By Andrew Coleman*

Fifty years ago, successive New Zealand governments introduced and then scrapped a compulsory saving scheme. It was eventually replaced by the most unusual government retirement scheme in the world, New Zealand Superannuation. While New Zealand Superannuation has several attractive features, it also has several serious drawbacks. So, is it possible to design a better scheme? Without doubt, yes.

In this article I will describe a form of compulsory saving scheme - let’s call it KiwiSaver 2.1 - that younger Kiwis could adopt for themselves as a replacement for New Zealand Superannuation. It is designed to deliver most of the benefits of New Zealand Superannuation, plus more, without many of its disadvantages. The scheme is designed along the four basic dimensions highlighted in this series:

⦁ the extent it is based on a mixture of welfare and contributory principles;

⦁ the extent it is based on save-as-you-go or pay-as-you-go principles;

⦁ the extent it is funded from general taxes rather than from social security taxes or compulsory saving contributions; and

⦁ the extent that the earnings from private retirement savings are taxed on withdrawal (EET principles) rather than as they accumulate (TTE principles).

New Zealand Superannuation is so unusual because it takes extreme positions on most of these dimensions. It does not have any contributory component, and it is entirely funded from general tax revenues. No other countries do this. Moreover, it is largely funded on pay-as-you-go principles (the exception being the New Zealand Superannuation Fund) and the earnings of public and private retirement savings are all taxed on TTE principles. These extreme positions are the cause of many of the drawbacks of the current scheme. The good news is that most of the attractive features of New Zealand Superannuation can be achieved at lower cost with fewer distortions when these extreme positions are modified.

KiwiSaver 2.1 as it is described here is a type of compulsory saving scheme that replaces a part of New Zealand Superannuation while ensuring all New Zealanders will still get at least as much retirement income as they do now. It is not means tested, but as it combines contributory and welfare principles, those who contribute more have higher retirement incomes like normal saving schemes.

However, from a wider perspective, KiwiSaver 2.1 is primarily a set of tools or options that can be combined in different ways to achieve different payment and benefit combinations. The way they are combined depends on the preferences of the community. The combination discussed today is designed to improve upon New Zealand Superannuation while replicating some of its basic features, but it could be easily modified to achieve other outcomes if that is what younger people want.

The two most unattractive features of New Zealand’s scheme are (i) the disproportionately large costs it imposes on current and future generations, and (ii) the distortionary nature of the taxes that are used to pay these costs. The taxes we use are unnecessarily high, cause capital investment to be misallocated, and help generate artificially high house prices, creating inequality.

But there are other problems too. Because the current scheme only has welfare rather than welfare and contributory components, it provides little help to people who want to save additional amounts for their own retirements. Moreover, the scheme may be contributing to long run wealth inequality because the taxes people pay to fund New Zealand Superannuation during a lifetime of working cannot be bequeathed. All of these problems are tackled by KiwiSaver 2.1.

A scheme for people born after 1980

The proposal below is intended for people under 45. The scheme can be easily modified for people who are born in different years, so we shall start with people born after 2000 and note that contribution and benefit levels for people born between 1980 and 2000 can easily be adjusted. It is closely related to a scheme proposed by the Financial Services Council in 2013, except it would be compulsory1.

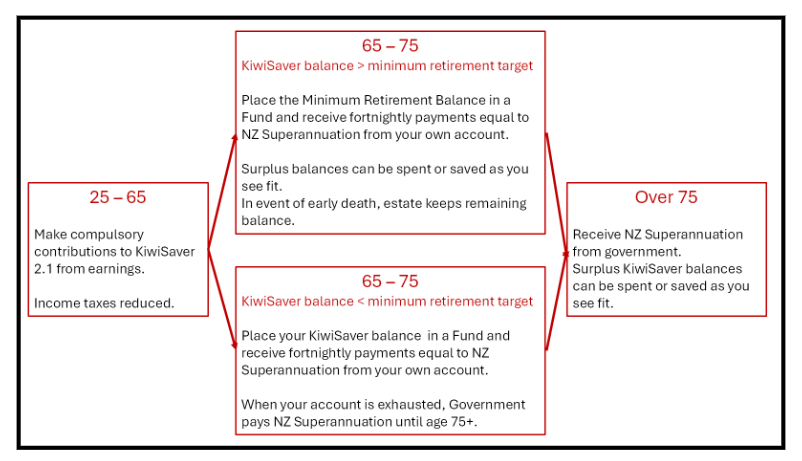

The scheme is a mixed contributory and welfare system. The contributory scheme is a compulsory saving scheme that funds the first years of a person’s retirement, and the welfare scheme funds the later years. To achieve this, there are two pension ages, the first for the compulsory saving scheme and the second for the welfare scheme. Say, for example, these are ages 65 and 75. The compulsory saving scheme would provide retirement incomes from age 65 to age 75, and the welfare scheme would provide retirement incomes from age 75 onwards. Both ages can be changed as individual cohorts wish.

When they are working, people and their employers would make contributions to private compulsory savings schemes, as they do in Australia, that can only be accessed in particular circumstances, primarily after age 65. The money in these accounts would remain the property of the individual or their estate if they die young.

Once people turn 65, they would make a deposit called the minimum retirement target with a public or private agency. This deposit would be enough to pay them a weekly amount at least as much as the government pension that is paid to people over 75. For example, if the pension were $25,000 per year, and interest rates were 3%, they would give the agency $220,000. (While $220,000 sounds like a large sum, if returns were 3% higher than inflation and people contributed for 40 years, this sum would be raised with annual contributions of $2000.) Any surplus money in their account could be used however they liked.

People without sufficient funds would be given a top-up that is enough to pay them the equivalent to the standard pension for people over 75. When people hit 75, they would get the standard government pension. If someone died between the ages of 65 and 75 the balance would be returned to their estate. This combination ensures the current welfare aspects of New Zealand Superannuation are maintained – everyone gets a minimum amount in old age – while enabling those who contribute more to their own savings accounts to keep the surplus.

The basic design has three main differences with the current structure of New Zealand Superannuation. First, it is a mixed save-as-you-go/pay-as-you-go system, so it will reduce the cost on future generations once the transition has occurred. The compulsory saving contributions are the save-as-you-go component, and the taxed-funded government pensions for people over 75 are the pay-as-you-go component. Future generations will be better off because they will be paying fewer taxes because the pay-as-you-go component of New Zealand Superannuation will be much smaller, and they will be able to enjoy the higher investment returns that are available from their contributions to the KiwiSaver 2.1 scheme.

Secondly, the compulsory saving contributions would be separate from income taxes and would allow income taxes to be reduced over time. This would enable New Zealand to adopt a less distortionary and more efficient tax system, as distortionary income taxes would be replaced by “incentive-compatible” contributions to personal savings accounts. General taxes would be smaller than the taxes needed under the current scheme because the population aged over 75 is less than half the size of the population aged over 65.

Thirdly, people who earn more during their working lives will have higher savings in their retirement accounts than those who learn less. Ideally, people who wished to purchase an annuity to obtain a higher regular retirement income would be able to buy them from the government at age 75. This option would allow those people who wanted a high regular retirement income to obtain one, while allowing those people who wanted to set aside some of their funds for expensive purchases or bequests or medical emergencies to manage the additional funds themselves.

Fourthly, the funds in the account would be taxed on an EET (Exempt – Exempt – Taxed) basis. Money placed in the account would be exempt from income tax when placed into the account, returns would be exempt from tax as they accumulated, but all withdrawals from the account would be taxed at standard income tax rates. This system, which is commonly used around the globe, increases returns and significantly reduces tax distortions, particularly with respect to owner-occupied housing.

This type of scheme will result in a different distribution of resources than the current scheme. The overall effects will depend on the way income taxes are changed to offset the introduction of compulsory saving contributions. In the United States, for instance, people pay social security taxes on their first dollar of income, but there is a large tax-free threshold before income tax is paid, so the total tax payments made by low-income people are low.

The scheme would have lower inequality if people who are married or in a long-term relationship make half of their contributions to each other’s accounts. This would automatically even out some of the income disparities between a couple, particularly if one person spends time out of the paid workforce to raise children. Because the amount remaining in the retirement account would be bequeathed in the event of an early death, the scheme may also reduce long run wealth inequality, by providing additional resources to the remaining partner if one person dies young.

The proposed compulsory scheme has some similarities to the Australian Guarantee scheme. However, rather the cut the amount of the government pension that higher income people receive, KiwiSaver 2.1 would replace the first 10 years that people receive a government pension. Rather than have a means-test for high income people, as occurs in Australia, there would be a “top-up” for people with insufficient savings to ensure that everyone gets the same minimum amount, but people who save more in their compulsory saving account keep the extra money.

The transition

As Peter Diamond made clear, any transition from a pay-as-you-go scheme to a save-as-you-go scheme requires some people to be worse off so that future generations can be better off. The transition has often been described as the “double pay” problem as it is typically assumed young people will be asked to pay taxes for the current and future beneficiaries of the existing scheme and make contributions to their own scheme. But young people do not have to be the biggest losers during the transition. As we have seen, one of the reasons to adopt a new scheme is to create a different distribution of the costs and benefits of a retirement scheme, as the current scheme requires young people and future generations to bear a disproportionately large fraction of the costs.

In fact, it is possible to design a transition path that shares the transition costs in any way a society wishes. The costs do not need to entirely fall on the transition generation of young people, by forcing them to contribute to their own pensions while still paying taxes to provide pensions to older people. Rather, older people could be asked to pay higher taxes or accept some reduction in their total pension bill to allow younger people to have a cut in their income tax rates to help fund their compulsory saving contributions.

Finding the right balance is the key political question.

Given that current generations of older people only had to support a relatively small number of elderly people when they were working age, many people will think it is reasonable for them to pay a bit more during the transition to reduce the tax burden on young people (Sinn 2000). As the survey evidence presented last week indicates, a majority of New Zealanders of all ages indicate they would be prepared to have a 2 percentage point increase in taxes now if it would allow the increase in future taxes to be reduced by 2 percentage points.

There are various ways taxes could be increased to fund the transition. One option would be to have a transitional social security tax on people aged over 45, introduced at the same time as a compulsory saving scheme for people aged less than 45, but designed to pay for a part of current and future government pensions while allowing a decrease in income taxes on younger people. This is somewhat similar to what happens in Switzerland. Alternatively, GST could be increased.

A more radical option would be to adopt a land tax to pay for pensions. Moreover, the funds in the New Zealand Superannuation Fund could be slowly reduced as the funds in KiwiSaver 2.1 accounts build up. Whatever the solution, the major point is that these solutions could be adopted to shift some part of the cost of the transition away from young people. The ultimate choice will depend on the political comprises people are willing to make to ensure that the taxes and opportunity costs on the next generations are not substantially higher than those we currently face.

Three other aspects of the transition deserve to be mentioned. First, if a scheme like this were introduced, the number of years that a person provides their retirement income from their compulsory saving scheme would depend on their birth year. This is straightforward to do: people born in 1980, for instance, might be expected to only contribute 5 years, whereas people born in 2000 might be expected to contribute ten years. In the future new cohorts might decide quite different combinations as they see fit.

Secondly, this scheme would be in addition to “voluntary” KiwiSaver, not a replacement for it. KiwiSaver 2.1 is designed to replace part of New Zealand Superannuation, whereas “voluntary” KiwiSaver is designed to provide a person with supplementary income in addition to New Zealand Superannuation. Depending on the mandatory contribution levels many people will decide, at least while they are very young, that they have no additional need for “voluntary” KiwiSaver. Others will want to use “voluntary” KiwiSaver to accumulate more funds for their retirement.

Lastly, contributions could be made by individuals or employers: ultimately, it makes little difference. Australia introduced its compulsory saving scheme in a particularly skilful way, by asking employers to gradually increase their contributions over a series of years as part of regular wage increases. If New Zealand were to introduce such a scheme, it could be done in this way, or in conjunction with reductions in income taxes.

As I hope to have made clear throughout the series, I believe that people under 45 years old should be able to design a new scheme for themselves, one suitable for the 21st century. No-one under 45 voted in the 1997 referendum and since it is clear that young people are bearing a disproportionately large share of the costs of the current scheme it seems reasonable that they should be able to design a scheme for their own generations.

KiwiSaver 2.1 demonstrates better designs exist. Other schemes are possible and could reduce many of the problems caused by New Zealand’s current scheme. The primary role of older people like me is not to dictate what younger people should want, but to find ways to help New Zealand fund the transition to a better, more affordable, and less wasteful future.

References

1) Financial Service Council (2013). Pensions for the Twenty First Century: Retirement Income Security for Younger New Zealanders. Wellington: Financial Service Council.

*This series and an accompanying paper are based on work I started in 2020 with Jeanne-Marie Bonnet while we were both at the University of Otago. I am very grateful for her assistance and insights. All errors remain my own.

(This article is part 12 in the series. You can find all other articles in the series to date here).

**Andrew Coleman is a visiting professor at the Asia School of Business. This article is his personal view of retirement policy in New Zealand, based on academic study.

Coleman is on extended leave from the Reserve Bank of New Zealand, while working overseas. The views expressed in this article do not represent the RBNZ and are unrelated to work conducted at the Bank, which has no responsibility for retirement policy in New Zealand.

71 Comments

By limiting his proposed compulsory-savings scheme to providing self-funded superannuation only for the first 10 years of 'retirement', from 65 till 75, Andrew Coleman cleverly mitigates a problem of Australian superannuation: the longevity-mortality risk.

At 65 a person may expect to live another 20 or 25 years. But they may live for 40 years, or drop dead at 66, Either way, through their working life an Australian will have saved, rather than have spent and enjoyed, a huge amount of money that if they live to 105 may turn out not to be enough, or if they become mortally ill soon after their 65th birthday will be a useless pot of gold that will taunt them with visions of the life they might have lived.

Even more cleverly, the proposition covers the decade from 65 till 75 during which those who are able will continue to work, so have no need of state support anyway. This is a big step to overcome the problem of those who have no need of super claiming it: the fully funded state pension awaits them at 75. Hence the need to make the saving compulsory.

Coleman's proposition requires a much more modest saving to cover a fixed 10 years, with a government-guaranteed top-up for those who cannot save, and a state-funded pension for all who survive past 75.

I rather like it.

A problem that is not addressed is that NZ Super now is not enough for those who really need it: those without savings or other income, especially renters.

A Retirement Commission survey in 2023 found that one-third of people aged between 55 and 65 live in rental housing, that 20% of people over 65 are renters, and that by 2048 40% of people over 65 will be renters.

The median rent for a three-bedroom home in New Zealand is about $600 a week. In Auckland, the median rent for a one-bedroom home is $500 a week, a two-bedroom home $670 a week.

NZ Super now for a couple is $800 a week after tax, for a single person living alone $519 a week. Do the maths: how can a renter survive on NZ Super?

The married couple after-tax rate needs to be raised to the higher of 100% of the after-tax full-time median income or 80% of the full-time average income, to about $1080 a week; the single-living-alone needs to rise proportionately by about $200 a week.

That would increase the annual pension bill to the state by close to 40%, yet it would still leave the retired couple getting only half the median wage each: $545 a week; a pittance compared with the minimum wage $768 after tax.

How to fund such a huge bill? Bring back the surcharge Winston Peters succeeded in having abolished in 1998, so that an enhanced Super goes to those who need it, not to those who don't.

https://www.auckland.ac.nz/assets/business/about/our-research/research-…

We could also address the rent subsidies such as the accommodation supplement. What good is it giving more money to the renters, as when the announcements are made you can bet your bottom dollar that the rent will be increasing proportionately and it will get hoovered straight into the landlords pockets. Case in point when the student allowance went up by $50 a week and many landlords upped their rent this exact amount per person.

It is difficult to control the unruly private rental market, much of it run by 'mum-and-dad' making the most out of their less fortunate fellow-retired. How about a mass build of state-owned housing for secure, lifetime, income-moderated rent? Build enough and it will collapse how much landlords can charge.

Easy, don't pay rent get forced into government housing and pay about $100 a week, hell rates are more $100 per week, don't forget, insurance and maintenance. You also get an accommodation supplement, if you don't live in a state house. You also get some to do insulation for free which you don't get in your own house.

For 40% of over-65s in 2048?

A very interesting proposal indeed. I can't see a way where there isn't bias from changing the current status quo, although it is sorely needed, there will be lower income workers, those with disabilities, divorces etc which may come into discussion as they may not have been able to pay in so much, however if the government guaranteed pension for those that need it is sufficient to survive on then it seems plausible and reasonable.

In general agreement with this approach, it balances many of the challenges with super very well. No doubt we have to start moving towards to more self-funding but retain the "welfare" aspect of super for those who have note been able to save sufficiently for retirement (for whatever reason) even with compulsion. This approach works well in that regard and allows retirement for 65 year olds who couldn't cope with continued fulltime work. This just needs to be phased in over time - potentially by steadily increasing the 75 threshold e.g 68 for those currently 50-55, 70 for those 45-49 etc. etc.

I don't see the need for changing the age thresholds of 65 and 75. It could be introduced tomorrow. It would simply mean that those retiring next year would have 98% of their pension between 65 and 75 paid by the state (still less than now), and that percentage would decline year by year as each cohort reached 65 with more savings to contribute to their own pension.

.

Still ignoring the fact that for many, present income is too low to actually live off.

Kiwisaver was flawed in that it allowed employer contribution to be deducted from gross pay (Except for minimum wage).

The aussie model was successful because it made sure the contribution was on top of salary.

Making it compulsory, without fixing this penalty, just further erodes the ability of those on lower (and lets not forget about zero) income to do anything.

It makes no difference, if the amount is on top of gross salary then just expect a few years of below inflation wage increases while it returns the total cost to the employer to what the market dictates due to supply/demand dynamics.

If it makes no difference, then for most they are better off with cash in hand now.

I was referring to this:

Kiwisaver was flawed in that it allowed employer contribution to be deducted from gross pay (Except for minimum wage).

Ultimately the market decides that truck driver, class 5 is worth a certain rate, and whether that has to be advertised as $X plus kiwisaver or $Y inclusive of kiwisaver makes no difference.

I would usually agree, except that Australia showed that to be false. Wages increased and have maintained similar (if not higher) year on year increases as NZ.

It would have been a one off effect back when kiwisaver was introduced. It wouldn't be affecting anything now.

Yes, wages are higher in Australia. But that's not because of the compulsory employer contributions.

That is my point, they have higher wages + higher contribution. It is win win.

I am afraid it is beyond a retirement income scheme or a tax scheme to fully alleviate the problems of low incomes. That is quite a different issue. But this scheme (i) ensures low income people still get the normal pension from the initial age (which in my example was left at 65). Some of the money comes from their own accounts; if this runs out it is topped up. (ii) The article suggests that the contributions will be partially funded by income tax reductions, and it specifically suggests that employer contributions could be used as was the case in Australia (iii) Earlier articles suggest the reform of the tax system could improve housing affordability by reducing the extent that the current tax system artificially inflates house prices. This indirect effect can be large - so even if a particular household does not gain directly from the system, it may still gain indirectly.

Obviously the details matter. But this sort of scheme suggests that details can be chosen in a manner that help lower income people as well as middle and higher income people. It is possible to choose these that improve on the current situation even if it is not possible for a retirement income scheme to eliminate poverty.

ac

Considering a significant number of the population are below poverty levels and don't even have minimum wage income levels (legally allowed to breach minimum wage levels in the Bill of Rights & deny income support to those unable to get/find work), then it should be brutally obvious Kiwisaver was designed to never work for those who have an actual need of retirement support and that kiwisaver will never support the poor. It is a scheme that is designed to increase inequality and benefit those with the largest incomes especially getting the taxpayers to pay for lolly scrambles for the most wealthy among us.

The worst assumption by the author is that they think all people can have an income to live on when NZ clearly and openly does not support most disabled people unable to work and does not adequately support those disabled by birth, chronic illness or disease that are lucky enough to get minimal support that does not even cover GP visits, medication costs, transport (so no chance of work or most tertiary training access, most necessary services etc), food, housing & essential living needs like wound care materials or basic mobility & equipment to communicate with essential govt services. Considering the large portion of people in NZ denied even a basic income that can cover the essentials for living it makes even the idea that everyone can support or participate in kiwisaver ignorant, offensive, & discriminatory.

Most people without any contributions to kiwisaver also have no income able to support their cost of living. This article is complete tripe. It started by punching down saying poor people must not be competent enough to save and that those without a retirement nest egg must be failures in investing. Neglecting the fact SHIT HAPPENS. You get cancer, nest egg gone. You have a disabled child you could not predict, gone. You have a bad divorce, gone. You are exposed to a 1/1000 natural accidental event, gone. You are made redundant early and cannot find new work, gone. You get a degenerative disease that hits early like MS that impairs your ability to work, gone. You are disabled and need to have someone to love you in your life to make it worth living resulting in no income at all (common issue for most disabled people under 65), gone. etc. etc.

Ignoring the reality of disparate access to any income to cover living costs & life events that need emergency savings is a huge gap that means what the article proposes is actually a harmful waste of hundreds of millions of dollars from taxpayers (supporting, maintaining, paying IT contracts, funding and rejigging the kiwisaver schemes), with the express aim to actually prop up the profits & bonuses of investment companies (see the attitudes around the banks for kiwisaver) rather then actually improving the wellbeing of NZ communities. Imagine if the poor could actually access a GP, accessible housing, cooked food, daily transport to necessary services, training & work, essential tools for mobility & communication and even the necessary medication to stay healthier. How much better the community as a whole would be and more able to prepare for retirement.

All this article is for is to protect the over entitled attitudes of those over 40 to the pension benefit irrespective of any actual need to welfare support and increase the customer numbers forced into investment companies and banks managed funds. As currently more and more of the population are unable to participate in kiwisaver, and those just going through a financial rough patch (that can extend for years) take contributions holidays & withdrawals (although those rough patches can turn out to be permanent e.g. severe & chronic illness resulting in disability, or having to quit work to take on support worker roles etc). It is not for the benefit of the actual poor needing pension benefits it is purely to retain & increase the future profit of investment companies, to secure their future customer & contributions numbers. We as a country do not need it, those needing retirement welfare don't need it, and lets be honest if we took the money for managing/rejigging and paying out to those who don't need retirement welfare benefits and actually supported those in need or without a living income now to have at least the minimum of essential living needs & access to their community we would be in a much better position as a country long term. Rather then crippling the nation to serve the interests of those who already are above the median incomes while over 65 lets provide a living cost income to those who are in need under 65. I hear it is hard for some govt officials to live on incomes above 180k with full transport benefits but they should really try to see what it is like to live when your income can be anywhere from 0-20k and there is no accessible transport available to you.

Wait, so you're saying there are poor people out there who aren't just some combination of dumb and lazy?

/sarc

Are you saying that KiwiSaver which was designed by the Labour Party was designed to increase inequality? Is increasing inequality the labour party’s secret agenda!

I think Michael Cullen was cast firmly in the neoliberal mould, and yes, KiwiSaver as designed by the Labour Party increases inequality by favouring those who between the ages of 20 and 65 have a steady income with enough surplus cash to stash away for their 'golden years'. Any saving scheme will do that. The problems with KiwiSaver are (1) savers get a $521 state subsidy each year, and the state has no business subsidising private savings, and (2) people who can save large pots of money, in KiwiSaver or anywhere else, have less motivation to support a universal social welfare pension like NZ Super. Andrew Coleman's proposal seems to address the second point with a mix of savings plus universal pension.

Wonder what Kiwisaver will look like if the global stockmarkets crash hard? Its not hard too see why some companies are over valued when theres exorbitant amounts of capital being pumped into the system weekly likely for the purpose of clipping the ticket and parking it.... its all happy days until ?

I agree kiwisaver should be compulsory, plus employer contributions increased by 1% every two years over a 14 year period so it reaches 10%

Currently Australia employer contributions is 11.5% so even at the minimum wage you are sorted for retirement. I can see why young go over there and why it might be hard to bring them back.

Also Australian super has other aspects like you can pay for life cover out of the fund so it doesn't hit your cashflow

As I say above, the problem with Australia's compulsory super with that huge 11.5% contribution is the longevity and mortality risk: people end up with a giant pot of gold that might outlive them, and if so would have been much more enjoyable to have spent throughout their lives. Andrew Coleman's proposal limits this risk by a finite self-funded period of 10 years, requiring less heroic compulsory saving.

I have Aus super, a pretty hefty total, if I die at 65, my kids/wife will be well looked after. I'm good with that

In NZ, you pay a lot of tax towards superannuation, if you die at 65.... you get nothing back.

Because NZ Superannuation is for the living, not the dead. It is a social welfare benefit.

Really we should be trying education. To solve this problem. Even if you start off on the minimum wage when you are 18-20. You can put aside enough to retire. At that stage in life you should easily be able to out a couple of hundred bucks a week away. After three years you have 30k. If you don’t save again and invest it in an index fund you will end up with around a million bucks to retire with……and that is if you stop saving when you are 22-23. If you want to carry on putting a bit aside, you are laughing. Education beats all these compulsory saving schemes hands down.

Question....who would administer Kiwisaver 2.1? and what fees structure?

No conflict to declare?

KiwiSaver 2.1 could be administered in a very similar way to the current Kiwisaver: ie deductions organised through the IRD and then transferred to registered financial institutions. This would not be very different from the Australian system. I would imagine the payment of the the first ten year's payments could also be done by appropriate private financial institutions - after all the calculations are sufficiently simple that even a banker could do them.

It is of course possible that young people might wan the option of investing via a government agency that manages their contributions. That would be a decision for them to make. The returns to sovereign wealth funds are often very good, but this is in part because they can make very long term investments as they do not face withdrawal risk. To replicate this aspect you would have to restrict people from prematurely switching funds from a government agency to a different pension fund.

I would advocate for the Government to make some annuities available for people to purchase if they want. There is almost no private annuity market in NZ. The British Government sold annuities in the 18th century, it should be possible for a modern NZ government to do so - or allow people to take the second pension (in my scheme the over 75 pension) at a later date in exchange for a higher payment if they wanted.

Peter Diamond emphasises the need for very low transactions costs in these type of arrangements, and warns high transactions costs can significantly undermine returns. This can be managed. US fund managers often charge much less than domestic NZ ones, and some of these fund managers are very large non-profits that emphasis low transactions costs. I imagine these details can be managed.

Oh, wouldn't conflicts of interest be nice to report. But no, I don't think I have conflicts of interests.

My current employment bars me from directly owning shares in New Zealand domiciled financial institutions. I have some indirect ownership claims on foreign financial institutions including Australian banks through personal pension funds (such as a KiwiSaver account) that invest in diversified indices of shares. I have not worked for a private financial institution this century, although last century I did work for a New Zealand bank and for a Scottish Pension Fund.

No financial institutions paid for any of the research I have done in the last decade, although in 2013 I was paid consultancy fees for work I did for the Financial Services Council concerning a voluntary KiwiSaver scheme. In 2022 I received a small amount of funding from the Retirement Commission to undertake the second survey described in article 11: they paid for the surveying, and contributed less than $15000 to the three researchers for the time involved conducting the survey and writing a report.

I pay tax on all income, but I don't think that this counts as a conflict of interest even though it might affect my perceptions about the appropriateness of different types of tax systems.

Thank you for the reply....it is good to note that this series hasnt been sponsored by the financial services industry, though with an average ticket clip of 1% of Kiwisaver they would certainly gain from such a proposal.

I note that the Australian compulsory super has expanded from an initial 3% (1980s) to a recent 12% of income (employed only, sole traders/self employed exempt) this suggests something of a tail chasing exercise....and it is now proposed to allow access for home purchase, hardly consistent with restrained RE values.

Again any wealth fund exercise only provides the ability to bid for whatever services/goods that may be available in an uncertain future, it does not necessarily ensure either provision nor access but it does provide the basis for a bidding war in an increasingly inequitable auction room....assuming growth continues, by no means guaranteed.

Fortunately we (currently) live in a democracy (of sorts) so as you suggest all manner of solutions can be put to the voting public and that is where it will be decided I expect, and can see that it is probably more palatable to the public than a tax increase which could more directly address the problem.

Didn't National get rid of Compulsory Super campaigned on it being communism? (Which the Boomers took lock -stock and barrel)

https://www.stuff.co.nz/business/money/300327451/the-worst-decision-by-…

Looking at the terms, it seemed to be a good system, much better than kiwisaver. There is also the possibility that if Muldoon had not cancelled it, some other govt could have in another term. I see it was all tax free too, actual incentives; and from.a Labour govt too. It just goes to show how far they have fallen in terms of sensible policy.

You should be a anchor on Fox news..

Well, I think it is fair to say that they have. After all, they tried to tax KiwiSaver last term, so they have fallen far from where they were. There is also no doubt that if we had all this money in this pot, then some govt (probably Labour) would have come along and done something dumb (like put a wealth tax) on it and started hauling 5-10B out of it each year to pay for bribes to get elected. So the fund was probably doomed to begin with unless there was some agreement requiring 75% support in parliament to mess with it.

I think Labour's plan was simply to levy GST on the management fees of PIE funds (including KiwiSaver), which would have been consistent with other areas of commerce. It would not necessarily have cost KiwiSavers anything, because fund managers might have lowered their fees to remain competitive.

https://archive.is/ZtWzV

This is an ignorant article, in the original sense.

The basic flaw is that money is NOT a store of value.

It is a forward bet, and only by studiously avoiding the resource/energy draw-down happening on a finite planet, can Coleman make his posits.

What will the young buy, after Coleman's cohort have extracted, used, burnt and discarded it all? What will this ostensible proxy be cash-in-able for?

But they are being told not to compete/spend NOW?

I suggest they will, in hindsight, see being told to 'save', as fraud. By us, on them.

Yah yah yah. The article is about whether such a program would be good for kids. It’s not a debate about whether money has a value now or in the future because clearly it does and will in the future. So, you adding nothing to the conversation apart from being side show pushing topics that irrelevant.

No, its a distraction money doesn't mean anything if we don't have actual resources, doctors, builders, land. If everybody tomorrow had a billion dollars in the bank it wouldn't make a blind bit of difference if we lived in a wasteland that couldn't produce food, the would all just die. Saving makes sense on an individual level person A can out save person B, so its in persons A's interest to out save B. On a world level it doesn't make a blind bit of difference. What we need for our children to be happy is to increase productivity buy teaching them better, and using the resources we have more efficiently. But hell we can all invest in housing, crypto, high frequency trading, and in general screwing each other over better and everything will be good.

"I suggest they will, in hindsight, see being told to 'save', as fraud. By us, on them."

There is every chance that will be the case, but consideration of the future is not economists' strong point....come to think of it, it is a common human failing.

this exactly what I was thinking.

from a personal perspective, retirement finance is about to having enough cash to pay for the retired lifestyle. but from a collective view, retirement is about to make sure the working population can support the retired non-working population. some study is already saying 50 years later, there will be 1.X working person supporting 1 retiree. that cannot be sustainable.

Think about it, during Covid, we suddenly had a tsunami of patients, while numbers of available doctors and nurses reduced dramatically, did it really matter whether DHBs fully funded or not? or patients couldn't get doctors simply because not enough resources? It'll be the same with people's retirement. it doesn't matter how much NZ save today if NZ simply cannot retain enough working population.

Future output will be made by future people working in future companies with future machines. This Scheme, like any save-as-you-go- scheme increases the amount of capital in the economy, and the claims on foreign income. By having more capital, the amount of resources in the future will be increased because workers will be more productive. By having more capital abroad, we can import extra goods services made overseas by younger workers living there - workers who are made more productive because they have more capital to work with.

Japan is an example of a country with an older population that uses a lot of machinery/capital to assist older people with their lives and reduce their need for so much labour-based assistance. Obviously you still need people, but you can change the number of hours of assistance each person requires if you have a lot of capital equipment and savings.

I agree that without enough people here NZ will be bleak. There is actually not much empirical literature on the extent that people migrate in response to differences in taxes and differences in compulsory saving schemes, so it is difficult to answer the question of whether KiwiSaver 2.1 would make it more attractive for young people to stay in NZ. I have yet to meet many New Zealanders living in Australia who think the contributions they make to the Australian Guarantee system (their compulsory saving scheme) are a bad thing and a reason to avoid Australia, however.

in Japan's case, their savings are not within Japan but invested outside of it, hence there is a saying, There is 'another Japan outside Japan'.

I absolutely agree with you that, we will, almost certain, have a more efficient economy and the per capita output will be bigger than now, and some savings are in tangible form, hence will be used by us for a long long time.

I am just saying one thing, people who saves now is not guaranteed a retirement, as it's linked with future economy. People still should save as it will make sure one get's as big proportion of that economy as possible.

Dr Coleman - absolute bu--sh-t.

It's not future companies with future machines - it a matter of future resource-stocks, future sink-capacities, and future energy-availability. Back one, it's not technology; it's energy.

'By having more capital, the amount of resources in the future will be increased because workers will be more productive.'

There we have it in one - the untruth that underlies economics. We burn our way through a million barrels of oil (all sources) a day - and an equivalent of coal & gas. Each day, that is a physical resource the future cannot have - because your/my cohort burned it today. They'll have to be gosh-darned more productive to displace Energy use per person, 2023 (ourworldindata.org) when they can manage 100 Watts each, max.

And ''more productive is really 'more energy-efficient'. Which runs into thermodynamic limits, Carnot etc. This I increased my learning about, at your Uni. It should not ever be, that a high-level academic (you're a Professor, no?) makes such obviously incorrect statements. The difference between you and me, is that I know why 'productivity' has flattened.

Presuming the money isn't spent on Bitcoin, NVDA, Tesla shares, Fletcher Building acquisitions resulting in "non-cash" impairments or overpaid and useless fund managers or CEOs. Assuming what we need is more consumption and production on a finite planet that's already seeing major ecological problems.

Assuming that we are going to build more machines with the capital when high prices resulting from the fire-sales of our infrastructure assets are causing de-industrialisation (see Ruapehu mills) and we have less heavy industry than 20 years ago.

Assuming the RBNZ doesn't cause a destruction of wealth through FOMO in the housing market by juicing asset prices through lowering interest rates to "solve" a pandemic.

Assuming the cost of energy and other "resources" doesn't go up with depletion.

You couldn't organise a piss-up in a brewery Andrew.

Most money is bank money, which is a claim on loans used to build businesses, houses, operate firms etc. In addition to these debt claims, there are equity claims on real resources. An increase in savings will lead to more real resources, and hence a more productive future world - the increase in debt and equity claims is merely a way of accounting for the ownership of these resources. Some of these resources might even be substitutes for the natural resources we currently use: for instance, when solar or hydro energy is used instead of coal.

As far as I am aware, the economics and geological literatures came to the conclusion a long time ago that while planetary resources are finite (although sunlight is really unconstrained), they are present on the planet in such large amounts that this constraint is unlikely to be binding for a very very long time. Iron atoms for instance, are so common it simply inconceivable that humans will use all iron ore on the planet. The real question is their "availability" and this is essentially an economic concept about the cost of extraction. As costs of extraction change, the amount of any resource that is economically available and viable changes - and when they increase, people look for substitutes and new ways of extraction/ reuse. It certainly is possible that humans could run out of affordable resources of particular types in the future, as they have in the past. So far these have not provided obstacles that cannot be circumvented - people have found different extraction methods, or cheaper and better substitutes. This is not to say that human's effect on the planet has been benign - far from it, as anyway who has read J.R McNeill's magnificent (and now old) environmental history " Something new under the sun: an environmental history of the twentieth century world" will attest. But the problems he outlines are really the effects of pollution because it is far too easy to extract resources, not that of underuse and scarcity because it is far too difficult. We have been wasteful, rather than we have run into binding resource constraints. These are quite different problems.

In any case this series of articles is about better ways to design retirement schemes for the near future, say 100 years (after which future young people or AI machines are likely to have even better ideas.) It is not designed to worry about the efficiency of different ways to extract and use or reuse or reduce use various types of resources. I shall leave that to the experts, who seem to have been making pretty good progress without me.

AC

Not good enough.

You are choosing not to be informed - which I find amazing given your position.

Data check on the world model that forecast global collapse - Club of Rome

The planet is anything but infinite; we are in ecological overshoot as it is - as others associated with your university could tell you

'Some of these resources might even be substitutes for the natural resources we currently use: for instance, when solar or hydro energy is used instead of coal.'

No. wrong. Coal, oil and gas are fossilised solar energy. We are burning our way through millions of years' worth in a 300-year frenzy. Yes, we will end up on real-time solar energy (wind and hydro being solar derivatives, as is firewood) but not at the rate we currently burn.

'So far these have not provided obstacles that cannot be circumvented - people have found different extraction methods, or cheaper and better substitutes. This is not to say that human's effect on the planet has been benign' Those two are not apples-with-apples points.

Not good enough, Professor. Not by half. Even at a BAU2 rate (per Herrington) there is nothing left in 50 - let alone 100 - years, for anyone. I repeat, what you are advocating, is that they accrue proxy while you and I indulge in resource draw-down. I would allow you the point on one - and only one - condition; that you had PROVEN the existence of viable alternatives, on a per-head basis, BEFORE you indulged in draw-down.

I think you need to do some serious homework.

EDIT - Every graph since we discovered fossilised sunlight underground, has been a hockey-stick. Population, consumption, pollution, degradation... So to claim that substitution has thus-far come to the rescue, is - in the light of doubling-times - invalid. Double-or-quits with a finite bank. The longer you push it, the bigger the reconciliation.

Hello Mr Pdk

I listened to your recommended podcast by Corey Bradshaw, and am curious why you would recommend it to anyone. I am sure he is a perfectly fine ecologist and mathematical modeller, but his views on public policy seem very poorly thought through. Moreover, he rambles incessantly. There is much much better material on extinctions and mathematical modelling of complex ecological systems in the 1996 book by Richard Leakey and Roger Lewin 'The sixth Extinction" and much more interesting on the current ecological situation in Elizabeth Colbert's 2014 book "The Sixth Extinction: An unusual history". Most people would learn far more about the science from either of these two than the podcast you recommend.

His views on public policy are somewhat bizarre. He says the worst thing that ever occurred is the invention of the joint stock company? Really?(and he still sees fit to use the products of joint stock companies - his phone, his computer, the electricity that drives his phone, his car, the electricity or petrol that drives his car - even though this means he is supporting the worst thing in history?) Surely not the worst thing, even from a purely ecological perspective. I mean, global warming is happening fairly quickly, but much bigger changes have occurred in the last 20,000 years (eg. A third of the Australia land mass disappeared under water in the last 20,000 years)

His most important policy recommendation is to ban donations to political parties? This can't be serious either. In any case, it is a western perspective, and seems to ignore the experiences of the bulk of the world's population. The largest increase in emissions this century is in China, by far, and I am not convinced that political donations are the main cause of emissions growth or resource use. Amitav Ghosh in his 2016 book "The Great Derangement: Climate change and the unthinkable" is a far more interesting read, and he makes a fairly compelling case that climate change is an Asian problem because that is where the bulk of the world's population live and that is where the bulk of the increase in emissions is occurring. His policy conclusions at least seem to have been well thought through, but not particularly western. I think Ghosh would find it surprising to learn that people in Asia are now unhappier than they have ever been, and the world would be a much better place if the population was heading towards 2-3 billion people rather than 10 billion people and enery use was much smaller. You only need to read "Late Victorian Holocausts" by Mike Davis about the climate related famines in the 1870s and 1890s that killed maybe 50 million people in China and India (and Morocco and Brazil and Egypt - in lots of places, really) to suspect that we are not in the worst of all worlds - that the world be could really nasty when the population was closer to 1 billion and energy use was primarily animate.

There is a lot of debate about the possible future, and an awful lot of uncertainty. To have his level of certainty about future outcomes and current policy options seems unwise. People have been forecasting disaster in terms of living standard outcomes for some time now, and while it may yet occur in the future, such forecasts really haven't had a good history - in fact that they have been terribly wrong so far. Thinking about appropriate policy as if the future is uncertain when it is anything does not seem to be a reasonable approach, even if contemplating disaster is perfectly reasonable.

Anyway, this series is about retirement income. Perhaps you could consider the relative merits of different retirement income schemes if the ecological situation got a lot worse. Would a system that directed a lot of capital to firms that specialise in green energy equipment as a substitute for black energy be helpful? Would one retirement system rather than another be better able to do this? Are there other considerations that would make one retirement system rather than another unambiguously better?. These questions seem reasonable and addressing them is important. I have already declared my belief that using a retirement system that accumulates capital is likely to be useful because it will assist in the production of green energy (powered ultimately by that endless supply of potential renewable energy, the sun), but I am willing to contemplate that other systems may be better. To do this you really need to assess the relative merits of different systems in different scenarios, rather than just say that different scenarios will occur and that they will be bad. To take a simple example, if a sudden shortage of black energy causes a reduction in economic growth (and, indeed, negative growth) and a reduction in the value of many existing economic investments, will the return to capital be greater than or less than the economic growth rate? Will we have been better off saving and investing in new technologies that reduce energy use and nitrogen fertiliser use, or will be have been better simply transferring production between people of different ages without saving? And should we as a country be trying to help poorer countries develop using green rather than black energy.

Lots of interesting questions out there, engaging with diverse perspectives is good, and i am sure civil discourse will lead to better outcomes.

ac

Thank you for bothering.

Methinks you perhaps didn't divest enough (we all harbour a collection of assumptions, which we bring to appraising new arenas); the 'joint stock company' comment makes entire sense to one who understands that unfettered resource-rape leads to overshoot. My own take on where our species went wrong, is in the levering of fire (and that is some time ago).

Your argument fails in assuming fungibility, and in 'colouring' of energy.

As to 'retirement: We 'budget' in proxy, but really we are allocating energy and resources (a Council for instance, will allocate diesel and bitumen for the coming year). Until now, your discipline's false posit (that at a certain price-point an alternative will appear; that all things are fungible) worked, the way I could believe that the mole on my left cheek has staved off cancer; it works until it is proved fallacious. Running an exponentially-growing resource-rape withing a Bounded System (Planet Earth qualifies, the only input being solar energy; the only output being low-grade heat) clearly was a double-or-quits series of bets, with only one possible ultimate result.

Doubling-times being what they are, nobody seems to see the Limit coming; 3 doublings from 1/8th-depleted to all-gone (if, of course, you can maintain growth from 50%-depleted, on...). Nonetheless, retirement proxy-accumulation is a bet that there will be future energy and future resources available, at the mentally-held exchange-rate the proxy-holder assumes. Those energy and resource stocks are limited; NNR's (non-renewables like fossil energy and minerals), renewables (nearly all of which we are depleting faster than they can renew) and sink-capacities (the ability of the biosphere to absorb; most of which we are overloading).

Thus the question - and the difference twixt me and thee - is whether there will be those stocks/capacities. when the proxy comes to be cashed-in. I can tell you now, that the current global collection of forward expectations (all pension/investment/return expectations) is unassuageable at this stage of planetary depletion. The redress action, is for forward-bettors to earmark/allocate/prove PHYSICAL resources, not proxy. In other words, a Council earmarks a supply of bitumen, enough to maintaina road, before it approves it (or are you arguing it paves in proxy?).

Same goes for retirement - the goal should be earmarking the non-perishable stuff required in the future, not amassing unrelated-to-stuff proxy. Perishables, of course, can be planned-for (I have extensive garden-space, for instance).

You might do well to have a think about fungibility - AI is not edible - and energy is colourless. Also, in energy/resource terms, the Georgescu-Roegen graphic is worth contemplating; most of us are parasitic upon those two flows (and they are inexorably left-to-right flows, across the diagram).

Steady State Economics: We’ve got some (systems) thinking to do - The Dig (diagram of natural resource flows). People don't 'earn a living' within the box; they acquire an amount of socially-agreed proxy, with which they go to the left-hand-side of the box, and cash-in (delays in doing this, you call 'the velocity of money'). But if the flows curtail? Or cease? Proxy becomes worth less, en route to becoming worthless.

You are advocating the amassing of proxy, without ascertaining the two input-arrows. I'm a studier of the inputs/outputs. Which do you think has the better handle on the bigger picture? There is a more serious angle; you and I are burning/chewing our way through the stocks (left, within the circle but outside the box) at a rate that cannot possible be maintained for another generation. AI is not a resource stock; for instance; as stated in the ham-sandwich comment (in my circles, the joke is that you can put 100 economists in a room for 100 years and they won't come up with a ham sandwich) - perhaps you need to mentally challenge the concepts of replacement/fungibility? Food, for instance is energy-input (without which all life fails) and cannot be traded for an artwork, say.

Surplus Energy Economics | The home of the SEEDS economic model – Tim Morgan (wordpress.com)

And here is a Professor - an astrophysicist, and no intellectual slug - who has worked it through; given up his position/income, and is addressing the ecological ramifications of his thinking.

Tom Murphy Profile | Do the Math (ucsd.edu)

Yes. I find it very strange that so called experts (as PDK likes to refer to himself and his sources) seem to have a very long history of being almost always completely wrong about absolutely everything. Even a stopped clock is right twice a day….

I’m with you Joe. Pdk is essentially saying we are all going to die (and therefore everything anyone is postulating today is futile). Now there’s a surprise…

Andrew Coleman.

Never engage with PDK. It's pointless. Even if you mostly agree with some point of his, he will still burn you for not agreeing enough.

Remove the "compulsory", then we can talk.

The scheme is created as an alternative to a retirement scheme funded out of a compulsory tax scheme, and seen relative to this alternative it does provide more "freedoms" than a tax system, particularly as people have the right to spend surplus funds in their accounts or have them bequeathed in the event of an early death.

There are some people who believe that the government has no role in providing any assistance for retirement saving, or any tax-funded welfare benefits to older people who have inadequate resources. No OECD countries do this. Without commenting on the merits of this idea, KiwiSaver 2.1 is predicated on the idea that there will be some type of government retirement income system or welfare system for older people with few resources. It is seeking to find a good design for one. If This KiwiSaver 2.1 scheme is not compulsory and there is a welfare system, you will find we have a compulsory tax system as the alternative.

Since I doubt there is the political will to move to a completely voluntary system in NZ or any other higher income country, I have tried to consider practical alternative to the current system.

AC

Good response!

Yeah I'm one of those people who believe the state should have nothing to do with retirement savings or welfare.

But OK, let's assume the state will be involved in these things as you say. I agree there's little point in being able to opt out of stuff if there's that welfare thing at the bottom you can't get away from. Wouldn't it be cool if it was possible to opt out of the compulsory savings scheme and the compulsory welfare as a whole? Everyone is in by default, but if you really want you can opt out, non-reversible or you need to pay all the fees before you're allowed back in. That is something I would like to see.

One final note. I've seen you compare NZ to other OECD countries a lot. How are you so sure the other OECD countries have got things right and NZ is has got it wrong? As an immigrant part of the appeal with NZ is how it differs from other places.

Lots of good things here Andrew. Some suggestions for you

a. Make the super benefit start age 80 years not 75

b. EEE please. This is a social instrument not a standard investment. And it's compulsory. So no tax at all.

c. Double pay. Deal with this by a gradual phase out of current scheme to new scheme. Say thirty years. So your 45 year cutoff becomes not necessary quite soon. Same scheme for all when changeover complete.

d. Low income or no income people. Government makes up via benefit system. For those dependent on somebody else, they get some of their contribution.

c. We have to do this regardless. National Super will collapse at some point.

d. The 80 plus super is best regarded as quite different from National Super. Better to rename it.

Useful suggestions. Thanks for your positive feedback.

ac

Great read, thanks Andrew.

Glad you covered the issue of transitioning, particularly for young taxpayers.

I find the whole argument about tax very unconvincing. Andrew says:

- It "increases returns". Uhh, yes, by forgoing government revenue which has to be raised somewhere else. Australia's revenue foregone from superannuation tax concessions amounts to about $50 billion a year or two percent of GDP ($2800 per working age person 15-64). The main difference to what the NZ does now (putting $521 into everyone's account annually) is to obfuscate the cost, and provide a much higher proportion of the subsidy to the rich who can maximise their retirement savings.

- It causes a distortion with owner-occupied housing being not taxed appropriately. Maybe solve that with land value or imputed rent taxes.

- Other countries do it. Other countries do all sorts of foolish things with their tax systems, doesn't mean NZ should.

Hello problem-9

These criticisms can be addressed, and to some extent have been addressed in the series.

There are two ways that returns to the whole country as well as private households are increased. First, when you switch from a pay-as-you-go scheme to a save-as-you-go scheme in a dynamically efficient economy you replace a transfer scheme with low returns (return = growth rate of the economy) with an investment scheme with a high rate of return (rate of return to investments). This raises potential output. For most of the last century returns to investment have exceeded the growth rate of the economy in developed countries (on average, albeit not every year) and there is not a good reason to believe this will change. Our current scheme prevent young people from getting the advantages of high investment returns by locking them into a transfer scheme. KiwiSaver 2.1 starts to undo this.

Secondly, with respect to the EET/ TTE debate, EET not only delays when the government gets its tax revenues, but it allows investments to compound at the high average return to investment. When the government eventually collects its taxes, it taxes the initial amount compounded at a high rate. If the government collected them early and used them to repay debt, the taxes are effectively compounded at a much lower rate (the government interest rate, not the average return to capital). In other words there is a compositional change in the investments in the economy. The average return to investments is much higher than the government interest rate, which is why there is an improvement in the wealth of society. if the government collected taxes early and invested them in a broad range of assets, this advantage would be curtailed, but in practice it does not. (The NZ Superannuation Fund is very successful, but the inflows are limited.)

For both these reasons, there is potential upside from reform. The government has chosen suboptimal ways of taxing/ investing, and Kiwisaver 2.1 would reduce the suboptimality of their interventions. Think of it as reducing some of the constraints of the current inefficient system - you might not like by suggestions, and there may be better suggestions that I would prefer too, but it should not be assumed that no improvement is possible when we know that the current interventions are constraining.

The whole idea of a tax concession can be strange. It assumes that the current full rate of tax is appropriate, and that to reduce it and offer people fewer services is somehow a concession. It sounds like smaller taxes and fewer services. Tax concessions can be badly designed, but they need not be, and they can be good ways to avoid many of the undesirable effects of badly designed and distortionary taxes.

We know income taxes cause large distortions. if it is possible to reduce these distortions by reducing the tax rates, this sounds like a reduction in distortionary tax rates. One of the reasons that so many countries use EET taxation is that they treat EET as desirable (because it has fewer distortions on saving and investment than TTE) and the TTE treatment of assets outside retirement incomes as an unfortunate necessity because they haven't found a better way to tax this type of capital income. They don't treat distortionary TTE taxes as desirable in their own right, and EET as a "concession" that involves fewer distortions.

There have been at least three recent tax enquiries in NZ that indicate our current way of taxing capital income has problems. One of the problems is the way it adjusts income for inflation. An EET system adjusts for inflation with far fewer distortionary effects: the current TTE system imposes very different tax rates on the income from different assets, which is very distortionary, and to reduce the extent that some assets are substantially over taxed seems less like a "concession" than the adoption of a sensible tax policy. The starting point of TTE in New Zealand is so far from perfect that it seems odd to choose as a benchmark from which "concessions" are calculated.

As to foreign tax systems: there are some very good ones too. I am no more advocating we adopt a bad system than i am advocating we build bad bridges over a river to avoid using a ferry. You try and build good bridges, and if necessary look at archetypes overseas. Similarly, you look at tax systems overseas and see if they have features that work well. Social security taxes work. EET systems work. The Nordic dual tax system works. I agree, if NZ had the highest income, most productive and most innovative economy in the world, with little inequality, I might be less concerned that our tax system may be unfit for purpose. But we don't have that luxury: there are good theoretical reasons to believe our tax system is causing problems, and little evidence that it is creating a flourishing environment.

AC

Hi Andrew, thanks for the response, lots to ponder. You're right I probably should have read the rest of your series in more detail before raising my points!

I take your point about tax concessions. Basically, your proposed system moves us closer to a system that taxes consumption rather than income, which makes sense from the perspective of reducing economic distortions (though in isolation, it seems like a regressive move). I guess my main concern is looking at the American tax system, where it seems there are all kinds of tax-advantaged accounts or investments that mostly the well informed or well off with accountants seem to take the most advantage of (Health savings, education savings etc). But crucially, having KiwiSaver compulsory limits this potential downside.

I’m a bit more unsure what to make of your first point, when you say “This raises potential output”, do you mean the potential output of the economy, or the future returns of the financial savings system? I’m not a macroeconomics expert, but the latter idea, that we could just collectively make ourselves richer simply by investing more in financial assets feels a bit magical to me, as if the NZ government should just take on debt (at a low interest rate) and invest in the stock market for free money. I admit, we’d be a lot better off today if the Key government had done this with the NZ superannuation fund in 2009-2016! But the long-term logic feels off to me - surely the value of financial investments is determined by expectations of their returns, and future returns have to come from future production—i.e it’s a claim on the value of the future economy. I also would question your confidence that the last 100 years are a guide to the future regarding asset prices/investment returns. The last 100 have seen a one-off explosion of population and increasing financialisation of our economy.

If the scheme is so enticing, why make it compulsory?

Why force me to move my funds (which are in VOO / equities / gold / bitcoin) into a managed fund with lower returns AND a high fee? And lock it until 65 years old, when I'd prefer early retirement.

If it were not compulsory you would save your money elsewhere, then when you turned 65 you would put your hand out for 100% state funding of your pension. Thus the proposed plan can only work if you are compelled to save x% of your income to self-fund as far as possible your pension between 65 and 75.

Why make it compulsory? Because we don't trust you. That's why.

Even among my highly skilled, mathematically literate colleagues, there is a lot of financial ignorance and failure to plan for retirement. I dread to think how little the average Kiwi thinks about it.

I can totally understand the desire to make schemes compulsory.

It's not financial illiteracy is the problem.

It's physical/ecological illiteracy - coupled with the silo-problem within academia.

The joke in my circles, is that you can put 100 economists in a room for 100 years, and they won't come up with a ham sandwich.

Its human nature people want pleasure now, it part of who we are. Being mathematically literate doesn't stop you wanting that nicer house, holiday abroad, in fact the more money you have the more likely you are to fritter it away.

On the one hand a lot of people are lucky to own a freehold house by retirement given how extortionate their prices are in NZ and on the other compulsory super is a grift for fund managers (including ETF providers) who take their fees without having any responsibility for investment outcomes.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.