Here's our summary of key economic events over the long weekend with news US payrolls rose much more than expected, reinforcing market expectations the Fed will raise rates at its next meeting.

But first, we start today with something we don't usually track. Indonesia’s GDP data showed that the economy returned to its pre-pandemic size in Q4-2021, expanding +5.0% from the same quarter a year earlier, as the recovery regained momentum after the setback from the Delta wave in Q3 (+3.5%).

In China, according to the private Caixin services PMI, business activity is now barely expanding with momentum slowing to a five-month low. Lockdowns affected them but new orders slowed as well. Their employment measure is in fact now contracting in the service sector. This report is very similar to the official services sector PMI.

China FX reserves were expected to rise slightly (by about +US$10 bln) in January, but in fact they fell (by about -US$28 bln) to US$3.2 tln. These are small shifts but are watched closely for early signals.

Meanwhile China has signed a 30 year deal for Russian gas. It is a lever Russia is holding over the EU, just at a time the Chinese are trying to woo some EU countries, like Poland. China might end up a stabilising influence on Moscow's Ukrainian ambitions - or they could accentuate the pressures.

In the EU, their retail sales data for December was a significant disappointment, falling from November and rising a very weak +2.0% from December 2020 when a +5.1% gain was expected. And given rising inflation, that meant that retail volumes are falling now.

German industrial production slipped unexpectedly in December - and it was a chunky move lower.

The OECD reported that overall inflation rose to +6.6% in the 12 months to December 2021, compared with +5.9% in November, and just +1.2% in December 2020, reaching its highest rate since July 1991. This increase was driven in part by a surge in annual inflation in Turkey (to +36.1% in December). Excluding Turkey, inflation in the OECD area increased to +5.6% in December.

If you missed it on Saturday, the big news was the US non-farm payrolls report was unexpectedly positive. The headline gain reported was +467,000 and far above the +150,000 gains which was widely expected, and nowhere near the -400,000 loss that some pessimists had feared.

Better, there were some significant revisions to job gains in November and December which mean employers added +700,000 more jobs than these non-farm payrolls reports had previously indicated. That is pretty significant.

The January 2022 employed workforce now total 147.5 mln, up +6.5 mln from January 2021. But it is down -2.5 mln from pre-pandemic January 2020 so they still have a long way to go to fully recover the pandemic effects. The US participation rate is an improving sign however. For the first time in a long time it rose significantly, up to 62.2% from 61.9%. More people are back entering their workforce and wanting to participate in their labour market. It is not yet back to the levels last seen in the Obama years, but at least it is back above most of the Trump period.

The other positive out of this data is that average hourly earnings increased to US$31.63 (NZ$47.70), up +5.7% over the past year. It was the largest monthly increase in the last year, and although inflation is high, it shows that wages are largely keeping up. CPI was up +5.5% in an actual (not seasonally adjusted) basis. Core PCE was up +4.9%.

Canada also released its jobs report for January and that was not positive at all. They lost -200,000 jobs on a seasonally adjusted basis (much more on an actual basis) and this was worse than the -118,000 analyst estimates. Their participation rate fell. Their jobless rate rose, and wage gains came in far less than current inflation. They will be grumpy with this result, especially after their neighbour's positive surprises.

In Australia, they bounced back with a strong expansion in their services sector in December and January and putting behind it the lockdown contractions in the prior four months.

The Reserve Bank of Australia has updated and upgraded its economic forecasts for the country in its Monetary Policy Statement released on Friday. But although they now say their economy will grow by +4¼% this year, growth will slow to +2% in 2023. However, both are upgrades from their October forecasts.

In NSW, there has been a drop to 7,437 new community cases reported yesterday, now with 85,344 active locally-acquired cases, and another 14 daily deaths. There are now 2,099 in hospital there, now well off their highs. In Victoria they reported 8,275 more new infections yesterday. There are now 59,801 active cases in that state - and there were 7 more deaths there. Queensland is reporting 4,701 new cases and 19 more deaths. In South Australia, new cases have slipped to 1147 yesterday but they had 5 deaths. The ACT has 399 new cases and one death, and Tasmania 473 new cases and no deaths. Overall in Australia, about 23,300 new cases were reported yesterday.

The UST 10yr yield opens today at 1.93% and up another +1 bp and another two year high. The UST 2-10 rate curve starts today a little steeper at +63 bps. Their 1-5 curve is little-changed at +90 bps, while their 3m-10 year curve is also little-changed at +189 bps. The Australian Govt ten year benchmark rate is up +1 bp at 2.03%. The China Govt ten year bond is +1 bps as well at 2.73%. The New Zealand Govt ten year is unchanged at 2.60%.

On Wall Street, the S&P500 has opened its Monday session soft and down -0.3%. Overnight, European markets all rose by about +1% catching up with teh US data. Yesterday, Tokyo fell -0.7%. Hong Kong was little-changed. Shanghai was back in action and in catch-up more, and up +2.0%. Yesterday the ASX200 fell a minor -0.1% while the NZX50 was closed of course.

The price of gold starts today at US$1818/oz and up +US$12 from where we left it on Saturday.

However oil prices are lower from Saturday by a bit more than -US$1 at just over US$90/bbl in the US, while the international Brent price is now just over US$92/bbl.

The Kiwi dollar will open today little-changed at 66.2 USc. Against the Australian dollar we are firmish at our lower level of 93.1 AUc. Against the euro we are a lot lower at 57.9 euro cents. That means our TWI-5 starts today just on 70.6 and about where we were this time last week.

The bitcoin price is up another +8% since this time Saturday and now at US$43,674. Volatility over the past 24 hours has been high at +/- 3.2%.

The easiest place to stay up with event risk today is by following our Economic Calendar here ».

Daily exchange rates

Select chart tabs

91 Comments

Imagine owning some of the best performing asset in history with a limited supply. It hits $69k USD. Then it nukes 50%+ to $32k USD. Only after a 50% draw down do you decide to panic and sell it. You mutter things like "its never going up again" and "it's a scam". Then you watch it pump 40% off the lows to $44k USD while the stock market is weak and the fed talks of raising rates. Now you think about buying back in and adding fuel to the pump. I love this market, so much opportunity and so much pain. If you don't have an interest in crypto then over the next 5 years you will regret it. Good morning to all!

Be quick!

It's a zero-sum game

And all 'investment' is parasitic on something real.

And there are more forward bets than there is remaining underwrite. Indeed, ever since 2008 I've been asking what 'money' is really worth, given debt? Even just using 'economic' counts (which avoid resource draw-down and life-supporting ecological conditions) it appears that every dollar of GDP requires more than a dollar of debt

https://surplusenergyeconomics.wordpress.com/

VTHO. Bit sad that.

Have you tried stimulating drugs, with regularly getting somebody to bang your head between two bricks.

Just as useful. Possibly better.

Sad? Get a grip. It is something I enjoy and it has rewarded me handsomely. Imagine judging someone on what they like doing, it really speaks volumes on the type of person you are. You might enjoy bike riding or visit nightclubs on k road, I don't judge you for it. If you are having a good time then good for you!

Fwiw I partied for years when I was younger without a family. Not as financially useful but definitely more fun.

I'm hoping we'll see another meme run and BNB blow the top off. Doesn't feel like this super-cycle has ended.

I'll be getting out, hoarding some cash for the winter and seeing what drops like a stone when the music stops. Have learned that I won't make mega-bucks this time, but next time I'll be ready.

So it's no good as a currency and it's no good as a store of value. What is it exactly?

A permission-less and censorship resistant global monetary network. Don’t confuse Bitcoin the asset and bitcoin the network. If you want to see a use case, just look at what happened with the GoFundMe debacle in Canada. Donations have now moved to the bitcoin network.

I don't think you understand what a store of value is. If you have owned BTC at any point in the past 13 years (except the past 6 months) then you have experienced the greatest store of value ever seen. Short term fluctuations are irrelevant.

A STORE OF VALUE is an asset, commodity or currency that can be saved, retrieved, and exchanged in the FUTURE without deteriorating in value. In other words, to enter this category, the item acquired should, OVER TIME, either be worth the SAME OR MORE.

There have been plenty of times where the value drops dramatically and takes a while to come back up

Imagine trying to trade with the stuff. Sorry, that price I quoted yesterday has gone up by 20%. Store of value only if you trade in a vacuum 1BTC = 1BTC. Still, the latest dip was a good opportunity for a small speculation.

You walk into the supermarket to buy groceries with your bozocoins. In the time that it takes you to choose which brand of cheese to buy, the value drops by 10%, so you put the cheese back.

There have been plenty of times where the value drops dramatically and takes a while to come back up.

Did you know that applies to every single asset / commodity market?

(Except New Zealand housing of course)

i have some tulip bulbs you might like to store some value in...

I don't think you understand what a store of value is

"the item acquired should, OVER TIME, either be worth the SAME OR MORE."

How is a 50% drop over three months, the "SAME OR MORE"?

I don't think you understand what a store of value is

"the item acquired should, OVER TIME, either be worth the SAME OR MORE."

BTC1 is still BTC1 10 yeas ago, last year, and today. Over time, the value has increased.

NZD1 in 2022 has definitely not held its value over the past 10 years or even 1 year.

And if you needed to do any financial transactions in Jan?

Say you sold your home and settled mid-Nov. Spent a couple months to find you new dream upper quartile home, offer is accepted and you settle 23 Jan. Opps, your bitcoin can only buy half as much house now, you need to pay penalties for failing to settle and now start shopping for a new home at the bottom end of the market. Opps! Bitcoin is now up 30%, throw away all those weekends searching and start your search again for a median market home, but then opps!

A giant casino, just like the stock market but on steroids. It is peak capitalism and a road to financial freedom or financial destruction. Once you taste the forbidden fruit, there is no going back.

At least the stock market represents companies, and most of them actually produce something.

Bitcoin takes power and produces heat from the back of some server, very useful

This is the argument people who missed out use. They are trying to cope.

Bitcoin represents freedom and decentralisation, among other things. Far more important than 99% of listed companies producing plastic consumer crap or platforms like Facebook and Snapchat.

Up another 50% and friends will start asking where the best place to buy some is again. It's as reliable as the cycles of the moon.

Yes sir. And then you sell!

You must have a different dictionary from the rest of us. I have not seen any "assets" performing in this manner recently.

Looks like the bears will have to wait a little longer for Bitcoin to die. Meanwhile KPMG Canada announced it has added it to its balance sheet. It will soon become common place as a treasury reserve asset.

Electronic digits an asset?

They must be economists.

Seems to be parasite/parasitic, your words for 2022? In which case, you could have notated consultants just ahead of economists.

Like your fiat recorded in your banks database? I thought there were smart people on this site.

Fiat doesn't chew through copious amounts of energy just to exist. "Proof of work" etc.

Is it true that an average of 140,000 kWh of energy is needed to produce one bitcoin?

"Fiat doesn't chew through copious amounts of energy just to exist" is one of those statements where if you really wanted to scrutinse the international monetary system as it stands, you'd probably end up with an answer you (or I) can't comprehend. I sure as hell wouldn't be making such a black and white statement like that tho.

Big difference between a keystroke on a spreadsheet and burning through resources to add to a ledger.

Or are you talking about the total sum of energy consumption to maintain a system. Comparing a financial network that services billions of people against a speculative system with 100 million people, there's a big difference between the per capita energy consumption.

My last power bill showed 5cents a unit plus the monthly rort fixed charges which took it up to 28cents a unit. However 140000 x .05 =$7000 per Bitcoin. If that is true, then this is truly a great asset to "mine".

Great to see Australia announce full border reopening in two weeks. For Kiwis this will finally allow a conduit by which they can enter and leave New Zealand once our government opens the gates at the end of this month so bypassing several of the 'stages' of reopening.

"I call on you Prime Minister Ardern to tear down those MIQ facilities!"

Very difficult to leave NZ in the first place if you need to provide a negative test within 24 hours of departure. They are very expensive too. Something else about which little thought and planning has taken place.

$141 via MedLab South or LabTests. Not great value but not a total ripoff.

Are you talking about pre departure covid test. Labtest may be charging $141 but they do not do the test themselves so have to go to GP or other medical centre and they are charging $250 to $285 and THAT is a total ripoff.

Unfortunately this government run by Jacinda Arden only listen and act when media highlights it.

That's the problem Foxglove, thought and planning. Two words which Jacinda and her merry go round team don't understand. The real world does, hence all the RAT test that the government have gone and confiscated from them (they have the planning to order early to protect their workers) and now turn around and say look we have all these test whats the issue. Disgusting abuse of power. Also where are the 10-20k cases a day that they have based there restrictions on...by my math the case numbers went down the last three days.

The Herald this morning quotes PM Adern thus, “No private company had their order delayed or taken as a result of government intervention, she said.” There definitely needs to be an urgent independent enquiry into this episode. Firstly you have the MoH and it’s director denying any stocks had been acquisitioned. Then stating they had been, but only applied to those not yet imported. Finally being forced to admit both of those statements as being untrue. Our Prime Minister now contradicts that and goes back to the beginning. How come?

Politics 101. Repeat the lie often enough and the people will believe it.

To be fair, if there was a list of priorities, making the cost to leave NZ more affordable probably isn't registering too much. Even once the borders are "open", the traffic won't be anywhere close to 2019 levels for some time.

there is a significant pent up demand in NZ - especially in healthcare to Get the ##$$ out of Dodge - a lot of healthcare professionals have already secured options in Australia and have simply waited for MIQ to go so they can come back to visit family/Whanau - not to mention many young people who have delayed their OE --- and i suspect but simply dont know about other industries.

There will be significant outflows in the next 9 months -- and they will all be skilled professionals -- meanwhile the In ledger will be filled by students, asylum seekers, fruit pickers and maybe a few backpackers -- not sure this will work out to well for us !

People keep talking about this mass exodus but once they work out what a logistical ballache it currently is (and how expensive shipping things is now), and how less green the grass is out there than they imagine, it'll be more of a trickle.

The "skilled professionals" are largely younger inexperienced types who currently are locked out of the housing market.

Anyone with a super hard-on to leave has been able to do so for a very long time.

I'll wait and see, in the meantime I suggest we nominate the Australian government for an award. They will have, after all, freed the Kiwis to return home or leave. That in itself is a service to liberty our own government would have withheld.

..obviously hasn't spoken to any highly experienced A&E professionals of late.

Friend runs one. They're on the cusp of a supposed fundamental salary increase.

If they're highly experienced (which to me would be 10 years or more in) and don't yet own a house moving location probably won't change that.

The other conduit is to book Aussie to Fiji transiting through Auckland and jumping off at Auckland, staying at an empty but fully booked MIQ hotel. Then it turns out that the MIQ bosses bumbling incompetence may well be your crime. As the "criminal" has plenty of financial backing he will not be prosecuted, let alone found guilty. Can someone print here what actual crime would have been committed. Not your own opinion, but the actual wording on any prosecution sheet?

“China might end up stabilising Moscow’s Ukrainian ambitions - or they could accentuate the pressures.” A bob each way, understandable. Perhaps the Russian President just wants to play dominoes.

Meanwhile China has signed a 30 year deal for Russian gas. It is a lever Russia is holding over the EU, just at a time the Chinese are trying to woo some EU countries, like Poland. China might end up a stabilising influence on Moscow's Ukrainian ambitions - or they could accentuate the pressures. [my emphasis]

Yeah right!! - 'Russian Troop Build-Up' - Eight Years Of Crying Wolf

China opens up another front of contention - China’s foray into America’s backyard angers Washington (and London)

Most striking about the China-Argentina joint statement was the inclusion of the Falkland Islands issue. This stance is not new, but it is significant that Beijing was willing to bring it up at this point. It was undoubtedly a diplomatic request from Fernandez as part of the deal to join the BRI. Its inclusion, however, was nonetheless a clear slap in the face for Britain and a knockback for the increasingly aggressive anti-China policy it is pursuing under Liz Truss. It is a signal to Britain that if the United Kingdom continues to push on issues China deems sensitive, such as Hong Kong, Taiwan, Tibet, and Xinjiang, China has diplomatic leverage to hit back by openly backing Argentina's claims to the Falklands/Malvinas, emboldening Argentina in the same way anti-China sentiment has emboldened Taiwan, creating geopolitical difficulty for the UK.

In what substantive measure, are the Falkland islands an equal assett to Taiwan?

Claims of sovereignty.

In the case of Taiwan - exports to China are up almost 50% since Dec. 2019 and amount to 36% of its GDP, about the same ratio as for Vietnam.

Audaxes,

At least six Conservatives including a former Cabinet minister joined MPs from across the political spectrum in linking the harassment to the baseless claim Mr Johnson made while under pressure over the partygate scandal.

Not even those in his own party believe what he said about Keir Starmer.

Falkland Islands? You mean Las Islas Malvinas.

Depends which language you use. Like Helvetica and Switzerland or Holland and Netherlands.

No, it's political

Like North Macedonia and the Cannibal islands.

More like Suisse, Schweiz, Svizzera

.

you missed Svizra

Call it" the frozen wop-wops" or whatever you will, it has nothing on Taiwan.

No that would be like using Aotearoa.

The Falkland Islands was called Malvinas while the Spanish had them as part of their South American Empire. After some war the British grabbed them. This was all long before the country of Argentina was formed. So they have never been part of the country we call Argentina.

China and Russia together appear willing to take on the world by force. COVID has/will cause China a lot of economic harm as the lessons learned stress the level of resilience that is not present when shipping companies hold the world to ransom and countries work to reinvigorate their manufacturing industries. The BRI might be a means that China will use to blackmail countries to either sit on the sidelines or come in on their side. The nightmare scenario is building!

More likely China will wait it out. Let the US military assets depreciate to the point of obscurity. Why fight a war when mother time will do the job?

Because that same timeline undermines their own aspirations in the South China Sea and elsewhere. Time is a double edged sword and Xi is impatient.

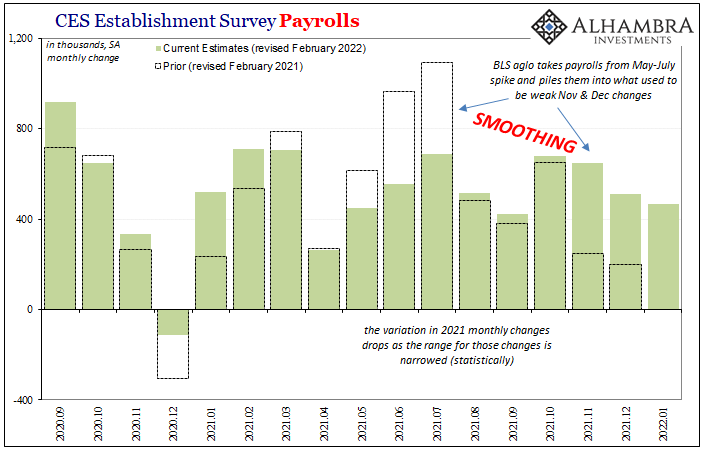

If you missed it on Saturday, the big news was the US non-farm payrolls report was unexpectedly positive. The headline gain reported was +467,000 and far above the +150,000 gains which was widely expected, and nowhere near the -400,000 loss that some pessimists had feared.

In the context of last year’s benchmark and how the series ended 2021, the current month’s change of 467,000 during January – especially as a sharp contrast with what ADP had earlier reported – would’ve been a nice blowout surprise. Instead, it’s still a slowdown from a less variable trend (above).

Under the statistical “wisdom” of the February 2022 benchmarks, the 467,000 for last month takes on an entirely different context. Better or worse depends, I suppose, on your perspective and take on such statistical manipulation (I’m not suggesting it is based on politics; on the contrary, the problem is, as always, trend-cycle theory). Link

{kind=link}

I'm bemused by the awed reception Interest seems to accord the US figures. As well as the Snider link you posted above, Mike Shedlock (Mish) and Rabobank are both of the opinion that, because of the measurement discontinuity, and the constant historical revisions, the numbers are essentially PDOOMA.....

When will the soil moisture map show the benefits of some of that rain?

Oh it’s still 2/2/22

Its been showing 2/2/22 for a few days now, link may be broken.

Seems to be working for me. Its a lot greener.

Yes, there was no green or blue in the north a couple of days ago and most of the red is gone now.

I want to get a blue marker pen and touch up the Taranaki coast there. From on the ground observations, it ain't red.

76.2mm for the week so far in Tauranga and more forecast.

I was wondering exactly the same thing. Glad you identified the date. Thanks

I just refreshed the page from an hour ago and the red reduced. Hard for those flooded but a relief for where I am.

Bought the current house with climate change in mind so now on top of the hill and not at the bottom of one like I was in 2005 when I never gave flooding a thought.

There was a news item at 7am this morning on RNZ (communist radio) that after recalculating the volume of water contained in glaciers there is a lot less than water originally thought. Which translates to, the sea levels will not rise. Wtf

Don't forget there's a lot of water melted from the glaciers already but the sea level rise in the last >100years? has not been catastrophic and is not likely to be so just more alarmism about the glacier water contribution to sea level rise. Wasn't it some UN johnnie about 5 years ago who said there won't be any glaciers in the Himalayas in 20xx. Don't recall the time that he gave but pretty certain it was < 2050. I think he withdrew that statement sometime afterwards.

One for the finance geeks:

5 yrs ago I put some money on a Kiwibank term deposit. It has now matured. At the time I was conscious that Kiwibanks' deposits I think were explicitly "guaranteed" by NZ Post. That changed days later to implicitly guaranteed by NZ Post, ACC and NZ super fund. i.e. Possibly less guaranteed than previously.

Anyway, that era has now come to an end. (Or will do in a few days time).

Instant change on the moisture map!!!.... if you did not see last week, the whole NI was deep red on Thursday or Friday. With more rain coming I am expecting to see almost completely green within a week. Northland still lacking I think.

Plenty fell here in Hawkes Bay over the weekend, to the point I even have some ponding in a couple of paddocks again. While I'm very happy to see it, I know others have been suffering terribly. Thoughts are with those who got far more than needed.

There is a saying, there is more money in mud than dust. Sounds right

Yep, here in Napier, the Mrs and I joked about the flooding we had about 15 or so months back which was described as a once in 100 year event. Once every 15 months more like it......but then it wasn't as bad as that 15 months ago - but for a while it felt like it could be!

Northland's been lacking for a while now.

High chance of a good 30 to 40 this week. Also could evaporate as so often happens.

I've got more faith now that one has actually come true.

Article on construction headwinds. Of course, it takes an economist to be perplexed by it.

https://www.oneroof.co.nz/news/40848

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.