Here's our summary of key economic events overnight that affect New Zealand, with news there are some early signs global households may be starting to feel they are owing too much debt. Any pullback from that will induce a 'balance sheet recession', that during stagflation, might be very hard to control.

But first up today, the latest dairy auction has come in with something of a disappointment. Overall prices rose as expected, but the +1.5% gain in USD terms wasn't as strong as the derivatives market had priced in. Chinese buyers were noticed by their relative absence. On the positive side, it did end a run of five consecutive declines. In NZD terms however, that small rise evaporated. Volumes were low so the direct impact was not great, but the flow-through to wider contract pricing based on these auctions will be noticed. Maybe the impact on farmgate payout prices won't be strong either given where we are in the season, but analysts will be underwhelmed by this result.

In the US, logistics stress as measured by the LMI index seems to be easing. The rise in freight costs seems to be tailing off, but warehouse capacity is getting tighter and so warehousing costs are rising faster. It's a mixed bag. Higher inventory levels in response to the extended supply-chain uncertainties appear to be embedded now.

However, at least one very large American retailer has announced plans to shrink their embedded high inventories. If that spreads, suppliers may face a drought of orders.

American retail activity still appears to be strong, according to last week's nationwide survey.

American exports of both goods and services rose in April and their trade deficit reduced. Even if these shifts were small, they were unexpected and noticed. In fact, their deficit with China decreased by -US$8.5 bln to just under US$35 bln, the most in seven years. Falling imports from pandemic-restricted Chinese ports drove the April changes.

The US Treasury had another very well supported bond auction earlier this morning, for their three year Note. The median yield rose to 2.87% from 2.74% at the prior equivalent event a month ago.

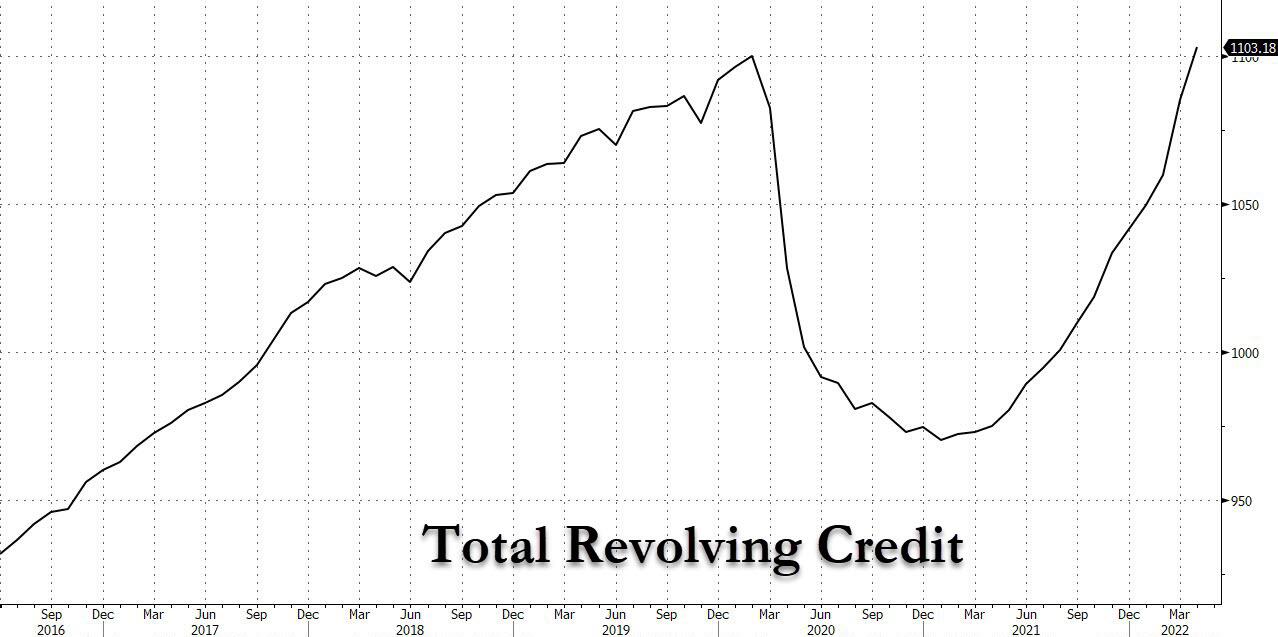

American consumer credit expanded more than expected in April, but that was down from the very high March expansion. Still, it continues a longish run of high demand, some of which will be inflation's effect, but it does support the ongoing strength of overall American consumption.

In China, they are expanding its safety net for the financial sector with a new rescue fund that could run into the tens of billions of dollars, as a cooling domestic economy and tightening monetary policy abroad pose growing risks. The new financial stability security fund is expected to provide a backstop for big institutions, such as banks, insurers and leasing companies, in cases of imminent collapse or widening investment losses sparked by overseas market turmoil that risk undermining the financial system as a whole.

They are worried about a 'balance sheet recession' because households have loaded up on debt, and will cut their spending plans for a long time to work their way through that new load.

German factory orders really disappointed observers. They fell in March and quite hard. A small recovery was expected, but in fact they fell again in April and for a third consecutive month. And foreign orders sank -4% which was faster than for local orders.

The Reserve Bank of Australia hiked its cash rate more than was expected to 0.85% with a full +50 bps rise, the most in more than 20 years. It is a real blindside curve-ball thrown to markets from a famously conservative governor, who apparently wants to know more about "least regrets". He has had an epiphany over the threat inflation poses for Australia.

But the pain it will cause their housing sector is a key concern for companies there.

Meanwhile, the World Bank has substantially cut its global growth forecast for 2022 to +2.9% in June from the +4.1% it forecast in January, citing the war in Ukraine, surging energy and food prices, and rising interest rates. They said that for many countries, a stagflation recession will be hard to avoid. Interestingly, the adjustment down to their forecasts for advanced economies was greater than for China. They still see China expanding +4.3% this year while the US's expansion will be reduced to +2.5%.

The UST 10yr yield will start today down -7 bps at 2.96%. The UST 2-10 rate curve is flatter at +25 bps and their 1-5 curve is also flatter at +77 bps. Their 30 day-10yr curve is flatter at +211 bps. The Australian ten year bond is now at 3.50% and unchanged again. The China Govt ten year bond is little-changed at 2.83%. And the New Zealand Govt ten year will start today up +7 bps at 3.73%.

On Wall Street, the S&P500 has started their Tuesday session up +0.6%. Overnight, European markets were all down about -0.7% although London was down less. Yesterday Tokyo closed up a minor +0.1% after falling away at the end of their session, Hong Kong fell -0.6, and Shanghai was up +0.2% with a late recovery. The ASX200 gave up -1.5% after the surprise RBA hike, and the NZX50 fell -1.3% in sympathy.

The price of gold is up +US$10 today from this time yesterday, now at US$1852/oz.

And oil prices are little-changed from this time yesterday, now just under US$117.50/bbl in the US, while the international Brent price is now just under US$119.50/bbl.

The Kiwi dollar will open today lower at just under 64.8 USc. Against the Australian dollar we are -½c weaker at 89.7 AUc. in fact, that is our lowest against the Aussie dollar in nearly four years. Against the euro we are also lower at 60.5 euro cents. That all means our TWI-5 starts today at just under 71.7 and surprisingly little-changed in a week.

The bitcoin price has fallen by -4.5% and is now at US$29,898. Volatility over the past 24 hours has been very high at +/- 4.0%.

The easiest place to stay up with event risk today is by following our Economic Calendar here ».

Daily exchange rates

Select chart tabs

44 Comments

“households may be starting to feel they are owing too much debt.” What to do about that then. Obviously, first up, stop borrowing but that doesn’t reduce the existing burden. Sell then, and/or downsize, if able, the leveraged assets. Could be a perfect storm on the horizon.

This whole thing is like a big pressure cooker, with many wondering at what pressure the relief valve will open. There will be a lot who have 1-2 year fixed mortgages coming off soon who will be sweating, frustrated that the promised "Rates will not be going up any time soon" mantra failed them.

The word 'unsustainable' has been used a lot in recent years when speaking of property prices, debt levels, interest rates etc but unfortunately you got labeled a DGM'er if you used it which de valued the word, however the true meaning of the word 'unsustainable' is about to be made very clear to all.

tks. you gave a vision. back on the farm when I was small. mother let the lid off the pressure cooker too early and dinner ended up on the ceiling. much noise, including that of father. as for me. I thought the world had ended, so joined in. Perfect storm that, too.

I thought the reason for thinking DGM was because it was thought unsustainable and hence the DGM noise .

Edited for clarity.

Matter of chance, met two families where banks created disharmony in family by brainwashing the adult childern to convince their parents to use their existing home equity as deposit to top up their deposit and home loan.

It is fine, if parents too are interested but if parents deny......gets worse if one parents in favour and the other not as saw in one of the two families.

Have to admit that banks are doing a fine job in convincing young adults to use their parents equity......

Childern do use but it is a new tool that banks are using to boost their loan.

Surely, many would be experiencing this trend gaining momentum.

well at end of the day they are just sales persons...if they don't sell debt, they don't get their bonus.

think of the downstream effects, parents decide to downsize or go into a retirement village, children can't repay, or refinance, means less to spend on that next move. watch retirement village share prices slide. Perhaps retirement villages start offering mortgages to buy a licence, or a lower entry cost and a way lower exit price

Intergenerational households instead of old folks in Ryman battery cages.

Work and save to rid yourself of that mortgage .............but bugga the Govt and Councils are taking on more debt for you to service ....and nek minute, the banks via the kids want you to underwrite even more debt.

Whatever happened to self responsibility?

IDK, ask the generation that basically took out reverse mortgages against 30 years of their kid's earnings for their own benefit.

Or the generation that took out mortgages to buy a house in their early 20's despite having such high interest rates (they'll continuously remind you of that) because they didn't have the patience to save for a few years when term deposit rates were double digits and pay for the house with cash.

Or the generation that got the taxpayer to underwrite a third of the financing costs of investment properties and then sold them down for huge tax-free capital gains, and then sulked when they got told they couldn't keep their grift up.

We haven't seen Peak Oil, but we may just have seen Peak Entitlement Mentality.

I would have thought that would be borderline criminal behaviour, going beyond just selling a service. But then i have always argued that the banks were a major contributor and cause of the problem. A part of that problem being the fractional system where to all intents they are creating money. I believe there is a strong need for a much more robust regulation of banks. Another part of the problem is how banks are interpreting the rules too. They often choose to interpret them in a way that undermines the purpose of the rules, penalising people and blaming the government/regulation.

Yes, it's annoyed me for years that banks have allowed the use of illiquid equity to use as deposits for further properties.

Until it's liquidates, isn't security against an already existing debt (excluding the situation where the property is held debt-free)?

It seems wrong to me that we allow multiple debts to be secured against the single large asset (or even group of assets), given the fluctuation of said asset's worth.

We would likely not be in this situation if this had been prevented.

for a start banks should be charging their standard business or commercial rates for any property lending that isn’t for a household mortgage, that is the actual occupier of the property.

Exactly. If Landlords are running a business and think they're entitled to various mechanisms real businesses enjoy (such as deductibility of lending interest), then they should take out business loans like every other business does.

If a landlord wants to take out a residential mortgage that's fine, but now you're in the camp of personal lending.

The interest rate is calculated based on the risk of the underlying security. If a loan is secured against a house then the interest rate (risk) should be comparable to other loans against houses.

Understood. But it wasn’t always so. The RBNZ (yes,yes quite some time ago) up until rogernomics split everything wide open, used to tier bank lending by both sectors and rate and within that, restrict the lenders for housing. We used to call it the “corset.”Then those lenders were predominantly, building societies, regional savings banks, life assurance, solicitors and state advances. By the 1970s trading banks had been able to enter but only by opening their own savings banks internally. Whether regarded as right or wrong it did give homeowners an edge and a bit of impetus when financing their own homes.

Overnight, Senators Lummis and Gillibrand have submitted their bipartisan bill to integrate Bitcoin and digital assets into the US financial framework.

https://www.lummis.senate.gov/press-releases/lummis-gillibrand-introduc…

why not, the existing financial system is looking as fickle as cryptos anyway, might as well all go boom together

That is exactly what Bitcoin was created to replace. It just needs time to grow :)

Interesting to see a player like Target looking to shrink inventory back to more normal levels. Those decisions are not made lightly and that will signal either forecast reduced demand and/or forecast eased supply. My bet is on the former.

I guess it believes extreme consumer credit growth is not a foundation for long term profitability.

{kind=link}

Inconvenient timing, to say the least. Auto sales in the US last month were, well, not good. According to the Bureau of Economic Analysis (BEA), the government agency responsible for GDP, unit sales of light vehicles tumbled to a seasonally-adjusted annual rate of 12.68 million in May 2022. That’s the lowest since December, down substantially from a not-too-high 14.50 million pace in April and third worst since 2020.

The other two months with lower sales than May had been September and December 2021, both COVID-plagued (delta then omicron). Like so many other indications around the world of late, we can’t use the pandemic as an excuse this time.

As I wrote earlier, demand wasn’t supposed to be a problem rocking the middle of 2022 what with sky-high CPIs making it seem the US economy was on fire. Link

Meanwhile, the World Bank has substantially cut its global growth forecast for 2022 to +2.9% in June from the +4.1% it forecast in January, citing the war in Ukraine, surging energy and food prices, and rising interest rates. They said that for many countries, a stagflation recession will be hard to avoid. Interestingly, the adjustment down to their forecasts for advanced economies was greater than for China. They still see China expanding +4.3% this year while the US's expansion will be reduced to +2.5%.

Atlanta Fed Slashes Q2 GDP Again, Now Just 0.9% Away From Official Recession

Only Fed Cult and its media kiss asses would've confused a supply shock w/actual recovery. The CPI wasn't inflation, and high consumer price acceleration hid just how little recovery there had been. Link

Big article in the Herald today about the house building slump. I am astonished at how little this has been talked about in advance, it’s been building for at least one year. This website is as guilty as any - talking up the monthly consent data without looking at and analysing the issues brewing behind the ‘rosy figures’ (which are clearly lagging ones).

And oil prices are little-changed from this time yesterday, now just under US$117.50/bbl in the US, while the international Brent price is now just under US$119.50/bbl.

EU to exempt private and corporate jets from green aviation fuel tax. We are not all in this together. Link

Sheeple just keep on sleeping. But dont worry, the poor and middle class will be made to pay to "fix the world".

And now they've found micro-plastics in snow flakes in Antarctica from every sample they took there.

We've successfully managed to pollute the furthest corners of the world. Well done us.

Only on the surface though. When they find microplastics in core samples from glaciers, then we worry. /s

Global elites doing their bit to fight tooth and nail on the war on climate change frontlines. We plant out productive farmland in pines and move our dairying to China - while the EU subsidies private jets.

"Executive jets will escape plans to tax polluting aviation fuels, according to draft proposals to be presented by the European Commission on Wednesday.

The commission plans to set an EU-wide minimum tax rate for aviation fuels, as it seeks to meet more ambitious targets to fight climate change."

https://www.irishtimes.com/business/transport-and-tourism/corporate-jet…

Is being a colossal hypocrite a prerequisite for law and policy makers concerning themselves with climate change and the environment?

I've got a family member who has some cushy-looking UN climate change policy gig, whose job - based off their social media feed at least - appears to consist entirely of telling people what to do, and then in private doing the total opposite.

How can you tell people with a straight face that flying is bad and then in good conscience jet off - business class, of course, for added emissions - over to Europe literally every single month, sometimes twice a month, for an endless procession of "summits". I thought Zoom was good enough for everybody, and we should all be striving to WFH?

I suppose the excuse will be some BS like "I buy the offset credits" (in other words, 'I am sufficiently privileged to use money to absolve myself of any sin')

I'm convinced that if those who make the rules (or try to encourage compliance) could be bothered to even make the slightest attempt to practice what they preach, buy in from joe public would be so much greater.

1. If the alternative is not being present at the table where policies that affect the climate's future are decided, it would seem there's little alternative but to fly there. Albeit private jets seem excessive and ridiculous.

2. In the very specific example of Bill Gates, he seems very conscious of the footprint of his flying and deliberately invests in both offsets and technologies to try to reduce and eliminate emissions in the future. The balance would seem to be, can he do more by investing more billions in more potentially transformative technologies by visiting and vetting them, versus fewer.

(Aside: let's not subsidise private jets or illegitimate utes...both seem ridiculous targets for subsidies, direct or indirect.)

Astonishing! Tony Alexander has turned from ultra bull to ultra bear. Acknowledges prices already down 10% in Auckland and Wellington, but capitulation has not yet commenced. Also talking about the looming house building crash. What a DGM!

Haha, things I was talking about middle of 2021…

https://www.oneroof.co.nz/news/41592

Yeah the real estate industry is starting to turn on its customers......need the sales to feed to machine, pay the overheads.

Some people are going to feel they have lead up the garden path very soon

I've not seen anything at all about the following on the net. Two polls, the first showing a drop in the Labour vote in the Tauranga byelection. It shows a swing against Labour, even if Labour never really has a chance in Tauranga.

The second shows ACT and thee Greens have increased their vote share, and National could govern with ACT. It's Roy Morgan, but still shows something interesting.

Newshub Reid research Tauranga poll

2022 Election 2020

Uffindell (National) 56.9 Bridges 42.8

Tinetti (Lab) 21.9 Tinetti (Labour) 35.5

Don't know 31.4

Party Vote

National 51.5 32.5

Labour 27.9 42

The Morgan Poll

May Election

Labour 31.5 50.01

Greens 11.5 7.86

National 40 25.58

ACT 10 7.59

Maori Party 1 1.17

Tauranga deserves a National/Act candidate - Boomersville

Uffindell is a Millennial? Easier to be pushed around by the Boomer puppet masters.

Everyone wants control and none more than the IPCC of the UN as in this showpiece in RNZ today.

Climate change: 'Global veganisation is now a survival imperative' - IPCC expert reviewer | RNZ News

Makes me want to put up a billboard saying:

"We are New Zealanders.

We eat meat.

Support our farmers, they're all we have.

We didn't vote for the United Nations."

Support our farmers...pay through the nose for your cheese..thats all we have?

Ports of Auckland scraps automation project rendering $65m of investment useless

“It was a bold and innovative project, but one that – despite the hard work of many - was unable to be delivered.”

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.