February was a steady-as-she-goes month for property website Realestate.co.nz, with listings down slightly compared to a year earlier but the total amount of stock for sale remaining remarkably stable.

The website received 10,535 new residential property listings in February, down 6.5% compared to February last year.

That trend was evident in most of the country, with new listings up compared to a year ago in just three regions - Wellington, West Coast and Central Otago/Lakes, but down everywhere else.

The biggest decline in new listings was in Northland, where they were down 20.4% in February compared to February last year, followed by Wairarapa where they were down 19.3% (see chart below).

However the website's total residential stock remained practically unchanged from a year ago, with 26,850 residential properties available for sale on Realestate.co.nz at the end of February, down just 0.3% compared to February last year.

Around the country, nine regions posted increases in the total number of properties for sale in February compared to a year earlier, while 10 posted declines (see chart below).

However the region where the figures stood out from the rest was Auckland, where new listings in February were down by 9.9% compared to February last year, while the total stock available for sale at the end of the month was up 6.7% compared to a year earlier.

That suggests buyers in Auckland will have plenty of choice as the market heads into what is traditionally the busiest time of the year, and vendors will have to be particularly realistic on price when listing their property or they may struggle to make a sale.

Realestate.co.nz spokesperson Vanessa Taylor said the property market had found a new normal.

"Unlike the Australian situation, where there's reportedly a long term high in the number of properties sitting on the market, that's not the case here," she said.

"We've been through the heady days of frantic activity and uncertainty and we have found our new normal," she said.

"It's characterised by a steady market, stable pricing and a pragmatic approach by buyers and sellers.

"It's a more stable environment where buyers and sellers can have more certainty and realistic expectations about what they can achieve in the current housing market," she said.

You can receive all of our property articles automatically by subscribing to our free email Property Newsletter. This will deliver all of our property-related articles, including auction results and interest rate updates, directly to your in-box 3-5 times a week. We don't share your details with third parties and you can unsubscribe at any time. To subscribe just click on this link, scroll down to "Property email newsletter" and enter your email address.

93 Comments

The Aussie version of the same thing said the same thing every other quarter since 2 years ago and is still spruiking. The word "stable" perhaps is being defined as not yet becoming Iceland 2.0 by the vested.

This weeks report from Metropole:

"Sydney auction prices are rising with Saturdays median of $1,230,000 higher than the previous Saturday’s $1,224,000 and now just 0.4% lower than the $1,235,000 recorded over the same Saturday last year.

Sydney’s inner-suburban, higher-price regions continue to produce generally strong results for sellers and from reasonably solid auction numbers.

The Lower North, Inner West and Eastern Suburbs were again top regional performers on Saturday with the South and Upper North Shore also reporting positive results for sellers.

February has provided some early signs of a recovery in the Sydney property market with prices and clearance rates now tracking similar to February last year."

From SMH:

"Sydney and Melbourne house values fell by more than one per cent in February, new figures show amid signs the national property slowdown is broadening to almost every market in the country.

CoreLogic on Friday reported house values in Sydney dropped by 1.1 per cent last month to be down 11.5 per cent over the past 12 months.

Melbourne values tumbled by 1.2 per cent and 4.8 per cent over the past quarter, making it the softest capital city market in the country. Over the past 12 months, house values have dropped by 11.5 per cent.

Every capital city bar Hobart reported a fall in house values with Perth down by 1.4 per cent and Darwin off by 1.3 per cent. There is also evidence that regional property markets, which until now have held their values, are also softening.

The February housing market results marked a subtle improvement in the rate of decline, however the housing market downturn is now more widespread geographically and we aren't seeing any indicators pointing to the market bottoming out yet.

Hi Masher the metropole figures are based on auction sales only instead of all sales via whatever method. The non-auction sellers could probably have done a lot better had they chosen the auction path. For them it is better luck next time.

I think you're missing the point....

Your argument is like someone commenting on how nice the life rafts are on the Titantic, yet they fail to realise theres only one way to arrive at that conclusion....

Sydney prices are tanking, and will continue to do so.

Houseworks just sprung picking a rotten cherries....

https://www.bloomberg.com/news/articles/2019-02-28/australian-property-…

One rotten cherry does not a make a rotten tree retired-poppy. When Auckland auctions get to a median 1.3 million like the Sydney median I will agree that the market may be due for a slight pullback and lose some cream off the top of the cherry cake.

Houseworks, your challenge (on condition you choose to accept it) is to present a basket full of fresh ones from healthy trees. If you can't, I guess all that remains is an empty basket...

House price reductions not possible you say? Are you going on record saying that "Auckland and subsequently the regions will not follow Sydney and Melbourne - down?

Speak up.....

How is your country & western ballad "Where Auckland goes the Regions will Follow"? Still a flop, nobody is buying it. I know you were hoping to get rich from that song, give it another three months and move on

Houseworks not prepared to go on record with a fact based prediction "Auckland won't follow Sydney". I thought you wouldn't. That's why I ask. Now that by default you believe the odds are indeed stacked to the downside, me now thinks you're a possum caught in the headlights.

I will explain this only once. You retired-poppy (and your disciple kiwimm) are the one making the big claims of destruction, annihilation and collapse in the regions and you have been doing so for over one year. Meanwhile the regions have continued to perform very very well, and furthermore the areas I focus on have actually strengthened. I am happy with the current state as long as it is zero or above so right now, as usual I am winning. You lose. Enjoy your evening

Houseworks, yup your a real winner :)

Too little, too late.

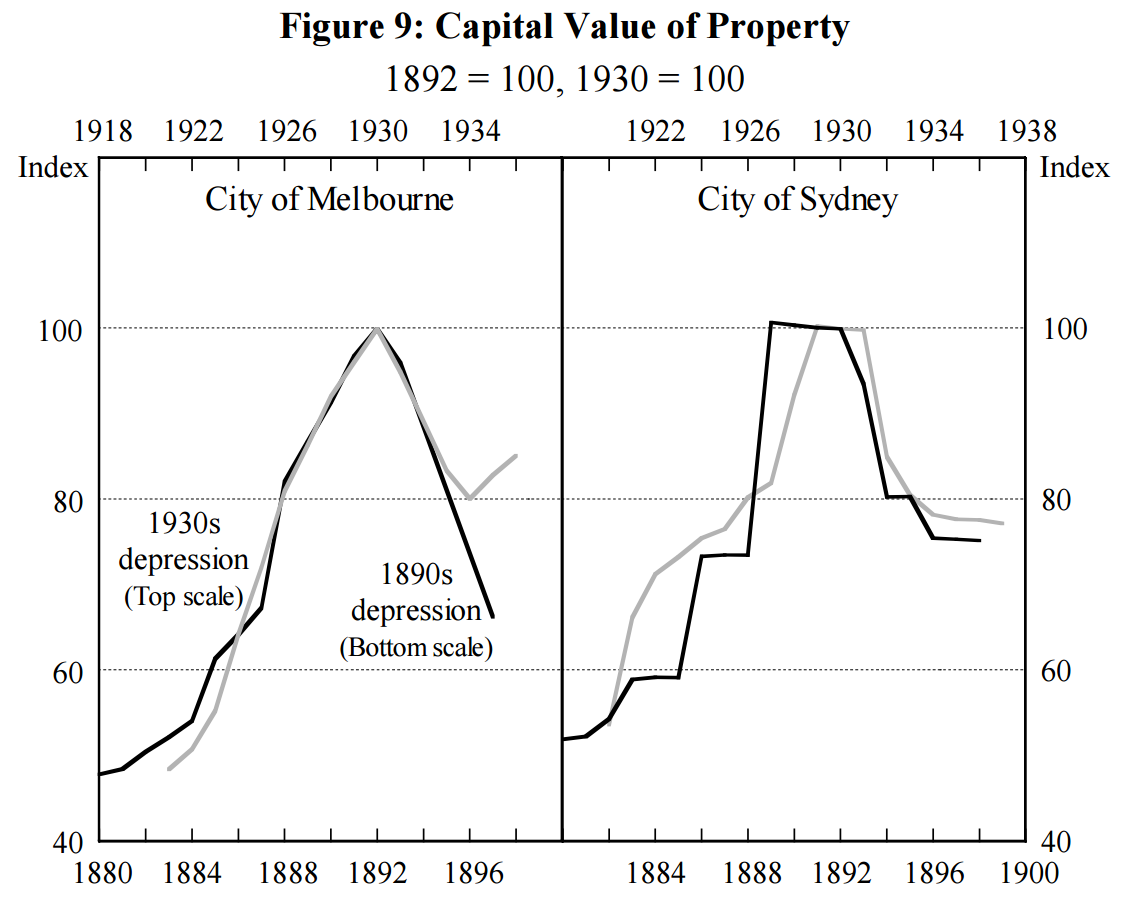

Is New Zealand just doing a “Sydney 1888 - 1892”?

https://www.macrobusiness.com.au/wp-content/uploads/2017/04/e6u.png

{kind=link}

If you read NZ history you will see the same period saw the same impact in Auckland. It was a mess that broke some and made others. Logan Campbell was a big winner. Slow and steady wins the race.

True, but at least this time will be different.

Nzdan, it's an interesting graph. The causes of the 1890s slump make worthwhile reading too ;) https://www.rba.gov.au/publications/rdp/2001/2001-07/1890s-depression.h…

That is the thing that is likely to catch out those highly leveraged residential property price extrapolators who purchased residential property in Auckland in the last few years. Especially those who extrapolated the price trends of the last 50 years of history to determine their future property price expectations. Those highly leveraged price extrapolators who used this method to purchase residential property in Sydney and Melbourne are now at risk of getting caught out.

The credit bubbles for residential property lending which lead to residential property price bubbles can be 50-90 year cycles as banks slowly build up lending on residential mortgages and relax their lending criteria over time to enable residential property purchasers to pay ever higher prices, and as individuals in management teams change. History is not learned by those individuals who manage banks and since they have never experienced it before firsthand, they repeat the same mistakes. It takes quite some time to set up the financial and economic conditions necessary for a credit bubble and residential property price bubble. It can take some time between bank failures - the last time a bank was recapitalised in NZ was after the commercial real estate prices collapsed and corporate failures in the late 1980's.

Banks start conservatively (such as 25% of gross household income for debt servicing) then become more lenient - using a bank website to determine a loan amount for a household on a Auckland median household income, one bank allowed bank servicing payments to be up to 45.5% of gross household income, whilst another bank allowed debt service payments of just over 40%. Two other banks allowed debt mortgage payments between 34- 40% of gross household income. And this is under tightened credit conditions by banks on debt servicing criteria. Only one bank was at 25%.

What happens when there is an economic recession and unemployment rises? If one person is in the construction industry and becomes unemployed, then the overall household income falls. If that household has a large mortgage then that household could be financially stretched, and may need to cut costs and even downsize (as that household cuts costs, there are knock on effects of reduced household spending on the rest of the economy such as retail, restaurants, travel, etc). If that household is a renter and wants to buy, then their borrowing capacity just fell significantly as they only have one income, so it is likely that they are unable to afford to buy on one income in Auckland.

When lenders focus primarily on asset based lending criteria (such as LVR) and are less vigilent on debt servicing criteria this can lead to a credit bubble which leads to a property price bubble. Some of the debt servicing lending criteria where the Australian banks have fallen short in their loan underwriting is the use of HEM's.

Then there have been cases where borrowers have overstated their incomes and assets (stories in Australia suggest that this was undertaken by mortgage brokers on loan application forms - incomplete loan application forms are first signed by loan applicants and the numbers for assets, liabilities and income are completed by the mortgage broker afterwards).

There’s a lot worse to come in Australian property market

Just wait

Worse still is retirement savings have been piled into extra investment properties with loans

NZ is looking pretty good unless your migrants sell & fly away

excerpt from the article

The overextension of the 1880s property boom and its unravelling led to an abrupt collapse of private investment in the pastoral industry and urban development and a sharp pullback in public infrastructure investment. A fall-off in capital inflow from Britain, adverse movements in the terms of trade and drought in 1895 accentuated and prolonged the depression.

The 1880s property boom was financed by rapid expansion in bank lending. In addition, many building societies and property finance companies, known as ‘land banks’, sprang up during the 1880s. The increased competition from such new entrants weakened banks' prudential standards (Merrett 1989). While some recognition of this came in 1888, when the Associated Banks increased interest rates and adopted stricter capital standards, for many financial institutions the damage already done was too severe to be repaired (Boehm 1971).

The collapse in property prices in 1889 led to a spate of building society failures in 1890. As it became clearer that the fall in property prices was not just a temporary fluctuation, the financial collapse spread to the land banks. As the number of failures and frauds grew, public confidence in financial institutions faltered, spreading the crisis to the institutions at the core of the financial system – banks that issued their own bank notes.

I don't want to reveal sources, but I have it on good authority that Christchurch property is the most stable at all.

*giggles*

Your source clearly knows what he is talking about!

What do ya get when you combine a slam-dunk with Poe's law?

A post from a podunk. ;)

I've now researched what podunk means... Haha, tuche! Perfect. In my own posts defence n education for others.... An astericks *followed by another asterisks* denotes an emotion or a truism over any intrinsic or face value of the statement or idea prior. Maybe po's law is now a bit out of date? I dunno, I'm just sharing :)

FLOCCINAUCINIHILIPILIFICATION

Some regional cities in NZ are still holding/increasing buoyant house prices.

Rentals hard to find, and family homes to buy in good surburbs also hard to find.

No signs of price collapse there yet.

there is always a lag between the regions and Auckland

BUT do you wait if buying as by that time the value lost in Auckland and what you can buy in the regions can narrow for both OO and those using leverage for rentals.

and whatever you do dont say you are a Jaffa, its an automatic 50K added to the buy price

Sigh. Happy for the Auckland stories to be "all about Auckland". But in the rest of the country the story is not "all about Auckland". They have thir own stories and drivers.

And at the moment a large part of those stories is the Auckland Exodus.

The regions are actually a very interesting example. Most regions have had very low (or no) population growth, as opposed to what's occurred in Auckland. Yet prices started increasing faster around the time returns on Auckland Investment Properties fell to abysmal levels .

Hmmmm I wonder why?

My customers in the regions (swimming pool builders) have their order books full building pools for.... aucklanders who escaped with their I'll gotten gains....

Past patterns are no longer a predictor of the future.

There is an abnormal outflow of families and older Aucklanders exiting Auckland and moving to more liveable and more affordable houses in popular regional cities So a) is there a decline in Auckland prices in the middle bracket anyway? And b) will any Auckland decline necessarily hit the regions, especially Hamilton, Tauranga, Napier etc - now desirable family friendly, commuting friendly areas with good job growth. And superior lifestyles.

I too fully expect prices to rise and The Tron to become more expensive than Melbourne.

Go the Tron and Toe-runga

So listings have declined but the total number has remained stable because houses are staying on the market longer and not selling...

I've seen about 4 houses relisted in the last 2 weeks in the Howick and surrounding areas that failed to sell last year.

I dont want to reveal sources but I have it on good authority that the Auckland housing market will drop significantly in the next 6-8 months (tip of iceberg at the moment). Housing developments (outside of HLC and HNZ) by building companies will stop. Double cab utes will flood the used car market and the construction environment will look very different....all by the end of the year. I know of a number of developments that are going on hold and developers taking a bath trying to sell their current stock. I am in the industry and we are the canary in the coal mine. I are seeing this happen now. There are serious storm clouds on the horizon. Dont listen to the rhetoric about immigration and lack of housing. Hog wash. This is from someone with feet on the ground and in it.

Is that you, Mr Twyford?

It will be interesting to see if that comes true. I'm scoping out major home improvements and am getting early numbers back between $250,000 and $300,000. Maybe those will come back $50,000 or more if the market tightens, but then where will the fat be trimmed from? I suspect the quality builders will hold their prices but be more efficient in getting the work done - no hopping from site to site.

Hi BH, Thanks for your "feet on the ground" report, a lot more valuable than "my opinion is…" I agree new developments are struggling, many that are coming on the market now started taking shape in 2016 and were counting on house prices being higher now than then. I too personally know several developers who were doing ridiculously well 2011-2016 but it wasn't really because they were so good but more because prices were so much higher by the time the development was completed.

I do disagree with one point of your post though, the fact that developers are struggling to make a profit does not mean that existing houses "will drop significantly in the next 6-8 months" (your quote), they are quite separate and no, having to sell a new (read expensive) development at a discount, does not drag existing housing down

Eh? If the market was previously a choice between an established (but a bit tired) house at say $700k, and a new build at $850k, the the price of the new build drops to $775k, how can that not affect what people are willing to pay for the established property?

Yvil and the likes also do not understand that when house prices fall and homes become vacant, rents will fall as well because renters have more to choose from in the rental pool. Meaning that they can get a better home for their rent. Which gives them the ability to milk the home owner and just kick back and wait/move until/when something great comes their way. All this time the landlord is paying off his or her mortgage debt btw. The landlord needs to stay competitive in this market. The tables have turned.

Why do you think homes will become vacant as prices fall? Where do the people disappear to?

Tenants can move anywhere. That's the beauty of renting.

Fair call. Tenants with jobs or without jobs? I guess as there’s an exodus from Auckland there’s increased demand in the regions, so those who cannot afford to buy in Auckland might find it easier to get a job?

Not just Auckland, every city centre in NZ currently has a surplus of people who cannot afford to be there. Too many students and beneficiaries.

It would be natural for city centres to become even more expensive over time and only the successful people stick around. Why do you think so many beautiful/pretty people are drawn to the major hubs of the world? It is no coincidence.

It is a natural selection that can be seen in every major city centre of the world. It also common for successful people to rent in centres instead of owning.

Outside CBD's (in the burbs and beyond) the supply of accommodation will go up and prices will come down. Tenants with jobs can still work in the city they just cannot afford to live there.

... Palmerston North !

Moving to Palmy North Voluntarily? Interesting concept.

They will all be crowding into the rentals that are left so landlords can crow, "look, we have an average of 23.75 people in each of our houses, you won't get that with owner occupied".

Most students and beneficiaries would move out of the city centers. So no need to all live together. Part of the problem in NZ is that people who cannot afford the city are still in denial. They will figure it out.

Like it or not housing market in Auckland is on downward trend and to expect otherwise is wishful thinking and no harm in being positive specially if you have lot invested in housing market but reality is that this downward grend has just started and wl continue for some time to come.

Like it or not the report above states the market is "steady as she goes" (you should read it). Suppose you think you know "alittle" better

Genuine question. Do you actually believe it's a good idea to trust the analysis from a source that has a strong vested interest?

If prices start to fall (like in Sydney/Melbourne) it's highly likely volumes of sales will fall at the same time. This is bad for Real Estate agents (fewer commissions). Thus they have a strong incentive to downplay this scenario.

I don't think old Vanessa has ever said a negative word about the real estate market in her life

Asking price is not the same as selling price! Selected data to serve their self interest.

And asking price is time dependent.. Asking price today will be $50k more than asking price in three weeks in many cases.

I'm going to list my property with an asking price of $72 Trillion, watch as average asking prices go through the roof.

No doubt they'll probably discard my figure from the dataset as an outlier.

Gee you never know your luck with a tail wind.

..nah they include it. Its only an outlier if it lowers the average.

... but if he's asking $ 72 Trillion for an Orc Land City house ... that will lower the average ... won't it ?

how True this is, the great example would be

125 Paremoremo Rd, Albany

2019-01-23 $1,375,000

2019-01-25 $1,275,000

2019-02-11 $1,100,000

2019-02-21 UNDER OFFER

Again I am having to inject some front line experience.

"Buyers have more choice" - is the housing market doomed to have cliched drivel tripped out every month regardless?

Stock is up because it is not selling.

Look at RE NZ regularly and pay attention: Gulf Harbour for instance - 54% of listings over 3m old.

There is more choice of old stock - like a tin of chocolates, that is all that is left because people do not want it.

New listings peaked 3.12.18 in Rodney.

Listings in Waitakere are down on where they were on February 15th.

People are listing less because they cannot get price they want, hence listing rate per day stalled 2 weeks ago.

Furthermore 25% of what is generically referred to as "stock" under houses and townhouses in FACT has no house on it - not built or not finished.

23% of what is sold in Hibiscus Coast (sorry, ON SALE) is land.

Finally, and AGAIN ad nauseam, Auckland does not have a shortage of housing.

It has a shortage of good quality reasonably priced housing to RENT.

And cheap decent housing to buy with 3 beds near sources of work.

Builders do not want to build that, or costs of doing so are prohibitive.

In terms of rental stock, government should be building it instead of piddling about with KiwiBuild for a max of 72,000 potential younger couples in Auckland.

While I am here: NSC prices and sales dropping precipitatively

It would be really nice if Interest NZ would do a few articles that stop generalising about market in housing and look at particular aspects in particular places. V frustrating

Stock v sales. On a 3 month average , there is now 6.56 months of currently listed Auckland housing stock when viewed against sales, an increase of 14 percent year on year, up from 5.82 months There is no rush to buy any Auckland property. It will gradually spread outwards.

Few months back - Last year had read the similar headline that Sydney market stable...........but now........

Being positive is good but if making investment decision than read the market correctly or else will have no one but yourself to blame. Media will present a new data/story every day which may not be a fact for data.......

Buying at low price is always a good time to buy but should buy only if have long term perspective or holding capicity in a falling market.

Vanessa's pronouncements remind me of one particular character from the 2003 Iraq invasion (stay with me)....

... anyone remember 'Comical Ali'? Bravely commending the Iraqi armed forces on TV for their demolition of US troops, while US tanks appeared in the background.

Propaganda...propping something up until the weight of the lies causes it to collapse in on itself. More debt ponzi with your popcorn anyone...?

"Comical Ali"? I thought that was Ali Williams

I have had some interesting conversations with RE agents in the last week (I'm looking at smaller houses or units in Central Auckland).

One, at an open home, attempting to convince me that the Auckland market has dropped at least 10%, even though "you'll never hear about it in the media".

The other on a follow up call after attending an open home, where I had expressed that I thought the property was overpriced. He was agreeing wholeheartedly, and just letting me know that he was working hard on adjusting the vendor's expectations.

So the conditioning has started.

Also starting to see some discounting on TradeMe.

Anyone else here have similar experiences? Have the RE agents switched from trying to talk prices higher to talking them down in order to pressure vendors to accept lower offers?

Had a RE Agent call us saying the vendor would now look at offers in the region of what we indicated in December. 100k below the asking price that was updated on TradeMe in Jan.

The agent conditioning behaviour you have described is nothing new, I am pretty sure. Usually starts the day after the listing agreement is signed. Apart from the properties that are in hot demand that effectively sell themselves.

Housing stock same as last year???

Realestate.co is fenced to allow only agents' listings.

Trade-Me listings tell a different story though. Just trawl the following and figure out yourself

Auckland listings

February 2018- 12,208

February 2019-13,547

Figures same as last year?? Either a person has zero mathematical ability or needs his vision checked!!!

Hmmm! Whom do we believe? A body with vested interests in real estate & trots out self-serving figures ?

The article above does NOT say that the Auckland housing stock is same as last year, actually it says, quote:

"... Auckland,... the total stock available for sale at the end of the month was up 6.7% compared to a year earlier"

(I edited out the non-relevant parts for you)

Maybe your statement applies to yourself? "Either a person has zero mathematical ability or needs his vision checked!!!

I'd like to know where the sellers in Auckland are moving to. Are they relocating outside of Auckland, upsizing, downsizing, moving overseas etc. It would be good to know the recent trends in this area. I did ask a real estate agent this question a few months ago and his reply was that the REINZ should be gathering this information - completely missed the fact that the agents would need to collate this information on their behalf so he should have a general idea of trends. I mean you would think that this would pop up in conversation at their weekly sales meetings. Just got the impression he didn't want to go there.

We don't know that they are not investors selling some of their stock , or overseas owners cashing up. The problem is that there are very few statistics. It was only until very recently that we actually had any idea how many overseas buyers were buying houses, and that stat isn't very accurate.

Also worth noting that Realestate.co.nz has 13990 total listing for Auckland this morning. The peak before Christmas was 14398 on 22 November.

Not that theirs any conflict of interest here, could it really be a Mexican stand off?

Denial won't help the over leveraged property investors / speculators, who would be better advised to cut their losses before its to late, as the smart ones are doing now.

Damn statistics & lies:)

The headline "NZ housing market is stable unlike Australia, says Realestate.co.nz". It's like "Consumption of MSG is perfectly safe. says Takeaways Food Association"

Both true to an Extent.. Both should be taken with a pinch of salt.

Taking MSG with a pinch of salt might make it overly savoury.

One has to query the motives of some of the contributors above - those who appear to resent the observation that the NZ housing market is pretty much stable......

TTP

Nah, we are just planning ahead for the benefits of the next generations!

So any pearls of wisdom from you TTP or have you had time to accept reality that they market is headed South for the long run!

If you head south for the long run you actually end up heading north

If you head south for a long run in NZ you end up in the Ocean.. Underwater.

So Australia is down like 11% and I think we can agree Auckland is down like 10% at present, so what ? hardly time to panic.To many people on this site thinking its the first sign of a crash, its not happening guys, not yet at least.

Death by thousand cuts....

... yes ... I think that Carlos67 may be missing a vital point .... that it's no good calling it a crash after the market has dropped 30 or 40 % , if you remained long , during the death by a thousand cuts ...

Folks wanna crystal-ballerise , they need to see whether to sell and lock in profits now / or whether to hold off buying that first home ...

... we need prophets to guarantee our profits ...

RE: 10%, is it likely that this will be got back in the short term and we'll see another 20% gain? if that is unlikely and surely it is why are you still in the game?

Problem is time lag from deciding "oh my god we are all going to die" moment to actually getting the money from the sale into somewhere "safe" (good luck with that).

I think the Experts need to break up the markets in to different regions, rather than just make a sweeping statement for the entire country. The country stats average things out, and people can always cherry pick particular stats to support a position.

Also as most of NZ banks are owned by Australian banks, I think we are kidding ourselves if we we think what happens in Oz, won't affect us here.

Real estate industry owned company says real estate is stable.

Well ok then.

Can't be doing with no neigh sayers around here

Wow 2.06 million. Gross rental yields are going up in upper quartile Auckland!

https://www.barfoot.co.nz/property/residential/auckland-city/st-heliers…

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.