This Top 5 comes from interest.co.nz's Gareth Vaughan.

As always, we welcome your additions in the comments below or via email to david.chaston@interest.co.nz. And if you're interested in contributing a guest Top 5 yourself, contact gareth.vaughan@interest.co.nz.

— Bill Bramhall (@BillBramhall) May 30, 2024

1) 'The most compelling trade I have ever seen.'

Earlier this week I saw this Stuff story about people stealing copper from powerlines in Christchurch. Such stories are all too common. One of the more brazen local thefts was the theft of copper sheeting from the Stardome Observatory and Planetarium at Auckland's Cornwall Park last year. This proved a costly crime, with a telescope at the Stardome only reopening almost a year later.

Such thefts aren't new. Some years back I remember teasing Interest.co.nz's then-resident copper bull commenter "Wolly" after another theft. (I wrote about Wolly and copper in a previous Top 5 here).

The copper price has been on the rise again, see more in the chart below. And Bloomberg's Odd Lots podcast has done another copper episode. In it hosts Tracy Alloway and Joe Weisenthal speak with Jeff Currie, who is described as "a long-time copper bull and commodities veteran who's now at Carlyle Group."

A bull Currie certainly is. Here's a taste;

You know, it is the most compelling trade I have ever seen in my 30 plus years of doing this. You look at the demand story, it's got green CapEx, it's got AI, remember AI can't happen without the energy demand and the constraint on the electricity grid is going to be copper.

And then you have the military demand. So unprecedented demand growth against unprecedented weakness in supply growth because we have not been investing, it's teed you up for what I would argue is the most bullish commodity that I actually, I just quote many of our clients and other market participants say, you know, it's the highest conviction trade they've ever seen.

Alloway asks Currie for a price target and timeframe.

You know, our view over, call it a two- to three-year horizon is it's got to reach somewhere around $15,000 a ton. Where do we get the $15,000? A ton is, you go back to 1968, the beginning of that supercycle and it was a big housing boom driven by the war on poverty through, you know, the great society. We saw copper prices reach the equivalent of $15,000 a ton.

We know that demand destruction occurred. Now, we'd never had another opportunity other than that time period to observe demand destruction because that's basically, you know, at the end use consumer level, you're out of supply, like that Korean concentrate situation. You ran out of supply, you're short and now you have to get the end-use consumer to ration their demand out.

That's when you find out how high these commodity prices can go. And that $15,000 a ton was, say, okay, the only time in history we've observed actual physical demand destruction or rationing of physical supplies was that time period. Whether or not that holds in the current environment, we'll find out. But that's our best guess of where prices could go because we've seen it before.

How long does it take to get to that dynamic? I thought we would've been to that dynamic by now. I would tend to think of, you know, if we meet back up in the next 12 to 18 months, there's a probability that we're looking at prices in that $12,500 to $15,000 range. Because if we know it's happening at the concentrate level, it's just a matter of time before it starts to physically happen at the end-use level. And that's where places, you know, the markets like the LME and the Comax are pricing it. And that's where you would see that price spike.

Semi-precious metals

Select chart tabs

The tweet/X post below from Forum New Economy, or the New Economy Forum, caught my eye this week. It features a Berlin Summit Declaration, signed by what's described as "more than 50 world leading experts" who mostly appear to be academics and economists. They include Dani Rodrik of Harvard University, Mariana Mazzucato of University College London, Adam Tooze of Columbia University, Thomas Piketty of EHESS, Isabella Weber of the University of Massachusetts Amherst, and Ann Pettifor of Prime Economics.

Worried about the plight of liberal democracies, "confronted with a wave of popular distrust in their ability to serve the majority of their citizens and solve the multiple crises that threaten our future," they say trickle-down economics has failed and warn of the danger of armed conflicts, wealth inequality and climate change.

There is ample evidence today that this distrust is not only, but to a large extent, driven by the widely shared experience of a real or perceived loss of control over one’s own livelihood and the trajectory of societal changes. This sense of powerlessness has been triggered by shocks stemming from globalization and technological shifts, now amplified by climate change, AI and the inflation shock. And, decades of poorly managed globalization, overconfidence in the self-regulation of markets and austerity have hollowed out the ability of governments to respond to such crises effectively.

Winning back the people’s trust means rebuilding these capacities. We do not pretend to have definitive answers. However, it seems crucial to re-design or strengthen policies based on some of the fundamental lessons we can draw from what has caused such levels of distrust.

Their suggestions feature in the tweet below and this link.

More than 50 world leading experts call for urgent action against rising popular distrust. Governments should counter the loss of confidence in democracies.

— Forum New Economy (@ForumNewEconomy) May 29, 2024

How?

Read more here:https://t.co/xeLLE19xkH@MazzucatoM @rodrikdani @BrankoMilan @adam_tooze @LauraDTyson @PikettyWIL pic.twitter.com/9T9JNitsMx

3) Are Biden's tariffs on Chinese goods a good thing (at least for the US)?

In an interesting, and perhaps surprising Slate article, Zachary Carter suggests US President Joe Biden's recently announced tariffs on electric vehicles, solar panels, semiconductors, and high-capacity batteries made in China are a good idea. It's the latest round in rising tensions over recent years between the two global economic behemoths.

Carter says "only" about US$18 billion worth of goods are covered by the tariffs, but the dollar amounts don’t convey the ambition of the tariffs. The US doesn’t import much in the way of green technology from China now as the sector is a fledgling one. The point of Biden’s policy is to make sure the US never imports much of this stuff from China. Here's Carter;

Contrary to the declamations from some of Biden’s ostensible allies, this is almost certainly good news for both the climate and the global economy. Biden appears to be learning the right lessons from an ultimately—gulp—successful Trump initiative. His new tariffs are indeed an affront to the conventional economic wisdom of the Obama era, but they are not a leap into the dark. They instead return U.S. economic policy to an intellectual tradition dating back to Alexander Hamilton—one that seeks to uphold the ideals of international reciprocity advanced by Adam Smith while adapting to the political complexities inherent to global exchange.

Avid readers of the business press may remember the Trump tariffs as, allegedly, the worst idea since 1680. By raising import duties on steel, aluminum, and a host of products manufactured in China, Trump was risking a recession, causing a recession, triggering a recession, and maybe producing a recession. Free-marketeers and ultra-neoliberals weren’t alone in leveling these accusations. Progressive economist, Nobel laureate, and all-around swell guy Joseph Stiglitz called the Trump tariffs “a very dangerous precedent,” singling out Trump’s tariffs against Chinese solar panels as a “job destroyer” that would hurt the climate.

With the benefit of being six years on, we can conclude that these people were wrong. The Trump tariffs created some costs for the global economy, but prophecies of inflation, recession, and job destruction were never fulfilled. Prices in a few sectors—washing machines, steel, aluminum—rose for a few months, and then fell. The United States preserved some long-term industrial capacity in exchange for a bit of short-term pricing friction.

Sound economic policy is about making the best of a strange, cruel world, and tariffs—like any other tax—can be either useful or destructive, depending on how they are deployed. If your only economic aim is to reduce consumer prices over the next six months, then tariffs aren’t a great place to start. But if you have broader objectives—say, national security, technological innovation, economic development, or addressing a climate emergency—then the payoff from tariffs can be well worth the price. Tariffs can even improve basic economic efficiency if they’re used judiciously to combat other problems in the global economy.

4) Goldman Sachs & Wall Street’s buzziest asset class.

There has been a lot of talk and hype in US investment circles over recent months about private credit. What is it? According to Investopedia this is how it works;

In the private credit market, investors make loans to businesses and sometimes individuals who may have trouble accessing credit from banks or the public market. Because there is often a heightened risk that the borrower may be unable to repay the loan, private credit investors can collect higher interest rates than they would earn on bonds or other debt investments.

Investment banks are into private credit. And it's always worth keeping an eye on what they're up to. Especially if you remember investment banks' pretty successful attempt at blowing up the banking system in 2007-08 in what became known as the Global Financial Crisis.

Bloomberg reports Goldman Sachs, known by some as a vampire squid, is very keen on private credit. Bloomberg's Sridhar Natarajan describes private credit as; "Wall Street’s buzziest asset class." He says private credit is; "helping the pivot from proprietary bets [when a firm trades with its own money seeking profit for itself]," with Goldman Sachs targeting US$300 billion of credit assets in this area within five years.

The firm just closed the latest iteration of its direct-lending fund, drumming up firepower that includes fresh capital, borrowed funds and co-investments. That along with separately managed accounts will be put to use making more directly negotiated senior loans.

For money managers looking to expand, private credit has become one of their favorite calling cards. For Goldman, it takes on added importance, as it needs to prove it can rapidly raise mountains of money from outside investors, seeking steady fees over the big bursts of revenue once generated by wagering its own money.

Marc Nachmann, in charge of Goldman’s money-management operations, has been logging flight hours to reel in cash around the globe — from pension funds and insurance companies to sovereign wealth funds.

“I’ll go anywhere in the world where people want to talk to me,” Nachmann said in an interview. “They all view this as a super interesting asset class. When you go back 10 years, none of them had big allocations to direct lending.”

Other investment banks are into private credit too.

JPMorgan Chase & Co. has earmarked more than $10 billion of the firm’s balance sheet for direct lending and is trying to put together a partnership with asset managers to join it in private credit deals. Meanwhile, its asset-management unit is on the hunt to acquire a firm that operates in the space.

Others, such as Wells Fargo & Co. and Barclays Plc, have also formed tie-ups hoping to originate deals that their partners can take on.

The International Monetary Fund recently said the private credit market, which topped US$2.1 trillion globally last year in assets and committed capital, warrants closer watch. It's hard to disagree.

“The last 10 years have been a very benign environment, you didn’t see much dispersion in people’s returns on credit because everything kind of worked,” Nachmann said. “It’ll be more interesting going forward.”

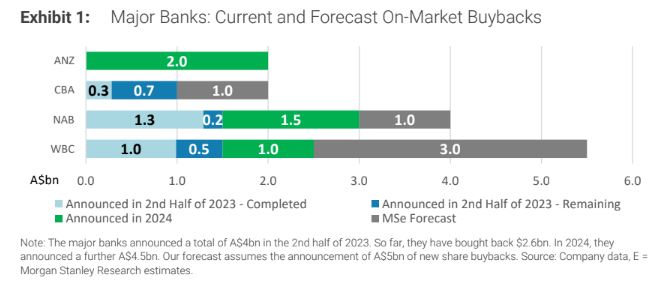

5) Chunky bank share buybacks & dividends.

I've recently written a couple of articles about, shall we say, the financial strength of New Zealand's big four banks. The first was on how two of the big four paid interim dividends bigger than their interim profit. And the second was on what I believe was ANZ's most profitable quarter ever.

The four are, of course, subsidiaries of Australia's big four. The Aussie banks are listed on the Australian Securities Exchange and just can't stop paying dividends and buying back their own shares. Morgan Stanley analysts, led by Richard Wiles, are picking another A$5 billion of share buybacks from the four over the coming two years.

Given healthy capital ratios and relatively modest loan growth prospects, we believe the major banks will announce another ~A$5bn of share buybacks over the next two years.

Share buybacks, like dividends, are a way to return capital to shareholders. Shareholders can sell shares back to the company for cash, sometimes at a premium. However, they're not universally endorsed. The late Brian Gaynor pointed out;

A number of studies have argued that buybacks are more about the interests of senior executives than the listed companies. The highest paid executives in the United States often received more than 50 per cent of their compensation in shares, share options or share awards.

Meanwhile, in its recent interim results the Westpac Banking Corporation "deployed the full suite of capital management tools" with a special dividend, a further share buyback and an increase to its ordinary dividend. Here's Morgan Stanley again;

Given its proforma Common Equity Tier 1 [capital] ratio of 12.2% and excess franking credits, we forecast Westpac to declare further special dividends of 15c at each of its 2H24 and 1H25 results and announce A$3bn of buybacks over the next two years.

And the dividends should keep coming too. It always seems to be a good time to be a big bank shareholder.

The average major bank [dividend] payout ratio was ~71% in FY23, but we expect it to increase to ~75% this year. In fact, payout ratios are likely to be near the top-end of the target range at each of the major banks.

23 Comments

Most people would not know this:

Copper used to be the prime material that power lines were made of. (Not just earthing, the overhead power cables themselves).

Now, most if not all, is aluminium. (Earthing is still copper). Aluminium is not as good a conductor, but is cheaper even though more volume of it is required to carry the same current.

If a fault was to occur when people are stealing the earthing copper, they would get fried. (Either a fault caused by say a car hitting a power pole, or a fault caused by themselves).

Also China uses nearly 60% of the worlds copper production and 30% is used in building and construction so what is happening in there is also very important to watch regarding demand.

Good choices Gareth. Reading them all together provides a clear picture of two worlds...

The real world where people want clean tech, good jobs, air they can breathe, greater equity, an end to rentierism driven by market power and poor regulation / tax policy. This is the world of interest to the group of progressive economists that signed the declaration in Berlin. A group that includes precisely zero NZ economists (who all seem stuck in an econ 101 lecture in the 1980s).

This real world is getting smothered by the financial world where people gamble on layers of derivatives and financial instruments products that are several steps removed from the real world. This world gives us

- Blackrock or JP Morgan investing in NZ infrastructure in 2026 - demanding a rate of return of 10%, and then achieving 15% by easily screwing over ill-equipped and inexperienced negotiators.

- Continued price shocks across commodities as short-term capacity issues and price rises are amplified and prolonged by gambling, hedging, and traders' algorithms. The inflation this will sustain will be tackled very seriously by, errrm, increasing business costs and making mortgagors poorer.

- A reliance on ever increasing private debt that funds (a) the inflation of housing bubbles, and then (b) endless expansion of private savings concentrated in the holdings of the top few per cent (see bank share buybacks for eg)

- A belief (the biggest of cons) that building huge portfolios of shares, equity and financial instruments is the very bestest preparation for an uncertain future; as if somehow the nurses, doctors, infrastructure, carers, food etc will just appear with a wave of the invisible hand.

- Govts trying to be small and austere but just getting bigger and bigger as they have to tax and spend more and more to prevent an increasing proportion of the population starving or living in tents.

Well said.

#2 resonated with me; Mazzucato gets closer than most.

Gareth

Interesting article regarding private credit

On May 31st Canada,s ninepoint partners halted all cash payouts on 3 credit funds

They said this was a temporary measure to preserve cash

Unit holders with about C$2 Billion won’t be able to receive cash payouts

The article says that this is the lates lender to put a squeeze on investors in the private credit market

Earlier this week Jamie Dimon CEO of JP Morgan said he expects problems to emerge in private credit and he worries that there could be hell to pay

Interesting in light of the article where JP Morgan are going to invest $10 Billion in private credit

Does anyone really know in the murky world of big finance

It sounds like you have finally come to the realisation that it is all just gambling with everyone thinking they have the best odds. Humans LOL we never grow up.

Kings birthday honours

https://www.newshub.co.nz/home/entertainment/2024/06/theresa-gattung-jo…

I stopped reading at Theresa Gattung.

I didn't start reading...

she obviously has the contacts, look at the amount of gushing advertising Stuff has given her new dating business.

I was delighted Mary Lee was recognised! And Peter Beck.

In an interesting, and perhaps surprising Slate article, Zachary Carter suggests US President Joe Biden's recently announced tariffs on electric vehicles, solar panels, semiconductors, and high-capacity batteries made in China are a good idea. Indeed.

Ford just reported a massive loss on every electric vehicle it sold

Ford’s electric vehicle unit reported that losses soared in the first quarter to $1.3 billion, or $132,000 for each of the 10,000 vehicles it sold in the first three months of the year, helping to drag down earnings for the company overall.

BYD unveiling a vehicle with ASTONISHING 2000 km range for the price of ... drum roll ... 100,000 yuan ($13,800). This, ladies and gentleman, is true 21st century Fordism! Link

I suggested to the other half we wait until 2026 to replace our present vehicle as MG is planning to introduce its solid state battery then. BYD is having an issue with rust on the vehicles it bought into NZ so I'll be waiting to see if they sort that one out.

Most of my adult life I’ve been told the U.S. can’t do a clean energy transformation because we’d lose out to dirty polluting China. Anyway Link

Investment banks are into private credit. And it's always worth keeping an eye on what they're up to.

Of course they are. But is it really 'private credit'? After the GFC, the pencil pushers in charge of banking regulations decided that they would create a two-tiered system in the US - 8 banks determined to be "Too Big to Fail" and given an unlimited government guarantee on their deposits.JP Morgan leads the pack, holding 16% of all US deposits. There is no risk in depositing to these mega banks. If a TBTF bank fks up, the USG will print the money needed to make sure all depositors get their money back. Essentially, these 8 banks are state-owned enterprises for which the profits are privatised to shareholders, but the losses are socialised to the citizens. In return for this sweetheart deal, these eight banks were given a ton of new rules to follow. These mega banks then spent hundreds of millions of dollars on political campaign donations to help tweak those rules and achieve the most favourable set of restrictions possible.

https://www.federalreserve.gov/supervisionreg/large-institution-supervi…

by Audaxes | 3rd Jan 23, 12:15pm

In that case, the core banks that provided much of the funding for private equity real-estate purchases could be on the hook. That has not happened yet, partly because lightly regulated firms are under less pressure to mark their books to market. Indeed:

Of course, the Fed doesn’t mark to market, nor have banks done so since the early-2009 market low, when the Financial Accounting Standards Board relaxed FAS Rule 157 (which is actually what ended the global financial crisis – by making bank insolvency opaque). Link -Hussman

Essentially, these 8 banks are state-owned enterprises for which the profits are privatised to shareholders

The danger I see here is that they effectively have carte blanche and can take on ann risk level they see fit, knowing they have government backing yet their motive is sheer profit. SOE’s can profit sure, but they have layers of responsibility in often being likes of core infrastructure e.g power companies, rail etc. I see an eventuality where the big 8 cause yet another GFC die to the arrogance and money hunger.

Thought things had calmed down but GameStop surged 20% again after Roaring Kitty reportedly buys $65 million of calls.

The calls have a $20 strike price with an expiration date of June 21st.

Kitty also owns $115 million of GME stock.

Update: Overnight trading of GameStop stock was halted on Robinhood.

Journo Michael Janda chats with ABC News Daily on Australia's hidden mortgage hardship crisis. Fresh research from ASIC Moneysmart today showing 2 in 5 Aussies with debt say they are likely to have trouble making repayments over the next 12 months (that's 5.8 million people).

https://www.abc.net.au/listen/programs/abc-news-daily/australias-hidden…

Oh Yeah its going to go south real quick

The State of Wisconsin has made significant investments in Bitcoin, marking a notable milestone in the adoption of cryptocurrency by institutional investors. According to recent filings with the SEC, the State of Wisconsin Investment Board has purchased a total of $161 million worth of spot Bitcoin ETFs from Grayscale and BlackRock.

https://gizmodo.com/bitcoin-price-pension-etf-wisconsin-sec-liquidity-b…

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.