Last week was Te Wiki o te Reo Māori, Māori language week, and coincidentally, one of the papers at the recent excellent New Zealand Law Society Tax Conference covered taxation and Māori business.

One of the more fascinating papers prepared for the last Tax Working Group was about considering the tax system from our Māori perspective.

It was therefore quite opportune and appropriate in Te Wiki o te Reo Māori, for the New Zealand Law Society Conference to cover the question of taxation and Māori business. As a supporting paper noted, in 2018, the Māori economy was estimated to have an asset base of nearly $70 billion, and it's projected to reach $100 billion by 2030. So this is something we're more likely to encounter as the Māori economy grows.

The presentation gave a fascinating background into what structures are developed as part of a settlement agreement between the Crown, and these post settlement government entities or PGSEs can be a very unusual mix of trusts, companies, limited partnerships and Māori authorities.

Māori authorities – a template for a difficult tax issue?

Māori authorities in particular, have very specific tax treatments and one of those includes the ability to distribute capital gains without liquidation. Which, as a presenter suggested, could perhaps be a model for companies as this is presently quite a difficult tax area. At present if a company has realised a gain then, unless it's a look through company, you would have to liquidate the company in order to extract the gain without triggering an immediate some form of tax liability. As I said, it's an interesting area of growing relevance. I think if you can get hold of the paper, do so.

Time to raise the GST threshold?

The accounting service provider Hnry released a poll which indicated that almost a third of sole traders in the country are choosing to earn below the median income to avoid passing on costs, because otherwise they would cross the GST threshold of $60,000 and have to register.

Their concern was that the 15% that they would have to apply to their pricing at that point was a cost they simply could not pass on.

This has sparked a debate about whether the threshold is presently too low. It was set at $60,000 with effect from 1st April 2009. Given that's now 15 years ago, an increase seems logical and based on CPI for example, it should be closer to $87,000. It’s not unreasonable to consider an increase. As I've said in other episodes, we seem to have an inbuilt reluctance to regularly look at thresholds and increase them for inflation. That leads to all sorts of difficult issues cropping up within the tax system.

On the face of it, an increase in the GST threshold is not unreasonable. I think somewhere around the point where the income tax rate goes from 30 to 33%, which is now $78,100 would be appropriate and is also around the median income.

But maybe not?

But there is a counter argument, and a very interesting one too, in that perhaps if we want to have a broad base, we should be lowering the GST threshold. A good example for this counterargument comes from the UK, where they have a very high threshold of £85,000, about $180,000.

According to the UK Office for Budget Responsibility, approximately 44,000 UK businesses will deliberately not grow revenue to avoid registering for Value Added Tax (VAT), the UK equivalent of GST, and which has a standard rate of 20%.

An obvious answer is to raise the threshold, but the counter suggestion made by Dan Neidle of Tax Policy Associates is perhaps it should be lowered. He notes that in Europe the thresholds are much lower, around the €30,000 to €35,000 mark, which is around $50,000 to $55,000 here.

In Dan’s view the registration threshold creates a ‘fiscal cliff’ that some businesses find difficult to hurdle because you aren't able to make a significantly big increase in your turnover to get past the effect on the customers because they cannot bear the cost. He suggests maybe a lower VAT rate might be one solution.

He also notes broader base for GST is important for competitiveness, because if there are people who are deliberately under-pricing themselves because they are not GST registered (as opposed to those who are) then there is a competitiveness issue. Dealing with that is going to be difficult.

I thought it was an interesting counter argument that Dan raised, but it still doesn't get past the issue that a threshold that has not been adjusted for 15 years perhaps should be. On the other hand, comments from Inland Revenue indicate there is no desire to do so at this point. The Minister of Revenue, Simon Watts, has also said it’s not really on their agenda. So, these issues will still remain.

Going underground?

There's one other question I think that does come to mind though. If people are deliberately limiting their income to below the GST threshold, how are they maintaining their lifestyles? Is there a cash economy and tax evasion going on here with jobs being done for cash, which won't go through books. Now I'm not saying it's true for every business below the GST threshold. But given that the median wage is above $60,000, you've got to wonder if there is some element of that going on. We shall see.

Inland Revenue ramping up its investigation activities

That leads us nicely on to another paper from the New Zealand Law Society Conference, which was opened by the Minister of Revenue, Simon Watts. He continues to impress as having a command of his brief and understanding the detail. This is not totally unsurprising, given that he used to be an accountant and began his career as a tax consultant.

Reform of FBT definitely appears to be on the agenda. Inland Revenue are focusing a lot on the near $13 billion of total tax debt that's outstanding across various taxes (including Student Loans) at the moment. There's a focus on what's called high risk debt, particularly in the construction industry. Inland Revenue would be putting more resources into the hidden economy, and the Minister also mentioned the work of the Tax Debt Task Force, which is about 40 people within Inland Revenue, which is now collecting about $4 million per week of outstanding debt.

Interesting to hear this from the Minister and his comments about Inland Revenue’s enhanced enforcement activities was also supported by a presentation from Inland Revenue policy officials. The officials were referencing the search powers of Inland Revenue and two new drafts for consultation which have recently been released.

“Knock, knock”

One is in relation to what are called Section 17B notices, which are issued under section 17B of the Tax Administration Act 1994. These are information demands and they're part of Inland Revenue’s information gathering powers. The more important one is a draft operational statement on Inland Revenue’s search powers.

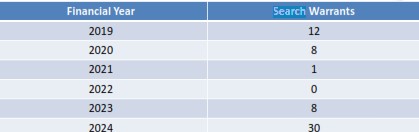

Now Inland Revenue’s search powers are incredibly extensive. To give you an example, there's a Court of Appeal case from 2012 – Tauber v Commissioner of Inland Revenue - where Inland Revenue raided six premises simultaneously. Officials obtained search warrants for these raids, but under Section 17 of the Tax Administration Act 1994 Inland Revenue officials don’t need to obtain a warrant to access property or documents. Documents in this case can include your smartphone.

And this is where we perhaps should be starting to pay a bit more attention, because, as the paper noted, Inland Revenue’s search activity dropped off because of the COVID pandemic. Information obtained under the Official Information Act gives an extent of how this had happened.

From these stats it’s very apparent Inland Revenue is currently amping up its investigative activities. According to the presentation, officers have “hundreds of unannounced visits planned” for liquor stores.

There are over 100 audits of property developers going on at the moment and another 50 investigations underway in relation to electronic sales suppression software.

Now, as previously noted and emphasised by the Minister, Inland Revenue has had a significant funding increase given to it over the next four years. All of this shows that we can expect to see a large amount of increased activity in investigations from Inland Revenue. And we'll also see them taking probably a far harder line in relation to collection of tax debt.

I want to repeat what I've said before, and which was also brought up at the conference. If you run into difficulties with tax debt, approach Inland Revenue immediately. Don't put your head in the sand. It's always best to front foot it and contact Inland Revenue. If you've got a realistic approach to getting out of your tax debt, it will be prepared to put together a plan that enables that to happen.

High earner tax rates – New Zealand in context

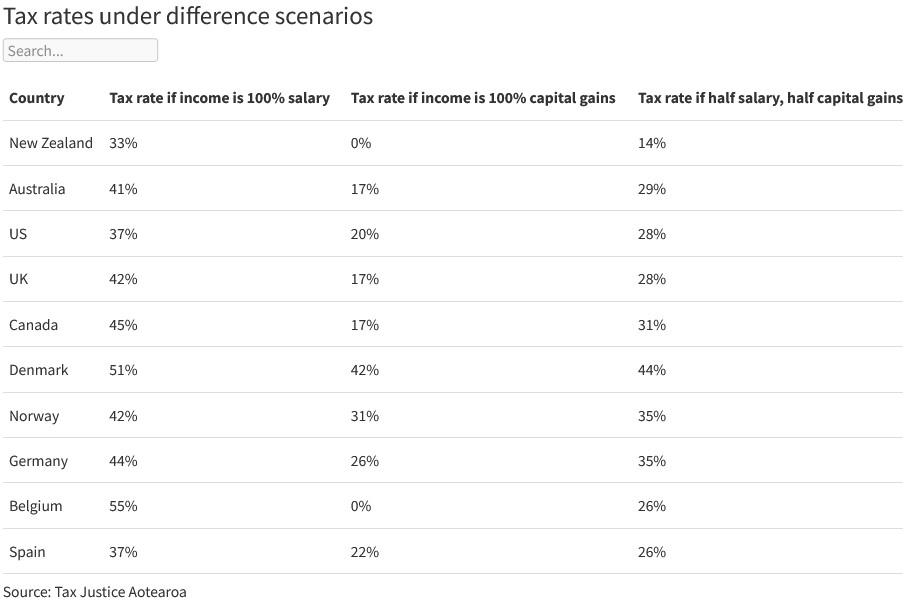

The debate around the taxation of capital continues with a RNZ report involving a Victoria University study, commissioned by Tax Justice Aotearoa, which looked at how much tax someone earning five times the average New Zealand wage (that's roughly $330,000) would pay in nine comparable nations. Those nations include Australia, Canada, the US, the United Kingdom and five European countries – Belgium, Germany, Norway, Spain and Denmark. The study found that there was a quite significant difference between the tax payable in New Zealand and that payable overseas, particularly in when considering capital gains.

Tax Justice Aotearoa are using this data as a counterargument to fears there would be mass capital flight if we introduced some form of wealth taxes. When I was interviewed on RNZ’s Morning Report about the story I agreed with the basic premise of this counterargument. That's not to say there won't be capital flight. There will because people's capital is mobile and there will be people with the resources to migrate into tax havens where there are very low rates of income tax and little or no capital taxes

But not all capital is mobile. Any property they held in New Zealand would still be subject to any form of taxation because the rule around the world is that property is always taxable in the country in which it is situated even if it is owned by a non-tax resident.

A false debate premise?

I also told Morning Report that the premise of the debate seemed slightly off in that if we have a capital gains tax or form some form of taxing capital, we will therefore have capital flight, so we shouldn't do that. In my view this is incorrect, the reason we're having the debate about taxing capital is not because other jurisdictions have such taxes so why don't we? This frames it as a question of equity and fairness.

The issue is the coming demographic crunch and also the more immediate crises we're now seeing regularly of the impact of climate change. How do we have the funds to deal with an ageing population, the associated health costs with that, and the impact of climate change. Last year's Cyclone Gabrielle and the Auckland floods were incredibly expensive events, so this debate isn't going to go anywhere because it fundamentally revolves around the question “We have costs building up. How are we going to fund those?” And that's a debate which will continue.

There isn't a magic bullet here in terms of one tax is superior to all others in my mind. We just have to look at all the options and then decide how we will move forward. But I think it's false to say, well, we can't do anything because people's capital will flee. That's doesn't say much, by the way, for the many citizens of New Zealand who built their livelihoods and have long-standing roots here, but as I said also seems to sidestep the issue as to why we're having the debate in the first place.

And on that note, that's all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

33 Comments

In regard for more government revenue for the "coming demographic crunch" and climate change.

I find it curious that means testing of New Zealand Superannuation is not also part of the discussion. The crown spends about $20B on NZ Super (ref https://figure.nz/chart/2eIStXKBWssxMIze ). If it was means tested as in Australia, one might expect a saving of about 25% - $5B saving ?. That is a large amount similar to the other taxes being talked about. If this analysis is correct it seems a no-brainer and hard for anyone to oppose.

I think a factor that is not acknowledged enough is that in my experience a key reason why people oppose additional taxes is that people don't believe government can spend money effectively and efficiently - I think this really does need to be addressed if there is going to be general support for new taxes.

Something like taxes being ring fenced for certain activities - e.g. 10% of taxes ring fenced for health, infrastructure decisions being taken away from politicians. The track record of government over the last 30 years is very poor - and is probably the first issue that need to be addressed.

There are 50k superannuants that are actually still working and earning over $100k p.a. Collectively that's $1b. Do they really need taxpayer funded welfare?

The biggest challenge is the generational entitlement mentality that has turned a benefit into a loyalty scheme, and people even imply high income earners are more deserving because of how much tax they have paid, while being totally ignorant that tax is proportional to income and the fortune of earning a high income should far outweigh the corresponding tax bill.

It is interesting that Australia, a country far wealthier than New Zealand, still finds it necessary to test their Government pension.

The Australians also have a massively generous super investment environment. As usual, the discussion only ever reaches as far as how to extract more tax from Kiwis, not how to make it actually function.

Taxpayers kicking in $100K are paying pretty much what they get in Super. If they're sufficiently over that amount, they're probably still net contributors. The same can't be said for many other taxpayer funded welfare schemes - most of which are income-capped and effectively limit what people can earn if they are eligible.

As usual, the discussion only ever reaches as far as how to extract more tax from Kiwis, not how to make it actually function.

Because how the revenue is gathered in the first place is to an extent a separate discussion to how it is spent unless you want each comment to be a novel.

It's a separate discussion but the problem is the various other bits of context and reform you need to make it work and the discussion around that never seems to happen. There is a pre-occupation for NZ with downing tools once you've got the 'other countries do x' argument out of the way without appreciating that other countries also have concessions and thresholds to make these things either acceptable to the electorate, or in many cases, not applicable at all.

If you want to income-test NZ Super (and effectively hand a hospital pass to those who were prudent and saved for their retirement) then you need to have a really thumping version of Kiwisaver that's an order of magnitude better than what we have on offer today, with the same kind of tax advantages Australian Super schemes have. Let's figure that bit out first before we do the 'how can we just take stuff from people' bit.

We should try something new now and then and give the horse in front of the cart a go. See how that works out for buy-in from taxpayers and the people who are actually affected by it.

Interestingly NZ has a much higher percentage of people at or over retirement age working. It’s like 26% whereas it is 12% in Aus and 10% in the UK. I wonder if that’s because many have little retirement savings and have to work or if they choose to.

I doubt its choice. If it was, it would be the same everywhere, as people are the same everywhere. However the average super balance for a 60-64 year old in Australia currently is $402k, and for a 65-69 year old its $453k. $1.9M Australians are self funded retirees and not drawing the pension. If you retire wealthy with a nice nest egg, why bother working? That's why Australia has so many golf courses :-)

Australian retirees also have access to a low cost home equity release product, where they can borrow money from the Govt to supplement their pension at 3.95% interest - lower than what they would earn if they put that money on term deposit.

Please explain where we will get the army of accountants from and how we will treat trusts, company income, gifted businesses (including farms) and how you will find out the overseas income of our million new arrivals...

Will you apply interest foregone on cap gain investments?

Will you charge income on the 'loans' or gifts to the kids to buy a home or business?

Will you expect an income form the $2mill holiday home of the 6 classic cars?

Sure, you will get the NZ worker who stays on working (because he has to), but others will just give the finger.

I wouldnt base your calculations off Australia - they have had compulsory super for 30 years, plus have always paid higher wages over a lifetime than NZ. Therefore they have a far higher number of retirees who can afford to be self funded (currently 35%). There would be very few NZ retirees who are in the same situation. So I would guess that Treasury has run the numbers and realised that the costs of asset and income testing far outweigh the miniscule savings that would arise from denying the pension to a tiny number of retirees.

Your last sentence says it all. In my books. Any introduction of New Taxes or means testing of the National Superannuation needs to be undertaken free from Political intervention

A capital gains tax fair enough, if you believe like the Left that the government always needs more revenue instead of downsizing. But looking at the experience of countries that had a wealth tax, and dropped it--also U.S. states like New York and California that have lost very many of their higher income tax paying residents due to wealth taxes--it would be stupid for NZ to introduce a wealth tax. We already have wealth taxes such as the FIF and similar taxes that tax unrealised gains. A comprehensive wealth tax such as the Greens want at a very low threshold (including the family home) would backfire. Even the constant talk of a wealth tax has discouraged money for investment from potential immigrants who would have started businesses in NZ.

"if you believe like the Left that the government always needs more revenue instead of downsizing"

You are tackling this from the wrong angle. A CGT should be there to level the investment playing field.

FIF is not a wealth tax. It is a form of CGT on unrealised capital gains on certain investments.

I can see the wind moving in the stratosphere, at this news!!

The collective nervous, inwards sphincter clutching, of thousands of wannabe, DuVal like, smalltime developers/house flippers - is sucking in the winds from on high!!

Many thought they could get away without declaring them flipping profits.......and now the fat chook comes home to roost. Hopefully!

Good column/pod as always TB. It should also be noted the 60k GST registration threshold is based on turnover, not taxable income.

Eg a small business owner or sole trader may scrape out a taxable income of only 50K after expenses, yet their total sales may be well in excess of 60K so are required to be GST-registered, and pay 15% tax on all sales.

Fairness of this situation is up for debate but the counter-argument would be they are able to claim GST back on all supplies purchased to run said business.

I wonder why the "RNZ report involving a Victoria University study, commissioned by Tax Justice Aotearoa" didn't include countries such as Singapore, UAE, Switzerland, Czechia, Hungary, etc...

Because that would be highly inconvenient to their left wing, socialist narrative. Currently you can move to Italy and pay a maximum of $100k tax on your worldwide income and assets. That would work for anyone earning more than $300k a year.

The giant Dinosaur in the room that Terry and others fail to acknowledge is how tax changes change behaviour and the unintended and unpredicted consequences. For example a sucessful business owner reaches retirment age and collects pension but has the choice to remain working full or part time despite having sufficient income and capital to live comfortably, owner like the social aspect of working but may see the extra taxation as a disincentive so decides to make his wife happy and spend up on holidays and toys. Results - skills and xperience lost and sold business may fail or employ / trade less due to reduced skill base so less taxes Gst, Paye, Acc etc. Then owner spends and next generation has a smaller inheritance so less capital to perhaps start or buy a business, admittedly such consumption generates tax but its a one time tax unlike taxes that result from business activity, the owner may even emigrate to Australia leaving NZ with tax on state super and spend his cash paying Aussie taxes.This has already happened in the UK - with France Sp[ain and Italy a major beneficiaries.

Results - skills and xperience lost and sold business may fail or employ / trade less due to reduced skill base so less taxes Gst, Paye, Acc etc.

On the other side of the coin, an opportunity opens up for someone to work in owning this business, it may also do well and exceed the previous owner, employing more staff and paying more tax, while either way, the retiree injects spending into the local economy and benefits the tax take by increased GST from increased purchases, and adding to the success of other businesses. Not dissuading your assertion here, just showing both sides of the potential :-)

Many retiring business owners struggle to find someone suitable to manage the business once they're gone, so the "missed opportunities" are pretty small in my opinion.

And that opportunity chasm widens as you apply the same thinking to the rest of the workforce. People are so scared that if we make Super less generous, that we'll lose skilled experience and talent because people will quit working to claim a pension.

So what happens when they die? Does a life time of experience negate the effects of cognitive decline in their final years? Young people delay their career progression prospects another 10 - 20 years because those further up the ladder can work and retire simultaneously.

an opportunity opens up for someone to work in owning this business

You mean like an immigrant? So we import more people to replace the people we already have, but have disincentivised from contributing?

re ... "The giant Dinosaur in the room that Terry and others fail to acknowledge is how tax changes change behaviour and the unintended and unpredicted consequences."

So you're say that because of "unintended and unpredicted consequences" we should never do anything?

Might I respectfully suggest you're the giant dinosaur?

My recommendation to NZ Inc.'s politicians remains: Set the CGT rate low, the net wide and simple, and get it on the books NOW !!!

No! once CGT is in just watch Politicians will find a way to increase it.. Case in point GST Originally 10%. Govt short of money just increase to accommodate increased Govt expenditure

Any study by a group called 'Tax Justice Aotearoa' is bound to be ideologically motivated, Max Rashbrooke certainly is.

Yeah. Fairness is the worst type of ideologically motivation ever, right?

Now add in Singapore as a comparative tax jurisdiction. Or any of the countries offering a Golden Visa.

Also basing comparisons solely off tax rates is highly misleading. In Australia, the wealthy utilise the self managed super fund scheme for holding investments - with an income tax rate of 15%, capital gains tax rate of 10%, and where everything is tax free after you hit 60 and "retire". There are now 616,400 self managed super funds in Australia. The super wealthy have everything tied up in trusts and offshore holding companies in tax free jurisdictions.

A very wealthy friend of mine in Australia effectively pays no tax - his business (hence his income) is owned by his super fund, along with his investment properties, and his share holdings. Because he is in pension phase he doesnt pay tax, and instead receives money from the tax dept as you get the franking credits on dividends back in cash. Its a family super fund so includes his wife and children, who will therefore inherit everything via the SMSF. I was just reading an AFR article on how you can take money out of super, then put it straight back in again, and it then suddenly becomes tax free when inherited by your kids on your death. I mean, this SMSF thing in Australia is just the bomb!

This is one of the reasons why the Labour Govt wanted to cap super funds at $3M - but the legislation couldnt get past the Senate. Australia, still the "The Lucky Country".

There’s never any balanced debate on CGT in this country. The usual powerful forces organise to frame the debate in a way that is favourable to their interests - i.e. give every excuse under the sun as to why it’s a bad idea. Terry is right property can not move offshore. Landlords are able to deduct expenses, many also benefit from accommodation supplements. It can’t always be take and take. It needs to go both ways. We also need to talk about an inheritance tax. My husband’s stepfather just inherited 6.8 million from his father (who made most of that via property of course). It’s a huge windfall, and knowing that this money was always coming to him has really kind of screwed with his head in some ways. He’s never had much of an incentive to work hard, and has floated through life quite listless. We at least need some kind of tax to even the playing field and broaden our tax base.

Most of the lack of balance I see in a CGT is from people who insist it's going to raise huge amounts of revenue while also making house prices cheaper AND let us drop personal tax rates.

The lack of balance is no one suggesting that not all of those things can happen at once, and media outlets amplifying claims from politicians about the tax system that have little to do with how the tax system works. The hysteria I usually see comes from the left and often goes unchallenged.

As for an inheritance tax: Some listless guy inheriting money after living an aimless life isn't really good enough justification to give the state the right to interfere in what I decide to leave my kids in the event I die.

I personally don't care what it does to house prices, I'm only interested in it from a fairness and equity perspective re taxing income. It's like why is this special and excluded? Why is New Zealand the only backwards OECD country with no capital gains tax, no inheritance tax? What's the reason for not having one? Some random guy worked hard for it and was already taxed on his rental income. Well, who cares. You pay GST and you've already been taxed on that income. It's no different in my mind. As for why should we do it? Look at the absolute cesspit of a society we are heading towards - we need to even the playing field somehow.

Love the we conversation around the side effects of never raising the 60k income gst kick in rate for a business.

i know many people who limit their business income to make sure they don’t reach this threshold. Buts it’s never because don’t want to pay the gst. It’s always because they don’t want to register their assets for gst. Usually a residential house, which is completely understandable.

Who is going to register their family home for gst because their side unit air bnb may crack 60k.

i feel if the IRD just allowed people to opt out of registering certain assets for gst, then their income could rise a lot.

I think they should look at raising the threshold but why should Airbnb owners get a free ride? If you're making $60k a year off Airbnb you absolutely should have to register that asset for GST. The government 100% should not be making it easier for those renting their properties out on Airbnb considering the damage it does to communities.

Should someone have to register their entire family home for gst, when they only rent out a small side unit. Seems very unfair.

On the GST threshold, 15 years ago access to free spreadsheet software, free tax calculators, etc. was limited. Not so now. The original premise for a threshold was to keep the administrative burden down. That premise is way past it 'use by' date. Ergo, the threshold should be scrapped to create a level playing field (and stop the cashies).

In the same 'technology is everywhere' vane - time to look more closely at PAYE thresholds and make many more of them which are adjusted far more frequently than they are.

And likewise for company tax to remove the flat rate and make it progressive like PAYE is. I mean, why is it fair that a billion dollar company pays the same flat tax rate that a far, far smaller company struggling to grow and develop economies of scale does?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.