Unbundling transactional services, lending products and investments is an area of banking services meriting more consideration from a competition perspective, the Reserve Bank (RBNZ) says.

The RBNZ makes this point in its submission to the parliamentary inquiry into banking competition.

As it did with the Commerce Commission's recent market study into personal banking competition, the RBNZ has proactively released its submission to what's likely to be a politically charged parliamentary inquiry. The deadline for submissions was Wednesday this week, with the RBNZ submission publicly released Thursday.

The RBNZ is under political pressure. After the Commerce Commission issued its final report, Finance Minister Nicola Willis said while the RBNZ's task of maintaining financial stability is "critically important," its settings are conservative by international standards. Willis said she will issue a new RBNZ Financial Policy Remit this year to make clear the Government’s expectations for it to support a more competitive banking sector.

Among other things the parliamentary inquiry intends to probe why banks favour housing lending over lending to "the productive sector." Its terms of reference are here.

'Disrupt the structural advantages'

In its submission the RBNZ argues open banking and the unbundling of services could disrupt the structural advantages of incumbent banks.

"One aspect of competition for banking services that we suggest deserves more consideration is the possibility of unbundling the key roles of ‘transactional services’, ‘lending products’ and ‘investments’, which may be enabled by progress towards open banking," the RBNZ says.

"A classic banking model is for deposits, both transactional and term deposits, to fund lending. As noted in the Commerce Commission’s final report, high levels of customer inertia are a barrier to the competitive process, particularly in giving incumbent banks a low-cost source of funding through deposits."

"In some other countries much lending is securitised, sold to investors who may hold those interests instead of holding term deposits. It is also possible for providers of ‘securities accounts’ to offer limited transactional services linked to the securities account, e.g. a debit card that can be funded when needed by selling securities, potentially offered by a new technology or ‘fintech’ firm that makes managing this easy. Similarly, deposit broking services can help to improve returns and competition by seeking out the best deal for customers," says the RBNZ.

"Growth in these channels, enabled by progress on open banking, would allow increased competition in the loan origination market, since it is not necessary to build a deposit base to lend. The loan originators do not require a deposit-taking license. The provider of the transactional account would need to deposit transactional funds into a client money account run by a deposit-taker, but the provider does not need a deposit-taking license itself. Even while they are reliant on a deposit-taker, they may be able to negotiate more effectively on behalf of their clients than the clients could individually. ‘Unbundling’ could have the potential to increase competition across all key deposit-taking activities."

The RBNZ notes the four big banks - ANZ NZ, ASB, BNZ and Westpac NZ- account for about 85% of the roughly $706 billion deposit-taking sector.

RBNZ highlights its proposals that'll 'have positive competition benefits'

Elsewhere in the submission the RBNZ notes changes being introduced under the Deposit Takers Act (DTA). These include a proportionality framework based on grouping deposit takers into three size bands to influence how the RBNZ designs the standards that apply to deposit takers under the DTA.

These size bands will see Group 1 featuring deposit takers with total assets of $100 billion or more. This is just the domestic systemically important banks being ANZ NZ, ASB, BNZ and Westpac NZ.

Group 2 is deposit takers with total assets of $2 billion or more, but less than $100 billion which includes Kiwibank, TSB Bank, SBS Bank, Heartland Bank, and the Co-operative Bank. Group 3 is deposit takers with total assets of less than $2 billion, including non-bank deposit takers (NBDTs).

Proposals the RBNZ is consulting on, or plans to consult on, it says will have positive competition benefits include:

Graduated capital requirements across groups of the proportionality framework, meaning smaller firms have lower requirements.

Reduction of the minimum capital requirement from $30 million to between $5 million and $10 million, reducing the initial entry hurdle for a deposit taker.

Considering broadening the criteria for use of the term “bank”.

Introduction of the Deposit Takers Compensation Scheme (DCS) ... the protection provided by the DCS is likely to make smaller deposit takers more attractive by reducing risks depositors face, and incentivising depositors to spread deposits across a number of institutions.

Review of elements of standardised [regulatory capital] risk weights to ensure they reflect risk (e.g. across mortgage loan-to-value ratios, community housing providers and lending on whenua Māori).

Recovery and resolution planning, to enable managed failures of institutions, supporting the exit of uncompetitive entities while reducing contagion risk across the system.

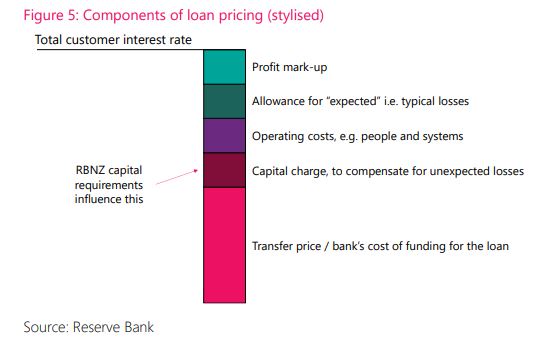

'The contribution of regulatory capital requirements to differences in overall loan pricing is small'

In the submission the RBNZ also explains and defends the role of regulatory capital requirements. It suggests even without these, banks would choose to operate with "some level" of capital to remain a going concern and attract creditor confidence over economic cycles. They would also need to assess the relative riskiness of their lending and assign capital to it, the RBNZ says.

"Our analysis concludes the contribution of regulatory capital requirements to differences in overall loan pricing is small – in the order of 50 basis points between residential mortgages and rural lending, for example. We observe wide differences in loan pricing between categories with similar risk weights applied to them – for example, in June 2024 large corporate loans and loans to SMEs had similar average risk weights in the Internal Ratings-Based approach [used by the big four banks of] 57% and 55% respectively, but average contracted interest rates were 6.5% and 12.2%. These illustrate that loan pricing reflects a far wider range factors than regulatory capital requirements alone," the RBNZ says.

It also argues that lending to one sector doesn't come at the expense of lending to another.

"Moreover, we would emphasise that banks’ balance sheets are not static, and their lending allocations are not a zero-sum game. Banks can build their capital resources over time to support new lending where they see it as profitable to do so. Growth in residential mortgage lending does not come at the expense of lending to the rural sector," the RBNZ says.

Customer inertia

In a press release accompanying the submission, RBNZ Deputy Governor Christian Hawkesby notes the Commerce Commission’s market study highlighted high levels of customer inertia as a key barrier to competition.

"Efforts to reduce real and perceived barriers to switching banks and supporting innovation through open banking is key to promoting competition," Hawkesby says.

He also describes regulatory capital requirements as an essential tool to promote banks’ financial resilience.

"Capital is the funding of a bank from its owners, and acts as the buffer protecting creditors such as depositors from losses. Our framework is based on matching the level of capital required with the underlying risk of a bank’s lending through the use of risk weights. This is consistent with global practice," Hawkesby says.

The RBNZ also issued this Bulletin article on capital risk weights.

3 Comments

" Lowering risk weights to promote lending in particular sectors .... could undermine financial system resilience. ....initiatives such as government guarantees can reduce the amount of capital needed for certain loan types by reducing the underlying risk faced by the lender. This has the effect of reducing risk weights without undermining bank resilience."

It would be handy to have an explanation, (or justification, more like) of what "particular sectors" and "certain loan types" are. Otherwise, we are no better able to form an opinion than before. And if my underlined word could, above, is actually 'has', then we are in heaps of strife, probably caused by overlending to one of the "particular sectors"

Lowering risk weights to promote lending in particular sectors .... could undermine financial system resilience. ....initiatives such as government guarantees can reduce the amount of capital needed for certain loan types by reducing the underlying risk faced by the lender

Hilarious when you look at how much the banks made off with from the FLP, LSAP, and removal of LVR restrictions in 2020, and now they wish to have government guarantees in case the proverbial hits the fan because they pushed loans as hard as the possibly could to maximise on profit because 1. this is their goal of being in business and 2./ the government gave them the likes of the FLP to promote lending to a particular sector....residential housing...which distorted the market...

Alternative mainstream saving products to term deposits would help enormously.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.