The Reserve Bank (RBNZ) has released details of what it believes to be the first published study on New Zealand non-performing loan (NPL) data, noting NPLs could increase 0.4 percentage points to as high as 1% by the end of the year, and if mortgage rates rose by about one percentage point from where they are now, loan defaults could surge 20%.

This comes from an RBNZ analytical note; Beyond the crystal ball: forecasting nonperforming loans, by RBNZ Senior Analyst Tyler Smith. Smith says although there've been plenty of studies overseas and by trading banks analysing the drivers of NPLs and using models to forecast them, his one appears to be the first published study on NZ data.

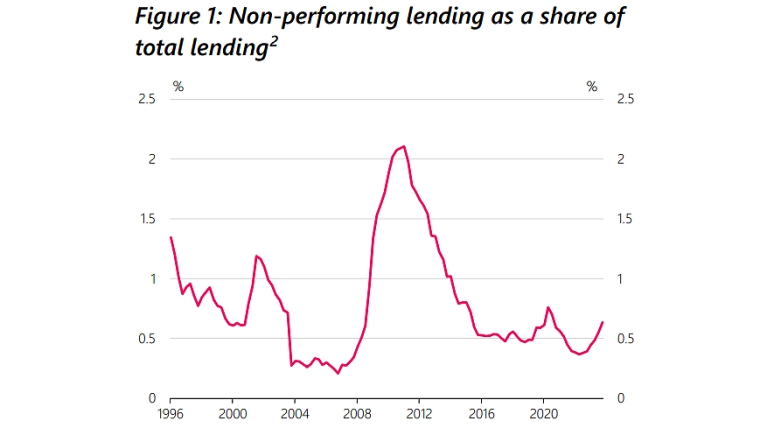

As Smith puts it; NPLs are lending where a financial institution is likely to incur some losses, i.e. the borrower is likely to default on the loan. And the NPL ratio measures the value of NPLs compared to the value of an institution's total loans.

"Whilst this metric is quite a lagged indicator of stress, it is important because lending that becomes non-performing and eventually defaults can result in a loss for the financial institution if the value of the seized collateral is insufficient to cover the value of the loan. An increasing or high NPL ratio illustrates that lenders are facing more defaults, which could reduce their profitability, their solvency and their ability to obtain funding. As a result, a large increase in NPLs could reduce lender’s willingness and ability to continue supplying credit to households and businesses, which would have negative impacts on the real economy," Smith writes.

He goes on to say NPL ratios are impacted by the general state of the economy, with higher interest rates potentially resulting in borrowers facing budgetary constraints, making them reduce discretionary expenditure or increase their hours worked.

"Similarly, a deterioration in economic activity resulting in less revenue for businesses could also constrain business profit margins and erode cash reserves. If these deteriorations persisted, then temporary support measures provided by their lending institutions such as extending the term of the loan or switching to only making interest payments, instead of principal and interest, may be insufficient to prevent the borrower missing obligated repayments, eventually resulting in the lending becoming non-performing. Given this, we might expect a relationship between the current economic indicators and the outlook for NPLs."

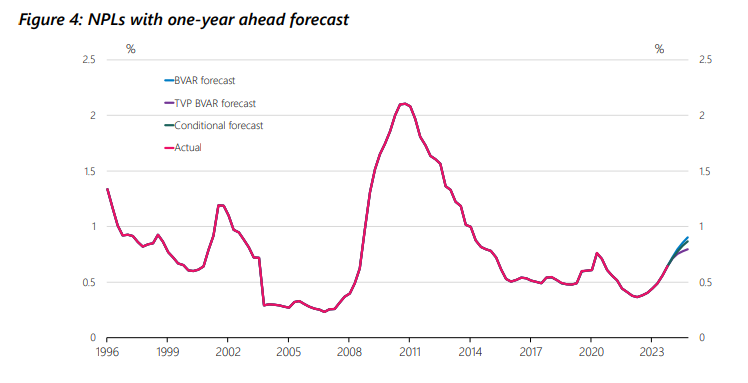

Against the current economic backdrop, Smith suggests NPLs could rise by a further 0.4 percentage points to between 0.7% and 1% [depending on the forecast, see Figure 4 below] by the end of 2024.

"This would still be lower than the peak of NPL in the aftermath of the Global Financial Crisis, giving confidence that the New Zealand banking sector is in a strong position to weather the challenges on the horizon whilst continuing to support customers facing financial difficulties," he says.

Smith says the combination of relatively high interest rates and low unemployment makes the current economic environment unique in recent NZ economic history, suggesting the pattern of future lending stress may be different to what's implied by historical relationships given these don't capture the impact of now significantly higher debt servicing costs.

"The analysis in this note has been undertaken over a period of a general trend downward in interest rates since the early 2000s which may present a modelling challenge. During the 2022 solvency stress test New Zealand’s largest four banks explored this issue in the context of higher interest rates," he says.

In the stress test banks had to undertake a sensitivity analysis of mortgage default rates to changes in interest rates, assuming all else was unchanged.

"Over the four-year stress test period, the level of defaults increases by approximately 30% when the mortgage rate increases from 4.5% to 7%. Defaults increase by 50% when the mortgage rate increases from 4.5% to 8%. This indicates that as mortgage rates move higher, particularly above 7%, there is a non-linear increase in lending defaults," Smith says.

"This non-linearity is consistent with the range of affordability test rates large banks have used since late 2020 to mid-2022, mostly below 7%, to determine whether to lend to a mortgage applicant during this period. Debt servicing strains are likely to become more acute as interest rates move above the original affordability test rates, which in this period were mostly below 7%."

"Using this sensitivity analysis as an approximation for the expected increase in NPLs resulting from higher interest rates, then defaults should increase non-linearly as mortgage rates rise above 7%. This suggests that if mortgage rates rose by around another one percentage point from around where they are currently then defaults could increase by 20%. While this is an imperfect approach to modelling the relationship between economic conditions and NPL, it does provide a more complete estimate for the magnitude of increase in NPL which could arise in this economic environment," says Smith.

The current average bank one-year mortgage rate is 6.83%, two-year is 6.47% and three-year is 6.33%.

*Figure 4 below comes from the RBNZ analytical note.

*This article was first published in our email for paying subscribers early on Thursday morning. See here for more details and how to subscribe.

6 Comments

I have a concern that the NPL metric isn't giving us an accurate view of what's happing with risk for these banks' loan books. I don't have any data to back up that fear, but there it is...

Hopefully banks understand they provided mortgages to people who have seen house price’s crash 20% from highs. Even with 20% falls average wage earners still have no chance of purchasing a home in many areas. House price’s look certain to continue downward trend.

RBNZ : When is a loan impaired or non performing?

Banks : Only when we have exhausted all possibilities and time available to say it isn't.

RBNZ : OK

Which is what I said yesterday, the RBNZ maxed the OCR to what the property market could take, it was obvious or else rates would have gone to 10% and spent much less time there than the current 7% rate. We had higher for longer or else the defaults would have gone off the scale.

Nice to know the RBNZ has fine grained measures to ensure they squeeze as much as possible from the have-nots to ensure the haves get as much as possible at the least risk.

There will be a higher probability of loss and loss given default on loans made in the 2020 - 2022 period where the bank stress test rates were lower than current mortgage rates.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.