Although today's (Monday) financial markets are not closed yet, wholesale and bond market trading suggests interest rates will be a little higher yet again, especially at the short end.

The short (one year) end is the part of the rate curve more susceptible to the Reserve Bank's policy rate moves.

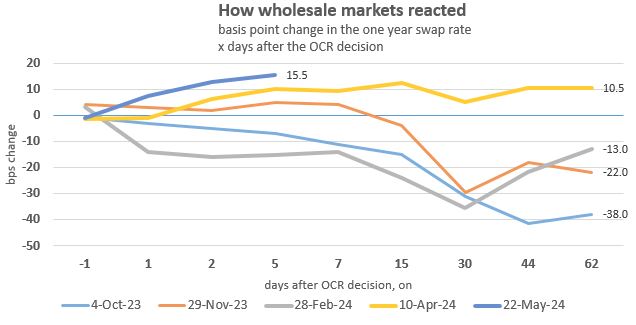

And the May 22 Monetary Policy Statement (MPS) has been widely interpreted as being more hawkish than markets had priced for.

In fact, we had a sharp rise in wholesale rates immediately after that MPS release.

So it seems appropriate to assess how markets responded after previous MPS/monetary policy rate signals. We have looked in detail at movements after all such regulator statements since February 23, 2022, that's 17 of them. The first 10 of those brought signals with an Official Cash Rate (OCR) rise. The next seven have brought no OCR change.

The reaction after the May 22 signals (last week) is unique in that it has brought by far the largest market reaction when no change was delivered or even signaled.

Five days after that, one year swap rates are now almost 13 basis points higher that on the day. That is half way to another 25 basis points hike.

This needs to be seem in light of the previous OIS (overnight index swap rate) pricing that expected two 25 basis points cuts by the end of 2024.

Now only one such cut its priced into OIS rates by the end of 2024 and no longer fully priced (ie less than 25 basis points).

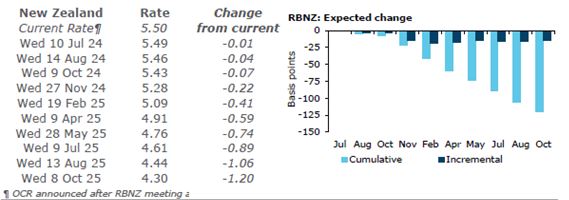

Monetary Policy Expectations

Source: ANZ

The difference between the two signals is large.

There is no point speculating where the one year swap rate will move to - there is much data to come between now and the next MPS on August 14. There will be a Monetary Policy Review that brings a short statement on July 10 which can also be used to signal policy intentions. Intermediate speeches and statements are another way to interpret what the Reserve Bank is thinking.

The purpose of this note isn't to draw any specific conclusions; it is only here to keep you up-to-date with market reactions after the latest MPS. These are important because they have a background influence on retail rate setting for both term deposits and home loans. But they are only one factor. (Competition is the major factor, don't forget).

2 Comments

Reserve Banks should have been talking about doing "whatever it takes" to tackle inflation not talking about the possibility of rate cuts based on a very long term forecast of regression to previous trend. They couldn't firecast Christmas.

Sep 23 CPI 1.8, Dec 23 CPI 0.5. Why is the expectation for a return to the target annual range now the end of the year? If the 1.8 rolling off in Q3 doesn’t see a return to 1-3% then it’s unlikely to be seen in Q4.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.