Top 10 at 10: US housing down for 20 years; 'US$ like sterling after WWI'; IMF selling gold; Dilbert

22nd Sep 09, 1:03pm

by

Here are my top 10 links from around the Internet at 10am. I welcome your additions and comments in the comments below or please send me your suggestions for Wednesday's Top 10 at 10 to bernard.hickey@interest.co.nz My apologies for lateness again today. I'm travelling a bit today and filing this from Wellington. Great weather here. No design specs here...

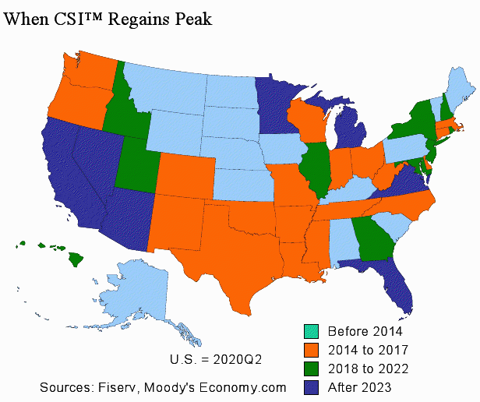

1. Moody's is forecasting that US house prices will fall 40% from their peak to their trough and some US states will not recover to their 2006 peak levels until the early 2030s, Marketwatch is reporting. HT Kate via comment stream.

1. Moody's is forecasting that US house prices will fall 40% from their peak to their trough and some US states will not recover to their 2006 peak levels until the early 2030s, Marketwatch is reporting. HT Kate via comment stream.

"For many reasons, the rebound will be disproportionately small compared to the decline," Moody's said this week in its latest outlook on the residential market. "It will take more than a decade to completely recover from the 40% peak-to-trough decline in national home prices." "The scars that this downturn will leave on the economy and the housing market will be long lasting and persist in nearly all facets of the housing industry, including the demand for homes, ownership patterns, homebuilding, and house price appreciation," the analysts forecast. "It will take more than a decade for many measures of housing activity to regain ground that has been lost as a result of the correction: The intense downturn will overcorrect for the excesses in the housing market generated by the boom years," they added.

2. It's worth watching what former Morgan Stanley China guru Andy Xie (who was let go for saying Singapore was built on laundered money) has to say. He writes cogently here at caijing.com about the risks of going down Japan's borrow and spend path to deal with the bursting of an asset bubble. He details a startling fact: Japanese nominal GDP will be lower in 2009 than it was in 1993. HT AndrewJ via comment stream.

2. It's worth watching what former Morgan Stanley China guru Andy Xie (who was let go for saying Singapore was built on laundered money) has to say. He writes cogently here at caijing.com about the risks of going down Japan's borrow and spend path to deal with the bursting of an asset bubble. He details a startling fact: Japanese nominal GDP will be lower in 2009 than it was in 1993. HT AndrewJ via comment stream.

Anyone who doesn't believe in the harm of a financial bubble but does believe in Keynesian stimulus magic should visit Japan. A likely dip for the Anglo-Saxon economies next year will underscore these truths. The same goes for anyone who thinks China's latest real estate bubble, asset borrowing and shadow banking system are worthwhile substitutes for real economic growth. The world including China can learn a lot by looking at what's happened to Japan, and what's in store for DPJ. Since Japan's stock market bubble burst in 1989 and the land market popped in 1992, the LDP government has run up debt equal to nearly 200 percent GDP in hopes of reviving the economy. And its economy has stagnated. The burst of the global credit bubble in 2008 brought down Japan's export machine. That was its only hope. Now, of all OECD economies, Japan's looks most like a depression. Its nominal GDP declined 8 percent in the first quarter 2009 from the year before. Although its economy rebounded a bit in the second quarter, nominal GDP for 2009 is still expected to decline substantially and will likely be lower than in 1993.3. Ambrose Evans Pritchard at The Telegraph always seems to find the best little gems. Here's a research note from HSBC saying America's profligacy will force China and others to forge a new global currency order. HT AndrewJ and Troy Barsten

"The dollar looks awfully like sterling after the First World War," said David Bloom, the bank's currency chief. "The whole picture of risk-reward for emerging market currencies has changed. It is not so much that they have risen to our standards, it is that we have fallen to theirs. It used to be that sovereign risk was mainly an emerging market issue but the events of the last year have shown that this is no longer the case. Look at the UK "“ debt is racing up to 100pc of GDP," he said Crucially, China and rising Asia have reached the point where they can no longer keep holding down their currencies to boost exports because this is causing mayhem to their own economies, stoking asset bubbles. Asia's "mercantilist mindset" of recent decades is about to be broken by the spectre of an inflation spiral.4. And here's another one from Ambrose on the problems in Estonia, where house prices have fallen 59% from their peak in the capital Tallinn. It's worth watching the Baltics because there are a bunch of Western European or Nordic banks exposed to any currency devaluation and national default. Estonia is hanging on to its peg for dear life. HT Greg Elliott.

Swedbank says up to 30pc of its mortgages in Estonia are in negative equity. Recent loans are in euros "“ not the local kroon. Professor Ãœlo Ennuste from Tallinn University says the private net wealth of Estonia's people has fallen below zero. I know of no other country in the world where this has occurred, though Latvia may be deeper in hock. Estonia's foreign debt is 116pc of GDP, second highest in Eastern Europe.New Zealand's foreign debt is 140% and rising fast... 5. The WallStJournal has a very detailed piece on the spare capacity in the US economy that is pressing down on prices, including in one town called Bend in central Oregon. HT Peter Moore via email

Additional underutilized industrial space, housing and workers are apparent across town. More than 9,000 people have lost jobs since mid-2006. Some 29% of homes are vacant. "For Lease" signs hang on store windows near the town's main drag, Wall Street. Similar slack -- the unused portion of an economy's productive capacity -- is evident across the U.S. Thousands of airplanes and hundreds of thousands of train cars sit unused, hotels report their highest vacancy rates in at least two decades, and millions of Americans are underemployed. How much slack there is in the U.S. economy, how fast it can be taken up and the degree to which it matters will be central to the debate when Federal Reserve officials convene this week.6. For those goldwatchers out there this is a useful piece in Bloomberg on how the IMF is selling 403.3 metric tons of gold. We wish them luck with the orderly sale.... HT Greg Elliott.

"These sales will be conducted in a responsible and transparent manner that avoids disruption of the gold market," IMF Managing Director Dominique Strauss-Kahn said in the statement. The IMF board last year endorsed the quantity to be sold, which accounts for one-eighth of the IMF's total gold stockpile, as part of a plan to shore up its finances. The sale will also increase the agency's ability to lend at reduced rates to low- income countries. The IMF is the world's third-largest holder of gold reserves.7. Felix Salmon from Reuters links to a fascinating study on just how many US mortgage holders send their keys back to the banks in so-called 'jingle mail'. The fancy phrase for it is 'strategic default'.

Unsurprisingly, it's financially sophisticated borrowers in non-recourse states like California who are doing this in droves: apparently there were 588,000 nationwide strategic defaults in 2008, more than double the total in 2007. This is a perfectly rational and ethically defensible thing to do, but subprime borrowers, almost by definition, tend not to have the sophistication to default in the most financially-advantageous way. Interestingly, the Experian-Wyman study (if anybody has a copy of it, do send it on over) recommends "that lenders and loan servicers take steps to screen and identify strategic defaulters in advance". I'd love to know how lenders are meant to do that. Credit score obviously isn't a good indicator, so what is? Financial literacy?8. Satyajit Das reckons in a guest post at Naked Capitalism there will be little meaningful reform in the way derivatives will be regulated in major markets. Plus ca change.

Volatile equity and currency markets caused problems with exotic option "accumulators" (known to traders as "I-will-kill-you-later"). Numerous investors and corporations are bunkered down with their lawyers hoping to litigate their way out of significant losses on "hedges" pleading familiar defenses "“ "I did not understand the risks" or "I was misled about the risks by the bank". If you assumed that these events meant that wild beast of derivatives would be tamed, then you would be wrong. History tells us that there will be cosmetic changes to the functioning of the market but business as usual will resume in the not too distant future. Problems with derivative problems of portfolio insurance in 1987 and Long Term Capital Management ("LTCM") in 1998 did not lead to fundamental changes in the operation of derivatives markets. "Holy water", "hosanna's" or other utterances (based on particular religious convictions) will be sprinkled or said in the form of initiatives to improve disclosure, increase capital and a new centralised counterparty ("CCP") to reduce the risk of a major dealer failing. Fundamental issues "“ the use for derivative for speculation, mis-selling of instruments to less sophisticated market participants, complexity, valuation problems "“ will not be substantively addressed. The industry and its key lobby group (ISDA "“ International Swaps & Derivatives Association) are well practiced in the art of regulatory skullduggery. Derivatives, it will be argued, are soooo complicated that only derivative traders themselves can properly "regulate" them. If this fails then there will be more subtle rhetorical thrusts.9. Former IMF chief economist Simon Johnson writing at The Baseline Scenario angrily rejects the push at the G20 to rectify imbalances in the global economy. He makes a strong case.

Granted, big current account imbalances are not a good thing and should be on some list of problems to address. But are they really on the top ten list of pressing issues for this G20 summit, which should include: much tougher financial regulation, substantially raising capital standards, workable cross-border rules for handling failed banks, a timetable for downsizing our biggest banks, how credit rating agencies are paid, and reforming "“ top to bottom "“ financial sector compensation?10. Gillian Tett at the FT points out how Barclays is shuffling some toxic Lehman era assets out the back door of its balance sheet to make things look better. It looks suspiciously like the same old practice of banks engaging in regulatory arbitrage so they can run light on capital.

For the really dirty secret that currently bedevils the whole financial reform debate is that the more that regulators force banks to clean up their "front rooms" (ie regulated activity), the greater the risk that activity will flee to unregulated corners of finance "“ if nothing else because financiers have little desire to subject their pay to public scrutiny. In theory, regulators could prevent that outflow, if they were willing to clamp down on the unregulated world in a co-ordinated way. In practice, though, western leaders are finding it so tough to agree on how to reform the front rooms of finance that I seriously doubt they will have the energy to attack the cellars too. Thus far, few banks have had the political chutzpah to exploit that situation too brazenly. Barclays, however, now appears to be blazing a trail of sorts "“ and I would hazard a bet that plenty more banks will be tempted to follow suit. So stand by to see more Protium-style deals emerge in the coming months. After all, financial cellars can come in numerous forms "“ and, it would seem, ever more weird names.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.