Here's my summary of the key events overnight that affect New Zealand, with news the IMF is calling out China's dangerous credit growth.

First up today however, the latest dairy auction was a disappointment. Prices did not gain as the derivatives market signaled. In the end, they were essentially unchanged in USD, dipping just -0.4% overall. However, given the fall in the New Zealand dollar since the last auction, these prices actually represent a gain of +3% in NZD terms. Among the key components there were few movements of note. This was a market event that gave no hint of future direction for dairy prices. There will be no forecast milk price changes based on this.

In the US, retail sales recorded their biggest increase in seven months in July as consumers boosted purchases of cars and raised discretionary spending, suggesting the economy continued to gain momentum early in the third quarter. This data is somewhat at odds with the weak car maker reports, but their sales to the rental car companies (which were very much lower) aren't in consumer retail sales. Along with higher retail sales, business inventories rose a little, which is where some of that car production probably went.

A detailed national survey by the New York Fed shows household borrowing is growing modestly but credit card delinquencies are rising. Total household debt rose by +4.5% to $12.8 tln in the second quarter of 2017 from the same period a year earlier. There were small increases in mortgage, car, and credit card debt, no change to student loan debt, and a decline in home equity lines of credit. Flows of credit card balances into both early and serious delinquencies climbed for the third straight quarter - a trend not seen since 2009.

American household credit may be generally under control, but the same cannot be said for China, according to the IMF. They are warning that China's credit growth is on a "dangerous trajectory". They say there is an increasing risk of a "disruptive adjustment" and/or a marked slowdown in economic growth" and they want to see "decisive action" to deflate the credit boom smoothly.

And investment in and by China is shrinking. Inbound foreign direct investment stopped growing and actually slipped -1.2% in July on a year-on-year basis. But Chinese outbound foreign investment plunged -44% on the same basis.

In Canada, sales of existing homes in July fell from the prior month, the fourth straight monthly decline amid a widespread cooling of the Canadian housing market. Sales volumes are down -12% year-on-year, and the national average prices are unchanged from a year ago, now having given up C$80,000 in gains in those four months. The average Canadian home sells for C$478,700 (NZ$518,200).

In Australia, political conversations are getting extreme and silly. All sorts of unseemly accusations are flying about "the day New Zealand conspired" to take down Malcolm Turnbull. The Trumpification of political discourse has gotten seriously out of hand in Canberra and their news media.

In New York, the UST 10yr yield is higher today, now at 2.27%.

The price of oil is unchanged today US$47.50 a barrel, while the Brent benchmark is still at US$50.50.

The price of gold is lower, down -US$7 to US$1,273/oz.

And the Kiwi dollar will start lower today at 72.3 USc, a one month low. On the cross rates we are unchanged at 92.5 AU¢, and at 61.6 euro cents. As a result that puts the TWI-5 index at 75.1.

If you want to catch up with all the changes yesterday, we have an update here.

The easiest place to stay up with event risk today is by following our Economic Calendar here ».

Daily exchange rates

Select chart tabs

32 Comments

""Chinese outbound foreign investment plunged -44%"" - is this echoing through our Auckland property market? A housing market only needs a small variation in the buying to massively alter prices.

It seems hardly a day goes by without reading some "warning" about China's debt level.

Yet, if the 2008 GFC is anything to go by, when the whole debt pile does collapse many will be screaming "why didn't you warn us?"

Very good point.

Everyone makes their own decisions.

If you wish, you can de-risk right now.

You may not make any additional big gains, but you will sleep easier.

Gerry Brownlee intentionally lied about Labour's involvement. It looks like dirty election tactics to me. If anyone really wanted to undermine the Australian Government the best way to do it is to leave Turnbull in power. In the end the real fault lies in the writing of their Constitution, which according to the latest political nonsense must have been written by New Zealand spies.

Yep - New Zealand spies are everywhere.....

Whats wrong with having a nationalistic constitution?

The Australians are upset that we wrote it.

Once they realise that every MP in their Parliament is either a Kiwi or a boat person they will understand who their next PM must be.

http://i.huffpost.com/gen/4117352/thumbs/o-ABORIGINAL-ELDER-570.jpg

{kind=link}

The whole Barnaby Joyce fiasco is just another indication of the shambles of the laws and constitution in Australia. No wonder NZers have stopped moving there; we don't even know what our rights are.

It is an amazing read.

I had to have a laugh at the fact, you don't have to be an Australian Citizen, you just can't be a citizen anywhere else.

The real part I like, is that in theory it is entirely dependent on other countries policies. i.e. We in NZ, could pass a law that grants all Australian MPs immediate NZ Citizenship and all the entitlements that come with it, upon successful election/re-election.

Boom, every successful Aussie MP would then have to formally revoke the citizenship after every election, or stand down.

Oh the fun that can be had with outdated laws and red-tape.

So typical of Australians.

They bury themselves in a mountain of bureaucratic laws that they barely heed beyond mindless box ticking, then cut up very rough if somebody has the temerity to point out if one of their mates is not complying. The problem lies with the silly laws.

Question - if they manage to negotiate round this situation, will all the other M.P.s who had to resign be allowed to return, or are the rules different for the members of the ruling government?

Chris-M I think they've put themselves in a complete bind. If those MPs can't return then why is the Deputy PM still in his seat.

I've also seen part of Section 44 of the Constitution posted and it rambles on about being under the influence of a foreign power. We don't even need to pass a silly law. The New Zealand Government could make a payment to every Australian MP, then they would all be under the influence of our Government. Technically they would all be disqualified as MPs. They are truly stupid.

Invest in such a way as to take into account a nasty debt fueled disruption with its origins in China - it's coming folks!

It will happen, the only question is when.

When things look too good to be true .............. they usually are . Remember how before 1997 , we called the Asian economies "Tigers" and saw spectacular growth , investment and rapid indutrialization .............. until the Asian Banking Crisis exposed the truth .

China continues to be a worry, the swings and movements in stats are big , and there is a risk they could lose control of the markets they have been so good at managing by dictat.

Dont be surprised if a financial crisis comes from the left of the field , like the previous crises we " never saw coming " .......... the Asian Banking crisis or the GFC .

Don't forget the Celtic Tiger as well.

Absolutely , I forgot about how the Irish got totally carried away with a credit fueled boom . China should take heed

admin please delete

In the US, retail sales recorded their biggest increase in seven months in July as consumers boosted purchases of cars and raised discretionary spending, suggesting the economy continued to gain momentum early in the third quarter.

Hmmmmm.....

The Commerce Department reports this morning that total retail sales last month were $479.9 billion, compared to $443.3 billion in July 2014, or $459.6 billion in July 2015 (for a pitiful 2-year growth rate of just 4.4%). Again, retail sales growth is concerning at less than 6% for a single year, so at barely more than 4% for two years indicates a special kind of stubborn stagnation that doesn’t fit the normal accounting of cyclical upturns and downturns.

Seasonally-adjusted, retail sales were up on the month, which is all the mainstream will focus on (as well as upward revisions to last month, almost entirely in auto sales). Year-over-year unadjusted, retail sales increased by just 3.6%, the second straight month less than 4%. This is the same sort of weakness that was evident for US consumers in late 2014 and early 2015. To this point, retail sales have yet to even match the “upswing” in 2014.

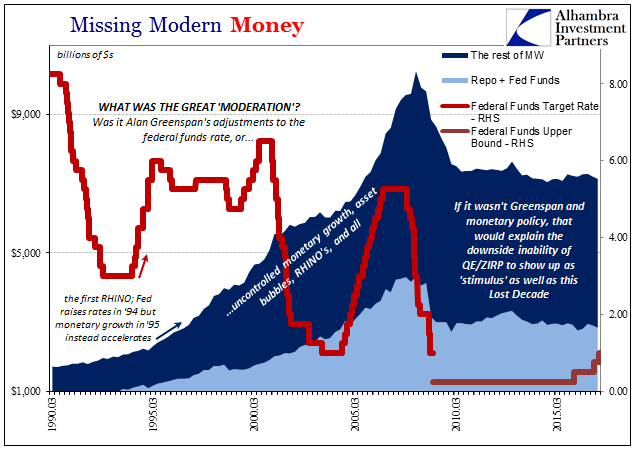

And like then, such softness will be characterized as “strong” and “resilient” so as to match in the conventional characterization the economy that “should be” as described by the unemployment rate (or Job Openings, to a lesser extent). In July 1999, the 2-year change in retail sales was 13.2%, including the first year captured by the downturn. That is actually “strong” or “resilient”, though it ultimately had nothing to do with Alan Greenspan or the federal funds rate. Read more

{kind=link}

"The Trumpification of..."

Please think before joining the rhetoric of the mass media.

Yes agreed, It's Trump that started this recent mess, by threatening large trade tariffs on China. Not to mention that he's quite happy to bring the world to the brink of Nukular war just so he can scare munger smaller countries in to buying arms from the U.S.

"Over the past 12 months, 1.5M borrowers have purchased a home by putting down less than 10 percent, which is close to a seven-year high in low down payment purchase volumes." Read more

Mortgage plus 2-3 x $500/month car payments + credit card debt means there will be another round of pain. I suspect there is still a massive housing oversupply in many areas in the US which will be holding house prices too high. Good luck to their financial system.

"Good luck to their financial system"

Unfortunately thats our financial system as well ...

The mechanics of being a dealer was at the start truly simple. The Federal Reserve would aid in the process by funding this warehousing of paper. Dealers would buy securities from the government or whatever agency (or private bonds later on) and then repo them back to the Fed or other dealers (with spare cash) as a way to finance them while they were being sold through brokerage. Since the funding arrangements were fully collateralized and often very short term, it meant some of the cheapest funding available.

By the 1980’s, it was significantly less than deposit funding (after the demise of Regulation Q) such that banks wanted in on repo, too. That meant a robust underground of sorts, where dealers could, for a fee, meaning spread, lend out their warehouse inventory to banks seeking repo financing. The 1990’s were a good time to be in securities lending, so long as, unlike Solly, you didn’t get caught being too aggressive.

This is how the dealer network was positioned throughout the late eurodollar period. Eurodollar is in my use an imprecise term, as the system overall became far more than just overseas deposits of dollars. It has become the emblem of wholesale or shadow functions that similar to the original eurodollars are freed from geographical constraints. So long as you are in that business, a dealer might conduct securities lending with a bank anywhere in the world. Read more

DEBT... according to our PM that is a good thing for FHB to take on, based on his stupid comments yesterday about removing LVR's...

Debt is something that FHB really need, on top of their student loans and any other debts.

This link is for anyone who is afraid robots are about to take over their job:

https://twitter.com/dataduce/status/897228678802755584

Hope it's okay to post links like this.

Ralph you might be distressed to find out that the robot's performance is still better than the human it would replace.

LOL - man I laughed.

the main problem with the robot is that he wouldn't meet the criteria for US car or home loan approval ... ie he can't fog glass

Heavens forbid making a flat white.

I agree that China is going to have a correction but expect it to bounce back and continue on.

The Asian tigers have massive foreign debt (160% gdp) and it was outflow of this capital as much as too much credit that caused the financial crises. China on the other hand has something like 15% foreign debt. Note also that the asian tigers recovered to have ~5% gdp pretty quickly and compare well vs. western economies

https://www.google.com/publicdata/explore?ds=d5bncppjof8f9_&met_y=ny_gd…

The main reason that long term trend will favour china is that it is only half done with urbanisation

https://tradingeconomics.com/china/rural-population-percent-of-total-po…

vs, say, korea

https://tradingeconomics.com/south-korea/rural-population-percent-of-to…

So I see chinese credit crises but different than asian crises as not exaggerated by exit of foreign capital and then continued growth. So many factors that it is crystal ball stuff but that is my best guess.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.