The following is a report on China's economy and trade opportunities, by MFAT. The original is here.

A strong start to 2024 ...

China’s economic growth outperformed expectations in Q1 2024, with real GDP growing by 5.3% (above market expectations around 4.9%). Strong industrial production, propped up by high external demand and domestic manufacturing investment, was the primary driver. Industrial value-added grew at 6.3% in Q1, although most of that was front-loaded in January and February, with March seeing some deceleration.

Robust performance in manufacturing continued into April and May. Investment in manufacturing was up by 9.6% yoy in the period of Jan-May, and the strongest performing sectors were 3D printing devices, electric vehicles, and integrated circuits, which grew by 36.3% yoy, 33.6% yoy and 17.3% yoy respectively. In May China’ exports rose 7.6% yoy, the fastest pace since April 2023. ASEAN remained the largest destination for Chinese exports, growing 9.7% yoy in May.

It is important to highlight that the headline GDP growth story has been helped by domestic deflation. Accounting for this deflation, nominal GDP growth was lower at 4.2% yoy (compared to real GDP growth of 5.3%). Factory gate prices have been falling over the past 18 months (although it has stabilised in the last few months) and this has helped China’s export competitiveness abroad. Export competitiveness was supported further by a weaker Chinese Yuan.

… but a two-speed economy has emerged

However economic data from the first five months of 2024 points to an economy operating at two speeds: manufacturing activity and exports racing ahead, as domestic consumption and the property market remains stalled. China’s retail growth remained below pre-pandemic projections, 2.3% yoy in April, the slowest rate since 2022, although there was an improvement in May (3.7% yoy). Automobile sales revenue saw a decline of 5.6% yoy in April, due to intense competition in the domestic market. Sales of EVs by volume was up by 4% yoy in April, but lower car prices caused overall sales value to fall by 5.6% yoy. However, in May domestic EV purchases by value picked up with a 4.4% yoy decrease (an improvement on April’s 5.6% drop). Commentators attribute this to consumers making the most of government subsidies for replacing old cars for newer models.

The property sector downturn continued, with property sales declining 20.7% yoy in May, after a 22.8% yoy drop in April. Investment in property also fell 10.1% yoy in the year to May. Looking at commercial property, both the total sales and floor space of new commercial building were down 28% yoy and 20% yoy respectively over the January – May period. There is broad consensus amongst analysts that the property sector remains the most significant drag on China’s economic activity.

Tourism: number of trips up; spend per person down

During the Dragon Boat Festival three-day weekend (June 8-10) total travel spending performed strongly. According to official data, 110 million domestic trips (in China) were made by Chinese tourists over the holiday period, up 6.3% yoy and 14.6% higher than the same period in 2019. Total consumer spending notched an 8.1% yoy increase and a 2.6% increase on 2019 levels. However, behind the increase in total spending, there has been a drop in individual spend, down 12.3% on 2019 according to Citigroup analysts.

The discrepancy between the increase in number of trips and the drop in per head spending was also evident during other Chinese holidays earlier in the year (e.g. Spring Festival in February and Labour Day in May). Analysts have attributed this to the changing behaviour of Chinese tourists, who are now opting for shorter and cheaper trips, amid more gloomy economic conditions.

Incremental shift away from deflation

China’s inflation has ticked upwards in the month of May to 0.3%, the third consecutive monthly increase, indicating a move away from deflation. The low price of pork (which plays a significant role in calculating China’s CPI), is anticipated to increase over the short-to-medium term as Chinese farmers limit pork supply for the upcoming season, so this will add further upward pressure to China’s inflation rate. The Producer’s Price Index (PPI) – a measure of the factory gate price of goods – showed that prices fell in the month of May, but the drop was the smallest drop in 2024. Simply put, prices were falling by less and less each month. The improvement was spurred by a rally in major commodity prices and last year’s low base. Analysts have interpreted the increase in inflation (observed in both the CPI and PPI) as a positive sign, but the current national inflation rate of 0.3% remains far below the government target of 3%, so the fight for higher inflation remains ongoing.

Trade friction continues

Geopolitics threatens to dampen Chinese exports as third country concerns over the country’s overcapacity increase. Critics argue China’s industrial policy has supported the creation of significant production capacity in a number of green technologies (namely EVs, solar panels, and batteries). Critics have furthermore argued that China’s overcapacity allows Chinese manufacturers to export their products at prices that undercut existing competitors, and by extension hampers the development (or even threatens the survival) of those industries overseas. China contends that existing competitors should instead focus on improving their competitiveness. Economists point out that many economies export more than they import (e.g. Germany exports 80% of its automobiles, the US 80% of its semiconductors), but what makes China’s overcapacity unique is the absolute scale of China’s trade and production capacity.

In response to these concerns, a number of countries have announced restrictions on Chinese imports. On May 14 the US announced upgraded tariffs on a range of Chinese imports, the highest profile being the increase in tariffs on electric vehicles from 25% to 100%. On June 13, the European Union followed suit with their own tariffs on Chinese EVs of between 17% and 38%, which would add to the existing 10% import duty on foreign-made cars. Most recently, on June 29, Canada’s Ministry of Finance launched a 30-day consultation on the imposition of a surtax on Chinese EVs.

Inbound foreign direct investment remains subdued

China’s inbound foreign direct investment (FDI) fell 27.9% yoy in the year to April 2024 to 360 billion yuan (NZ$80 billion). FDI in April totalled 58.8 billion yuan (NZ$13 billion), the lowest figure since November 2023. A challenging macroeconomic environment, weak domestic consumption, and tense geopolitics are cited by analysts for the drop in FDI.

Policy support for the property sector

On May 17 China’s central government announced a nationwide programme to provide 300 billion yuan (NZ $67 billion) in loans to fund state purchases of unsold homes, and the relaxation of mortgage rules. The 300 billion yuan relending tool allows provincial SOEs to purchase unsold property and repurpose it into social housing. For mortgages, minimum downpayments have been reduced (first-time home mortgages down to 15% from 20%, and second-time home mortgages down to 25% from 30%). Additionally, individual cities are now allowed to set their own mortgage interest rates rather than abiding by the national floor rate (i.e. cities can set their rates lower than the national rate).

These measures aim to reduce the quantity of housing stock on the market as well as stimulate purchases from would-be-buyers. This marks a stronger policy response than the smaller incremental changes introduced over the last six months, which have not stimulated demand for property. Analysts assess that using public money to buy up property should help stabilise property prices and provide much needed liquidity to troubled property developers. In the short period (first two weeks of June) since the policy came into force, new home sales have fallen 36% yoy (based on daily housing sales reported by 26 cities). It remains to be seen whether the new policy settings will be more successful in lifting consumer confidence in property over the medium term, and if not, what additional policy support might look like.

Third Plenum: Setting the economic tone for the next five years

The Third Plenum is a key CPC meeting that sets the economic tone for the next five years, and in the past this political fixture has had considerable historic significance: the Third Plenum in 1987 saw Deng Xiaoping adopt China’s ‘Reform and Opening up’ economic policy; and it was at the Third Plenum in 2013 that Xi Jinping scrapped the One-Child Policy and placed a greater emphasis on national security. Based on recent speeches by President Xi and other senior leaders, analysts contend the upcoming Third Plenum will focus on high tech manufacturing, job creation, and measures to improve the business environment.

New Zealand China trade: Recent trends in key export sectors

NB: the most recent goods trade data available for New Zealand is to April 2024 and for services data is March 2023.

China remains Aotearoa New Zealand’s top trading partner, with two-way goods and services trade totalling NZ$38 billion in the year ending December 2023. In the March 2024 quarter New Zealand exported NZ$5.34 billion of total goods and services to China. This represented 21.6% of all New Zealand exports of total goods and services in this time period.

The following sections of this report look at the performance of key sectors during the first 3-4 months of 2024 compared to previous years.

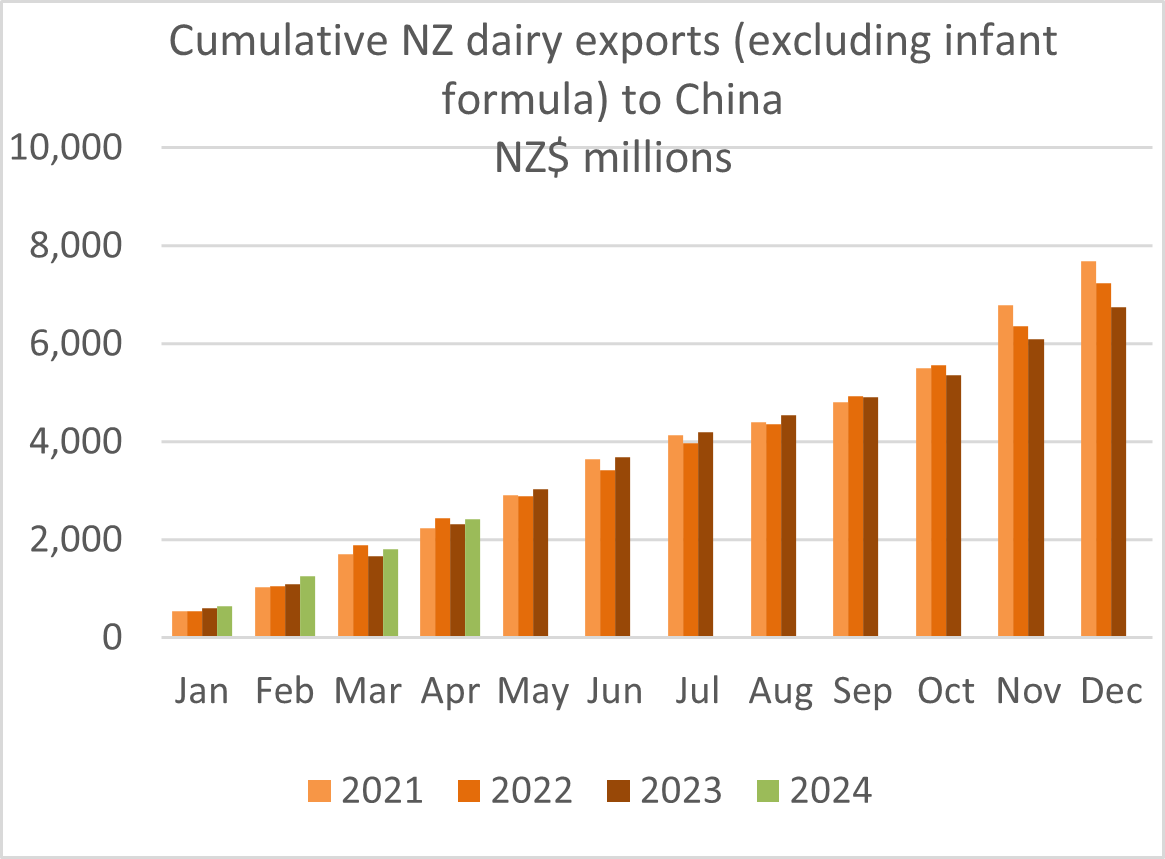

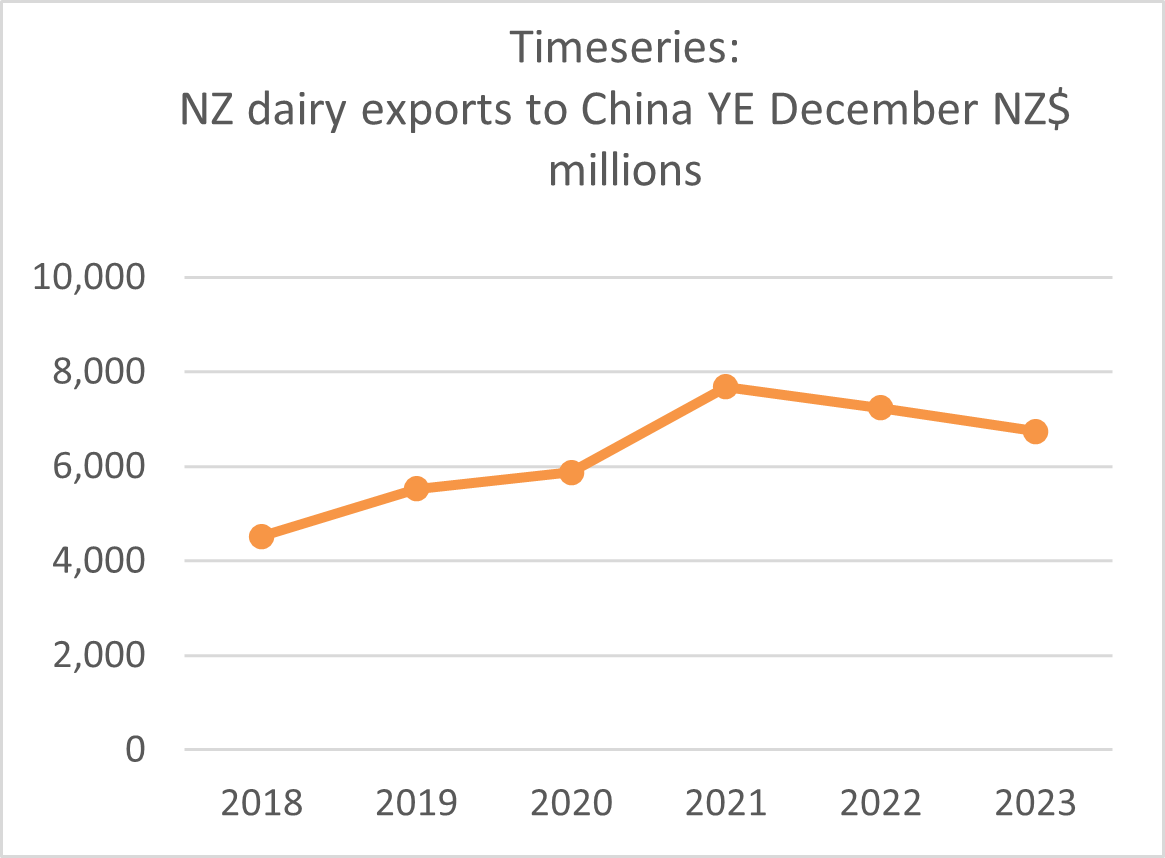

Dairy (excluding infant formula)

The value of New Zealand’s dairy exports to China in the first 4 months of 2024 was NZ$2.4 billion, up 3% on the equivalent period in 2023. This can be partially attributed to the ending of the remaining tariffs on milk powder on 1 January (per New Zealand’s Free Trade Agreement with China).

At the same time, there were a number of factors that weakened dairy export revenue. These included tepid consumer demand in China, which placed significant downward pressure on global dairy prices; a reduction in New Zealand’s total dairy export volumes in the 2023/24 season due to a decline in the size of the New Zealand dairy herd, strong export growth to the US, and high input costs.The current El Niño in New Zealand is likely to also contribute to a decline in milk production through unfavourable weather conditions. More broadly, there has been a 12% reduction in China’s total imports of dairy in the YE April 2024.

Taken together, 3% yoy growth year to date April shows the relative resilience of New Zealand dairy exports and savvy business decisions of some firms to concentrate on higher value sales channel (e.g. food services and bakery), and less so on retail channels.

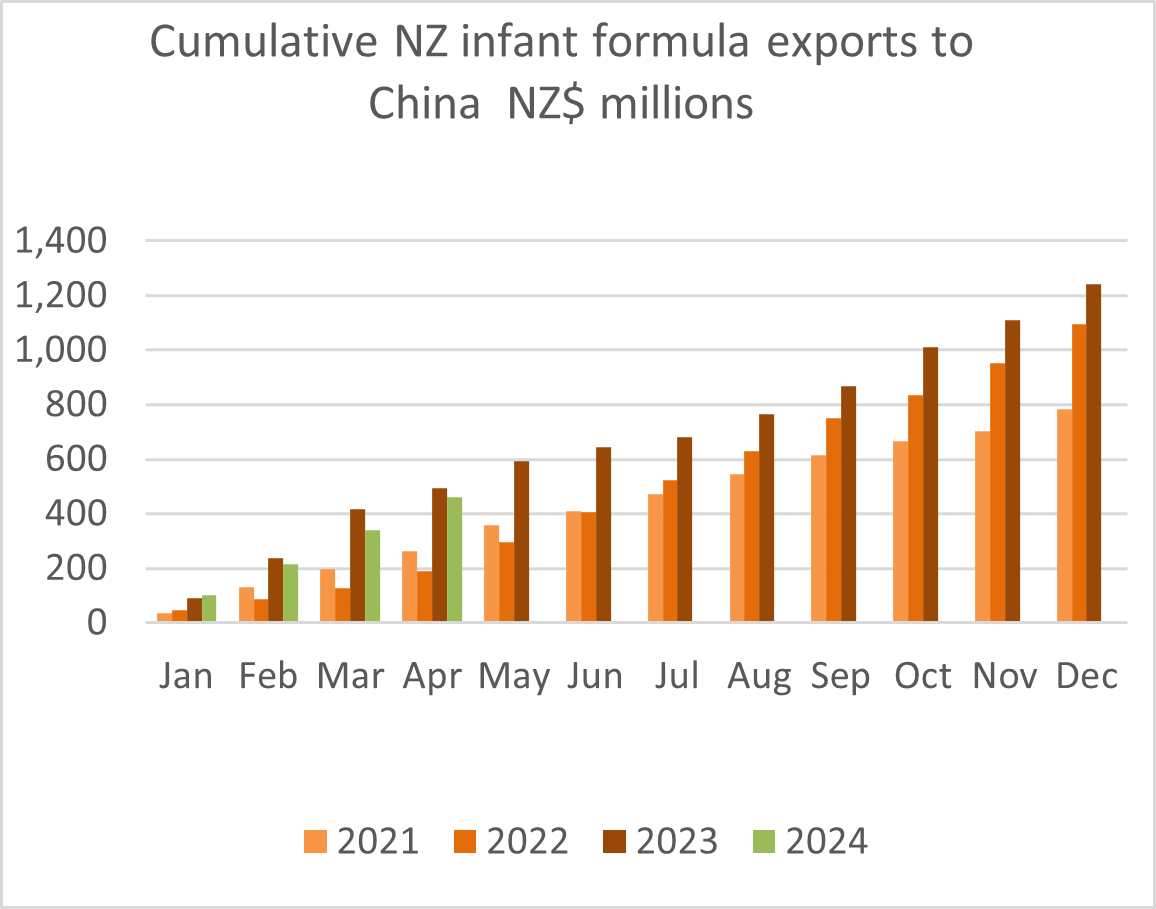

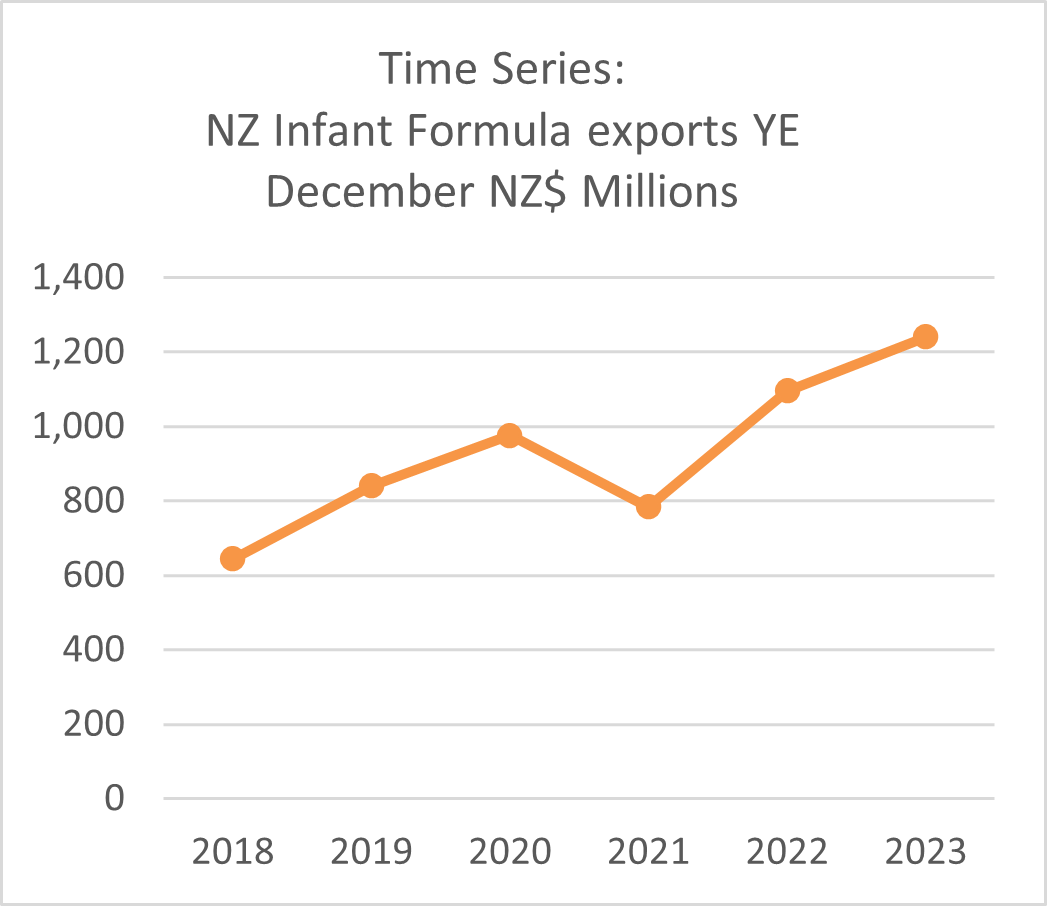

Infant formula

In the year to date April, New Zealand’s infant formula exports to China were NZ$410 million, a nearly 17% decrease on the same period last year. However, the drop comes against a high base in 2023 when New Zealand companies were fast out of the gates meeting China’s new infant formula registration requirements. The increase in China’s total imports of infant formula from competitors, show they have now caught up. Trade data also points to an 31% reduction in China’s total import of infant formula in YE April 2024, the drop in total imports points both to the growing trust in local brands and China’s low birth rate.

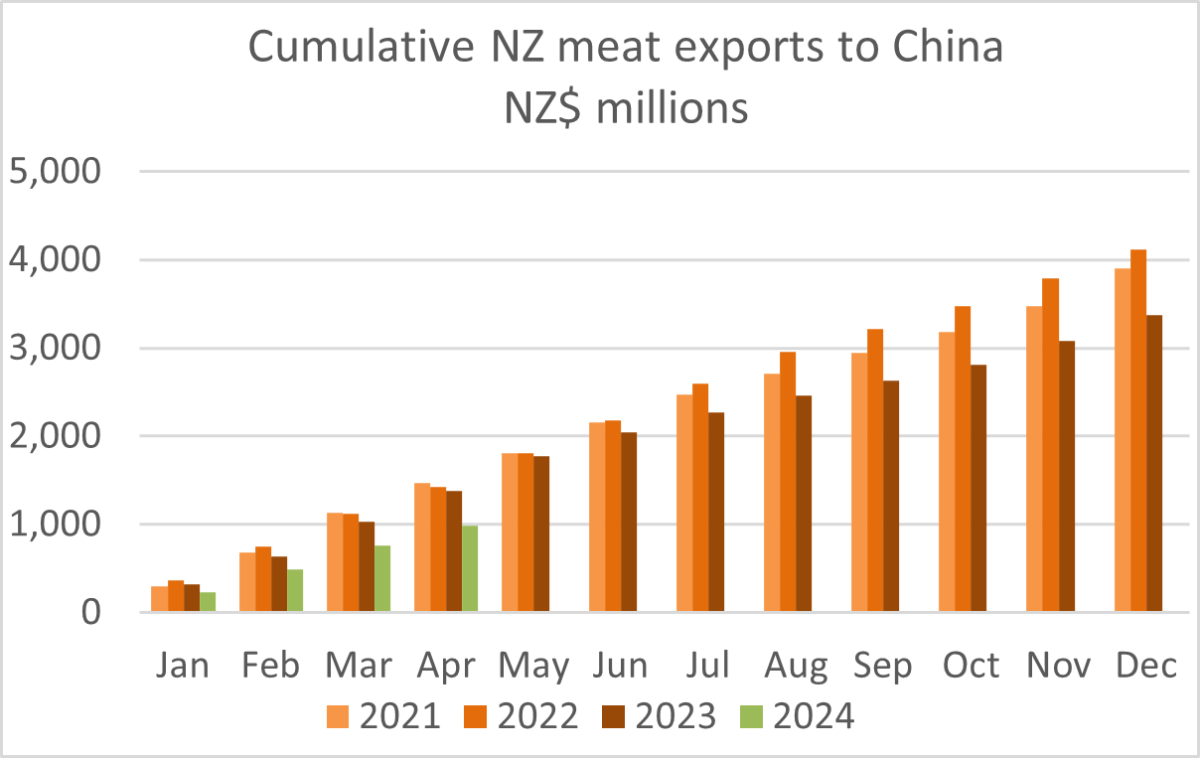

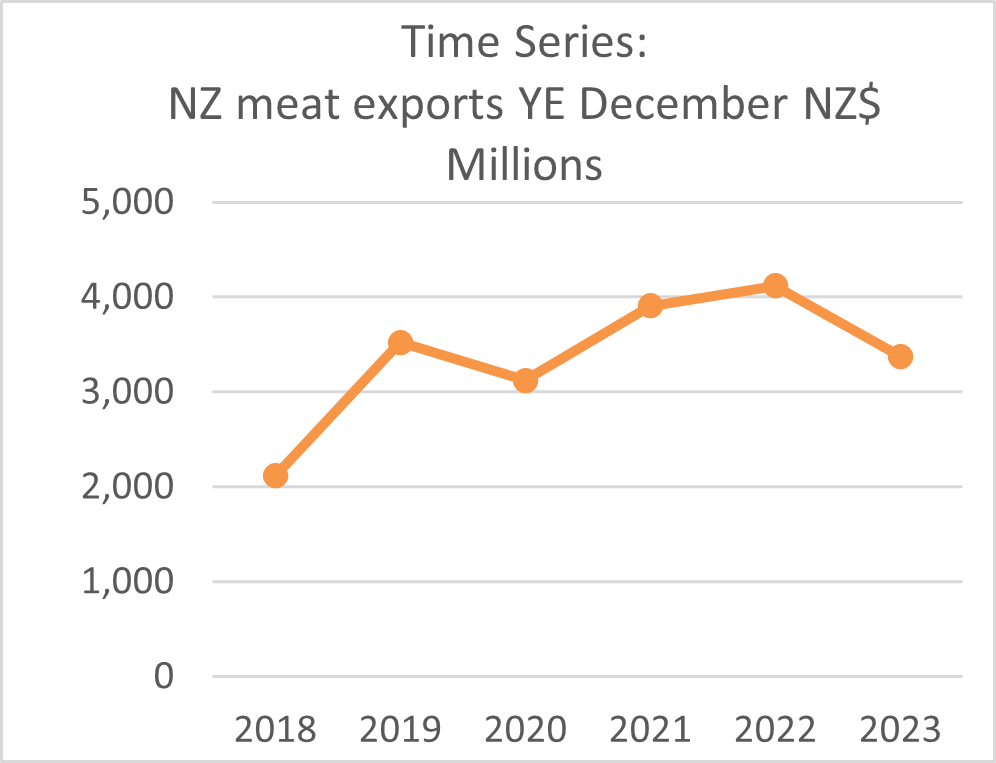

Meat

Meat exports to China in the 4 months to April 2024 were NZ$985 million, down almost 29% on the year prior. The drop can be attributed to a number of factors: the high level of inventory held by Chinese meat importers means less foreign meat products are being imported; as this inventory reaches its ‘sale by date’ there is more supply entering the market; China also has released some of its strategic pork reserves onto the market, which is pushing down the price of meat ; and there is tough competition from other meat exporters (e.g. Brazil, Australia, Argentina, and the US). Moreover, this is against a backdrop of weak overall domestic consumption. However, China has reduced its pork production in the upcoming season to recalibrate supply closer to demand. The number of piglets born in Q1 2024 have dropped by 4.9% yoy. This should see pork prices – and meat prices by extension – increase in China over the medium term (Q2 and Q3 of 2024).

However, this drop in export revenue has been offset by growth in NZ meat export to the US market. In the month of April, exports to the US rose by 14% yoy to NZ$231 million in April, making it the largest market for meat exports for the month. Given the low price of meat in China, it is likely NZ commodity traders have followed the price, opting for the US market with higher meat prices. The same can be said with the Canada market, which had a large increase in meat exports in April, up 121% yoy from $14 to NZ$31 million.

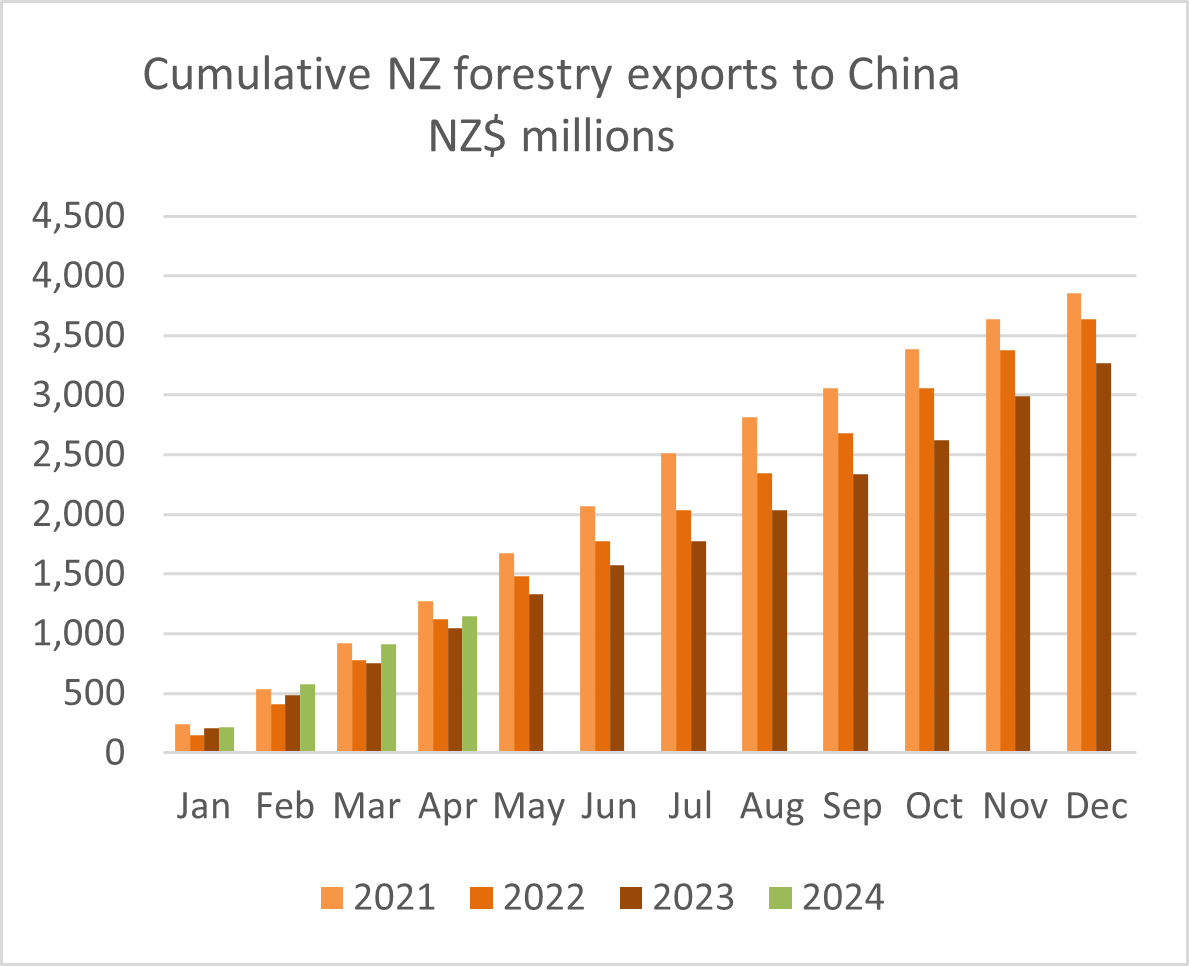

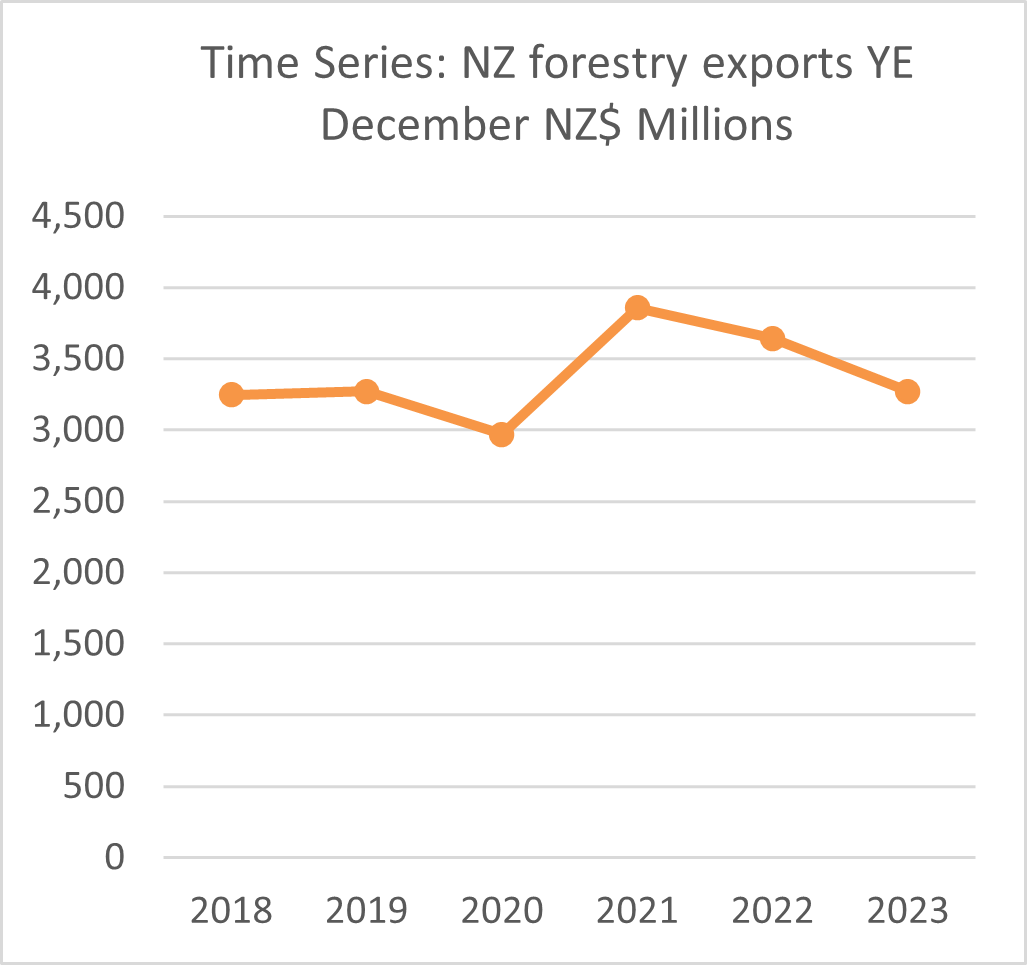

Forestry/wood

New Zealand’s forestry and wood product exports to China increased by around 8% in the year to April 2024, to NZ$1.1 billion, when compared with the same period a year prior. New Zealand’s trade in forestry and wood products is dominated by shipments of raw softwood logs, approximately 89% of all softwood logs are exported to the China market and New Zealand is China’s largest supplier.

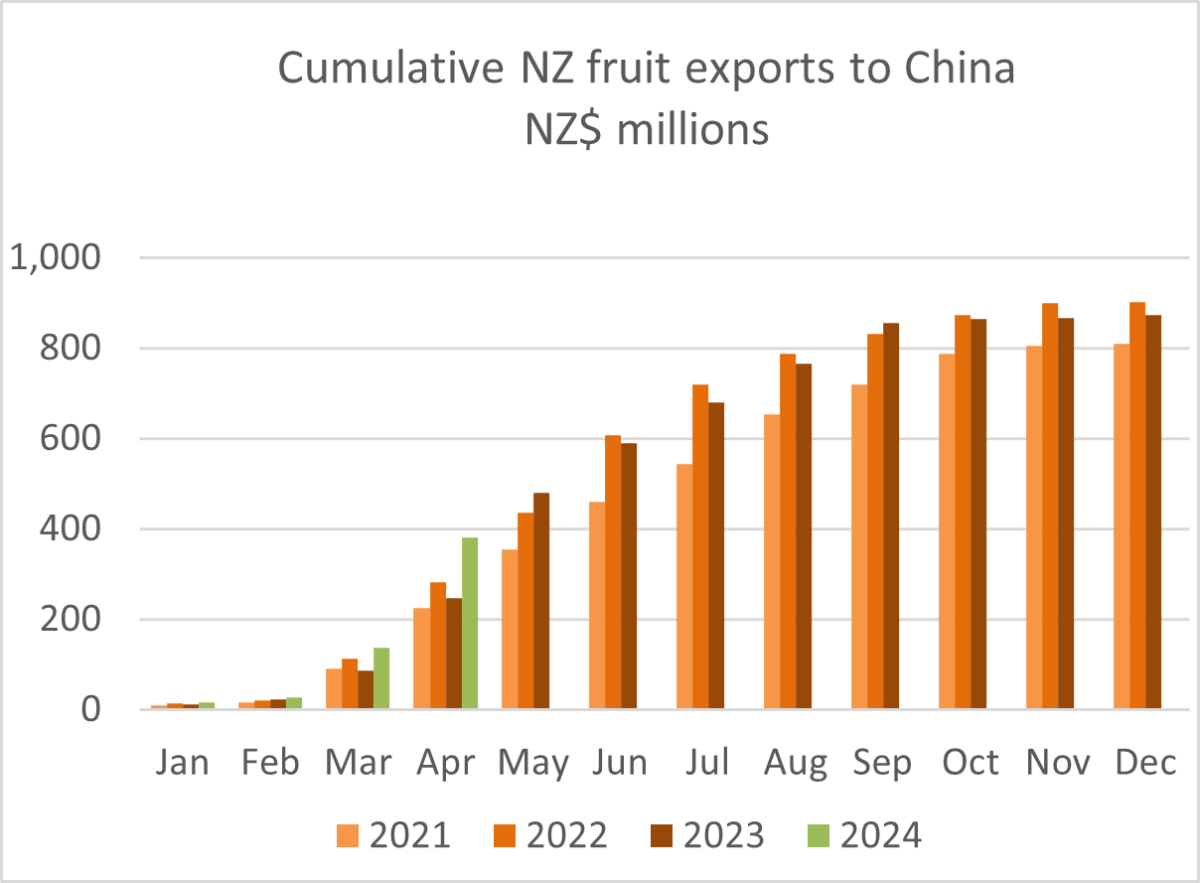

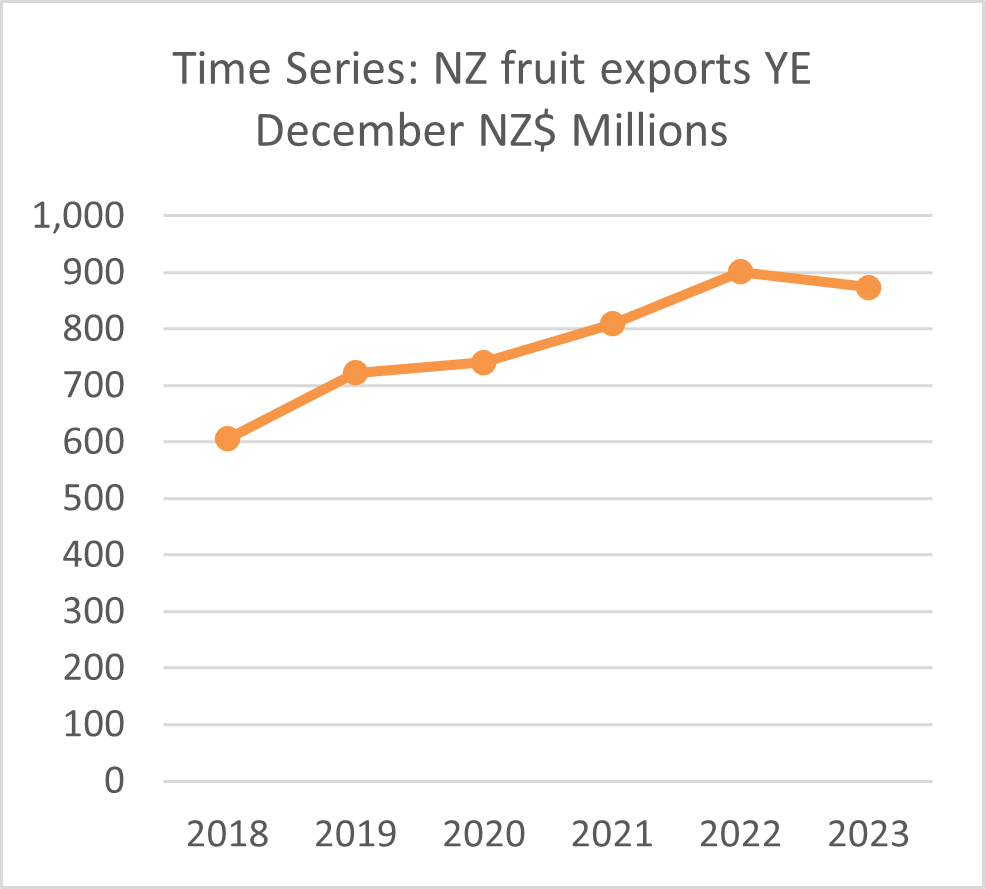

Fruit

New Zealand fruit exports to China totalled NZ$378 million in the 4 months to April 2024, a 53% yoy increase on the same period last year. The increase is a result of the latest shipment of Zespri’s kiwifruit to China. Following two difficult growing seasons growers report a much bigger crop and of high quality this season. A significant amount of that crop will be directed to the China market, and it is likely the fruit category of exports to China will continue to perform well in the coming months. Apple and pear growers have grown a high-quality crop and hope for this to translate to a high price point in export markets, including China. Envy apples have had a later harvest, so should be reflected in export figures in the coming months. The year-on-year result is also buoyed by the gradual recovery of orchards from the impacts of Cyclone Gabrielle that damaged key growing areas in February in 2023.

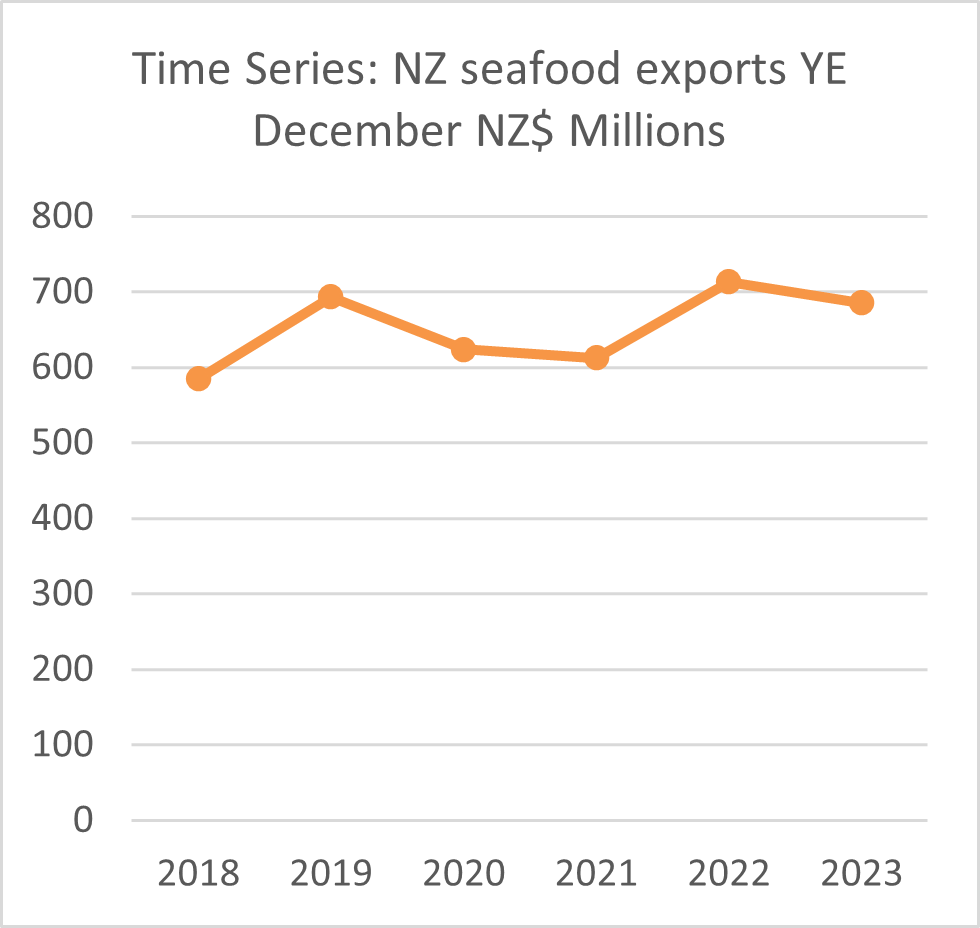

Seafood

Seafood exports to China were up 14% in the first 4 months to April 2024 compared with a year prior, totalling NZ$231 million. New Zealand’s seafood exports are dominated by rock lobster. This growth is driven by high demand for seafood, record high rock lobster prices, and tight global supply (China’s ban on Australian rock lobster remains in place). New Zealand ranks 11th in terms of source markets for China’s seafood imports.

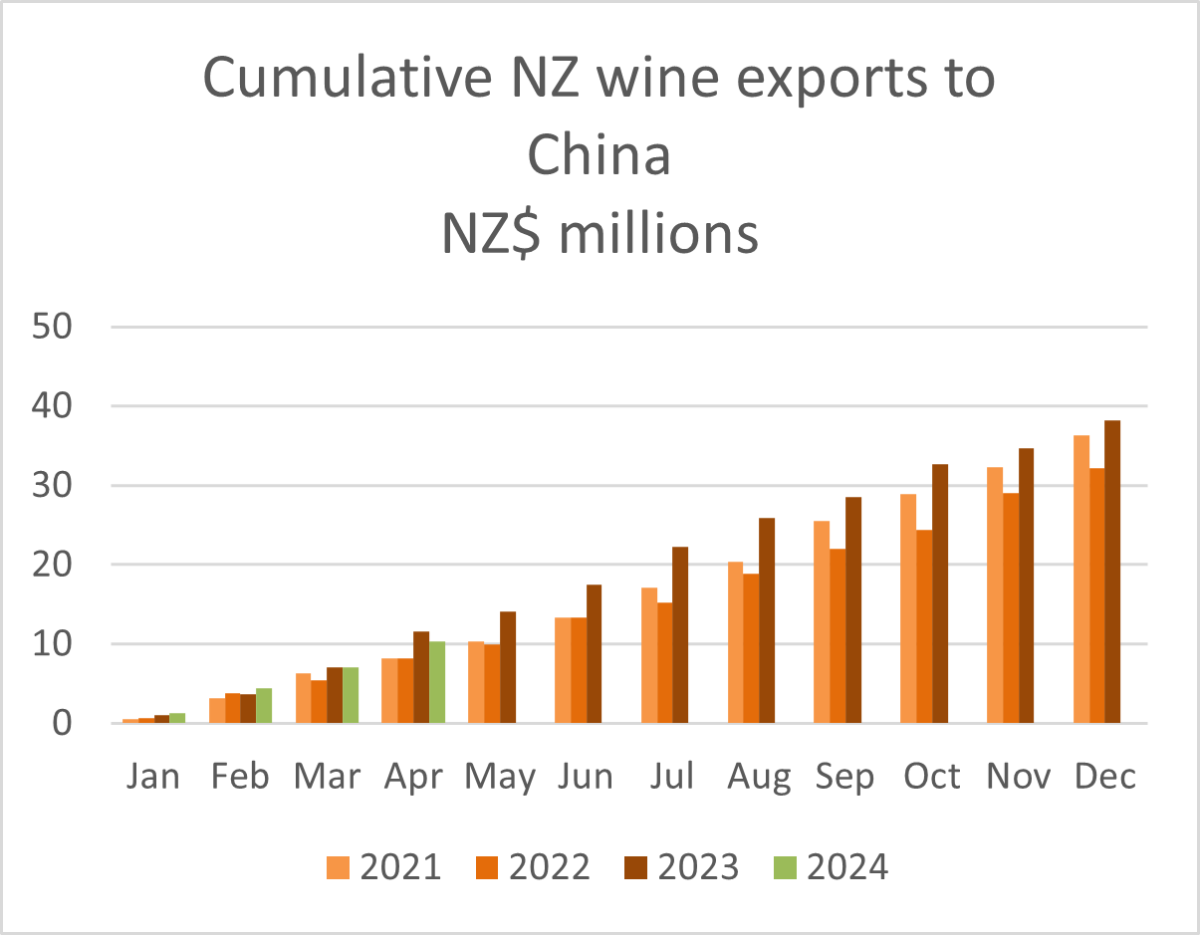

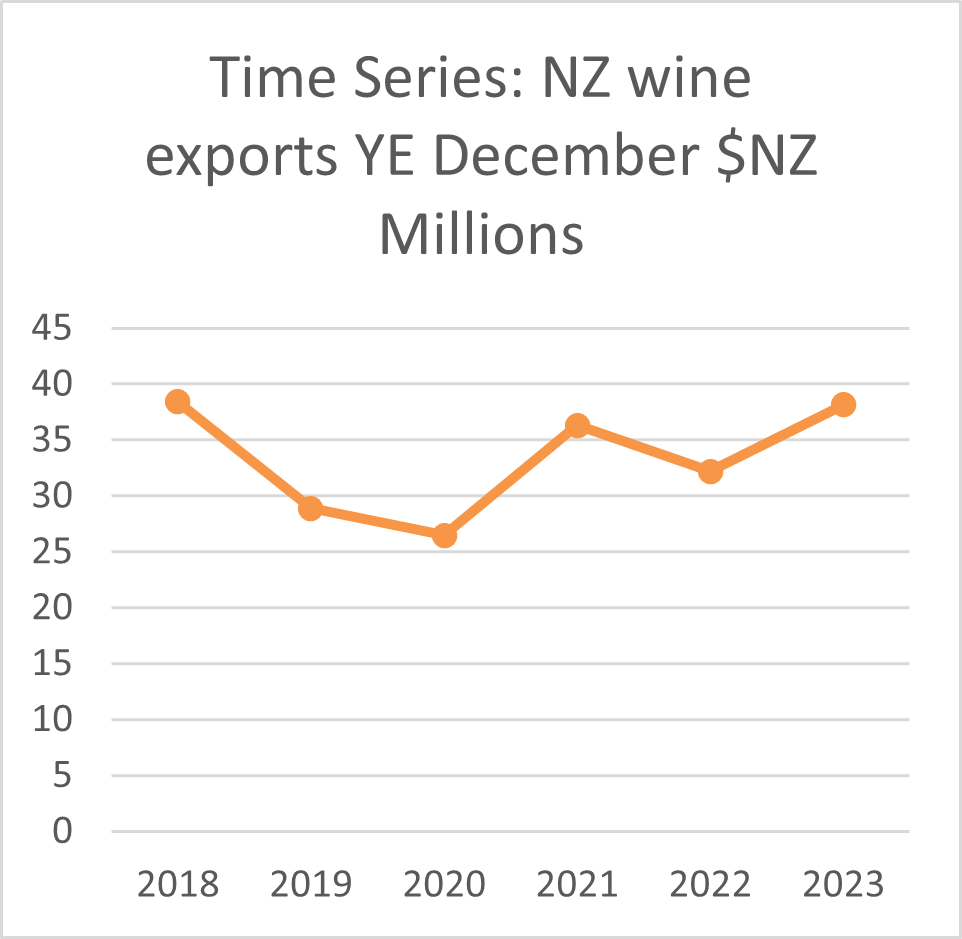

Wine

New Zealand wine exports to China totalled NZ$10 million in the 4 months to April 2024, a decrease of 11% compared to the same period last year. Challenges faced by the sector include weak consumer spending and “downgrading” (i.e. opting for cheaper alternatives).

However, when taking a longer view, exports rose 4% yoy in the year end to April (May 2023-Apr 2024). White wine especially Sauvignon Blanc has driven the growth over this period, with white wine making up 80% of New Zealand’s wine sold to China (up from 60% in 2021). The New Zealand wine industry remains generally confident on market prospects, even amid the resumption of Australian wine imports to China (which are predominantly red wine).

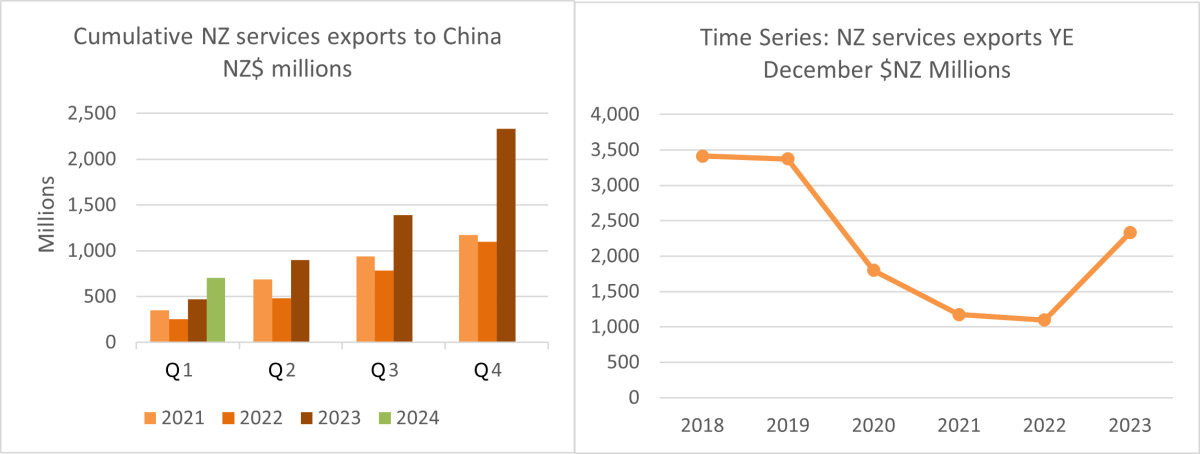

Services

Services exports to China grew 50% yoy the first quarter of 2024 to NZ$ 703 million. This growth has been driven by a strong recovery in tourism, as well as growth in most other service sectors. China was the second strongest tourist market by spend in the January-March period (behind Australia and ahead of the US).

Regular China market updates and other useful resources are available on the NZTE “myNZTE” online platform. Exporters can also sign up for myNZTE for China market information on a number of topics. The Ministry for Primary Industries regularly provides information on requirements [Overseas Market Access Requirements or OMARs (login required) and Importing Countries Phytosanitary Requirements or ICPRs) and For Your Information (FYI) documents, including for China, with guidance on exporting issues relating to animal products (such as meat, seafood, honey, and dairy)], food products, plant products, and wine. MPI also produces regular reporting on New Zealand exports globally in the Situation and Outlook for Primary Industries reports.

[i] Factory gate price describe the price of goods when they leave the factory before any retail profit or additional costs (e.g. transport).

[ii] While the definition of “overcapacity” is debated, the phenomenon of overcapacity can be generally understood as production exceeding demand and rational output levels.

[iii] As the price of pork drops, so does the price of comparable meats, this is because consumers generally prioritise price over a specific type/cut of meat product.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.