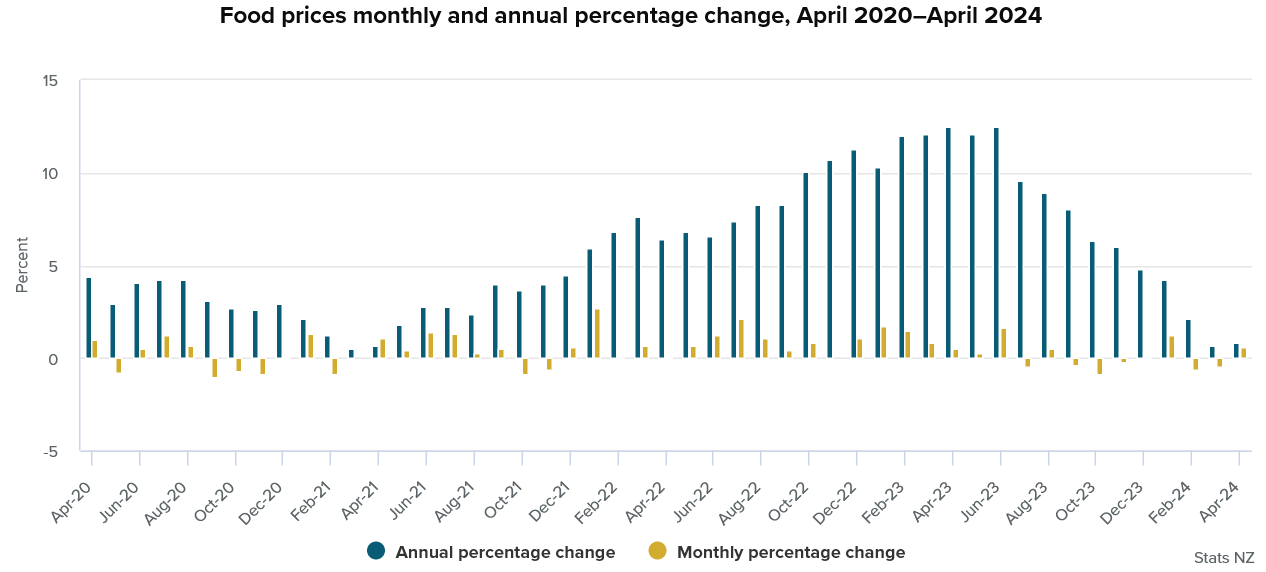

Food prices rose for the first time in three months in April, forced up by higher prices for olive oil, potato crisps and and chocolate blocks.

The olive oil price in April was $18.57 per litre, up some 10.5% on the $16.80 price in March.

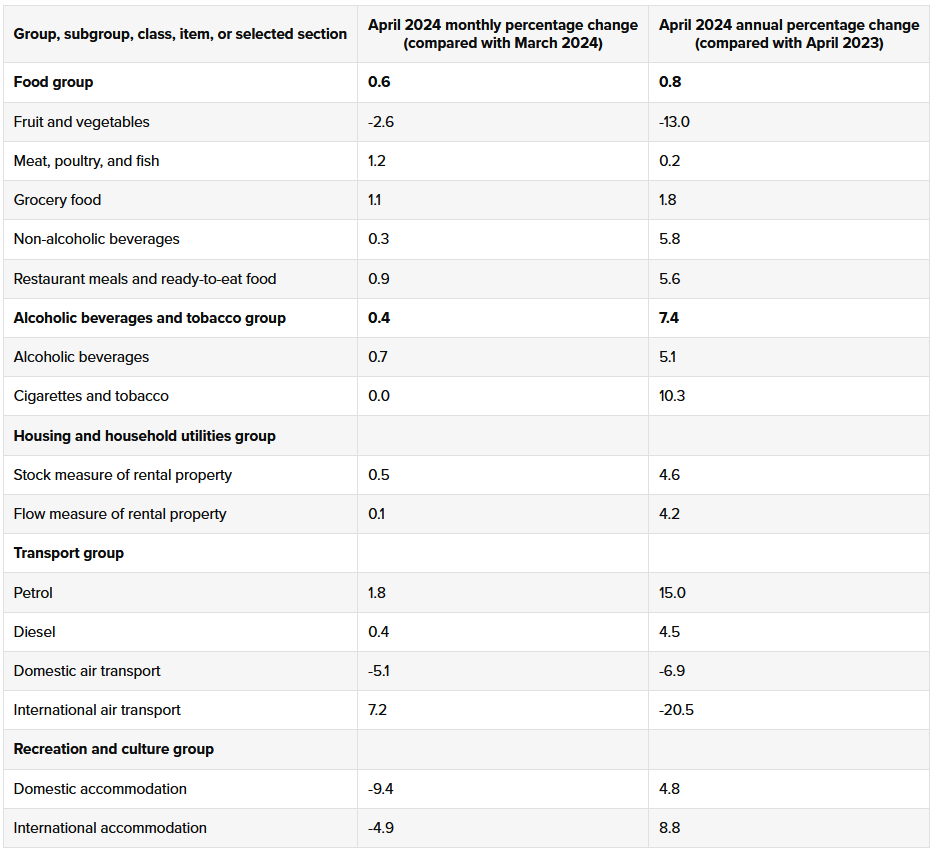

Meanwhile, the ever-volatile international airfares rose by 7.2%, while rental accommodation costs are continuing to rise fairly strongly.

ANZ economist Henry Russell and chief economist Sharon Zollner said while the overall pricing data was "on the stronger side of expectations", the miss was not significant enough to alter their view of the outcome of the June quarter inflation figures (they see a 0.5% quarterly rise and 3.4% annual rate) "and we remain confident that headline inflation will be back within the RBNZ’s 1 - 3% target band in Q3 this year."

ASB senior economist Kim Mundy said consumer prices generally ticked higher in April. Quarterly price rises remain higher than what is required to be consistent with the RBNZ’s 1-3% inflation target, she said.

"At this stage, we continue to expect CPI inflation to fall below 3% by year-end. However, there is a risk that this takes longer than expected, given evidence of stickiness in some of today’s data. Despite consumers doing it tough, there were still sizeable monthly price rises in certain categories," Mundy said.

Statistics NZ said in April food prices rose 0.6%. This followed a 0.5% drop in food prices in March.

On an annual basis, the latest increase brought the overall rise in food prices for the past 12 months up to 0.8% compared with 0.7% as of March.

At the same time a year ago, food prices had increased by some 12.5%.

Discussing the monthly figures, Stats NZ's consumer prices manager James Mitchell said the fruit and vegetables group slightly offset the increased prices, with cheaper prices for kiwifruit, broccoli, and mandarins.

“Stocking up with fruit and vegetables became cheaper for the third consecutive month,” he said.

“At the same time, filling up the fridge and pantry with other food items, and heading out to a cafe or restaurant became more expensive.”

In terms of the annual picture, he said the smaller increase compared with last year was due to cheaper fruit and vegetables, down 13 percent in the 12 months to April 2024, while all other broad food groups increased in price.

“The fall in fruit and vegetable prices, compared with April 2023, reflects prices coming down from highs seen throughout 2023,” Mitchell said.

“Tomato prices were more typical for April – about $3.50 cheaper per kilo than what they were this time last year, while kūmara prices have more than halved since the start of 2024," Mitchell said.

This is all according to the latest monthly release of Selected Price Indexes (SPI) by Stats NZ.

The SPI late last year replaced Stat's NZ’s previous monthly releases for food prices and rents and alongside those monthly indexes, they now also publish indexes for petrol, diesel, alcohol, tobacco, airfares, and accommodation.

Stats NZ's Selected Price Indexes incorporate about 45% of the Consumers Price Index (CPI). The SPI isn't meant to replace the CPI – which still comes out every three months – but is meant to give preview information about inflation.

Economists have found the new SPI information very helpful as it captures quite a lot of the elements in the CPI that are more volatile in nature.

This includes the earlier-mentioned airfares.

As stated higher up, prices for international air transport rose 7.2% in April 2024 compared with March 2024. However, prices for overseas accommodation were down 4.9%.

“Kiwis travelling overseas in April would have experienced higher airfares than those who travelled in March,” said Mitchell.

“On the flip side, the prices for their accommodation were cheaper.”

International air transport prices were 47.7% more expensive than five years ago, in April 2019, while prices for overseas accommodation were 30.8% more expensive over the same time.

In terms of rental costs, Stats NZ said the 'flow' measure of rentals (which is for new tenancies) rose just 0.1% in April. But this is a volatile figure.

The 'stock' measure of existing tenancies showed a 0.5% rise, which was higher than the 0.4% rise in March. The massive surge in migration is helping to fuel the rising rental costs.

The annual rate of increase of stock rentals was 4.6%, same as in March, while the 'flow' increase was 4.2%, down from 5.1% in March.

Rentals make up about 9.5% of the CPI figure, so are very significant and they are continuing to rise at a rate that is higher than the most recent annual CPI figure, which was 4.0%.

Here is the detailed SPI information as supplied by Stats NZ:

41 Comments

Hang on. I thought reinstatement of interest deductibility for landlords was going to flow through to give relief to renters. Timing issue?

Assume a 1-2 year lag for the impact of any changes to flow through. I'm paying my taxes on 50% previous FY deductibility this year.

The trickle down is so slow its evaporating due to climate change.......

The flow has been been re-routed to olive oil, potato crisps and and chocolate.

If landlords could just pass their costs on, rents should have doubled in the last 3 years due to rising interest rates alone.

How sad ....never mind.

Just like how they all cut rents when their interest expenses dropped?

Sounds like a bad financial decision to be a landlord.

If the government were serious about giving relief to renters via reinstatement of interest deductibility, they would have paid out the deducted interest directly to renters, cut out the 'middle man' (as in the landlord). But we all know that was never the intention..

Its called the accommodation supplement. I suppose you support that, either way the landlords will get it one will just be less direct.

Argh, you're so right! Whether the taxpayer money gets handed to the landlord or the renter, either way, it ends up in the landlord's pocket.

Since covid NZ Inc. seems to be run by the big 4 Australian "banksters", the supermarket "duopoly", oil companies "cartel", greedy local and overseas slumlords, overspending gummints (I know what you are thinking but where is National going to get the taxes from? )

If NZ was run like a household, it would be screwed .....hang on ! it's run worse than a household !

Enzud - living beyond its means since ..... fill in your own date.

A household that spends more than it earns (current account deficit) and borrows to buy more unnecessary clutter (housing investments) rather than invest in improving its earning potential (business capital and skill development).

The biggest reason to worry is not the current situation, it's the fact that we're doing nothing to improve our situation; in fact, we're doubling down on those very policy decisions that put us into this situation.

So, we have an increasingly turbulent global economy where prices of key inputs like fuel, freight, cooking oil, grain etc can swing upwards and stay high for months as traders gamble on future prices and wholesalers (literally) pass on the costs of hedging their bets to customers.

Now consider our complex economic system where increases in input prices play through to other prices over time as contracts expire, eventually reaching wages, which then drive higher rents (which then feedback to wages, and so on).

Now remember that *every* episode of inflation in NZ in the last 50 years has results from an imported price shock (generally oil).

Now what weapon would you choose to target price stability in the world that I have just described? The price of money (interest rates)? Really?

Firstly, the price of money is an input cost for businesses... so you are saying that you need to increase business costs to persuade businesses to reduce their prices. Does that sound smart?

Secondly, how do you know whether a sudden hike in an imported price is going to last a month or be sustained for a year? So, when do you use your interest rate weapon? Inevitably you go late, by which time your imported price shock has propagated through your price structure, meaning wages will follow etc.

Thirdly, your weapon is inaccurate and limp, so it takes ages to work. By the time you are crushing demand, the imported price shock has worked its way through to wages and rent, and you are playing catch-up.

Finally, what if you are fighting the wrong enemy - crushing jobs left right and centre will bring wages and rents down eventually, but will it make any real difference to prices in a domestic economy that is not exactly known for its vigorous competition? What if businesses just accept the lower demand, downsize their capacity, and keep their profit margins as they were?

Pertinent post Jfoe. So how would YOU answer your own question:

"Now what weapon would you choose to target price stability in the world that I have just described?"

I'm a broken record on this I know, but in the short-term we need automatic dampening mechanisms on key input prices. The most obvious one is oil (and its various fuel derivatives). Govt could easily vary the existing excise / ETS levy on fuel to smooth out price changes over the medium-term. This could be fiscally neutral and would go a long way to preventing imported price shocks spreading into the wider economy. I would also go or collective wage bargaining (Danish model) and I would also cap rent rises at 3% per year (around their average increase). Again this would smooth the shocks out and stop rents chasing wages when we do have spikes (the rent - wage price spiral is real).

In the medium-term, we need to reduce our exposure to volatile commodity prices - by increasing our self-sufficiency (get off oil and gas). Same with housing - the market will simply not provide enough of it to bring prices down (imho).

This all seems to make sound sense. Wonder though whether fuel levy adjustments to dampen price increases to shield businesses and consumers would deincentivize the transition to energy self-sufficiency/renewables. Meaning your short-term solution might reduce the feasibility of your medium-term solution.

Probably not. Electricity is rapidly becoming the cheapest source of energy for applications that can use either electricity or fossil fuels. Still some way to go though. And the 'storage' issues with electrical energy remains an issue (although gravity looks like a promising solution ;-).

"Govt could easily vary the existing excise / ETS levy on fuel to smooth out price changes over the medium-term. "

Golly. That sounds like an excellent solution. ;-)

Lol. Is the search function on interest.co.nz sophisticated enough to work out who said it first?!

No. But google is. :-) ... But who cares. Those that came up producer boards should get the credit. What's nice is to see is ideas being picked up by others. Lamenting the broken status quo achieves little while getting potential solutions on the radar is what's important.

Price increases are just around the corner kicking in Q3 24 in some big ticket items. Insurance premiums, energy prices (gas shortfall and weak electricity supply this winter) and council rates all going up in double digits.

EV charging, astronomical AI demands and general migration to electric charging for everything .. coupled with issues with the main fossil fuel producers (wars mainly) means energy prices will just keep rising and pushing inflation up.

Insurance premiums, energy prices (gas shortfall and weak electricity supply this winter) and council rates all going up in double digits."

Higher interest rates will reduce these prices.... NOT !!!

Can't have it both ways yvil ...hoping interest rates will go down, just so to reduce your mortgage costs.

You're "shortcutting" the system - interest rates should actually be at least 3% above inflation, to keep up with costs rising, that are totally out of NZ's control.

So we destroy our domestic economy to cope with imported price shocks? What kind of crazy is that?

Jfoe ....this "debt" based economy is destined for a big fall, not only here but around the western world.

But we know what happens when interest rates drop ......the NZD falls and that means the price of oil will go up anyway...so more inflation, furthering destroying the domestic economy.

You will probably have a better idea than me, but what % of NZ's gross GDP is being used for interest payments on the debt ?

You will probably have a better idea than me, but what % of NZ's gross GDP is being used for interest payments on the debt ?

Jfoe has previously highlighted how debt servicing inflation is a large contributor to overall inflation.

As to your question re debt servicing to GDP, as a comparative benchmark, US interest payments as a proportion of GDP are 2.5%.

The whole world has a debt-based economy - all money is debt, every financial asset is someone else's financial liability. The $20 in my pocket is my asset, but it is Govt's debt. My kid's $30,000 student loan is their debt and a Govt asset. If all debts were paid of tomorrow, all money would basically disappear.

The Crown is a major owner of financial assets, bonds and equity etc; so their net interest payments are less than 0.5% of GDP ($1 - 2bn per year). Sadly, Treasury only publish the gross figure regularly, which, per year, is currently about :

- $2.2bn interest on settlement account balances (bank reserve accounts at RBNZ)

- $4.4bn interest to offshore investors holding Govt bonds

- $1.5bn interest to domestic bond holders

- $2.5bn interest they pay to themselves, which doesn't count (ACC & RBNZ own a stack of Treasury debt)

Households are net beneficiaries of higher interest rates - they get more interest income than they pay out (noting that this includes dividends from fixed-return assets). Obviously this masks the few hundred thousand households (and a fair chunk of landlords) that are getting absolutely murdered by higher rates.

Big losers of higher rates are businesses - currently paying over $14bn per year in interest - that's 3.5% of GDP.

My view on the sustainability of debt is that our private sector debt (households + businesses) is unsustainable. We pumped up private sector debt from 70% of GDP in the 1980s to 150% of GDP in 2009 and it has been broadly steady since (currently a bit over 140%). Private debt at this level means that once interest rates get above inflation / GDP growth, the economy dies a death - there is simply too much money flowing from businesses and mortgagors (spenders) to savers and investors. Our high private debt levels are only sustainable with very low interest rates.

Our high private debt levels are only sustainable with very low interest rates.

Spot on. And this is the reason we need to keep interest rates just high enough to motivate people to change their future habits (borrow less and risk less). And let the economy cool off. HFL will dampen house price rises, reduce energy usage, reduce immigration and lead to a much better longer term economic outcome for NZ (vs dropping rates as a means to grow an economy from cheap money and asset bubbles). Th GDP growth will slow but thats a minor price to pay.

Yes, GDP will stagnate, but the greater price to pay will be skyrocketing unemployment, rapidly rising inequality, and social unrest. Our economy is a consumer economy - when consumption slows, jobs go. when jobs go, things go badly wrong, very quickly. There are more elegant ways to de-leverage than a few years of recession.

Agree. However nobody seems to have any motivation to solve any other way.

The issue with unemployment and social unrest for this dip may be far worse with autonomous vehicles and AI removing jobs at the same time demand cools. And central govt won't have the ammo to assist.

Jfoe appreciate the reply ....still can't see how reducing interest rates, wouldn't devalue the NZD ?

"Can't have it both ways yvil ...hoping interest rates will go down, just so to reduce your mortgage costs."

Thanks for your concern CH, but my mortgage cost is at 2.89%, so no, I'm not hoping to "reduce it". LOL

Well Yvil ....a coin has 2 sides ....my bank term deposits are earning 6% gross....while in the States I was getting a 12 to 15% gross return on the rental properties (if you were starting out as a NZ residential property investor now, you would have to have rocks in ya head !)

So you keep paying the banks and I'll get them to pay me .......while your NZ property assets continue to decrease in value.

You're still off the mark CH, I pay the bank 2.89% for my mortgage and they pay me 6% for my deposits... Sorry it's not the bad news you were hoping for.

Why have term deposits, when gross interest doesn't even cover inflation ?

Disclaimer: with my term deposits, I also have a crypto portfolio currently returning 70% pa - nuff said.

The obvious way for renters to be able to make renting more affordable, is to allow renters to deduct the rent they pay off their taxable income up to a certain level.

This is not a new idea, as all businesses can deduct 100% of their that rent off their taxable income, so why not renters?

The argument that renters are not a business is just a customary notion, and not based on logic.

Agree. Apply the same to home owners with their mortgages. What a hit to the tax receipts that would be, and a huge incentive for Governments to keep rents and house prices/mortgages tame.

Sounds inflationary.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.