KiwiSaver early withdrawal figures have dipped down slightly from their all-time highs in March, but people still withdrew almost $160 million during April.

New data from Inland Revenue tracking monthly KiwiSaver statistics, shows 7,020 people made early withdrawals, taking out a total of $159,228,108 from KiwiSaver during April, $13.7 million less than what was withdrawn a month earlier in March.

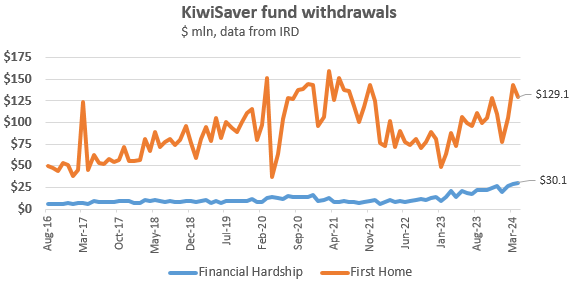

From those April headline figures, 3,320 people withdrew over $129 million in home ownership early withdrawals while 3,700 people withdrew over $30.1 million in financial hardship withdrawals.

Home ownership withdrawals in April were down around $14.6 million compared to March, but financial hardship withdrawals were up almost $1 million in the same period.

'More applications from people looking to just get by'

Amy Cavanaugh, head of Corporate Trustee Services Transformation at Public Trust, said that the number of financial hardship withdrawals from KiwiSaver schemes aligned with the trends observed by the Crown entity.

Public Trust oversees nearly 40% of New Zealand’s KiwiSaver schemes, including four out of the six default KiwiSaver providers.

“As a supervisor, we play a role in assessing the applications for withdrawal under serious financial hardship and we’re certainly seeing an increase that's reflected in those numbers,” she said.

“Financial hardship is a reflection of the economic environment and those numbers are higher than we expected them to be.”

Cavanaugh said whereas previously, people often had savings or enough money to handle unexpected expenses – like vehicle repairs – or something happening in their life – like divorce, or having a baby – that was no longer the case.

“What we’re seeing now is that they’re looking to access that [KiwiSaver] money because they don't have enough from their income just to cover minimum living expenses. So we're just seeing more applications for people looking to just get by,” she said.

While almost $160 million was withdrawn from KiwiSvers in early withdrawals in April, according to Inland Revenue, KiwiSaver providers received over $847 million in April.

It’s $100 million more than the almost $747 million KiwiSaver funds received in March.

As of April 2024, Inland Revenue said there were over 338,000 members enrolled in KiwiSaver with 3,459 new members joining in April.

Of the scheme entry method, 660,746 members were in default allocated schemes, 214,405 were in employer nominated schemes and 2,463,212 had actively chosen their KiwiSaver scheme.

Across the age bands, the 25-34 category currently has the largest number of members with 742,860.

The number of non-active members – which Inland Revenue tracks through those who opt out of the scheme as well as those who close their accounts – came to 740,067 in April.

March’s numbers

In March, $173 million was withdrawn from KiwiSaver funds in early withdrawals, the largest ever monthly amount from the retirement savings scheme.

March’s headline KiwiSaver withdrawal figure topped the $171.4 million in early withdrawals in March 2021, which was withdrawn by 7330 people.

Breaking down the March 2024 numbers, 3,630 people withdrew $143.7 million in the first home category, while 3,680 people withdrew almost $29.3 million in the financial hardship category.

KiwiSaver was introduced in July 2007 and total KiwiSaver funds under management rose $4 billion, or 4.3%, to $93.7 billion in the March 2023 year.

16 Comments

New Zealand consistently shoots itself in the foot growing our countries wealth. Be it the 70/80s where we got rid of superannuation, or the ability of kiwisaver members to withdraw down to use their retirement savings to buy a house.

Imagine how rich NZ would be if we didn't allow KS to be used to prop up the housing market. All of that capital flowing into business and commerce, rather than 4 overseas owned banks in the form of interest payments.

We urgently need to reform KS to have it compulsory like Aus ( maybe starting at 3%, moving .5% every 2-3years, so to slowly effect the lowest income earners). Offset this with adjusting the tax brackets upwards so they are net net. Stagger the employee and employer over the next 20 years and eventually have it sitting at 10% ( what Aus has just moved from over the last few years to target of 12%).

At the moment the biggest welfare cost to NZ is the pension ( which isn't means tested like all the other welfare payments nz gives out). If you read any of the experts in retirement, they all point to the fact that NZ is not going to be able to afford to continue paying this out in the coming years - as it continues to grow as a % of GDP. We seriously as a country need to begin the slow transition to a private pension, with a small government means tested top up.

Early withdrawals should continue to be applied how they are - some people need it when they fall on hard times. But remove the component to withdraw for a house.

Am I yet to hear a good argument against the above and if you give 20 years notice period, noone will be caught out investing money into KS for a house deposit. Heck you could even say anyone who has an account at the moment can use it for a house deposit, but any new members will no longer have that option.

NZ avg KS: $30k

Aus avg Super: $130k

Agree. Where the rubber-meets-the-road is the average KS balance at retirement. Statistics website puts that at $54k.

20 years from now that'll be a better picture, but contribution rates need to increase to make it meaningful.

the Aussie Super started long before Kiwisaver, and comparing average balance is not exactly fair.

The comparison was meant to show the opportunity, not have a dig.

I personally don't see any advantage of kiwisaver vs a normal investment or PIE fund. Kiwisaver can get some 'tax credit' every year, but in exchange the ks holder has to lock money till 65.

It prevents the user pulling the money out to buy random things, rather than lock it away for retirement. similiar to aus pension, or uk etc

I kind of agree with the sentiment but reality is that any prudently structured investment portfolio would have <5% investment in NZ inc (excluding NZ bonds and cash). So the argument is more about people not juicing up the housing market from Kiwisaver - still a good reason to prohibit withdrawals (and make savings compulsory).

If you had a normal investment or PIE fund you would miss out on the employer contribution and government contribution of $521 per year so a real advantage with kiwisaver

Thank you Ella for the article and stJohn for your insightful comments which I agree with. We can't keep ignoring the ticking timebomb which is our lack of retirement savings

Making the 3% employer contribution mandatory would be a good start as currently 1 milliion out of 3.5 million kiwisaver accounts aren't contributing so not getting the 3% or the govt contribution.

We should try and emulate Australias super which is one of the best in the world

But our system is rubbish. The government contribution is pointless, and probably does not cover the fees associated with it. Much better to self manager or put into a private fund. If they want KiwiSaver to work, there must be incentives, tax incentives for putting money in. At the moment, it is tax paid money, which is pointless. and the fund operators are not that good. So, never going to work.

Agreed, it is taxed twice at the moment - much to the governments delight ( extra tax revenue). Neither main party wants to touch this as they will have to find extra tax to cover the short fall, regardless of how dumb it is in the first place.

Imagine if we had similar structures to USA and 401 ROTH. The government should incentivise people putting their money in, so that they can shift the $30 billion a year cost they are incurring to pay retirement welfare, towards private. Let's say they could reduce the yearly amount by 20$ billion and still fund $10 billion a year for low income earners, they would have $20 billion a year they can put towards other expenses..

Yep, money makes money, that is what passive income is all about. There is a reason why other countries apply incentives, and they have a successful program and we don't. The reason probably is that those that could afford to chuck a load of money in and gain the tax incentives for doing so, would. But, then everyone would moan that the incentive is only available to people with money....and around and around we go getting nowhere.

You would not necessarily miss out on the employer contribution, it cost the same either way so its irrelevant to them if they contribute to a private fund or not. An employer, like mine may be willing to do that. As for the $521 a year I am quite willing to wave that for flexibility it gives me, also the lower likely hood that a future government may choose to meddle in the requirements of the fund, e.g. put up the age to 65, stop allowing withdraws on kiwi saver for houses or or change the criteria.

It really depends on your personality, I have always saved and invested I don't need the government to force me to save for my retirement, but I can see how the majority of people may need to be forced to save.

I don't know why anyone would turn down free money

Simple, haters gonna hate. (shrug).

Because it comes with conditions you may not find acceptable. If you are on a good income then that may be a price you are willing to pay. Also on the other end if you are struggling to make ends meet, $520 dollars + employer contributions in 40 years may not be as valuable to you as eating dinner today.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.