Here's our summary of key events overnight that affect New Zealand, with news all eyes are on the US Fed.

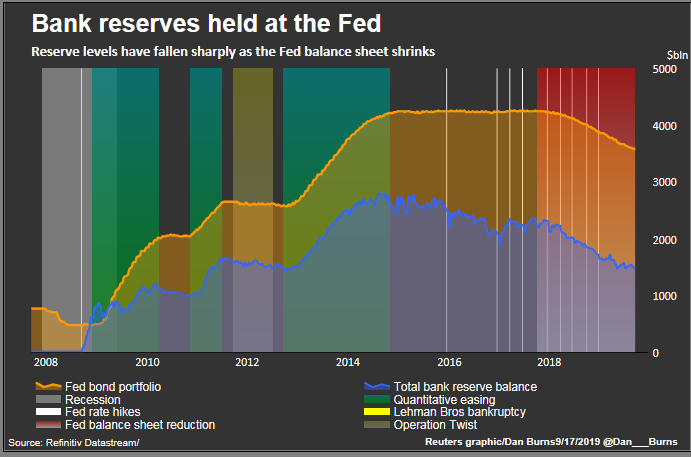

The US Fed announced its rate review decision at 8am today. However no-one expected them to make any rate changes today and they didn't. They emphasised their new favourite word; patience. So future rate hikes may be on hold. And there is a growing expectation that the Fed will not drain its stimulus reserves as much as expected as it 'normalises' its balance sheet.

{kind=link}

The S&P500 rose strongly on the announcement and is up +1.6% in mid-afternoon trade. Some stronger earnings reports also are helping.

This weekend US non-farm payrolls for January will be reported and markets expect a modest increase of +165,000 following the rather unusual December result. Today the ADP survey was released and that indicated a gain of +213,000 which is an historically average level. Most of the growth is coming from mid-sized companies, those that employ 50-500 people. The weakest contributors are employers who have staff levels under 20 - they are really struggling.

We were expecting the advance estimate for US Q4-2018 GDP today but that has been indefinitely delayed as a consequence of the shutdown. GDPNow suggests it may come in at +2.7% pa when it is released. That is higher than analysts forecasts of +2.6%.

And there was more evidence today that American residential real estate markets are in the doldrums. Pending home sales data for year-on-year contract signings fell -9.8% in December, making this the twelfth straight month of annual decreases.

By most measures, the US economic expansion is slowing, and relatively quickly.

Mexico reported its Q4-2018 GDP result today as scheduled but that wasn't strong; up +1.8% when a +2.0% result was expected and the Q3-2018 was +2.5%.

In Europe, the British are making a pigs-ear of their Brexit negotiations - and it seems the EU has had enough. The British prime minister is trudging back to Brussels to try and renegotiate an orderly separation but the nost senior EU officials look like they will have none of that. It could be humiliating. A hard, disorderly Brexit is now the most likely outcome for March 29. Britain seems tone-deaf to the idea that it is just another mid-sized economy and no longer a real player in international affairs. Even its neighbours are ignoring it now.

The official EU business climate survey results took another dip in January, matching the lower consumer sentiment. The strong confidence improvements we saw in 2017 have now all been wiped out and the next challenge will be to keep business sentiment from going negative (consumer sentiment has never been positive).

Back in Washington, the US and China opened a pivotal round of high-level talks aimed at digging out from their months-long trade war amid deep differences over Chinese practices on intellectual property and technology transfer. The American continue to send conflicting signals. The talks got off to a rough start.

In China, they have decided that some of their stimulus support will be targeted at 5G development, and the car industry. And their rival to the World Bank, the AIIB, has suddenly about-faced and now says future investment will concentrate on Chinese projects rather than in other Asian countries. New Zealand was one of many countries that took an equity stake in this development bank, but it is just an instrument of the Chinese government when it really counts.

In Australia, and in advance if the release of the Hayne Report this weekend, banks are jockeying for position, with Westpac reportedly trimming mortgage rates as their housing credit crunch bites. They see a market-share opportunity. But for some big property developers, the change is existential.

The UST 10yr yield is basically unchanged today to be just on 2.73%. Their 2-10 curve is still just under +15 bps. The Australian Govt. 10yr yield is at 2.25% and up +2 bps. The China Govt. 10yr yield is down -2 bps at 3.14%, while the New Zealand Govt. 10yr yield is unchanged at 2.35%.

Gold is up another US$1/oz to US$1,310 and that is a seven month high.

US oil prices have risen today, up about +US$1/bbl to just on US$54.50/bbl while the Brent benchmark is just on US$62/bbl.

The Kiwi dollar starts today holding at the 68.4 USc level. On the cross rates we are a little lower at 95 AUc, and holding at 59.8 euro cents. And that has the TWI-5 still at 72.5.

Bitcoin is only marginally higher today at US$3,444. This rate is charted in the exchange rate set below.

The easiest place to stay up with event risk today is by following our Economic Calendar here ».

Daily exchange rates

Select chart tabs

55 Comments

Britain has one abiding advantage that the EU doesn't in the Brexit process - it has its own currency. That....is the backstop, if ever one is needed - leaving the EU and returning to WTO trade guidelines. Britain can vary its currency, or the market will actually, to suit its own individual circumstance. With 27 other economies shackled one way or another to the Euro, that just isn't as easy. Just ask Italy!

Remember Y2K? Wasn't the World going to stop at 1 second past midnight 1/1/00? Did it? No. We all just got on with things as usual. And something similar will happen on 29th March 2019.

A lot of what is and has been written is awfulizing - I think the reality is the world will keep spinning, the sun will continue to rise in the east and the world will not end. The UK may go through some pain - how much is really unknown. In the end the UK just has to make a leap of faith and get on with it.

Agree. The EU will do all it can to ensure Britain struggles post Brexit. The biggest fear of the Germans, Belgium etc is that Britain does well as an independent. If that happens the likes of Spain, Italy, Greece will look at how they might perform under their own exits. The truth is only a few nations have done well in the EU"utopia". For the rest it's been mediocre at best.

It shows how committed they were, the only country not to adopt the Euro, how arrogant

In other news:

The official EU business climate survey results took another dip in January, matching the lower consumer sentiment... (consumer sentiment has never been positive).

Ordinary Brits who holiday in the 20% unemployment regions of southern europe still hold to their ridiculous beliefs that the EU is a big con. Their betters, who holiday in wealthier enclaves, still think they should jolly well do what they are told. 10% of Irish mortgages remain underwater.

hmmm I'm a committed Europhile, studied French at uni, speak a smattering of German, Italian and Spanish, but I've always disliked the Euro.

Then, by definition, you're a Europhobe, not a Europhile

Yvil,

That must be one of the stupidest comments I have seen and that’s saying something. The Euro is NOT Europe. It is perfectly possible to support the EU while not supporting the Euro. The Canadian economist Robert Mindel wrote the seminal work on optimal currency areas as far back as 1961 and the EU does not meet the criteria he set out.

I was an early member of New Europe set up by Anatole Kaletsky called Britain in Europe but not in the Euro.

The following comment is also a strong contender;

by Averageman | Tue, 22/01/2019 - 13:46 "Just like the GFC"

by Yvil | Tue, 22/01/2019 - 15:08 "Do you mean KFC?"

I think you might need to work on your definition of "definition" - Europhile - A person who admires Europe or is in favour of participation in the European Union. Anyway I still dislike the Euro, In the same way I thought Esperanto was a pack of balls.

Oh and as an FYI, you're also wrong - Denmark doesn't use the Euro it opted out. https://ec.europa.eu/info/business-economy-euro/euro-area/euro/eu-count…

Err no actually. The Pound used to be very strong compared to the Euro. The fact that its now almost the same is a reflection of how the bunch of looser in Europe have pulled them into a hole that they are now trying to finally get out of.

The pound was weakening long before the EU existed.

https://www.telegraph.co.uk/money/special-reports/from-5-to-122-the-200…

I think the blame may be closer to home.

Quite the opposite Carlos67, if Europe had been "a bunch of looser" to quote you, the Pound would today be stronger vs the Euro, the fact that the Pound lost a lot of ground vs the Euro shows exactly the opposite

they also have a group of nations to resume trading with called the commonwealth

of which there are 53 and include some fair sized economies like india, Australia, Canada, Singapore, Malaysia

they should shift their focus and start to resume talks with their own network of countries rather than rely on germanys puppets

https://en.wikipedia.org/wiki/List_of_member_states_of_the_Commonwealth…

The commonwealth is no replacement for the EU. The EU is about 22% of the world's economy and right on the doorstep (you can fly from the UK to most of the EU in an hour or two).

edit: for reference, the Commonwealth represents about 14% of the world economy and is dispersed across the world. Much of it takes the best part of a day to fly to from the UK.

Indeed, and it smacks of staggering arrogance that there's an assumption that the UK will be able to sign these deals without difficulty, or that those deals will be in anyway better than those currently negotiated with the EU.

A huge amount of work was put in to prevent Y2K from causing problems. If noone had seen it coming and done the work to fix it, the damage could have been huge.

So actually, the comparison with Brexit is enlightening. Here, we know there will be problems but the actual mode of exit hasn't even been decided yet, so noone can take the necessary steps. Therefore there is real potential for major disruption.

mfd,

Rubbish. The countries which did nothing suffered no damage.A vast amount of money was wasted on a non-existent problem. I had clients-self-employed IT contractors who were able to charge eye-watering hourly rates and told me that they thought it was a waste of money,

Rubbish. I was heavily involved; it was never a serious problem. What has always shocked me is nobody ever did a post mortem / debriefing to explain why. If we knew why top businessmen and governments spent so much time and money on a 'cry wolf' situation we might understand attitudes to climate warming (and I am a strong believer) and other panics.

Is the UK now facing the consequences of too many decades of political mediocrity?

This is not about being a part of the EU, but the willingness to handover the nation's industrial wealth when buying into flawed economic models?

Auckland listings on realestate.co.nz have rocketed up over the last ~30 hours.

Was at 12442 total, (6154 Houses, 1698 apartments, 547 Townhouses, 329 Units) on evening of the 28th.

Now at 13023 total, (6379 Houses, 1744 apartments, 575 Townhouses, 340 Units).

Night of 16/1/19 was 12198 total, (5898 Houses, 1672 apartments, 512 Townhouses, 320 Units)

Rush for the exits is back on?

I always thought that between Auckland Anniversary Day and Waitangi Day that a lot of properties were listed, as a lot of people who had been waiting for the holiday season to wind down finally put their properties on the market. That could be the explanation...or it could be, as you suggest, a desire to get out before things go bad. Who knows?

Indeed, Might pop into the Auction rooms at B&T on Valentines day and see how much love is in the air. Should be a fairly good indicator as volumes should be pretty high by then.

You need to get out more Pragmatist, your obsession with a constant stream of meaningless data is holding you back in life.

What the hell are you doing on here if you think data is meaningless? I guess the closed mind doesn't need data, since it already knows everything and nothing ever changes.

No govt and no amount of talking can keep growth going exponentially. Why so many don't understand this basic fact, beats me.

Quite simple their political life depends on it - they are but sycophants after all.

But infinite amount of talk can keep growth going in a logistic manner.

Which makes a lot more sense than the rubbish you prescribe to - which essentially pressumes that one day we will all of a sudden hit finite limits.

Tuesday; fine, with consistent growth.

Wednesday; fine, unchanged growth.

Thursday; catastrophe, our exponential growth path just hit our finite limit.

do they not teach reality in Econ101?

I'd ask for my money back while it's still worth something

Oh they teach some weird things in ECON 101 (typically not called that anymore). Most importantly though, they teach us about exponential versus logistic growth paths.

Evidently something they don't teach in the land of potato farming. Although just as pertinent.

But okay. Fine. Show me the reality.

Name one - just one - instance in history when we have reached the finite resources on the planet.

https://theconversation.com/phosphorus-350-years-after-its-discovery-th…

https://www.learner.org/courses/envsci/unit/text.php?unit=7&secNum=2

http://elementsmagazine.org/2017/10/06/mineral-resources-and-the-limits…

https://www.weforum.org/agenda/2018/07/fish-stocks-are-used-up-fis

https://www.theguardian.com/environment/2015/dec/02/arable-land-soil-fo…

http://science.sciencemag.org/content/343/6172/722.full

but this is the biggie, given that all else is extracted (not produced, extracted) using energy:

https://www.sciencedirect.com/science/article/pii/S0301421513003856

Cool, thanks. Well, apart from the ones that were dud links.

Just one question, though - which one highlights a time in history where we reached the finite limits of resource?

I mean, not really a biggie, but it was sort of my question.

FYI - that Energy Policy paper doesn't contradict the notion of a logarithmic growth path.

Easter Island comes to mind.

I'd say STI ridden sailors were the main cause of the collapse of the Easter Island people.

They were well past collapse long before the first sailors reached it

That's debatable.

It's generally considered that peak population was reached about one generation before the arrival of European sailors.

Nymad you can't have both statements concurrently. Makes me wonder if you actually ever defended a thesis.

Two share market indicators -

Rymans down significantly over last 6 months - a barometer for housing.

Air NZ profit downgrade - forward booking and tourism activity down.

Get rid of your debt, hunker down (and buy some gold).

I'm not saying there's necessarily a correlation, but the amount of Chinese tourists heading over seems to have dried up a bit since the announcement of the FBB, also, I think I'm correct in stating we've actually had negative immigration from China for a few months now.

Are you saying our tourism sector was 100% pure housing?

Hi Rastus

The retirement homes sector has gone on such a building spree that they may have to change the model completely. Half for the elderly and half for single mums. That way the elderly get to play grandparents and mum’s can go back to work. Much nicer environment having a few kids around!! Otherwise we’ll see bankruptcies in this sector!

Saw the following posted earlier this month on Linkedin.

http://iforce.co.nz/i/sm3ozy5w.g53.png

{kind=link}

Retirement Villages:

Ryman Healthcare - 39 Projects totaling $899 Million

Summerset Management - 37 Projects totaling $741 Million

Metlifecare Auckland - 25 Projects totaling $679 Million

Oceania Group - 18 Projects totaling $381 Million

Arvida Group - 14 Projects totaling $321 Million

"The British are making a pig's ear of Brexit negotiations". Really? Here's what I call a pigs-ear!

"Brussels orders Britain to pay £39bn Brexit bill even if there is no deal".

But of course, that's a quote today from the person who famously stated: "When it gets serious, you have to lie". Good one, Jean-Claude....(Psst. JC! Whatever happened to "Nothing is agreed, until everything is agreed")

"Britain seems tone-deaf to the idea that it is just another mid-sized economy and no longer a real player in international affairs. Even its neighbours are ignoring it now."

Perhaps things closer to home are of more interest:

" households with an income of $180,000 expenses were understated by $80,000, increasing borrowing capacity by $640,000. In 2016, a household would have been approved for a $1.15 million loan but would now only be able to borrow $620,000.....banks systemically relied on expense measures that potentially overstated the ability of borrowers to service their loans, and the application of responsible lending laws is set to feature prominently."

Of course, that's the Aussie banks - nothing to do with us....

https://www.afr.com/business/banking-and-finance/credit-crunch-to-trigg…

The UK is the second biggest economy in the EU after Germany and the 9th largest in the World (GDP—PPP) . It would be foolish for its neighbours to ignore it. Even more foolish to do so from the an export dependent country at position 67 - whatever prejudices one nurses or reads.

https://statisticstimes.com/economy/countries-by-projected-gdp.php

Britain is never going to pay the £39bn. Brussels will get the middle finger. Take Germany out of the Euro and the wheels will fall off it. Germany wants to sell its BMW's, Mercedes and Porsche's to the UK so will sign an independent trade deal before the ink is even dry on the Brexit "No Deal".

Apologies I’m a bit lost with your statement, are you saying Germany will sign an independent trade deal with the UK? Or are you saying the EU will negotiate a better deal than the one that’s on the table after Brexit?

If it’s the first you have absolutely no understanding of how the EU works, if it’s the second I’ve got a bridge I can sell you and some unicorns that shit gold...

"....the AIIB, has suddenly about-faced and now says future investment will concentrate on Chinese projects rather than in other Asian countries....."

OMG!! Why did we ever support such a thing!!!!

Because JK was a Chinese puppet.

Job done - 20 million dollar house sale as the bonus! You can keep the tennis court John.

We were never asked to " support it"

"Another grand legacy by Jonkey...

"NZ played an important role in setting up an international investment bank that will initially have capital close to $143B, John Key says."

Used the proceeds from electricity sales to fund it (vs. schools, hospitals, etc). Country was duped.

Bond Curves Right All Along,

https://www.alhambrapartners.com/2019/01/30/bond-curves-right-all-along…

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.