Barfoot & Thompson sold a third of the residential properties the agency marketed for sale by auction last week, while Bayleys sold half of their auction properties.

Barfoot marketed 142 homes for sale by auction last week and sold 47 either under the hammer or by 5pm the following day (see table below).

At Barfoot's main auctions, there were sales clearance rates of 30% at the Manukau auction, 23% on the North Shore and 33% at the Shortland St auction on 17 May, when most of the properties on offer were from central Auckland suburbs such as Grey Lynn, Epsom, Mt Eden, Mt Roskill and Kohimarama.

Bayleys had 14 Auckland properties scheduled for sale by auction last week and sold seven. At Bayleys' auction south of the Bombays a house at Matamata sold for $690,000, and a two level townhouse at Cambridge was sold by mortgagee sale for $339,000.

You can see the individual results form both agencies' auctions, with the prices achieved on the properties that sold, and details of the properties that didn't sell, on our Auction Results page.

| Date/Venue | Sold | Not sold | Total |

| On site. 16-20 May | 3 | 7 | 10 |

| Manukau. 16 May | 6 | 14 | 20 |

| Shortland St, CBD. 16 May | 6 | 5 | 11 |

| Whangarei. 17 May | 3 | 5 | 8 |

| Pukekohe. 17 May | 0 | 4 | 4 |

| Shortland St, CBD. 17 May | 10 | 20 | 30 |

| North Shore. 18 May | 7 | 23 | 30 |

| Shortland St, CBD. 18 May | 7 | 15 | 22 |

| Shortland St, CBD, 19 May | 5 | 2 | 7 |

| Total | 47 | 95 | 142 |

You can receive all of our property articles automatically by subscribing to our free email Property Newsletter. This will deliver all of our property-related articles, including auction results and interest rate updates, directly to your in-box 3-5 times a week. We don't share your details with third parties and you can unsubscribe at any time. To subscribe just click on this link, scroll down to "Property email newsletter"and enter your email address.

55 Comments

Similar low rates at many of the Tauranga auctions I have attended recently. The tide has definitely turned although many vendors are still being unrealistic with their asking prices as are some real estate agents.

I'm wondering why so many people are still sending their properties to auction. The bloom is definitely off the rose.

Because a Barfoot agent will get more of the commision if it sells via Auction.... introducing agent fee's a lot lower then if sold via negotiation... pure self interest mate

Does anyone know how many real estate agents in Auckland?

Are we back to 2012 price level yet? If not don't expect the auction results to be anywhere close to 100%. The current overcooked house prices are not sustainable for the average families and FHB's. Hopefully National is able to change this before the election, otherwise...

> a two level townhouse at Cambridge was sold by mortgagee sale for $339,000.

Gulp. Wow.

This is the season for bargain hunters. Only a fool would pay a high price for a dwelling in Auckland.

that Cambridge one had a 2016 CV of $420k

last sale was a long while ago.....

2 bd rm on a cross lease

It doesn't sound that great. They probably paid too much.

no they bought it ages ago, probably just borrowed for business or other use etc

I was talking about the current buyer. :)

Cool, let's do what Agents do and use latest sales information as a benchmark for value...

Vendors should expect a 19% discount to CV based on latest sales.

Mortgagee sales can be hit and miss, some are great when you get a troublesome tennant who wont let most people into viewings and has a big dog etc ... $20 notes work 8)

It last sold in 2004 for $175k... How do you buy a property in 2004 and have a mortgagee sale on it 13 years later? Surely you would have most of the loan paid off by then?

business lending secured against it tuned sour.... one of many reasons

Or, they had increased the mortgage and withdrawn equity to buy other properties, which seems to be the most common "investment" behaviour in recent years.

Something I've noticed with every mortgagee sale for the Auckland region is that they are 10+ years since the purchase. Change of circumstances (drop in income, etc) or additional borrowing to maintain spending more than they earn are the likely cause.

Ive seen a few buy businesses, although the thought process is more about buying freedom from the man.The cross over from corporate to small business is a a huge leap of faith for some.

Right. Thanks for the info guys :)

Or it's a foreign national who's left the country, leaving their debt behind.

Are Barfoots on course for record low sales volumes for the May month. Obviously auctions are but the coalface of sales , but 132/360 sales currently for May. If you are a prospective vendor you have currently a 1 in 3 chance of selling by auction , possibly because you are overpriced or out of luck. Price is but an opinion, even the Chinese have relocated their counting trays.

Looking forward to the new Auckland re-valuation in July 2017. I expect the new CV's to be around 10-20% less than the 2014 CV's, which will be a relief for the FHB's and struggling families trying to purchase their own homes.

That is extremely unlikely Double-GZ.

In a cooling market the new CVs will have to reflect or 'meet' the market, especially when the new values are going to be set for the next 3 years. The market is obviously pointing to a downward trend over the next 3-5 years so it is quite reasonable to assume that the new values are adjusted accordingly.

Confirming the desperation and confusion of Auckland housing Double GZ and Zach go head to head.

Actually I will still be wealthy at 2014 values and I suspect DGZ will be too.

Zach, I detect a note of apprehension in your post.

I am apprehensive about Double-GZ's state of mind.

So any countering of 'out there' statements is going to be a sign of apprehension? I see.

I will be wealthy even if it goes back to 2008 level. Right now I just want to see lots of support for the FHB's and average families who are struggling to purchase their own homes. I feel sorry for them especially for the people I know I just don't want to see them suffer.

That's all well and good however you are being disingenuous when you state, "I expect the new CV's to be around 10-20% less than the 2014 CV'..." as if it is a real possibility for July 2017, a matter of weeks away. You could, perhaps, say, "I hope..."

It doesn't matter what I say you will always find something to correct me. I have no intention to sell in the foreseeable future so I really do HOPE the market will crash to give some relief to the FHB's.

DGZ, have you had a road to Damascas moment?

This attitude you're showing is a 180 degree turnaround from your previous celebrations and wishing for the government to encourage greater immigration and foreign buying to push prices and rents up, up and away.

"Kaching, kaching!" were your previous words...

Why this change of heart?

I am not a drone and I have a real human heart. Is it really that unbelievable when people have a change of heart? If a married couple have a change of heart and file a divorce, why can't I do the same in terms of my view point?

I'm not criticising, DGZ, just genuinely interested. Would like to hear more about how the change of heart came about, if you're happy to share.

As an aside, speaking of divorce...that's obviously going to become a no-go for many now, given they'll be unable to get into a house again after halving their assets.

DGZ and Zach is one and the same person playing both sides/mind games now in order to get a reaction. Totally disregard him. You cannot be so cruel towards those struggling to get on the ladder then change tack completely and still have credibility.

Gordon, after saying the same thing for so many years aren't you feeling a little tired?

Zach the more you comment the more obvious you and DGZ are one and the same person. You are here simply to upset people and now you are confusing them which is even crueller behaviour on your part.

That's not obvious at all. Keep in mind that values don't really affect rates charges across the board so it really doesn't matter all that much. Rates will neither go up nor down because of value changes. And, dude, 10% less than 2014 figures would represent a massive fall in prices. This is not the reality.

Not enough water under the bridge for it to affect the 2017 CV's I am picking they will stay static (or minor changes either way) but with those few areas in the country where sales and price hikes are happening will in fact go up....

That would be a pretty safe bet to put money on. In fact it would be unconscionable to place such a bet. Maybe a long shot for the 2020 valuations.

CV's assessments have two components - The Value and the Rate that the value is charged at. Conceivably, the Value could halve, but rates still go up if the Rate at which the Values are assessed is increased. Councils need $X to run their patch. How they get it is simply a matter of maths....

I'm not saying that I want the rates to come down. I just want the house values to come down to 2012 level to give hope to young families struggling to purchase their own homes.

0 out of 4 in Pukekohe, thats great news.

Auctions definitely aren't so relevant in a cooling market.

But their time will come again.

In the meantime, those with counter-cyclical investment strategies can do quite nicely.

First home buyers should have a better chance. And hopefully so.

Housing shines as a long-term investment - especially in Auckland and Wellington.

I dont think FHB should get into the market now, too much uncertanity so best to wait. No point paying 50-100K more for a home you are sure to buy cheaper in 12 months. Keep renting far cheaper option right now and wait for the down trend to continue. It will bring a reality check to vendors with over inflated expectations who will have to drop asking prices to reasonable levels. More supply on the way, reduced immigration number, higher interest rates perfect conditions for the downward trend to continue. Dont get caught up in the RE spin, trust me the tide has definately turned in your favour.

I hear from an increasing number of young Kiwis who were raised in Auckland who have simply lost interest in Auckland for the long term too. They're looking more at perhaps working in Auckland for a while, then moving to a different part of New Zealand to settle, raise kids etc.

Not to worry, I'm sure National will keep importing an alternative lower class population to fill the gap.

Could that be the plan? Auckland will be a working city populated by the rootless cosmopolitans while those wanting to settle down and raise families will head out and reinvigorate the regions? Historically revolutionary movements have drawn their heavy lifters from the country folk while cities have been dens of inequity. The trouble is in modern times most people are urbanites thus making radical social change rather an unlikely possibility.

...keep importing an alternative lower class population.

From an old school point of view that may actually make sense. If you wanted to raise your own people up you could import "lower classes", you know, to do the jobs you don't want to do. I believe Saudi Arabia does this. Probably a bit short sighted though.

It could be the plan, indeed.

I wonder if we can look and see any other places where importing large numbers of people from the third world then giving them low wages, unenviable lifestyles, and ultimately some level of marginalisation from the more well-to-do population has worked out well for all concerned?

I don't think so. I think we can see plenty of examples of - once a critical mass is reached - young, marginalised people ripe for picking by extremists and ideologs.

We should as a society be worried about creating huge inequality of opportunity and - at some level - outcomes.

Worked okay in the Southern States for a while in the 1800's while the cotton fields needed picking....

In modern NZ, swap cotton for rent to be paid to Darkords and cheap takeaway restaurants...

Sorry to be that tiresome pedant, but you've misspelled that. Should be d-o-r-k-l-o-r-d-s.

2 class systems, South Africa, Fiji etc... dont bode well. Although then the national government could build mud huts and walkways for the underclass thus fulfilling most of its affordable housing promises. The utility companies would need to work out how they can get paid for open fires, wells and long drops. I'm sure after six months of meetings they will have an equitable solution.

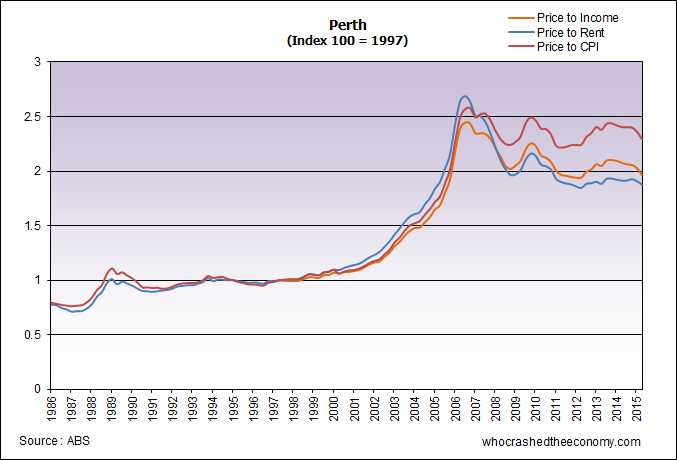

GS - I'm thinking much longer term than that. I think we might have seen the highest house prices in Auckland that we'll see in a very long time. Big call perhaps, but I just don't see where the credit is going to come from to push them any higher...Unless there is a significant blackswan type event, that causes a big reversal in immigration (which may see a short sharp correction), I think there might be a long and slow decay in house prices in Auckland. That could take 10-15 years to return to some figure that would make it a buyers market. About he same time as the babyboomers are all downsizing and moving into retirement villages....See what's happened in Perth in the link. I'm sure there were people there in 2006 who were saying that house prices will never drop, because everyone is coming here and its great, but look at the chart. It's stagnant. And if you took our a whole lot of debt to buy a house in 2005/2006 - the ROI on that would be terrible...

http://www.whocrashedtheeconomy.com/graphs/Perth_PriceIncome_PriceRent_…

{kind=link}

I am also very worried about Double-GZ's state of mind, rather than the state of the housing market!

Does anyone know where he lives so that they can call in on him to check out that he is ok?

I really wouldn't want to place any bets myself on when or how the housing correction will come. If there was accurate information about how many ghost homes there really are, how many houses are actually owned by overseas investors etc, then we could assess the actual fundamentals, but its still all smoke and mirrors. The current slow down could be the beginning of a major correction or a long term stagnation.

When I look at NZ household debt and debt to income ratios, my eyes water. NZ has supposedly had more growth and economic success than the rest of the developed world since the GFC, so why are its citizens more indebted than anyone else? The supposed rock star economy hasn't filtered down wealth to its citizens if they have no savings and nothing but piles of debt. Regardless of what their houses are worth on "paper", it looks extremely precarious for the indebted NZ-ers.

Modelling on debt cycles state that at some point all that debt will have to be deleveraged, and considering most of it is mortgage debt, that can only really mean that at some point, lots of home will be going on the market. Sure, houses prices will probably revert to the long term trend point at some point in the future, but there is no telling what the route to that point will look like. The human animal has never proven itself to be all that rational and calm about risk.

accurate information about how many ghost homes there really are, how many houses are actually owned by overseas investors etc, then we could assess the actual fundamentals

Lets say these numbers werent damaging. What would the average politician do with them ?

So the answer is, the real numbers are hugely damaging, and the ponzi is too big to fail.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.