Bernard Hickey talked to Nadine Chalmers-Ross on TV One's Breakfast program earlier today.

They discussed the roaring Auckland housing market and how the Reserve Bank is viewing what is going on.

Many first-home buyers have never experienced anything but very low interest rates, nor any period when house price fall.

This lack of perspective is seeing some people gear up dangerously, some with risky 100% LVR loans.

Although the situation is only a problem in Auckland at present, history has shown that such bubbles spread out from Auckland once they take hold.

The usual dampener is for the Reserve Bank to raise interest rates, but such a move will hurt already struggling businesses and exporters and push the exchange rate even higher.

Alternative dampeners are being readied by the Reserve Bank including LVR controls, but the regulator does not think now is the right time to bring them in.

However, Bernard suggests the situation is rapidly spiraling and both the RBNZ and the Government need to step in very soon to calm things in the Auckland property markets.

36 Comments

Sorry, Bernard did not really give answers to the problem other than response to the earlier comments from the broker.

He could not do so because it was only a few sound bites he was given to answer specific questions.

No opportunity given to address the investor who does not need finance who can easily outbid the finance tied aspirants. The RBNZ cannot answer that one. Only the Government can do that and that avenue is populated by incompetents

Good on you BH, you cashed out your Epsom for over $1m, then you are talking abot cooling housing market.

All you are telling me is you are going to buy a house soon.

However, Bernard suggests the situation is rapidly spiraling and both the RBNZ and the Government need to step in very soon to calm things in the Auckland property markets.

Leave no stone of moral hazard unturned eh, Bernard - parliamentarians and their central bank apparatchiks will not only seek to curtail private lawful activities they will feel duty bound to rescue the not so nimble at a cost to the taxpayer - witness SCF- best to leave gamblers and their losses to their respective bankers while prudential regulatory guidelines are being adhered to.

A serious round of losses will create opportunities for the younger family buyers. Harmony all round then.

The RBNZ and Monetary Policy are completely snookered.

Interest Rates

If the RBNZ increases interest rates, the only people affected will be local businesses, local borrowers with an existing mortgage, make it more difficult for a LOCAL first home owner to raise a mortgage. It will increase the value of the NZD which will attract more overseas money which will chase property and force up prices further. It will have no affect on overseas buyers borrowing money overseas and bringing it into new zealand to buy property

LVR's

The only people affected by LVR's will be LOCALS who need to raise a mortgage locally

No affect on outright cash buyers, whether resident or non-resident

No affect on buyers who can borrow overseas.

iconoclast,

do you hold EDA and are you disappointed like me?

I'm inclined to agree Stephen. If a bunch of Manic Aucklanders want to blow up a house price bubble I'm past caring. What were some of the more deranged "investors" saying on this web site? $1m average house price in a year or two. Something like that.

Buy your home when these clowns have lost the lot.

Keep up with the warnings, Bernard. Young people need to know.

..... and need to VOTE. Tell the pollies what you want!

first home buyers should buy in

HAMILTON.

We would welcome more people down here along with everthing that comes with them like more crime and traffic jams.

On seconds thoughts just stay where you are .

Of course interest rates will rise, eventually; one only has to look at the historic charts to see that this epoc is an aberration. What should Auckland first home buyers do? Simple, buy somewhere else .Rural New Zealand offers lots of job opportunites (real jobs too not in pansy offices) and houses with big sections for $100-300K. The young, in particular, are too fussy - give it a crack, you all may be surprised and never look back at squalid Auckland life.

Ergophobia

To paraphrase Bill Clinton , " it's the land supply , stupid " ....... free up some land for development , and watch the section prices tumble ....

....... until the stupids in charge of the land supply (the local councils throughout our great land ) are brought to heel , the supply / demand squeeze will continue to drive house prices up and up ...

Tell first home buyers to head down to their local council chambers , and raise merry hell with those ignoramuses ...

what is dubbling?

dunno what dubbling is

Though I did get a bit of a surprise from urban dictionary when I found the entry for "Dubble Bubble Trubble"

Dubbling is a city in Ireland , isn't it ?

Dubbling is short for dumb arse.

Snippy - the biggest problems lie in the area of Council who are controlling the land supply. Councils are making big money off developments and the building consent and applicable RMA fees.

The other big cost inflator is GST. Take a land and house package selling for $500k the GST component is $65.217.39. (500,000 x 3 divide by 23 gives you the GST component on Inclusive prices). This brings the GST excl price to $434,782.61.

Surveying costs are also enormous even just to do a boundary adjustment.

The banks don't have any control over any of these costs for that is not their business.

Supply of land for housing is severely restricted by Councils. Demand for housing is high so the price is being driven up.

House prices will continue to rise so long as building including land and infrastructure costs plus GST exceed the cost of second hand houses that are already established and free of tax.

For example a $500,000 new house carries $75,000 tax on top of everything else.

This tax adds nothing whatsoever to the value of a new build house.

Therefore used house prices have a long way to go to before they catch up to new builds.

The party ain't over yet folks.

It's still drinks and nibbles.

Attn 1st Home Buyers: Look for Gypsy Tea Room, Black Box Boutigue, and Richmond Rd cafe - you know where!!!

The best thing a first home buyer can do is wake up to the fact that should they do so, they are going to be fleeced. Interest is a method of redistributing wealth, if you are paying then you are willingly handing your future over to those receiving.

The young buyer should get familiar with terms like fiat money and fractional reserve banking. It wouldn't hurt to get schooled up on ponzi schemes either, where the last suckers entering get taken to the cleaners. On top of that look at the peaking trend on the world population graph and realise that the new input of suckers to fuel the housing ponzi scheme is drying up.

..realise that the new input of suckers to fuel the housing ponzi scheme is drying up.

So long as the Governments of the day remain captured by the growth lobby and maintain positive immigration it won't matter for quite some time that the world population at a macro level is decreasing.

True, but my pick is that at some point there will be a rapid decline in employment over a period of months that will really result in pressure on immigration. As the kiwis come home from Aussie it will add fuel to the fire. I am seeing signs that this process has been in progress for a few months and might accelerate in the new year.

Personally I doubt that the plug will be pulled on immigration in my life time.

It would require a big enough percentage of the NZ voting population deciding that the "growth forever" story is a crock. And start voting appropriately.

My perception of the New Zealand voting population is that is very unlikely to happen.

My gut tells me that the quality of life for the poorer part of the NZ population would improve with either zero growth in population or perhaps the population size decrease a little from where we are now.

However, doubt very much that would be a popular or commonly shared view - especially amongst those in the growth lobby who are keen to see their ability to seek rent increase in line with an increased population size.

Well I have to say I share your opinion of the voting population.

Are you 92 and on your last gasp

;]

a) Personally I think it will be a max of 20 years and maybe even as little as ten before the plug is pulled.

b) Its not a Q of deciding growth is a crock , its a Q of it wil be forced on us. Personally I odnt think we will admit it until its (considered) irrifutable by the blindly dogmatic.

c) I dont agree on your gut, we live fossil fuel, and the poorer are always the worst hit.

d) "growth lobby", see b)

regards

Steven

If I live to be as old as my father is now I'll have at least another 30 years

I think it will be more like 40 to 50 years before NZ wakes up.

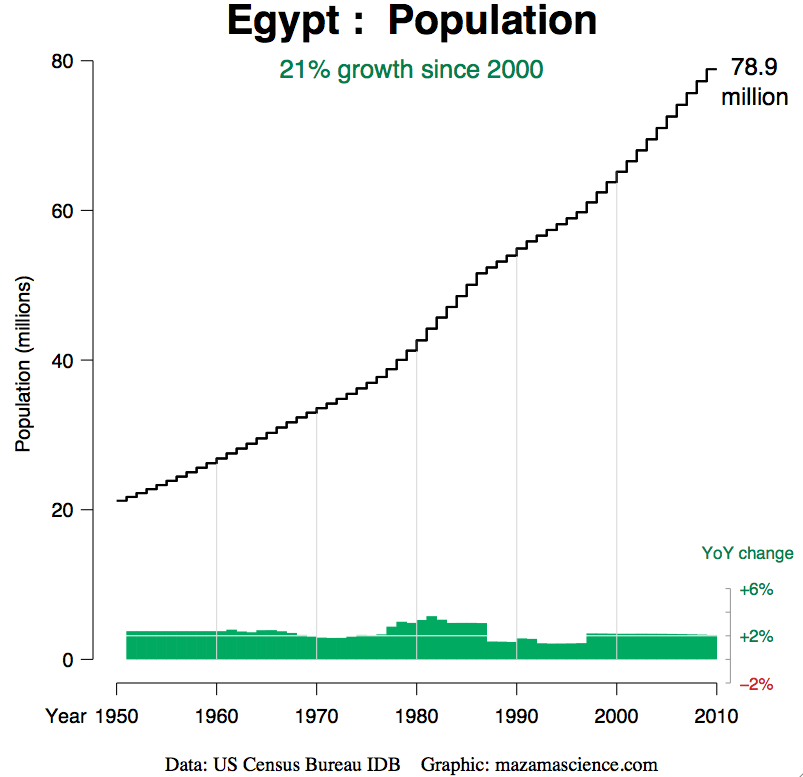

A lot of people like that rive in Egypt....Beats facing reality

(I see PDK saying he was predicting peak oil back in the 1980's..... Yet there are very few who appear to agree with him on this site. Lots of people who vehemently disagree.... So I see no reason why my prediction about the antipathy to the continual growth mantra should remain a minority view point for at least another 30 to 40 years from now)

Good for you, the best gift a parent can give is good genetics imho.

Think I commented earlier that I see reality being forced on us ie no more growth.

Just take some simple stats, crude oil output peaked in 2006, the housing ponzi scheme peaked in 2007. 5 years later oil output is about the same and so is the world's GDP....give or take a little despite strenious efforts that is taking future work/energy and commiting it to day (debt).

Lets take another analogy, Hitler and the Nazi's....I would suggest by 1942-3 the Nazi leaders knew they had lost....the vast majority of german ppl almost certianly not for some time, why then did they keep fighting? The leaders were looking out for number 1. The point I am trying to make is information isnt evenly distributed, those in power (wDE$$ESWD <-- rabbit being noisey! LOL) should be able to see the bigger picture and have access to all the information they want and make rational decisions even at the expense of others and the nation.

So yes the growth mantra will continue until its blindingly obvious we are in decline. The thing to watch is crude oil output...by 2015 or 2018 at the latest we will drop off the output plateau...It will I think be the equiv of the Normandy Landings.....only fanatics think we can win (grow) beyond that point...

With 30 years left, we both get to watch.

Once thats accepted of course then massive changes will happen, 1 I think is no more influx of ppl, whether we start kicking ppl out is another thought...

regards

Egypt

http://gailtheactuary.files.wordpress.com/2011/01/egypt_databrowser_pop…

{kind=link}

you byuild a big dam and the people will come. What next?

http://en.wikipedia.org/wiki/Aswan_Dam

Food crisis

Double rates(property taxes) in Auckland, most people and businesses moved there, they can move away, after all they moved away from somewhere else.

At least homeowners could rest (after eviction) in the fact that they can spell. It is mandatory to pass a spelling test before signing mortgage documents and succumbing to the "trap". Possessive is "their job".

If you think mortgage rates will double in the next 3 years you are seriously deluded.

Secondly, if our house prices fall - most of us couldn't care less.

When we all lose our jobs - then the renters amongst us will be the first one out on the streets. It takes quite a while for mortgage defaults to translate into a forced mortgagee sale. Keeping an emergency fund for hard times is just as relevant (if not more so) for renters who live a precarious existence.

However, your outburst is mildly interesting - if revealing of a certain bitterness in some quarters ...

I agree mortgage rates wont double...more likely to halve....

In terms of house prices falling the problem is "most" thats because the few will go neg quite quickly, say 10~15%...given bank leverage the banks are then technically insolvent....if you think you wont care.....I suggest you are in la la land.

Emergency funds are stored where btw? unless its cash or better gold in a fireproof safe or short term govn bonds....banks shutting their doors wipe you out...

Renters and mortgagee sales, I'd expect that the Govn will legislate to stop these evictions....I think spain is going it now?

If this gets this bad our credit rating is gone, that means massive ie doubling of taxes....and cuts....huge un-employment, shortages.

Quite why you think you wont care in a situation like this is beyond me....

regards

Erm, yeah. Back in the days when we were doing refi's during CA's RE boom our presentation was like reading a children's book, and if they couldn't remember how to spell their own name, I would write it in myself. All I needed was proof they had served, thereby qualifying for the VA loan, underwritten by Uncle Sam. If the market here keeps moving up, I have no reason to believe it will be any different here amongst mortgage brokers and refi guys. The only thing people care about is getting their own piece of the action.

rinse and repeat....

Want to buy a tulip? I have agreat offer for you, get in before the rush...

regards

The answer for first home buyers in Auckland is simple ; build upon the experience of similar folk in other countries ...... here's a couple demonstrating some nifty lateral thinking ....

http://news.uk.msn.com/blog/trending-blogpost.aspx?post=95375004-a9bb-4305-b423-bf7bccdaa8a3

...... if the real estate agent offers you a budget priced fully enclosed unit with special water features and local fauna , be wise to tell him " I smell a rat " ....

Get a home loan from Tesco. 2.39% for the first 2 years, then floating @ 4.24%.

Home owners in NZ are being completely ripped off.

Do we believe the media that "rates are so low"? No actually, given there is a Triple Dip Recession hitting Europe, Uk, USA etc we are paying comparitively very high interest rates....

These rates are being held up high for other parties - not the citizens of NZ.

2.39% 4.24%

http://www.nzherald.co.nz/business/news/article.cfm?c_id=3&objectid=10853204

Boom! It's spreading Auckland wide...

If you are a first time buyer. The solution is to go to Australia get the $10,000 first time buyers grant. Additionally you will be paid more and do less hard work. After 30 years sell your house in Australia and retire in New Zealand, as long as you think the weather is acceptable enough. Problem solved! Other solution is to encourage Australia building companies to NZ to drive down the cost of house building and increase supply. More competition brings better prices for kiwi's . Problem solved ! Other solution is the Dubai solution. Bring in cheap labour from India and phillipines to build houses on government aranged Indian / phillipine builder salaries with free accomodation while they build. ie $5 dollars a day with meals and free accomodation.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.