ladder” they say, so you do. You downgrade your quality of life too, paying the same with a slightly worse house or paying more than you rented for. Prices appreciate a wonderful 50% over 10 years, great you think, my house is now worth 750k! But then you realise the house you really wanted is now 1.2mil… suddenly you’ve gone from being 250k away from your ideal home to being 450k, that’s almost the entire price I paid for the house to begin with, you realise.

But they say “don’t worry, now you can borrow 5x your 250k gain, you can ‘afford’ a million dollar house just on your capital gain!” Without realising that the risk on an additional 750k is significantly higher, and if you’re leveraging you would do better leveraged into the stock market…

Your “benefit” is being allow to get yourself further and further into debt, to the point where your day job and cashflow is your limiting factor. Banks are the only ones benefiting as it’s allowing them to issue more debt with juicy premiums for the same stock of houses.

SKF

Where will the tenants live, Rastus? The ones that can't afford a house? Choose not to buy due to lifestyle(or other) and the ones that have shot credit? The ones that would have to wait on the ever increasing state house list?

Are you suggesting we have the perfect balance of landlords and tenants? That we need more landlords rather than less?

Because our home ownership trends suggest otherwise, unless you're also going to claim that less people want to own a home these days? Pretty big rationalization there.

Not at all. I'm asking whether some emotional comments around home ownership vs rentals are necessary or informed.....There are are big waiting lists to get into rentals and not all of those people can fund or justify owning a house for whatever reason, but they do have a right to have a roof over their head. Who provides these people with a home? Should we see more home ownership, of course. But the witch hunt for who is responsible seems to get emotional rather than informed!

Emotions aside, I find it dubious at best to argue that owner occupiers would be the cause of the level of unoccupied dwellings around NZ.

The ratio of population to dwellings is about the same today as it was in 1991. This is not a supply issue.

Correct. There is a utilisation issue due to speculators and investors.

When you have untaxed capital gains being used to finance, ever higher borrowing, you end up with the speculative property bubble that NZ has.

Completely ban short term rentals and we would have too many houses.

I can see this increasing over the next year as rates continue to come down.

Better get in quick DGM's.

Or you will turn into a pumpkin just after Xmas 2024........

There is just as much correlation to investor activity and low interest rates as there is to christmas and my shape changing to round.

Suggest studying almost any other recession in modern history. The "this time is diffrunt." was 2020 covid response - massive fiscal and monetary flex. Unless we go there again in the next 6mo, I wouldn't be so hopeful of a quick recovery. The economic trend is your canary, looks like it's about to fall of its perch.

The prophesies are all coming true

Lower dollar off the lower OCR

Investors bailing due to over exposure and low yields

Its a sign, the messiah has bought an investment property.....

This simply shows that, overall, it’s got harder for FHBs over the past year.

while house prices have dropped, the drops in % terms for entry level homes - often new build townhouses - have been lower than higher valued properties on full sections.

in short - the big hikes in interest rates have more than offset the falls in property prices, for FHBs

at the same time, investors will be picking up some good deals in the $1 mill - $1.5 mill range

Harder for FHB's or is word is getting out...wait, the bottom is still to come?

HM, a genuine question for you - do investors go for houses in the $1m to $1.5m range?

Exactly I would buy 3 to 4 for that and then build on the back. Had this conversation today with a young potential FHB who was looking at 1.mil house.

It's the natural way. The settlers had large plots and chopped them up + sold them off to fund retirement or lifestyle, as did their children, and their children. Has and will always be the case until they can't fit a house on and a developer will chuck up a multi-story building of flats when conditions exist that would allow a profit on them.

In Auckland I imagine that is fairly typical

Nope Queenstown. We're the market ain't going backwards

I think there is a huge range of investors and what they want/can make happen.

From buy and never sell to buy and bulldoze the existing asap. In the AKL market under 1mil you won't get enough land to knock down and build two or more.

You pays your money and takes your chances, at the peak they when paying over 4k a sq m in top suburbs for 800sqm sites with ideas to build expensive townhouses/homes. more if it was 850sqm on a corner site. (yeah that's 3.2-3.5 mil).

Been a lot more talks among family friends recently wanting to go in on IP's, with the view we're close to the bottom. Purely anecdotal of course but would be interesting to see more data in the next 6-12 months to see where we're headed with investor sentiment.

I would buy at least one tulip, just in case, and a BTC, perhaps an ounce (gold not weed, well it is actually green shoots though).

Another anecdote but FWIW I've seen several properties that had been languishing on the market for months sell in the last couple of weeks since the OCR was cut. Definitely feels like sentiment has shifted.

August HPI is just around the corner, Barefoots in AKL auctions, mainly the under 1mil is selling still very little action upper 2/3rds of market at auctions.

Will the RBNZ move quickly to adjust LVRs / DTIs to damp down this silliness?

Based on past experience ... Probably not.

(They will eventually. But by then it'll be too late.)

i wonder if there are ways around DTI's that people will find holes in.

for example.

1. if you get a loan, and change jobs to a smaller income?

2. work a second job for 3 months so you can provide a statement?

The biggest flaw is that currently the average mortgage requires an income of $42,000 to hit a DTI of 7.

Do we think the income of the average mortgage holder is higher than $42,000?

Is that the average existing mortgage?

Average sizes of new mortgages for July:

OO: $315k (~$45k for 7x DTI)

Investor: $532k ($76k for 7x DTI)

FHB: $550k ($78k for 7x DTI)

Though DTI is a total debt, not just for this new portion of debt. So assuming OO and Investors have existing debt would push those incomes higher.

It's an owner occupier (in line with your figure).

For investors and FHBs, the income requirement is just over $70k a year - average income for one person. Do we know what the average income is for a mortgage holder?

So there's plenty of overhead to push prices up - even assuming no one's trading one property for another.

Minimum wage is just under $50k/yr at 40hrs/wk currently XD

Just go to a second tier lender who are not obligated by the DTI and or LVR yes the interest is higher but that's the price of doing business

Rookie , if you read the DTI rules (like reading fine print in a contract), it says that 80% of the banks mortgage book has to be under DTI limits the other 20% not so much, its not really a valid question if you read the rules.

sharpen up young investor, the world is your leveraged oyster.

What silliness ? According to most punters on here the markets not going to recover for years so what's the rush ? LOL

Swap "market" for "entire economy" and I think you're onto something.

"Will the RBNZ move quickly to adjust LVRs / DTIs to damp down this silliness?"

Remember, the RBNZ's remit is stability of the financial system.

Housing policy is the responsibility of the central government.

Numerous governments have been willing to kick the can down the road with respect to housing unaffordability. The policies of the previous government to address the tax advantages of non owner occupier buyers over owner occupier buyers and incentives to non owner occupier buyers in new build housing to add new supply of dwellings were promising, however these policies were changed by the current government.

Hardly surprising....investors are the smart money.

Such as Lehman Brothers?

The government will be pleased as punch about this. Everyone knows that without investors there is no capital gain. This government is desperate to get them back in to the mix. They are doing absolutely nothing for owner occupiers. In fact, I think they are very likely opposed to people getting into their own homes.Their focus is entirely on "increasing rental supply" to put "downward pressure on rents." If you want a laugh read the regulatory impact statement on reinstating interest deductibility for existing homes. https://www.treasury.govt.nz/sites/default/files/2024-07/ris-ird-ridrip-dec23.pdf It's literal insanity.

The aim is to "remove a tax bias that is discouraging debt-financed investors from acquiring rental properties." No mention of home owners of course. It goes on and on about how only allowing interest deductions for new builds was unfair on people who bought new builds before the policy came in (and therefore weren't entitled to deductions). No mention of how fair this is for people who paid a premium for new builds under the previous policy, and no mention of how fair it is to landlords who aren't hugely leveraged and therefore have to pay tax on their rental income. The whole thing was just like something out of the twilight zone.

My favourite part is where agencies conclude the change is unlikely to put downward pressure on rents, and then recommend progressing the change to reduce rents. No effort made to quantify what the demographic make up is of landlords who will benefit from this policy (likely the richest). Honestly, this country is absolutely run by vested interests, with David Seymour being lobbyist in chief.

If it's so lucrative, join the club, be a landlord - and get rich....according to you.

Off you go to your bank and borrow a million or two, and Bob's your uncle....right?

Well, yes, a lot of things are lucrative. Arms dealing, human trafficking, slavery, etc. Doesn't mean we all necessarily want to get in on the action.

What a gross exaggeration, you should be ashamed of yourself.

I was a landlord for decades, it wasn't a picnic, but I got on well with my tenants and it was mutually beneficial. If it wasn't for landlords, there'd be a lot of homeless out there.

There's 40,000 empty houses in Auckland...I'll leave it to you to figure out why that is.

If it wasn't for landlords, there'd be a lot of homeless out there.

Lol what?

Reads: "If there was less demand for existing housing, there would be less existing housing existing already!"

All of it has been heavily subsidised and incentivised by successive governments, but where is the growth in the next 40 years? The last 40 took our private debt from ~20% of GDP to ~160%. Are we going to hit ~1000% GDP by 2060? Where are the debt slaves coming from? The population will be well into decline by then. Keep whispering in the ears of fools though.

Edit:

There's 40,000 empty houses in Auckland...I'll leave it to you to figure out why that is.

Uhhh because of property investment??? Sorry, landhoarding.

landhoarding

Which I why I advocate for 'landhoarders' to pay an LVT.

Encourage them to do something with empty houses and sections. If they don't then at least the LVT tax can be used to pay for something else such as income tax cuts, UBI or roads past the vacant sections and houses.

"Which I why I advocate for 'landhoarders' to pay an LVT. "

LVT rates need to be sufficiently high. Will an annual LVT be sufficient to stem this behaviour? - https://www.oneroof.co.nz/news/return-of-the-land-grabbers-millions-on-…

Singapore's current ABSD rates may be more effective.

https://www.propertyguru.com.sg/property-guides/additional-buyers-stamp…

Will an annual LVT be sufficient to stem this behaviour?

Stem? Yes, the amount of stemming will be as you rightly point out - dependent on what the LVT is set at.

That ABSD seems like more of a stamp duty, just a one off. I'm keen on the constant annual nature of an LVT as this makes it predictable in terms of revenue raised (can be used for tax relief elsewhere with relative certainty) and asks the question of the land holders each year if they want to hold more land than they need. Continual gentle prodding each year to make them do something useful with it. Whereas your ABSD, or capital gains tax for that matter, don't do that.

ABSD and capital gains taxes will have other [minor?] distortions such as an owner not selling (if they intend buying again later) when they might have done so due to the existence of these only at point of purchase/sale type taxes. Reduced liquidity due to there being no cost to hold.

Always amazed there's so many socialists posting here, on a business and investment website......wanting to lighten the pockets of those who make good decisions, work and save their money.

Posters here want taxes on everything...one of the reasons thousands of wealthy kiwis decamped for QLD a few decades ago when there was death taxes and 66c in the dollar income tax.

If you're smart you can make money on property...risky, but obviously not for you guys. I can't figure out why you guys aren't piling into it.

It's a pretty good feeling to take a huge risk and make a killing, but I guess that's not for you.

Continuing govt subsidies and incentives for non-productive investing in existing housing is more aligned with socialism than advocating for their removal.

I suppose you're all for a free market then? One where the government does not heavily intervene with the property market causing constraints, regulation, one where there are no handouts or tax incentives or low interest rate adjustments?

A free market might drop prices....don't you think?

The govt. has never subsidised anything for me. Thousands of houses in Auckland aren't being built because of bureaucracy. I agree that unlimited urban sprawl is certainly undesirable, but when it costs tens of thousands to get a new build underway, bureaucracy is driving up prices.

It's also amazing how many "capitalists" on here want all the benefits of a socialist govt (see housing supplement) in order to fuel untaxed capital gains from their "investment" business (property investment).

I'm sorry. You're right that was completely inappropriate and said in anger. The investors aren't the problem, they are just responding to economic incentives. The government is the problem, and of both stripes. They have done nothing to reverse the slow march downward of home ownership rates.

Here's something you should inwardly digest.....

The cost of housing and building is never going to go down, and that's a fact. More regulation, more civil servants, more inspections, more local body BS, more plumbing, building, environmental regulations, it's endless. The cost of subdivision, labour, fuel, et al.

It's really up to the rule makes wingman - and to date you're correct.

But rule makers and rules can change. Imagine if a land vale tax was implemented and sections were priced at only the cost to add services. Then the cost of housing would be less than it is today (all else being equal). Is it likely? Not if people keep voting the way they have been...but it is possible.

Taxes make things go up, not down, and a recent example was that dim-witted Labour minister, Robbo's tax on landlords.

Rents went up, not down.

Don't be too hard on yourself, a bit of exaggeration seems reasonable given the flippancy shown towards your apt points by some.

'Slavery' really isn't far off the mark unfortunately.

slavery is on point and a key factor in the AEWV fraud schemes.

July was a big month of changes by Govt & RBNZ... it will be interesting to watch what further impact this has on the market.

This makes sense, I've seen a few places sell for 7% yield recently, up from 4-5% max in the last few years (due mostly to lower prices, not higher rents).

If prices keep going down, I might chat to the Mrs about making some offensively low offers, still a way to go for me though.

Everybody has a price Officebound.

Maybe the entire country can be landlords renting to each other for tax benefits.... (some did this by the way back in the LAQC days), and then we could all get real estate certs and save on that too, some did this too.

And we can all make 2 times out salary while we own these each year (that's me for about 15 years.).

And this can go on forever.... wait a minute. What a party, it was icing sugar your honour.

Well yes, at the right price it becomes a good investment.

Also, you seemed to miss the many people pointing out how wrong you were on this (after you doubled down on it)

by IT GUY | 24th Aug 24, 7:34amHPI for July showed house prices Shooting DOWN 7.8% in auckland MoM

I missed the word medium price in Auckland, the altered numbers for HPI factors shows a smaller drop, this shows lots of lower end sales not many higher end hence the adjustment, Still calling confidently

-10% Dec 2023 to Dec 2024.

Virtually now one had a negative 24 call, most here where up 5-10%

Spruikers more

Is that 10% HPI, Median, or "Medium"?

Or would you like me to explain the difference?

Or are you simply throwing vague statements like that commenter a few years ago "10% interest by Christmas" who claimed victory when some second tier lender bought out a 10% rate?

I personally don't think you're wrong, but it is funny to see someone so boldly making predictions about property prices miss such a basic concept.

Higher for longer?

Australia would be a considerably more egalitarian society, and we would be financially better off if our homes were half the price they are now and we did not carry so much debt.

https://www.macrobusiness.com.au/2024/08/aussie-housing-boom-creates-mo…

Their home ownership is still 67% (although on the march downwards). They must be doing something better than we are.

What I have learnt over the years of property investing is that most people are not that financially intelligent.

The financially literate are the ones who do invest well, by buying under market value and improving and making a good profit.

Buying to rent out nowadays has passed and the money is now in the what I have just said.

Personally do not understand the Auckland market as it has appeared to be grossly overvalued for a long time.

I can understand why so many posters are bitter and twisted about housing but then they are clearly living in locations that are overvalued.

It is simple. Auckland is where they want to live. That pushes up its house prices. You live where many don’t even consider living hence your low house prices. You choose to invest in an unpopular location and you miss out on large profits .

lol you keep saying that people choose to live in Auckland.

Reality is that it is immigrants who have flooded Auckland in the last decade or two and that is a major problem.

If you ask people outside of Auckland they would say that they wouldn’t live there even if you paid them.

You only need to watch online auctions in Auckland and see who are the ones bidding and it isn’t NZ born people.

The percentage solid profits are not in Auckland at all.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.