In a new consultation paper on debt serviceability restrictions, the Reserve Bank assesses the impacts of introducing a debt-to-income (DTI) cap for borrowers of six or seven and a test interest rate floor for bank lenders of 7% or 8%, but stresses these are illustrative models and might not necessarily be where it would set such restrictions.

The Reserve Bank is seeking feedback by 5pm on February 28 on the merits and design features of debt serviceability restrictions on residential mortgage lending.

“We are not proposing to implement debt serviceability restrictions at this time, but we want to prepare for implementing them in case financial stability risks warrant it,” Reserve Bank Deputy Governor Geoff Bascand says.

"We are seeking feedback on the merits and potential design of two types of debt serviceability restrictions: restrictions on debt-to-income (DTI) ratios – which impose a cap on debt as a multiple of [a borrower's] income; and a floor on the test interest rates used by banks in their serviceability assessments which test the ability of borrowers to continue repaying their loans if interest rates rise to a certain level," Bascand says.

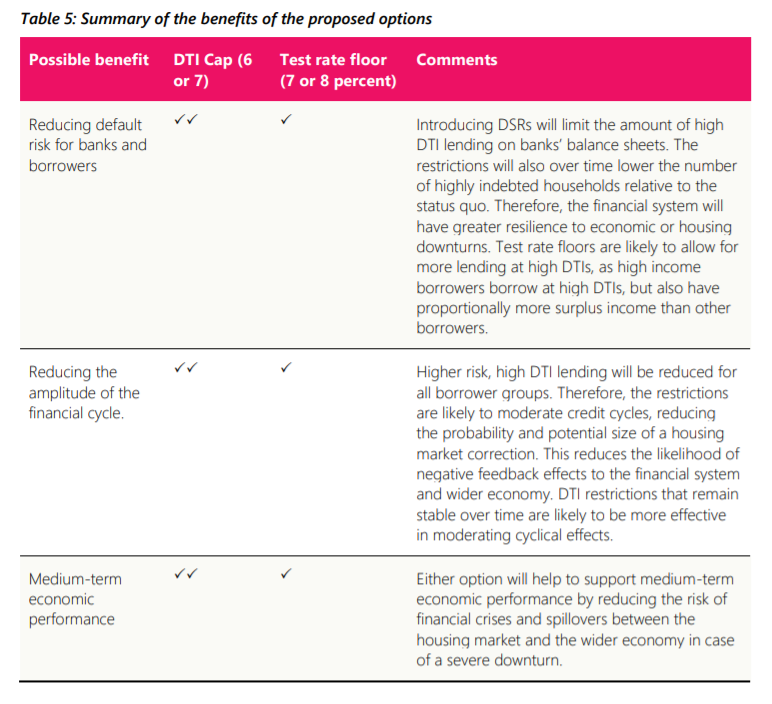

An initial assessment of the expected impacts of implementing a DTI cap of six or seven times gross income, and of a test interest rate floor at 7% or 8% are provided. However, the Reserve Bank says these settings are illustrative and don't mean the tools would be calibrated at these levels if introduced.

"At this stage it is unlikely that we would implement both options simultaneously. Instead, we are considering a staggered approach where test rate floors are implemented initially, if needed to address short-term risks. These would then be replaced by DTI restrictions once the design and calibration of these tools is finalised," the Reserve Bank says.

"In the past, we have referred to a DTI above five as ‘high-DTI’ lending. However, with the continued decline in interest rates, almost 60% of new lending is now taking place at a DTI above five, while around a third is at DTIs above six. We do not consider it appropriate to calibrate DTI restrictions in a way that would capture a very large share of lending at current levels. This could create a shock for the housing market and the potential for unintended adverse outcomes, e.g. disintermediation," the Reserve Bank says.

"As such, our initial view is that a DTI cap, if implemented, should be set at no lower than six and possibly higher. We have modelled the impacts of a DTI cap of either six or seven in our initial assessment."

"We may also want to set different calibrations for different borrower types, e.g. owner-occupiers versus investors. As such, banks should operationalise their systems to be able to introduce either the same or different DTI calibrations for owner-occupiers and investors," the Reserve Bank says.

"Further consultation on the calibration is likely to be needed, should we proceed with implementing DTI restrictions."

The Reserve Bank says banks will need to prepare their systems for the potential introduction of a regulated DTI limit no later than the end of 2022. It estimates a DTI restriction could be implemented by the fourth quarter of 2022, and a test rate floor could be implemented in the second quarter of 2022.

Banks currently set their own test rates

In terms of test interest rates, New Zealand banks currently set their own to assess a borrower’s capacity to continue to service the debt if mortgage rates were to rise from prevailing rates. These bank test interest rates have fallen in the past few years, reflecting the low interest rate environment.

"However, they have fallen more slowly than the Official Cash Rate (OCR), and hence the margin between test rates and OCR has remained relatively stable. At present the weighted-average test rate across the industry is just over 6%, which represents a margin of 5.5% above the OCR of 0.50%," the Reserve Bank says.

"There are several options that could be used to specify a floor if we implemented a test interest rate floor, such as: a. A uniform fixed test interest rate floor. b. The rate specified in the mortgage contract at origination, plus a fixed buffer. c. A benchmark rate (e.g. OCR, swap, average floating rate), plus a fixed buffer. d. The Reserve Bank’s forecast neutral interest rate, plus a fixed buffer. e. A combination of the above."

The Reserve Bank says it currently favours option (c).

"A benchmark rate, plus a fixed buffer may be the most appropriate methodology for specifying a test interest rate floor – as it fits our preference that a test interest rate floor should be stable over time, move automatically and be the same for all mortgage applicants. If we were to adopt this approach, we would need to specify a preferred benchmark, e.g. OCR, swap or other, alongside the proposed buffer."

"Option (c) would be dependent on what benchmark rate was chosen. For example, mortgage rates are closely linked to changes in the Official Cash Rate. However, a longer term rate, such as a five or ten year swap rate, might better reflect long-term trends in interest rates. To ensure that the benchmark is more stable over time, it could be reset periodically, e.g. quarterly. Additionally, borrowers would all be subject to the same test interest rate floor, which would automatically move through time," the Reserve Bank says.

The debt serviceability restrictions the Reserve Bank is consulting on would be macro-prudential tools alongside the restrictions on high residential mortgage loan-to-value ratios already in use.

"We use macroprudential tools to reduce the financial stability risks associated with ‘boom-bust’ cycles in the economy. This in turn helps us to meet our statutory purpose of ‘promoting the maintenance of a sound and efficient financial system’. Our most commonly used macroprudential tool is loan-to-value ratio (LVR) restrictions. These measure how much a bank lends against mortgaged property, compared to the value of that property," Bascand says.

“Although the financial system remains strong and banks are well-capitalised, we are concerned that the combination of very high debt levels and unsustainable house prices poses financial stability risks, particularly if current high-risk lending flows remain unchecked. Adding more options to our macroprudential toolkit will help us to address these risks if needed,” Bascand says.

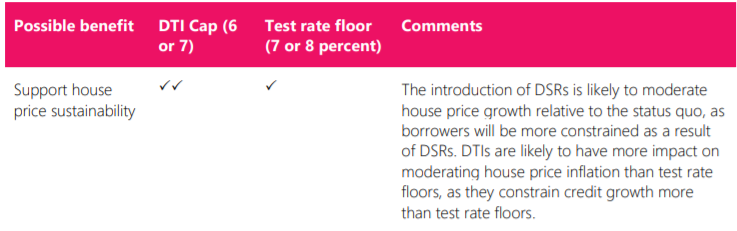

"Our initial assessment indicates that DTI restrictions are likely to be more effective than test rate floors in supporting financial stability and sustainable house prices. DTI limits link credit availability to income growth and can therefore be more effective in constraining debt levels over a longer period compared to other macroprudential tools. DTI restrictions are likely to take six to nine months to implement, while interest rate floors could be deployed faster, making them a useful interim measure."

"DTI restrictions can also be calibrated to minimise impacts on first-home buyers. This would align with the formal direction issued to us by the Minister of Finance and with our Memorandum of Understanding on macroprudential policy."

The RBNZ's attempts to add a DTI tool to its macro-prudential toolkit date back to at least 2016, but were previously stymied due to politicians' concerns about the tool's potential impact on first home buyers. The central bank previously consulted on the potential introduction of a DTI tool in 2017.

99 Comments

Yawn…. So much hot air! Keep consulting RBNZ. Talk is cheap.

There it is- considering the number 7. Unbelievable. What they are saying is they may have something ready by the end of 2022 that will be ineffective. What they should be saying is DTI of 6 now. “We are not proposing to implement debt serviceability restrictions at this time, but we want to prepare for implementing them in case financial stability risks warrant it,” HELLO Auckland average house price 1.4 million !! Wake up RBNZ. Meanwhile UK banks restricted to 4.5 times income, they learnt from 2008.

With DTI of 7, what they are saying is

Housing Ponzi trumps Financial Stability

That's 'Gross Income', so really it's like 8 or 9 times income.

Everybody knows the housing Ponzi is based of credit creation [money printing].

Everybody knows the housing Ponzi is based of credit creation [money printing].

Disagree. Only a minority really understand. The sheeple generally think the banks lend out deposits.

you're right.

But Orr has already asked our retail banks to be kind. So we can stretch it a bit :)

What they are saying is they may have something ready by the end of 2022 that will be ineffective.

"Yes, hello, we are stalling as long as we can."

This RBNZ needs fresh blood. These are the people who read books written in 1901 and are totally out of sync with modern economics. This is the modern connected world. Things happen fast in the economy these days. This is she modern age of donkey follow donkey. So if one person is doing it, everyone does it thinking it will make them all rich. Critical thinking is lost for this generation and coming generations because we read too much social media.

Nothing will change how kiwis are totally into buying houses, no amount of changes made by RBNZ will have an impact.

RBNZ is non relevant, we should just get rid of them and let more free economy.

Taxpayers will save a lot of money if we don't have to have pay for hundreds of mind numb bureaucrats sitting in those high rise buildings.

I believe that instead of an absolute number, RBNZ should ask banks to stick within a range, say 5 to 7 DTI and give individual banks to consider specific circumstances to approve each loan.

As for Test rate, why stipulate a rate for all Banks ? Each Bank's Risk Management Policy and Tools should take care of that.

RBNZ should audit test cases and satisfy itself that each Bank is being prudent in its lending.

The problem with that is banks don't have risk, if everything goes to custard then the banks will simply have the tax payers bail them out. So the best strategy for them is highest risk possible.

South Canterbury Finance, but on a far larger scale. And the government will do it, like Cyprus, Greece, and Ireland bowed to banks' pressure.

Unless they gear up Kiwibank on a massive scale in the meantime and let the Aussie banks leave if they want to. Not much chance of that.

You have to laugh at the constant consultation, paper-writing, committee-forming, feedback-seeking, pussy-footing around. It's like the RBNZ and the Labour party are singing from the exact same hymn sheet.

It’s amazing how quick they are to drop rates, launch QE, or basically instruct banks update their systems to allow for negative interest rates.

But when it comes to actually putting in place protections against the dangerous bubble they helped create it’s a long drawn out consultation that would take almost 2 years to implement. DTI tools are something the RBNZ has been asking to have for 5+ years

The RBNZ under Orr seems to be all about sending a message about the dangers of excessive debt and speculation, but always very light on any action

The statement that it takes many months to implement DTI related system changes for banks is dubious at best. One input only i.e. income x multiple = maximum allowable lending. Just not that hard.

You've obviously never worked at a bank

Sounds like you've worked at one too long... ;)

I actually did! They're lying to the RBNZ about systems.

exactly, they will piss about doing sweet FA until the everything bubble pops, then they can lay the blame on external forces.

Either way a lot of people are going the get shat on except the banks, those profiteering parasites will be at the front of the queue for taxpayer bailouts

Its the nature of our society. No one wants to take any responsibility for anything, they are so scared of putting a foot wrong they are paraletic. Look at our health and safety rules. You cant cure stupid, but boy a few more meetings and Im pretty sure we can....

Eh, they were pretty quick to leap to inflate property...

Like watching a discussion between the club manager, barman ,dj and bouncer at 3am about wasted patrons!

Keep on playing or call it quits?

Can someone tell whether the "I" in DTI is taken into account before or after being taxed?

Surely gross...

You would think so, but kind of pointless doing gross. What with PAYE, KS and SL all taken out before it even hits your bank account. Then there are child support, court garnishes and all sorts of other compulsory payments that can come out of someone's wages.

Exactly my thoughts, this will end up normalizing a family spending 75% of their net income in mortgage alone. Well done RBNZ.

Gross im at 6.6

Net im at 9.4

If I include my boarding income im at 6.7

Isnt that the point of having a 30 year mortgage though? to pull your future earnings into the present and use that time to pay it off.

All while the currency devalues.

It’s before tax. I asked the same question on these forums and someone answered with the link to the rbnz site stipulating it.

b21, it's gross income as stated in the article above.

An initial assessment of the expected impacts of implementing a DTI cap of six or seven times gross income

There's just so much wrong with this paper that it's not worth the effort of trying to analyse it.

Although, Form 1 Economics is due to attend lectures this arvo. It will be good material for them to get stuck into.

Imagine 8 percent interest rates many would have nothing to left to pay any other bills etc but great for savers and any not leveraged.

I expect it will never happen but then again the old rules no longer apply since covid hit or do they.

Looking forward to this playing out.

Inflation will be the key and at moment unless the demand falls away and cheap money end then we will crash up but I would prefer a crash down which way will it go.

"Breaking news: RBNZ starts consultation on debt-to-income measures; not intending to use them 'at this time'."

Tell us something new. We know that Mr Orr is not interested so is using all trick to slow and delay the process.

Why February and than......more time......

Insisted and waited for years to get the DTI tool (Confident that politicians will not give them) and now that they have got are sleeping over it than will start consultation than will give six months time....by that time will be 2023 and hope by that time, may not have to impliment.

It's as Farce.

He's been begging the government for years for a new car and now it turns out he doesn't even know how to drive it.

So Banks have been successful in influencing Mr Orr to not touch DTI for now, not that Orr required convincing.

Why was he insisting for DTI tool and IF NOT NOW WHEN.

Understand his attitude is wait and watch for ponzi to prosper but when house is on fire and have water, should use it to douse and not wait UNLESS enjoying the warmth from the fire.

What was he doing since August, when he got the tool and now also is IF.

Basically, he will always find reason to delay and justification.

No intent.

“This could create a shock for the housing market and the potential for unintended adverse outcomes”

It could be suggested that the above price outcome on the way up didn’t stop the RBNZ continuing to push ahead with ultra-low interest rates and excessive credit creation when no longer required.

Exactly. They have created one of the biggest Ponzi schemes of the history of modern capitalism: the NZ housing market. Given how inflated it is, the NZ housing market is in an extremely fragile state, thanks to their stupidly ultra-loose monetary policies, and now they act as if this was an act of God. They have created the problem, and be sure that they will never acknowledge responsibility for it.

Yes we can not neglect that many authorities consider our market to be a bubble and the most vulnerable housing market in the world. These are objective, international observers not local spruikers like A. Church.

Sad too, that affordable housing for more Kiwis is considered an "adverse outcome". We have no free market, just an upwards wealth transfer scheme.

The biggest threat to financial stability is the RBNZ with their constant interventions and one size fits all regulation. There will be another demand surge off the back of this as people try to get in ahead of DTIs. An interest rate floor of 8% when people are paying 4% is ridiculous. What evidence is there that regulators can manage credit risk better than the banks who are lending out the money? Government need to remove all these tools from the RBNZ toolkit including LVRs.

Were you paying attention during the GFC? If you don't regulate the financial system it will push and push until the system explodes. It's like a tragedy of the commons - if your bank doesn't push the lending criteria the other guy will, so we may as well go first.

Other countries learned from this and tightened up regulations. There is nothing inherent to NZ that makes us immune to these risks.

Hmmm, not that you have a vested interest in the continual pumping of the debt businesses do you Mr Mortgage broker.

Judging by the amount of squealing I'd say its pretty obvious how hard this will hit the mortgages being written currently.

Five years in business we have only ever had a funnel for first home buyers - we spent 30k on advertising in the last year. Our main response to this regulation is going to be to build a proper investor landing page and retarget our advertising. We are pulling the first home buyer stuff entirely. The slowing of the market is fantastic for buyers with equity (including FHBs with 20%) - there is no competition. As brokers we work the buyer side so December is looking to be the biggest month we have ever had (current projections are it will be 60% higher than May this year which was previous high). This is all largely off the back of non-bank settlements for investors who have been squeezed out by the affordability rules on rental income. I suspect we will have similar results in Q1 2022 off the back of the CCCFA legislation which forces out even more borrowers.

Even though we have spent the last week contacting first home buyer applicants and telling them they need to double their deposits I think the future looks very bright for mortgage brokers. I guess we’ll see if this stuff continues or not. Maybe it all falls over as volumes drop or maybe we head to a UK style system where potential borrowers are rationed based on their ability to pay up-front fees. I think both outcomes are pretty terrible compared to what we have now but the champagne will be flowing in newsrooms now banks aren’t lending money to first home buyers.

Must admit I do find it highly arousing the RBNZ are admitting that lenders will still be able to operate outside the ‘regulatory perimeter’ on DTIs et al. My business will look very different in a year.

Any mention on interest only loans????

It took six months for RBNZ to start the process of consultation though In June, he hinted that DTI may be implimented in start of 2022 but now the consultation will continue till end of first quarter of 2022 and than may give another six months to year to impliment.

https://www.stuff.co.nz/business/125458249/reserve-bank-gets-new-tool-t…

What the F$%@#

What was he doing till now and even if start today, does one need four months besides the of DTI as a medicine is NOW to cure the menace of ever growing house price.

They are a joke. The whole lot should be sacked.

Agreed. A very high paid bum on seat by the sounds of it.

He'll implement it in Winter; after the main selling season is over. If he'd say now that DTI at 6 or 7 applicable on say 1st January, NZ Herald and all other housing media ponzi ads would create more FOMO 'Buy now before DTI' ; and lemmings would go and buy quickly pushing the price up... he'll do it in autumn, now is unfortunately too late

So since most people are borrowing at levels considered high risk, the DTI levels will be set at a level to let this continue?

Rather than de-risk the system, they will be signaling DTIs at that level are acceptable and people will borrow to that level.

Nothing will change until people start defaulting, don't look to RBNZ to regulate against financial instability.

The RBNZ has been blatantly and consistently ignoring the most important part of its mandate and the very reason why they exist in the first place: ensuring financial stability.

Agreed. They have defaulted on their primary reason to exist. Rather than firing some of them we have employed almost 100% more of them under Labour. Mandate DTI in at 6 x with it ratcheted back to 5 the following year and so on back to 3. NZ has been held to ransom long enough with the majority of our productive effort being sucked out of NZ as foreign bank profit.

The RBNZs mandate is to de-risk the system. The RBNZs actions are to increase risk in the system.

If it's not the RBNZs job to regulate against financial instability, who the hells is it I wonder?

Consultations, committees, political correctness gone mad, paper-shuffling, pen-pushing, declarations of principles etc.... all while we have a rapidly deteriorating inflation scenario and an incredibly inflated housing Ponzi, with all the associated risks to the financial system.

We need some doers at the helm of the RBNZ, and somebody who is ready to take the necessarily unpopular but urgent actions NOW; the current indecisive muppets at the RBNZ are just full of hot air and NZ can't afford the risk of continuing with the likes of Orr. He has badly overcooked the monetary response, and he has not even acknowledged yet the urgent need to normalize monetary policies.

Hopefully the banks take the lead and raise the interest floors - that way we don't need to wait for RBNZ. I'm sure the banks would rather send a signal that they can self regulate

should not the banks own systems have these measures in place to manage the risk, i know it has changed a lot in the last twenty years and now housing makes up a large chunk of income for them, the problem i see is they know the government WILL step in if they get them selves in trouble so have taken on a lot more risk for return than they would have in the past

Self regulate agains endless super profits, and being so over leveraged and under capitalised that a Govt bailout would be required. If the RBNZ is dumb enough to allow an all reward and no risk model for banks, surely you jest that they would take the "responsible" path and self regulate against it?

"they know the Government WILL step in if they get themselves in trouble"

Like cautiously driving a truck with a trailer attached into a blind alley, there are just some situations that you cannot reverse out of - the New Zealand Property Market, driven forwards by the RBNZ/Government, is in just such a predicament.

After lots of pointless manoeuvring, backwards and forwards, the answer is to unhitch the trailer and pull it out to where you started to get into trouble.

Does that mean "Re-regulating the New Zealand Financial Markets; Fixing the NZ$ to the US$ and establishing Exchange Controls over goods and services"? Quite possibly. Because that is exactly what our biggest trading partner does.

Why now after the horse has well and truly bolted. The time for this was a long time ago before we got into this absolutely stupid situation that we now face. This should have been done long before desperate and selfish people sank their futures on infinitely increasing house prices. The professionals of government are supposed to be wise, not get caught up in the hype and act before situations occur. These proposed actions, while moving in the right direction are the reactive responses of rank amateurs.

Long term we need to migrate the DTI closer to 3.5 and lift the burden that housing places on the whole productive economy. But that is far to forward thinking for these turkeys.

Delay, delay, delay.

Did they give a 3 month "consultation" period back in early 2020 before cutting the OCR, loosening LVR's, printing money (forgery and devaluation) and stimulating the housing bubble?

That's why we are having inflation at the moment. Even now they are still trying to downplay it as "transitory".

Investors laughing all the way to the bank.

FHB now out the market throughout most of the country. 6, 7, 8, even 9x income won't get them in anywhere in Auckland. Even as a couple you would be pushing at 7 or 8.

Yep the return to the days of 3.5x are well and truly gone. The banks have already sorted the problem and have already shut the doors on FHB as they see the rates rising to 6%+. RBNZ have lost the plot, no idea what we are paying them for.

Very few FHBs take out loans at a DTI > 7 - the data is out there if you care to look. This firmly targets investors, who will moan and moan about the impact on FHBs to distract from their own problems. This is misinformation.

https://www.rbnz.govt.nz/statistics/c40-residential-mortgage-lending-by…

~40% of money loaned to investors is at a DTI > 7, versus 7% for FHBs.

Investors moan? Surely you jest! I cannot imagine the likes of Ashley Church doing such!

Maybe he's just genuinely concerned about the difficulties that NZ's youngsters face in settling down in their own home.

I'm sure it's nothing to do with the tap of easy money for investors being steadily closed one step at a time.

RBNZ Consulting of potential restriction is like the announcement about a announcement from the government.

They know what they are doing.

"They know what they are doing"

Correct but can say

They know what they are doing to ensure nothing is done lol

How blatant arrogant this people are and it reflects, how they treat kiwis that they are confident that will get away with any shit.

He has all trait to be a politician.

Yes, they do. They know this will create yet another rush of people trying to get in with DTIs of 7 and above before is too late for them, without realizing they are just jumping off the cliff.

Fail to understand why Mr Orr is playing delaying game, why is is no upfront and be honest with his intention.

DTI was and is needed as house prices are growing in double digit on monthly / Quaterley basis and that too after 35% to 80% rise since panademic, so why play.

Besides, if they delay in implimenting and if house price cool, do they realize who will be worst effected, all those FHB who are buying now under FOMO by over streching, so is it not better to impliment DTI, if have to ASAP.

This is, when one has no intention and under pressure are forced to potray but ultimately, will do what suits their vested interest.

Are they public servant, where is their accountability.

Another problem, media is reporting but not asking question theory by allowing them to get away with smirk on their face.

RBNZ dribbles on about nothing more than my Nana.

I must confess I've not heard them comment on her at all. I'm sure she's lovely, though.

Showing up late for every party, doing too much, staying too long.

So the RBNZ are consulting on a DTI rate double than what it should be, because they pumped up the housing market ridiculously with crazy monetary policy and idiotic decisions. And IF they implement it, it will be so far away it will allow another huge run up in house prices, which is already the problem that they are(n't) trying to fix.

Colour me surprised

We shouldn't be too harsh. Before they do anything they first need time to study the potential effect of the policy on climate change. Then they have to consider how this fits within the framework of Maori values. It's a complicated business and much more involved than simply keeping inflation in check and not asset blowing bubbles.

Gareth Vaugha, apt image for the article.

RBNZ will play with DTI, till FHB is not crushed under debt and still a long way to go.

Real Shame, how RBNZ is playing instead of acting just the way they did to support the ponzi.

"The RBNZ's attempts to add a DTI tool to its macro-prudential toolkit date back to at least 2016, but were previously stymied due to politicians' concerns about the tool's potential impact on first home buyers. The central bank previously consulted on the potential introduction of a DTI tool in 2017."

If they have been desperate for it since 2016, surely they must have been prepared, done their homework and if they have consulted in 2017, they just need to brush up with few meetings - so called consultation, Why do they need six to nine months for thinking and that too IF.

What is the critearea that will force them to impliment as using IF. If not now than when ????

Can someone explain what them mean by

potential for unintended adverse outcomes, e.g. disintermediation

I think it means that the banks might struggle or even collapse as the house market implodes with lots of negative equity lending, or more kindly, that people will simply borrow from non regulated lenders to achieve required gearing if the banks can't provide it. To me, I think the second explanation is difficult to justify since non banks would struggle to get funding to make a material dent in bank market share. And anyway, it's not about protecting the banks' positions, it's about protecting the NZ taxpayer and broader economy from systemic problems.

It means the RBNZ are concerned these moves are so officious that new finance companies may spring up who they can’t regulate in order to serve the borrowers who are cut out of the market

I tried running their statements through Google Translate, but all I got out was: 🤡🤡🤡🤡🤡🤡🤡🤡

DTI is 4.5x in the UK. They want to go with 7x here. Brilliant. It's totally not a bubble.

And no capital repayments if that is all you can repay....hey go interest only!

Is the choice of 8 clowns intentional? After all, the team of leadership clowns is being increased to 8.

The Chinese would say that's a lucky number.

Remember only intelligent person are Orr and Robertson, so they know best and if they say 7 times, can say as they at the back are their to support.

This just smells of "the horse has already bolted" because the RBNZ left the gate open. But rather than own up to that, they're trying to look as though they're doing something, without actually doing anything substantive. That is because the bubble will burst, which they more or less admit by not contemplating DTIs at 5x.

And interest rate caps in particular just give themselves a huge moral hazard headache. They then can't conduct monetary policy independently of mortgage lending. But I agree option c) makes most sense if you had to choose that approach.

Best solution is to require banks to allocate more shareholder's funds (capital) to risky home lending assets and let the banks make their own choices. The banks need to take the pain from their misadventure without threatening the financial system.

Agree interest rates are rising not because of their doing but for external factors.

Best opportunity for them to redeem somewhat by raising OCR by 0.5% to 1%.

Interest rates are rising as it is, like it or not so why not try to bring some normalcy at home, when have an opportunity.

Know Orr's pattern, he will not raise the OCR by 0.5% but as under pressure will have to force himself to raise by 0.25%.

Is their any betting TAB, so can bet as this characters are highly exposed and predictable.

RBNZ statement will be ( has already been printed and just has to be read tomorrow).

We thought and after consideration are raising by 0.25% for now but are concern and will keep a watch out and not hesitate to raise further, if need arises.

May also say that it was difficult to decide...

Not sure, if he will still continue with shit INFLATION IS TRANSITORY and please if he says such a thing, any person in media should ask him, what is his definition of the word Transitory ( As to manipulate can be used in relative form....compare to century, decade is Transitory or compare to decade, few years may be Transitory though uptill now - word, transitory was used for quarter or two).

They really, really don't want to shut down the housing ponzi do they?

No they dont, they obviously have no problem with house prices going even higher. On thursday they will increase the OCR a meaningless 0.25%, the banks are already effectively lending on an OCR level of about 1.5%

Banks lending mini credit crunch will not help in contain the housing ponzi.

https://thekaka.substack.com/p/banks-launch-mini-credit-crunch-but?toke…

I thought that the boom might run out of puff in March/April, but I'm bringing that forward to January.

There will be a bit of last minute FOMO before Xmas, I'm sure, but the brakes are going on big time.

You see dreaming mate. The house buying kiwis don't think sensibly. Additionally people get paid a lot in NZ and they do not have a lot to spend on.

So they eat a pie and put rest of their money in buying the house.

Lol, RBNZ logic.... pump $100billion into the market, boost house prices

Then come up with a series of ways to fix a problem they themselves created later... penalising every borrower

This is actually very good news for rents.

Which is bad for asset prices. Rents rise, CPI rises, interest rates rise, real asset prices fall.

Keep believing it IO and it might happen

Geez it is funny reading all the anguished and angry comments. Mostly by people who did not buy a home when they had the opportunity. Live life without regrets!!

And f#%k the young! That's basically what you are saying "I was born at the right time, other people should have been too!".

Ah the same attitude right before the guillotine was widely used. Be careful what you wish for because when basic needs cannot be met for essential jobs and services to keep you alive society tends to not place as much value on your life anymore. This is really easy to see in other countries where very high walls, home protection security forces and man traps are needed just to sleep safely without being killed at night. Take a look at SA; countries with very wide inequality gaps do not provide a rosy future for many. The breakdown in the value of work is another example. If you cannot afford a home with work what is the point of earning a wage as a nurse, police officer, ambulance crew, or teacher; roles far more needed in this country than any politician or RBNZ staffer. When it comes time you need a medical test for cancer you may find the refferals get delayed and turned down to deadly results and those youth who cannot get jobs from lack of education will seek other sources of income around your place. Allowing people to have basic living needs from wages is the best way to have staff in essential services so you can actually receive essential services for your life in your home. No breakdown in social fabric ends well.

It is the uncontrollables living in public housing we should all worry about.. not protesting or anarchist fhb

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.