ANZ New Zealand, the country's biggest bank, posted a 2% drop in annual profit as expenses rose faster than income, losses on hedges used to manage interest rate and foreign exchange risk rose, and its net interest margin fell.

ANZ NZ's September-year net profit after tax fell $44 million, or 2%, to $2.091 billion from $2.135 billion the previous year.

The ANZ Group reported a seven basis points fall in its NZ unit's annual net interest margin, the difference between the interest earned on lending and the interest paid on deposits, to 2.57%. ANZ NZ CEO Antonia Watson says was caused by costumers' preference for higher earning term deposits and "sharp price competition."

Operating income rose $33 million, or 1%, to $5.046 billion with net interest income rising $77 million, or 2%, to $4.316 billion. Operating expenses rose $101 million, or 6%, to $1.760 billion which Watson attributes to "inflationary pressures on staff and vendor costs."

ANZ NZ's cost-to-income ratio, as reported by the ANZ Group, surged 230 basis points to 38.8%.

The bank's credit impairment charge fell $139 million to $44 million. However, its fair value losses on economic hedges used to manage interest rate and foreign exchange risk rose $68 million, or 54%, to $195 million.

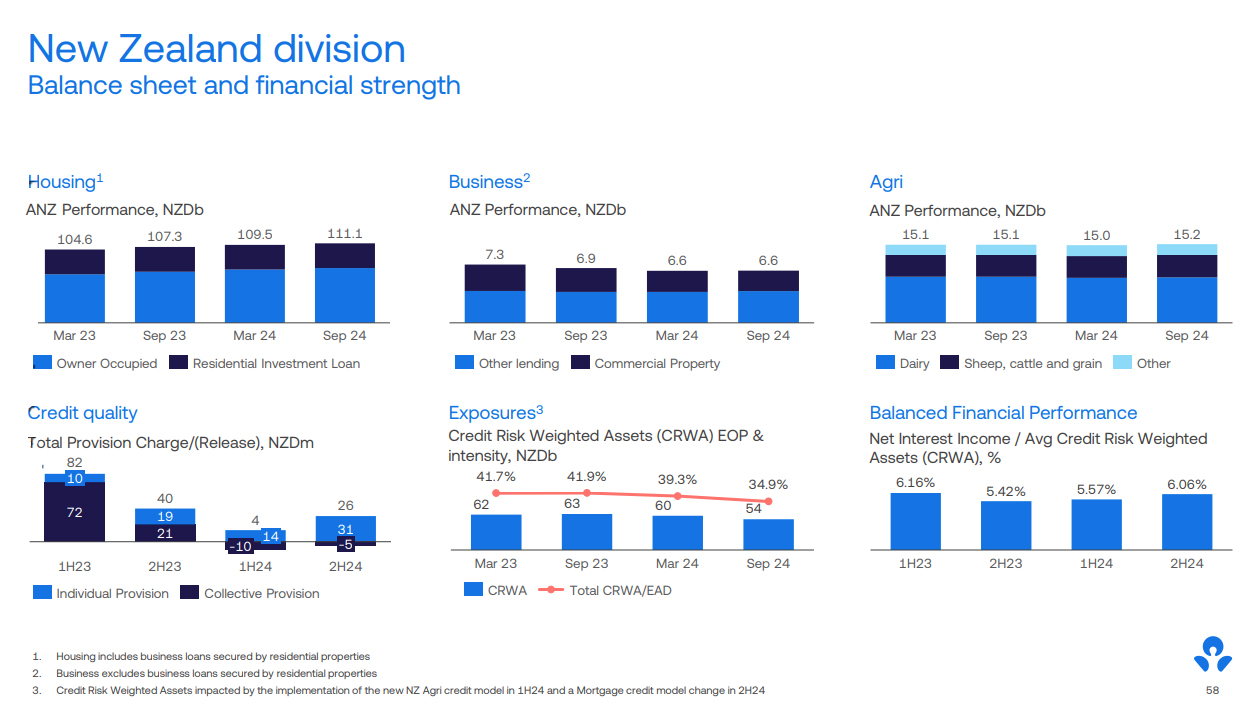

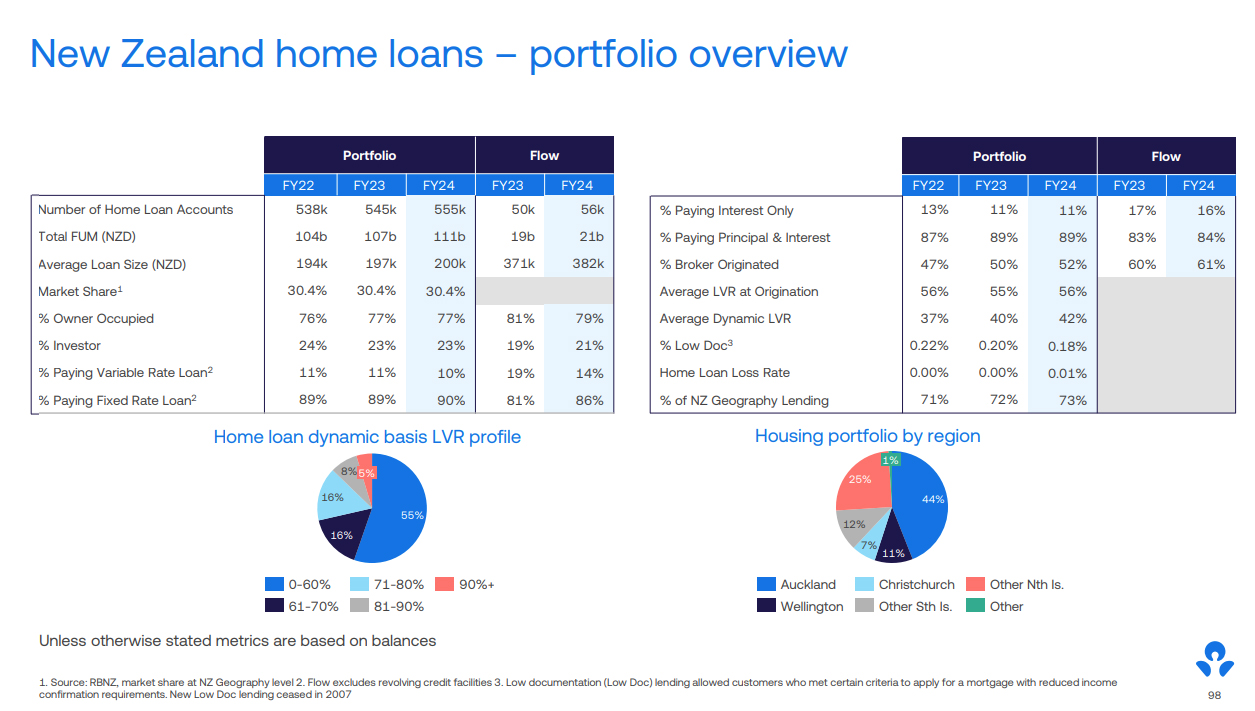

Home lending increased $4 billion, or 4%, year-on-year to $111 billion. Deposits rose $3.34 billion, or 3%, to $109.8 billion, whilst business lending "remained subdued," Watson says.

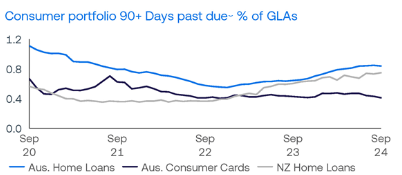

She says about 29% of ANZ's home loan accounts are ahead by six months or more, with more than half of customers having a savings buffer in place with about 20% regularly contributing into a savings account.

"As interest rates come down, inflation is controlled and businesses feel more confident, there is a sense of cautious optimism surrounding New Zealand's economic future," Watson says.

For its personal banking unit ANZ NZ says annual profit rose $1 million to $1.130 billion, while at its business and agriculture unit profit fell $14 million, or 3%, to $530 million. Institutional banking profit climbed $31 million, or 6%, to $573 million.

The ANZ Group, meanwhile, posted a 9% drop in annual cash profit to $6.725 billion. Its net interest margin fell to 1.57% from 1.70%, and its return on equity dropped to 9.4% from 10.5%. The Group's cost-to-income ratio rose to 52.3% from 49.5%. It's paying annual dividends of A$1.66 per share, down from A$1.75, which is equivalent to 76% of profit.

*The charts and tables below come from the ANZ Group.

ANZ NZ's press release is here.

37 Comments

Our largest trading partner is quickly weaning itself off of our exports unable to rejig its lacklustre economy despite throwing the kitchen sink at it.

Our second-largest trade partner is also seeing rapidly dwindling export orders. Our third-largest trading partner will soon slap painful tariffs on us.

Nothing our almighty central bank cannot fix with a hearty cut in domestic rates, am I right?

You're starting to catch on, yeah.

😎

Some interesting crystal ball gazing.

It's time for Orr and his friends to play a game of slashy slashy cut cut.

for the medium term?

Inflation in the 3's. To slowly eat away at the existing debt.

Mortgage rates in the 4's. To make debt servicing manageable

NZD in the mid 50's. To devalue the debt in USD and make our exports more competitive.

Alternative headline - ANZ profit remains pretty much the same at $2.1 Billion

The ASB TD rates are still holding for the 6 month anyway. I would have thought they would all be getting a real kicking by now. There must be another rate cut coming this month, its going to be a hard call to make now Trump has got back in however he doesn't actually take office until the end of January so maybe the RBNZ can stay on track and revaluate things in February.

Over-indebtedness is a huge problem and we need to take ownership of it - and fix it.

Slashing interest rates is not the solution. Rather, it will make matters worse. As we have seen, NZers get addicted to cheap money and all hell breaks loose.

TTP

The cost of debt has increased significantly yet there is barely a mortgagee sale to be seen, doesn’t that suggest we don’t have a debt problem?

See above. Some of our BORROWERS are ahead on their mortgages. Some of our CUSTOMERS have savings accounts and some of them actually put money in their savings accounts. So move along, nothing to see here.

What there is to see, WestieAJ, is huge......

Before jumping to conclusions, take a look at the national debt figures. They're mind-boggling.

Further, you need to be circumspect: mortgagee sales aren't a comprehensive measure of the problem.

TTP

Sorry, I was trying to be as clever as the ANZ Comms team that constructed that sentence. I know there is plenty to worry about.

No problem, Westie. You write worthwhile posts!

TTP

@TTP

nz debt per capita was $13,800 in 2023. Are you saying that this is huge?

When household debt to income is north of 160%, it's somewhat of a problem. The MMTers think this could be easily solved. I'd like to believe them, but I'm still waiting on a convincing why and how.

Its been 160% for almost 20 years now. How long before we can say "hey maybe that isn't a problem"?

Good question. And why can't it be 200% or even 300%? I don't have the answer as to why that's not feasible. All you seem to need to do is rejig benchmarks in lender frameworks and borrower mentality considering the money supply is infinite.

Well all the 5-year-olds and 95-year-olds better go and get jobs so they can pay off their share.

Maybe we don't on a micro individual basis and certainly from a banks perspective there is no problem. But on a national basis going forward where such a huge proportion of our pitifully small productive capacity is used to pay the collective interest bill, yes we have a debt problem.

Is debt a problem if you can afford the repayments? Some would call it an investment.

Some choose resolute ignorance

And spout foolish comments as a result.

Read the most recent post here, and compare to your comment

Surplus Energy Economics | The home of the SEEDS economic model – Tim Morgan

Or is your income dependent on peddling a message?

No my income is not dependent on peddling a message. But I do tire of the comments that debt is always bad. Debt can be bad, it can be very good too.

In terms of energy, we've been burning up fossil fuels for over a century, and during that time many people / countries have used debt to make themselves wealthier. What makes you think that has changed as of today?

Do you not see how ignorant that question is?

It's a finite resource.

We're halfway through it (the best half, net energy-wise).

Those folk used debt to track growth - in real activity. On the way up, you could issue ever-more, and either real-activity growth or inflation dissipated it away.

Except not since at least 2008 - and arguably before - since which it has taken more than $1 of debt to register $1 of GDP (and GDP is false accounting anyway). As the net energy (original joules minus extraction-processing-delivery joules and minus entropy-parrying - maintenance - joules) falls away from peak - an inevitability and no scalable alternative exists - the ability to underwrite debt becomes impossible, and ever-more so

But to write that post, you have to have not read the link - and that's what amazes me about you; the ability to assert while choosing not to learn.

@ powderdownkiwi - So you provide the problem. What's a viable solution you can offer?

Fair enough. Firstly, viable doesn't mean 'this economy', OK? It means physically maintainable in the long term (lots of folk run away if you suggest BAU isn't viable...).

Growth (physical, and ultimately virtual expects to be spent on physical too) is not possible forever within a Bounded System (That's Systems 101).

So we need to concoct one which doesn't grow physically - but of course, social and knowledge growth can still exist, unlimitedly.

Others have had to do this; desert cultures - with not enough resources to support compound growth - stipulated a no-interest financial arrangement. You could charge a flat fee, but not compound interest. Given that interest only allows bankers to tap into the physical stream (buy stuff), that shouldn't worry the rest of us. There isn't enough planet to assuage the current collection of debt, so adding to it - especially virtually - should go.

Also, other rentier-ing should be phased-out or outlawed; money should be related to something real - I've long advocated the Joule, and it's not an original idea by a country mile. (Ironcally, there might always have been enough gold to facilitate global trade at a sustainable level).

We work out what is a sustainable - as in long term maintainable - materials circulation rate. We work out what we can harvest from the solar input (the only incoming energy source) and divert to our needs, again long-term - without repercussions (like ice-melt). Then work out your desired per-head consumption - and you'll be blown away by how few people the planet can ultimately support.

There will be a massive exodus from cities - they needed fossil energy - and a re-skilling in useful jobs; lots in food production (the demise of Haber Bosch tells us this; an energy displacement to labour, of monumental proportions). Many things we think of as 'jobs', will turn out to be discretionary rentier-ing, to the dismay of those who thought they were doing something real.

Simple, really. And quality of life doesn't get measured in dollars - ask any rich person coming out of Oncology with a 6-week prognosis. The happiest cultures I've visited - and I've sailed to a few - have been the poorest.

Thank you for asking :)

@ powderdownkiwi - So anotherwords:

The solution to our societal problems is not the economy, which is based on debt.

Is not to focus on growth but rather find some sort of a happy medium & just stick with it staying stagnant & consime minimalisticly

Trade using knowledge & an exchange of skills, rather than finite physical resources in a non financial arrangement. A sort of "You scratch my back & I'll scratch yours" type arrangement instead, essentially doing favour's for each other in exchange for other favour's. This would some sort of social credit, rather debt credit.

But then a flat fee could potentially be added, but with no compounding interest. Just a simple fee for a service exchange.

Renting should be phased out & outlawed, but unsure what we would replace it with, or how these people would be housed, if it were up to them to source their own housing or if housing was supplied but for only a flat fee, or for an exchange of services or sustainable materials.

We instead spend our times finding & harvesting only sustainable materials on a needs only basis. We work that out by calculating the sustainable material per head. We find too many people, too little resource, so the only option is de populate. But how? And by how many? And who do we choose stays to reap the benefits of the finite resources on a needs only basis?

Mass evictions from cities to the outer country to harvest sustainable materials. Up skill these people to harvest off the land, essentially turning everyone into farmers as the only business profession. But of course they'll do this for a flat fee, or harvest one sustainable material in exchange for someone else's harvested material, in an exchange of goods in farming for a needs only basis.

"Simple, really. And quality of life doesn't get measured in dollars" - Well, after breaking down your answer, what are we all doing wasting precious time chasing such idiocracy ideas such as money to fund passions & thrive on life. Whay a waste. Our time, apparantly can be better spend instead all becoming farmers farming for each other in a non for profit exchange of materials only to be consumed minimally on a needs only basis.

When put like this, your essentially saying to reduce quality of life & the purpose of one's life to simply a needs only, in order to survive, nothing more. Take only what you need & only if you have either harvested it yourself physically as real work, or have exchanged it. Turning people into boring mindless cattle powderdownkiwi? The old herd immunity must be amoungst the buzzwords.

Feel free to re eloborate if I have mis inturpreted, but what a terribly boring life! Essentially it dulls the purpose of life to nothing more than an organism, just surviving on only what it needs, that's it. And all for what? To keep the planet alive? So that others may also do the same? Then of course there's the issue you mentioned of too many people, too little finite resources. The elephant in the room of course is to depopulate, but of course no one wants to say how, as we all know any way it's done is cruel.

The joke is that you - I'll forgive you for being new here and not knowing much - probably live a more boring life than me.

And the joke is, I pursue low-impact.

:)

You raise a valid question re the future - yes, I believe we have an obligation to leave things as close to how we found them, for who and what ever follow. Or what's a reproducing species for?

@ powderdownkiwi - "The joke is that you - I'll forgive you for being new here and not knowing much - probably live a more boring life than me."

Ya reckon powderdownkiwi? Couldve fooled me. What makes your life so interesting? Someone who advocates for a minimalistic "needs only" "non for profit" life, think your perception of interesting would rather differ from mine.

"I believe we have an obligation to leave things as close to how we found them, for who and what ever follow. Or what's a reproducing species for?"

Leaving things how they are for whay reason? So people can do what? Leave it how they found it? Then pass the baton on to the next generation so they can also leave things how they found them? Again, round & round in circles, but all for what? People are born, told to consume little, profit none, work physically hard, then die & pass on the baton to the next generation to do exactly the same? Essentially just like an organism, is what you are reducing human life down to.

So anotherwords you feel the only purpose to life is to survive? Purely just to keep the human race going? For what purpose? For how long? What's the cut off point? This directly contradicts your hinted suggestion of de population. Leaving things as close as we found them is to not consume resources, & most especially not to reproduce, as that means more people consuming.

Yeah nah there absolutely no way your life is in any way interesting. You can't have interesting & "leave things as they are", consume minimalisticly, & all out of non for profit.

To be clear, my previous comment I didn't call your life boring, I said the ideal life you pitch for humanity sounded boring, especially when you've essentially reduced life to a mere survival organism, like some kind of jellyfish. Thought humans were more intelligent, were made for more than just that. But according to you, we're not.

Good luck to you

:)

Perhaps you need to quit posting evidence PDK and tell us when the worlds going to end or else to be honest nobody is interested.

That isn't the choice.

This 'economy' is doomed. And, as a species, the sooner we construct something different, the better.

Does that truth diminish because I don't give you a specific day? I can give you a decade - we're into the last one. My pick is implosion prior to 2030 (or war, diverting the plebs). I think that's soon enough to sound the alarms as loudly as possible.

The person interviewed here, I'm guessing has little or no cognisance of what I'm on about (and probably couldn't admit it if she did). I think we can do better than take the word of such people. Yes, there will be a cohort who wish not to know - but has chosen-ignorance ever been a reason to go silent?

@ powderdownkiwi - The economy is doomed? And yet you still offer no viable alternative?

"And, as a species, the sooner we construct something different, the better." - & what would that look like?

"Does that truth diminish because I don't give you a specific day?" - No, but Spouting out "the worlds going to end, it's all going down, our money system is stuffed" isn't very constructive. Everybody is going to die some day, albeit from finite resources or something else. So what? What are you suggestion as an alternative?

"My pick is implosion prior to 2030" From what?

You may have brilliant & key information, but it's poorly communicated Powderdownkiwi. Screaming out "we are all doomed, the sky is falling" is a doomsdayer. It's not constructive. You offer the problem, but fail to produce a viable alternative, then get offended when people ask you for one. You have an opportunity to explain yourself in lemens terms so that others around you understand.

"The person interviewed here, I'm guessing has little or no cognisance of what I'm on about (and probably couldn't admit it if she did)." - At this stage I don't even think you know what your on about. I get glimpses of an environmental nut who turns everything into a nature debate. Hug a tree, whisper admirations to some plants, be one with nature & all that right. You'll feel better.

"Yes, there will be a cohort who wish not to know - but has chosen-ignorance ever been a reason to go silent?" - That's not it at all. It's just that no one actually knows what your on about, including yourself so it seems. Stay relevant?

Your using a lot of words, but it doesnt seem as though a lot is actually being said. Smart people have a way of making complicated things sound simple, stupid people have a way of making simple things complicated. Use your words powderdownkiwi, it's the most powerful thing you have.

I don't think you have any idea about what you shunt out via a keyboard. It's just all unsustained verbage. I note that in the 000s of words you have written in the last few days there has been no source, reference, link or justification. Typical of the conversation in a 1950's public bar at 5.30pm.

When you have asked the questions, done the required research, read the journals, tested the hypothesis' in real time, evaluated the results and modified your original posit then you can make informed statements such as those by PDK and others. PDK's alternatives are filed in writing on the Interest.co website. Spend the weekend reading.

The only message you need be cognizant of for your immediate future is that you will have to make do with less. And you will have to do all the above in order to survive at the level you are accustomed today. It is not going to be easy and you and your cohort will be the first to scream," but you didn't tell me this was going to happen."

In the land of the blind the one eyed man is king. There are others who think otherwise

Sitting in your bunker on the morning of 01/01/2030 with your arms crossed and a big frown on your face when the world hasn’t collapsed 🤦🏻♂️😂

You might be absolutely bang on…and I’m just too optimistic…guess we’ll find out eventually

I often hear that.

I cite the Titanic - there was a big enough sample of people to be representative - uber-rich, uber-smart, talented, optimistic, pessimistic, deluded, believers (same thing) and so on.....

The point is that physics overrode the lot - optimism is irrelevant; money was no use (although the pushy survived in larger percentage, true).

All the banks are spending more in the last week of their FY so as to report ever so slightly lower profit than previous year so the politicians, journalists & public forget about their excessive, outrageous, uncompetitive, rorting profits

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.