Here's our summary of key economic events overnight with news there was an overnight phone conference between the US and Chinese presidents regarding the Ukraine invasion. Markets responded positively that something like that even happened. But there is no evidence yet of any changed positions.

Meanwhile, American existing home sales faded in February continuing the see-sawing pattern of the past few months. High mortgage interest rates are one reason they were down a rather sharp -7.2% from January, and down -2.4% from a year ago. The other reason is the very unusually low houses being offered for sale at present, about seven weeks worth at the current rate. Those that are selling are at the top end of the market, so average prices seem like they are rising.

The very good Canadian data continues. Their retail sales rose more than expected in January, up +3.2% from the prior month, up +12% in a year. The virtuous trend continued for strong February jobs gains too. The ADP report showed a +475,000 gain in the month, more than making up for the under-result in January. It was also the strongest monthly rise ever recorded in this series.

Japan's consumer inflation rose by +0.9% in the year to February, and as low as that may seem to us it is the most since April 2019. It comes after a +0.5% January gain. The latest figure marked the 6th straight month of annual inflation, with food prices rising at the fastest pace in 4 years, up +2.8% pa. Japan's central; bank likes the rise, but it was not enough for them to shift their policy direction.

The Bank of Japan reviewed its policy settings late yesterday, leaving them unchanged at +0.1%. The recent pickup in their economy is undermined by the recent Ukraine war impacts

The Russian central bank also reviewed their monetary policy settings overnight, and they too left things unchanged - at a 20% policy rate. There is little they can do after their government invaded its neighbour. Inflation is rampant, their currency is in the toilet. Monetary policy isn't able to do anything about either in the short term. But they know a huge decline is ahead of them, calling it a “large-scale structural transformation”.

Aluminium prices spiked on the invasion of Ukraine. Since, they have stayed high, volatile in the past six weeks, and again this week. But they are ending high.

Although global coal prices remain very high, they are easing off their early March peak.

High prices are one thing, but commodity markets are also suffering a liquidity crisis as intermediating traders disappear because the risks are too high and real buyers and real sellers have trouble agreeing terms directly. Aluminium isn't being spared in this crisis.

The IEA is warning of "the biggest supply crisis in decades" as war consequences sweep over energy markets. But it also reports sudden important responses in regions hardest it, especially Europe. Measures implemented this year could bring down European gas imports from Russia by over one-third, with additional temporary options to deepen these cuts to well over half - while still lowering emissions. It seems war is bringing sudden innovations in some areas. It is a great shame it takes a war crisis to motivate these adaptions.

A Parliamentary report on Australia's housing affordability problems has recommended that their States should ditch stamp duty and replace it over time with a broad-based land tax, review the taxes holding back development of the emerging build-to-rent sector and reform surging developer contributions that are not being used to fund crucial local infrastructure. These are just a few of their 16 recommendations to improve long term housing affordability there.

And you know it is election season in Australia when talk of tax cuts grows even as their deficit rises.

And there is more evidence that the Hayne financial services review is being gutted. The Canberra government is going to let the obvious conflict of interest stand that mortgage brokers have by receiving commissions from banks. New Zealand regulators turn a blind eye to that as well. Few things in the financial world are more obvious than this, but no one wants to do any about it.

The UST 10yr yield opens today at 2.14% and down -4 bps from this time yesterday. A week ago though this yield had just risen to 2.00% so it has been a big mover up this past week. The UST 2-10 rate curve starts today flatter at +19 bps. Their 1-5 curve is steeper however at +93 bps (and much steeper over the week) but their 30 day-10yr curve is flatter at +194 bps (but much steeper in a week). The Australian ten year bond is up +1 bp at 2.53%. The China Govt ten year bond is unchanged at 2.82%. And the New Zealand Govt ten year is little-changed at just on 3.19%.

Wall Street is up +1.0% on the S&P500 in Friday afternoon trade and heading for a heroic +6.1% rise for the week. That Biden-Xi phone call is helping the immediate mood. But it is still -7.5% lower than its year-end record high. Overnight, European markets were all up about +0.2%. That means Paris was up +5.1% for the week, Frankfurt was up +4.2% and London was up +3.5% for the week. Yesterday, Tokyo ended +0.7% higher on the day and up +5.9% for the week. Hong Kong was down -0.4% yesterday, but up almost +6.0% for the week. And Shanghai rose +1.1% yesterday, but it booked a retreat for the week of -0.6%. The ASX200 rose +0.6% in its Friday session, taking its weekly gain to +3.3%. The NZX50 finished with a flourish, up +1.5% yesterday, and up +2.9% for the week.

The price of gold starts today at US$1929/oz and still yo-yoing and down -US$15/oz from this time yesterday. A week ago it was at US$1990/oz but that was its recent high point.

And oil prices are higher today, up +US$2/bbl. In the US they are now just under US$103.50/bbl. The international price is just on US$106/bbl. But both are -US$4/bbl lower than a week ago and -US$7/bbl lower than two weeks ago.

The Kiwi dollar will open today firmer again, now at just on 69.1 USc and a four month high. The Kiwi dollar has appreciated +1.6% in a week. Against the Australian dollar we are little-changed at 93.2 AUc. Against the euro we are +½c up from this time yesterday at 62.5 euro cents. That all means our TWI-5 starts today at just over 74.2 and also a four month high.

The bitcoin price was up +1.9% from this time yesterday to US$41,579. That is a +7.5% weekly gain but really only taking it back to levels of two weeks ago. Volatility over the past 24 hours has been modest at +/- 1.9%.

The easiest place to stay up with event risk today is by following our Economic Calendar here ».

Daily exchange rates

Select chart tabs

23 Comments

The UST 10yr yield opens today at 2.14% and down -4 bps from this time yesterday. A week ago though this yield had just risen to 2.00% so it has been a big mover up this past week. The UST 2-10 rate curve starts today flatter at +19 bps.

Very simply, the outer pieces of our curves are considering, pricing greater confidence that perhaps the labor market just isn’t near full employment, that the overall economy may not be all that good. There is a substantial likelihood high CPI rates have obscured these possibilities, particularly in mainstream public opinion spoon-fed the Fed’s QE6 “flood of digital dollars” lie (given to them by Jay Powell’s May 13, 2020, appearance on CBS News’ 60 Minutes). Link

Meanwhile, American existing home sales faded in February continuing the see-sawing pattern of the past few months.

The median existing-home price for all housing types in February was $357,300, up 15.0% from February 2021 ($310,600), as prices grew in each region.

This marks 120 consecutive months of year-over-year increases, the longest-running streak on record.

"Housing affordability continues to be a major challenge, as buyers are getting a double whammy: rising mortgage rates and sustained price increases," said Lawrence Yun, NAR's chief economist.

"Some who had previously qualified at a 3% mortgage rate are no longer able to buy at the 4% rate.

Even the NAR is rubbishing the Government's CPI data...

"Monthly payments have risen by 28% from one year ago – which interestingly is not a part of the consumer price index – and the market remains swift with multiple offers still being recorded on most properties."

The most expensive homes are seeing the biggest increases in sales while lower-priced home-sales are crashing... Link

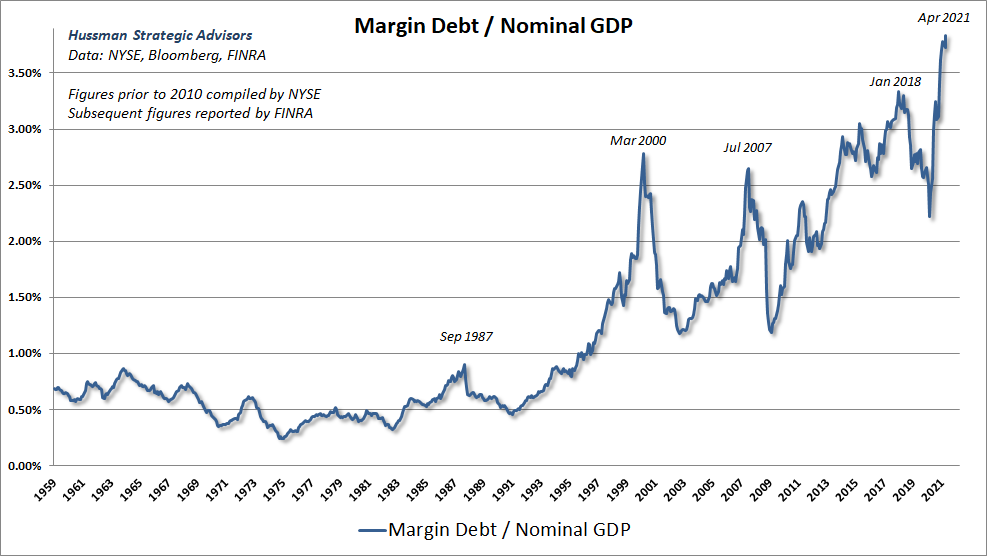

Policy makers sometimes flatter themselves with the idea that holding interest rates at untenably low levels makes it cheaper for borrowers to obtain funds. Unfortunately, it does so only by transferring income from people who are trying to save for the future. Replacing Treasury securities with base money may make savings more “liquid,” but it doesn’t suddenly make people abandon their retirement plans in favor of consuming today. Low rates also don’t magically create productive investment opportunities.

What economic activities suddenly become viable at zero interest rates that were somehow not viable before? Only projects so unproductive that any positive hurdle rate would sink them. The main activities that are encouraged by zero interest rates are activities where interest is the primary cost of doing business: leveraged real estate transactions; “carry trades” that employ enormous amounts of leverage to profit from small yield differences; and speculation on margin. Presently, margin debt as a percentage of GDP is at a historic extreme.

https://www.hussmanfunds.com/comment/mc210614/

{kind=link}

Exactly..nice series of posts 👍

"Wall Street is up +1.0% on the S&P500 in Friday afternoon trade and heading for a heroic +6.1% rise for the week. That Biden-Xi phone call is helping the immediate mood. But it is still -7.5% lower than its year-end record high."

Yippee...stocks looking good.

Hmmmm.

Gen. Kenneth Wilsbach, commander of Pacific Air Forces, on Monday said he hopes that one of the "key lessons" the Chinese are taking from the military conflict between Russia and Ukraine is "the solidarity of the global community" in opposing "an unprovoked attack on a neighbor," according to US-based Air Force Magazine. He added that if China behaves in a similar way against the island of Taiwan or a neighboring country, "something more robust will happen." Wilsbach made those remarks during an AFA Mitchell Institute streaming discussion. Link

Blind optimism is fuelling these relief rallies in markets. Its almost as though all of the risks have just magically disappeared.

AKA euphoria

Exuberance

or mania

pop!

Yep I reckon there's damage still to come.

I will remain on the sidelines for some time yet.

Yes it comes down to the Fed...

If they chose to tackle inflation the consumer wins, the cost of capital will increase and asset prices will fall.

If they don't chose to tackle inflation the consumer loses, the cost of capital remains at historic lows and asset prices can remain very elevated.

If the consumer continues to lose, in time the economy is strangled, and then asset prices will fall as income isn't sufficient to cover the cost of debt.

Do you eat your frog first, or last?

Is it blind optimism or is it pessimism about the future of the New-Zealand dollar. Most of the pundits I talk to a petrified of an inflation. Any real asset at any price Is preferable to fiat paper whose value is determined by fools such as Ardern and Orr.

There is a trans-Tasman slur on page V of the Chair’s Foreword of the above linked Australian Parliamentary Report in to Housing Supply and Affordability.

“…effectively, we cannot be bothered building more housing so we should deny other Australians the opportunity to own their own home. Further, so egregious is our laziness that we would prefer the entire economy suffer rather than deal with the underlying issues of the housing market.

This is largely, but not entirely, the path the New Zealand Government has taken.”

Pretty accurate assumption I would say . Nzs laziness extends to subsidising rent so as to continue to lock tenants in and futher lessen their likelihood of being able to acquire their own home . Along with government reluctance to implement a tax free threshold to incentivize work .

...oil prices are higher today...

This could be a good time to internationally coordinate gradually releasing the SPR, I mean if not now - when? That will allow drillers to ramp production.

US quietly backtracks on Russian oil ban – media

Senate unlikely to pass House-approved energy import restrictions

No doubt a piece of solid reporting from everyone's favourite propaganda network, RT. Shame it's been 404'd. I needed a good laugh.

Don't worry, there are plenty of other propaganda networks available for you to chuckle at. I find The Guardian quite a good one; currently running a piece about George W. Bush visiting a Ukrainian church in Chicago, and applauding his heartfelt display of solidarity.

That would be George W. Bush the war criminal, who invaded Iraq in 2003 in blatant violation of international law, after his administration spent two years trying to get the UN on side using fabricated evidence and outright lies.

You couldn't make this stuff up if you tried, but most people will read all about it without blinking an eye.

Their eyes will glaze over, and then they'll accuse you of being a trump supporter. If you ask why that's a problem, they'll fumble their way for a reasoning and eventually land on "he's a womanizer and a chauvinist".

How about he's a narcissist, a liar and after a loss incited an insurrection that resulted in deaths. Murderer or was it just manslaughter? That guy is so stupid stupider people thought he was actually hiding genus. You can't make this stuff up.

Interesting, could you share article. I just searched for it but couldn't find it. It did return results for the same story reported on CNN, WSJ, NYpost, FoxNews, Washington Examiner among others which is that Bush and Bill Clinton laying flowers at Ukrainian Church.

I've found the guardian to also be a willing and frequent critic of supposedly western values and governments so am surprised you would determine it to be propaganda? For example: https://www.theguardian.com/commentisfree/2022/mar/17/western-values-en…

Are you sure this is not just a case of balanced reporting. The very thing that Putin has made illegal in Russia.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.