The housing market looks likely to favour buyers even more strongly this year, with a surge of listings on Trade Me Property and asking prices heading south.

The website had around 39,000 residential listings in January, which was up 17% compared to January last year and the most for the month of January in five years.

"It seems that a lot of vendors have come back from the break and are ready to make a move in 2025, which is great news for buyers, who now have more properties and more choice," Trade Me Property Customer Director Gavin Lloyd said.

The biggest increase in properties for sale was in the Wellington region where listings in January were up 28% compared to January last year, while Canterbury listings were up 23% and Auckland listings were up 17% on a year ago.

However, while the number of properties coming on to the market was up strongly in January, asking prices headed in the opposite direction.

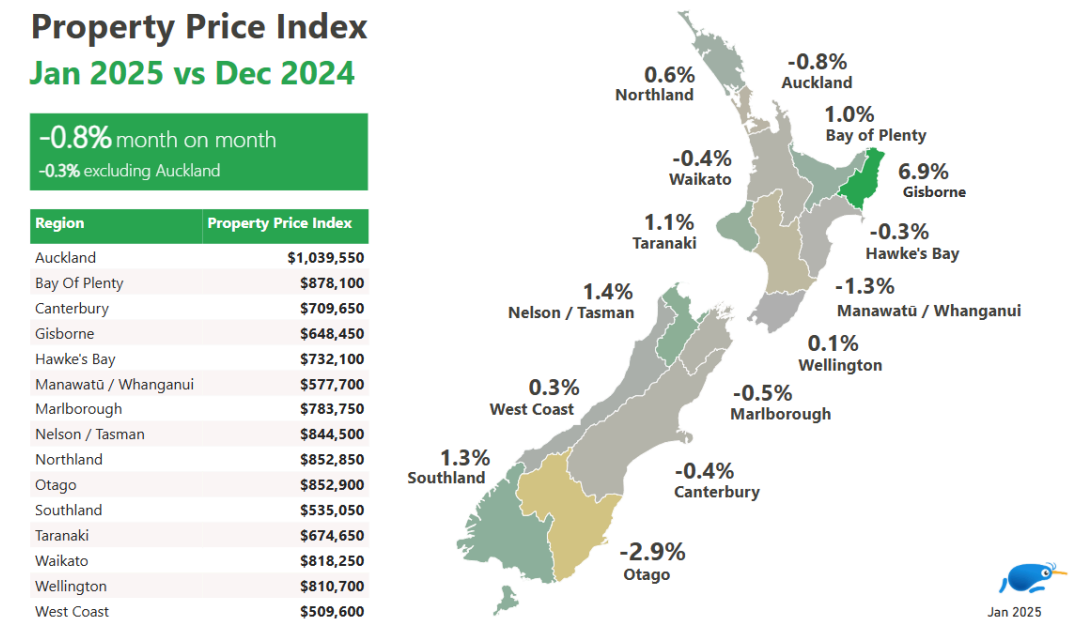

The national average asking price on the website was $842,900 in January, -0.8% compared to December last year.

In Auckland, the average asking price also declined by -0.8% for the month, while the biggest decline in asking prices was in Otago at -2.9% - see the chart below for the full regional figures.

The combination of a surge in stock on to an already oversupplied market and reduced asking prices suggests the market remains very much in buyers' favour heading into the busiest time of year for residential real estate.

The comment stream on this story is now closed.

136 Comments

Just a reminder - asking prices are a leading indicator on sale prices.

Prices to keep falling this year.

🥂 lower prices equals more FHBers qualifying....

Many will ask but how much lower?

The lower bound could well be defined as the point that a rental becomes cash flow positive with the required 30% deposit and that current 2year mortgage rate at that point. Sure some may try to front run the market and may pay more on the basis that they will be able to derive more by developing or subdividing etc etc.

FHBers the investors out there will be using the numbers below, they are your underbidder.

Investor Calcs

if you have an Auckland rental providing $660 a week = 34,320 and rates of lets say 3,000 insurance of 2,000 that gives you 29320

current 2year and 30 year term 5.29 from ASB you can borrow $440k plus the other 30%

you can pay max $628k you have to put in 188k

all sites have unique benefits.. your millage may vary

if rates fall to 4% for 2 year you can borrow 512k plus deposit of 219k

you can pay max $731k you have to put in 219k

on both cases you will have a tax bill, unless you get creative.

Yep! Though there is no rush, at all.

Don't listen to REAs.

That's why the cute little family are hugging.

Just gotta hold together a bit longer living in the landlords overpriced shit box and then we'll buy an even cheaper house.

yeah nah, just a slightly less expensive little shit box....

My 2c worth.

In my observations over the years, in previous cycles we have seen more buyer interest at this stage of the rate cut cycle. Which tells us other macro and socioeconomic factors are having a larger bearing on sentiment.

Intuitively that is plausible, we are exporting buyers and importing renters at a rate of knots unseen at any time. Just imagine how dire things would be without the interest deductibility and capital gains changes.

its the same as the valuation of a startup problem.... while you are making no money the startup could be a unicorn, as soon as you make any the velocity of earnings values your entire startup. The blow off top has no rationale re valuation its 100% FOMO.

- First rentals had positive cashflow and capital gains where icing on top, though it used to be double every 10 years.

- then positive cashflow disappeared but by structuring in an LAQC you could still win on personal tax deductions

- then the ring fenced that tax loss transfer

- then they bought in capital gains taxes

- then they outlawed interest deductability

- there is a pattern here if you cannot pick it up.....

All the while prices went up, now they are so high , how do you realistically price a rental on any known economic valuation method...

You have to go back to yield as capital gains are fairy tales now... its a hell of a long way down.

And buyers are in wait and see mode due tot he huge numbers of listings, perhaps if so many people where not lining up to get out buyers would have more confidence...

The masses entering the IP game late are oblivious to the changing incentives, just following the herd, strengthening conviction as savvy investors as money got cheaper.

Don't hear enough about the ring-fencing change but I believe that to be the tipping point, and the deductibility an encouraging firm nudge for those who didn't get the hint.

But still plenty looking at the historical gains (or espousing them) without consideration of the settings that made IP such an attractive investment in days past.

Deductibility may be back but ring-fencing did the damage and is unlikely to be undone.

Won't investors will be assuming a labour govt will return and bring back reduced interest deductibility?

you can play the argument between FHB and investors, if properties are cash flow positive, investors will come to the market.

i feel there is a balance between investor coming to the market and FHB paying more than an investor would be willing to.

A key takeout for me is that its only at the very bottom of the market that property even presents as possible buy for investors, as you move up into 1-1.5 mil the site either has to have a lot of land or be something unique that represents a development opportunity.

Though there are so many bag holders with these properties now, and no developer activity, and developers are ruthless bastards when making offers. (many bought these at 800k so there is little stress re mortgage payments, but there is also very little action re being able to sell at 1.5), I see clearance for these as a long and drawn out affair, but importantly they can fall a long way and still not be a loss. watercare will not help as developers will not touch until they have clarity

Most of the movement above quartile 1 will be upsizing, downsizing, death and divorce. only 1 of these will result in a bigger mortgage

it would be interesting to know the average number of days on market for each quartile would it not?

With stock levels relatively high and prices relatively low, it's fertile ground for counter-cyclical strategists ......

TTP

A good strategy for catching a falling knife is

A) let is stop moving around once it reaches the floor

B) a stainless steel mesh glove?

Prices are lower, not low. Very different things.

You go first...

Except that prices are not yet relatively low…relative to what? The Covid bubble? Or the post-GFC artificially low interest rates?? We have to look back before GFC to get a sense of what’s long-term normal. At best it’s going to flatline for years

From a Property Investor group forum posted today (the bold emphasis is mine). Note $400 per week is $20,800 per year.

"Seeking feedback. Purchased townhouse in Auckland 2021 (fail, we know). $800k pp, rental income of $600 pw. Tenancy up April. Deciding if we cut our losses (topping up $400pw), possibly could sell for $700k.

1. Tenants want to stay on, so could either fix for 6 months, then sell (betting on market going up)

2. or sell in April taking a massive loss but ability to purchase better.

Help please!"

It's been a while since I've been there, but the general consensus in that group forum is this:

- Put the rent up to $1000 per week.

- Whatever you don't recover, take a note of every bit of minor wear and tear you can think of and claw back their bond.

- Tenants are scumbags.

Whatever you don't recover, take a note of every bit of minor wear and tear you can think of and claw back their bond.

Ah, so that's why our landlord tried that on us (tried to claim wear and tear is deliberate damage that landlords should not be responsible for - and not just ours, but the previous decades!).

We simply said no. We didn't need our bond to pay for the next one, but I feel for those who do. Several months later, the TT agreed with us.

A bit like our Landlord that tried doing us for pre-existing damages. Until we presented them with the pre-tenancy inspection form and date stamped photos.

Was funny seeing the very damages in question when they listed the property using the old listing photos.

I'm under the impression the cost of the loan interest only + rates + insurance should be what is compared to rent, since the principle is going to principle and buying the asset. Please don't confuse this with paying an interest only loan, that's not what i'm referring to.

how does this look when comparing renting vs owning.

Loan = $520K ($650K house w/20% deposit)

Interest payments = $27.5k (5.29%)

Rates = $3k

Insurance = $2k

Total = $31.5k

That's about the same as $600/week in rent.

so owning a $650k house is about the same as paying $600/week in rent. (or a house that yields around 4.8%)

Most seasoned investors are not requiring to put any deposit down, just leveraging.

Buy at under market value and deposit equity is already there from existing property.

Yup, suggests a drop in vendor sentiment and willingness to start to meet the market.

Hopefully the combination of potential unemployment and emigration numbers doesn't result in vendors chasing ghosts and the market down with them.

The question you need to ask yourself is "Are prices falling faster than what I'm paying out each week in rent ?" You need to earn $1000 pre tax a week down here to pay the average rent on a house.

in almost all cases renting is cheaper then paying a mortgages, especially at current settings.

You need to earn $1000 pre tax a week down here to pay the average rent on a house.

I am glad you see how ridiculous the current situation is.

so that's about $1 million on term deposit ?

Yes, and there’s plenty of rentals on the market - an over supply. Negotiate low rent, otherwise move out.

A relief I have from moving from ownership to rent is not worrying about R&M and what the weekend 'chore' will be. I was always conscious of an ageing asset, many seem to ignore this, but I spent a good deal of time staying on top of it.

But the biggest relief by far is only being a spectator to the inevitable house price collapse. Sure I'd be worried on a rising housing market, but in my mind (which is what matters) it's all down hill from here.

Agreed, just replaced a sink mixer in one of our bathrooms, threaded rods holding to the vanity had rusted away. $100 and ~1 hour later it was sorted. 18 months ago we dropped $30k on a new roof, and we're about to spend about the same on a new kitchen.

But I personally don't mind the R&M chores/expenses, as there are so many other plusses/positive attributes in our home that completely outweigh the negatives.

Sure, at a time in life it is satisfying and adds to ones asset. Later in life you tend to get a bit over it - 1 day out of 40 years left of living aint much.....as you get older that 1 day becomes a big hunk of what's left! Enjoy being young.

Its why lifestyle blocks are often run down, the owners run out of ability to either maintain themselves or pay for maintenance.... your LSF IMHO needs a decent cashflow to present as a home and income to the next buyer, either a side business, 2nd minor dwelling (hell $500 per week rent would add about 600k to value at current lunacy) but what ever its worth thats $500 a week could be spend on maintenance etc.

Zwifter, just for a change, try asking yourself some questions.

What sort of questions RP ? Like how to retire at 50 ?

Zwifter, perhaps ask yourself why the online world doesn't seem to take you seriously. If you felt deep down they did, you'd be committed to posting here after 01-March. What's your precious financial advice to others worth?

Glad to help.

the online world doesn't seem to take you seriously. If you felt deep down they did, you'd be committed to posting here after 01-March.

So you're saying you're doing the world a favor by subscribing to interest?

Maybe I'm mistaken, i was under the impression peoples egos relaxed as they age.

Look who shows up when I was replying to Zwifter about not being taken seriously - FUNNY!

Like night follows day, some individuals are hell bent on becoming the entertainment.

I take his comments about as seriously as i take yours.

Aaaand considering i am part of the online world...

Zwifter and I possess two very different ideologies. What do you take seriously - LOL!

Just because an ideology is different doesn't mean it shouldn't be considered.

I can with your massive LOL.. see how seriously you should be taken.

well at least you paid for your opinion to be heard.

Actually RP you are correct, nobody ever took me seriously and in fact most people thought I was a bit of an idiot to be honest despite my qualifications and certificates hanging on the wall, still I'm not too worried about it now, made the right decisions in life when it mattered and definitely got the last laugh.

I only laugh at your love of term deposits , which are just such a low returning investment for anyone with your level of education.

No one I who could be considered financially astute ever mentions them as a prudent financial strategy , they all talk managed funds...

All part of the plan to be honest, just not greedy I have all the money I need and just enjoy my hobbies these days. I stay away from people that all they can talk about is how much money they have made this week, not interested I have other sorts of personal challenges.

sounds like you have life sussed.

The interest can pay the rent, but the real gain is the capital loss for the current owner that is effectively being transferred to new buyers.

Untaxed capital gain on my house fund is how I look at it.

The vast majority of house owners have made a capital gain. Further, homeowners avoid paying rent, while gaining security/stability in their lives.

But the blind follow the blind - like lemmings over a cliff.

TTP

Homeowners with a mortgage still pay rent - it just happens to be they are renting money instead of the house. Stop paying that rent and see how long you keep the house (the action will come, even if it takes longer than the TT).

The security has been given to the bank.

There are none so blind

- Propellor property

- Property apprentice

- Property together

There is no fool like a rich fool chasing tax free capital gains....

Amen to that - feel you might of forgotten one more - Tim the naughty lying Property Broker https://comcom.govt.nz/news-and-media/media-releases/2017/property-brokers-manawatu-and-director-fined-$1.5m-in-price-fixing-case

Homeowners effectively pay a "rent" equal to the interest accrued from their mortgage, plus the opportunity loss of repaying the capital (eg sticking that money into an investment fund), plus other home ownership costs that are covered under rental fees (insurance, rates, maintenance, etc). And usually home ownership costs more than straight renting, the hope is that capital gains is worth the extra cost plus loss in opportunity.

ttp...I've cashed in my cap gain, however my reference was in respect of saver/non homeowners - and in real time, not yesteryear.

The decline in house values is transferred to savers as a tax free cap gain on the buying power of their savings.

It's their turn now.

Greg has tossed another grenade

The article is just stating facts. Can't argue with facts, there is more stock and people are asking less for their homes.

It’s a fact grenade, expect spruikers to dive on it and protect others from the reality (apologies for using the word spruiker).

Tragic end to the housing market.. listings up, asking prices falling, CV's falling, migration falling, job ads falling, rents falling, inflation rising, unemployment rising, list keeps going on..

"End"? Do you know something the rest of us don't know?

. listings up, asking prices falling, CV's falling, migration falling, job ads falling, rents falling, inflation rising, unemployment rising, list keeps going on.

for years people are asking for price falls.

this is what price falls look like.

Too soon to call, too.

Last time hard times came around for property the Reserve Bank spent circa $10 billion of taxpayer money on welfare handouts to property and banking (FLP) in case prices might fall.

MPs are heavily invested in property. What chance we might see more attempts at welfarism for property, beyond borrowing to fund tax cuts for landlords?

You cannot stop the falls, but you can plan to have ambulances at the bottom of the cliff.

Lower FHBer houses are a very good thing. Lower boomer house prices equals lower quality retirements (if they only have this equity for retirement.). You cannot eat the house, though Cam Bagrie will let you lend against it to eat. Equity Withdrawal is going to be a growth business, he has positioned himself very well.

If its only Ranui type shit boxes that get lower, our young people will keep leaving.

Everyone wants housing to be cheaper, just not theirs.

I am OK with all house prices dropping. Including my own.

Not unexpected, economy is jacked & government policy not helping.

Population continues to grow however, with mumerings of relaxation of immigration and foreign 'investment' rules.

More Sushi chefs and Uber drivers, living the Kiwi dream of 15x to a shabby West Auck 3beddy.

Yeah, that will save the mid death rattle, dying Ponzi....not.

Some of those Ranui developments make flat bush look nice.

if owned, how will they ever appreciate in value to let you onto the next rung of the poopertty ladder....

By stating so openly that we need direct foreign investment to save our economy, it should be obvious to all but the most mentally challenged, that housing is not going to supply the credit pulse to save us here.

Act accordingly.

Friends just sold their Kelburn house for 150k more than they thought. Individual situations can be quite healthy.

Think it's a typo, didn't you 'mean' 500k above?

To quote my friend TTP "Long live the humble anecdote".

Is this the stable footing the NZ Housing market is on, that he speaks of?

Is TTP really a convicted fraudster ?

stay tuned, same bat channel....

TTP, have you been playing tennis, or are you taking a break from the courts?

I take notice of anecdotes. Just as I carefully examine Greg's chart.

Especially when they don't say what I wish.

I agree with that UB. Many sellers are still holding out with their prices in the hope an uninformed or desperate buyer will pay up. It happens.

So they "thought" wrong? How much you "think" something is worth is kind of meaningless as it is subjective and dependent upon the experience/competency/ability of the person making the assessment. Was it backed by a property valuation or anything?

Housing is overpriced, reality is finally settling in,

2025 will be the year of big declines, followed by a couple of years of stagnation.. until the balance is equal on both buyers and sellers..

yes this is called clearance then the accumulation phase....

buy this stage of a crash no one wants to ever own an investor property again.

the question is how far down is that clearance

Might need the prophet back again

Anyone have any thoughts on why Gisborne is bucking the trend?

I think it’s like Tauranga, with cashed-up retirees leaving Auckland, leaving a few bagholders behind. The pot has come off the boil.

You would be correct. Its the perfect move for the mortgage free Aucklander who no longer needs to work. You get a far better house for the money with enough left over for a decent size TD and toys.

I would guess that cyclone damage may have created short term demand?

This is my suspicion. Auction clearance at 55% over the weekend with pretty strong prices I thought. Listed rentals have climbed quite a bit over the 5 months I have been monitoring. Sucks as I am an FHB looking in this region and I can't quite tell who is buying.

Where is this 55%?

I watched a RW auction on Saturday, Gisborne

Ah, small town and sample size. Some regional towns still doing OK but for how long?

There isn't one homogenous housing market in New Zealand.You can see from the property price index at the bottom of the article that there are variations in supply and demand, particularly with people wanting to live by the better beaches.

When people can get a mortgage rate between 4-5% then there will be some reasonable price increases in areas like the Bay of Plenty.

Don't forget Riverhead

😂

Is this some kind of in joke?

There was, until recently, a guy here who would never cease harping on about a property he was developing in riverhead and how he wad going to make a lot of money on it, encouraging anyone and everyone to buy into riverhead, borrow a million and make a fortune. His choices aren't ageing well currently, possibly why he isn't posting here any longer.

I believe he was banned from posting, rather than he chose to stop posting.

There used to be a poster on here who was doing property dev in Riverhead, no matter what happened he would post how good things where are in Riverhead.

Most of these guys who Spruik a single suburb, but never comment on other topics should be ignored...

Is the ChChc promoter next?

The truth of the matter is that I promote ChCh because it is the best city in NZ for property investment and lifestyle.

The people going on about prices dropping or going to drop has been going on here for the last decade.

I do not deal in the North Island property market but it has seemed to be overpriced and not good value for a long time

The ChCh market is where the successful property investors operate.

Christchurch is set to take off, affordable accomodation , IT businesses expanding , manufacturing expanding, look at Hamilton Jet. Not only is Christchurch holding its own , but the holiday home market of Akaroa and Kaikoura keeps trundling along behind. Wolfbrook have just built a block in Kaikoura. Biluders still busy in Christchurch

There kind of is though. You’ll see ebbs in random markets, but property crashes tend to take down all regions

People need to keep things in perspective. Five years ago there were more houses listed on TradeMe than there are today. A drop of 0.8% in asking price is miniscule.

Perspective? Alright, here’s some. House prices in New Zealand shot up over 40% during COVID, then dropped about 19% from the 2021 peak. A 0.8% dip might not sound like much, but it’s movement in the right direction. For years, first-home buyers have been priced out while investors raked in the profits. If prices keep softening, maybe - just maybe -housing can become something people live in again, not just an asset class for the wealthy.

The world of the 20 something FHB looks very different now.

- unstable unemployment ( government employees need to be very worried)

- unstable global world order.

- AI, climate change, wars and so on driven unexpected changes

House prices, job security, rents, inflation, world event and incomes need to be stable to motivate young people to buy houses. All are messy. Safer to rent and keep savings in the bank for unexpected events (redundancy or a move overseas)

Investors are unlikely to expand housing portfolios vs diversifying. Especially those individuals/boomers now approaching retirement. Better to hedge now.

Expect rents and house prices to continue to fall for a few years yet. Sound investment is in areas to be positively impacted by AI, climate and military tech.

" If prices keep softening, maybe - just maybe -housing can become something people live in again"

For owner occupier buyers to be aware of:

Former prime minister Sir Bill English is optimistic that New Zealand’s house prices are going to trend downwards, in real terms at least.

“Our housing is too expensive,” English told delegates to the INFINZ (Institute of Finance Professionals New Zealand Inc) conference at Auckland’s Cordis Hotel on Monday.

“If we successfully deal with housing affordability, your house prices are not going to go up for the next 15 years, much.”

https://www.waikatotimes.co.nz/business/350451961/get-used-it-sir-bill-…

An real life example of first home buyers in Wellington who bought at the peak. They're in negative equity (i.e loss of over 100% of their equity deposit, which could be their entire life time of savings). Bolded words are my highlights for emphasis.

"I met a couple recently who bought their first home in Wellington at the end of 2021 and are now feeling – quite frankly - scared.

She works in the public sector, and he’s in the construction industry. The headlines suggest their local council rates will soon go up, despite the valuation of their home having fallen 25% (or more).

Their hard-fought deposit, which they scraped together using their KiwiSaver and years of savings, was 20% of that 2021 purchase price – so on paper that entire deposit has been wiped out. If they sold at today’s valuation, they would have no savings and still owe money to the bank.

She has so far survived two rounds of redundancies – but they’re scared about what the future holds. Didn’t they do everything right? They played by the apparent rules of the game – work hard, save hard, buy a house. That’s the conveyor belt to security that society sold them. Instead, they feel like they have been financially punched in the face."

https://www.stuff.co.nz/business/360582273/katie-wesney-ready-anything-…

Owner occupier buyers: CAVEAT EMPTOR

The exact situation there were a few commentators on here warning about around the time of their purchase - to which we were abused as doom gloom merchants by those who benefit from ever rising house prices.

"The exact situation there were a few commentators on here warning about around the time of their purchase"

Exactly.

"- to which we were abused as doom gloom merchants by those who benefit from ever rising house prices. "

These were attempts to discredit people like you (who were warning the general public about elevated house price risks) by those with their undisclosed vested selfish financial interests.

After all, those with the vested interests need to put food on their table and pay for their accommodation costs (most likely a mortgage).

This guy might have been very disappointed at the time of being refused a sufficiently large mortgage to purchase a residential real estate dwelling, but being rejected from the bank was actually a blessing in disguise. Being rejected was better than getting approved to overpay for a house, be stuck in negative equity (and a loss of his entire life time of savings) in 2025. He can be a buyer today with a lower mortgage.

https://www.newshub.co.nz/home/money/2021/11/first-home-buyer-not-very-…

My exact situation..

"My exact situation.."

You are Kyle Welch?

incorrect

What did monthly sales look like 5 years ago, compared with today ?

as buyers are learning, asking is not a hard price, its an opening gambit

A drop of 0.8% in asking price is miniscule.

Over a month? Not at all.

Though prices in Auckland's city fringe suburbs seems to be holding up. Anyone got any insights into movements around town? Downsizers from mission bay moving to grey lynn?

Or say from high maintenance Remuera older homes to Stonefields low maintenance.

Vendors keep seeing a few decent sales figures so are holding out. but there are not enough buyers for them all..

Its musical chairs, which is fun with 5 year olds, but may cause hip problems with 80 year olds.

Yeah. Def a few substantive sales in Grey Lynn/Ponsonby being used as marketing tools.

Tools being the operative word

Auckland is huge, people are contantly trying move to a 'better' location.

Listings up, sales down, spec town needing real equity for DTI requirements - all equals ....down down down in ponzi town.

Erica is the Minister of Immigration and Education. The gold plating (TBA) on the visa will be the ability for your children to study as domestic students in our tertiary institutes. Scrape together 5 mil to put in a managed fund (you get the money back in 3 years + interest) The right to buy a nice house (TBA) for the wife and kids to live in while you carry on doing whatever you do wherever you do it. Meanwhile, your kids can study for an internationally recognised/transportable professional degree sponsored by the New Zealand taxpayer.

This is a thinly veiled scam to inject liquidity into the property market. We have seen this movie before, and the ending was a bit stink. Australia ended screenings. It turns out the ticket price doesn't cover the cost of putting on the show.

You will not even need to scape together, as long as you have security the big 4 banks will lend you the 5 mil.... play the game son.

Wow. So Erica Stanford is going to effectively make working Kiwi taxpayers pay for foreign buyers to come in and purchase property, to help property values?

Really feels like smarmy scamming of the younger generations.

I have been looking in the Wellington region and noticing a clear trend of auctions/deadline sales failing and then moving to enquiries over $X, followed by price drops later on. Open homes seem busy but are not translating into sales. Anecdotally, I am hearing people unable to fill rooms in flats when trying to leave other regions or go overseas for other job opportunities, sometimes having to wait until the lease ends. Students flats also being harder to fill, especially ones with 6+ rooms. It seems like the Wellington market is circling the drain. Anyone else with observations who monitor this area?

It has been the same since the downturn started and people stopped buying in aggregate. Tenders, auctions died for a long time, offers over, delist then relist under different title, followed by price by negotiation, followed by delist and relist again 6months later. It is a cycle - the key is to track how many times places get listed, any price changes and then you can offer accordingly, knowing the pace you may want has been relisted a couple times under a couple of agents for over 6 months and the vendors are therefore more likely to be starting to consider reality.

The five stages of grief

- Denial: A defense mechanism that helps people protect themselves from shock. People may refuse to accept the reality of the loss.

- Anger: People face the pain of their loss as reality sets in.

- Bargaining: People dwell on what they could've done to prevent the loss.

- Depression: People face the inevitability of the loss and may feel intense sadness and despair.

- Acceptance: People come to terms with the loss.

we are not yet in Anger, when it comes , and its starting too, Luxy is going to cop it

Had my youngest got to Aus a year ago. She reckons there are very few of her crowd left in NZ.

Apart form job opportunity and lifestyle, one thing she doesn't miss is the requirement to engage in pagan worship at morning start-up.

Question for all Australians, why is the welcome to country in English?

I cannot imagine NZ Iwi lowering themselves to this here?

what exactly are you referring to?

the requirement to engage in pagan worship at morning start-up

Where have you been?

are talking about prayer?

If so i don't know where she was working that required prayer at start up. i've never experienced that in my whole life in NZ.

I find it extraordinary that you haven't. Another family member says her staff are bordering on a work to rule. New management is having half and hour wasted very morning as they 'pray' to an imaginary friend. This is in health. But its prolific in all public services. Seen DOC release a bird lately or open a walk? New road...you name it. And all on your dime old chap...it's not done for free.

I'm sure it exists, relatively minor and not a concern of mine by any means.

Jesus wept. We still have prayers in parliament too.

Even Karakia has elements of a Christian prayer.

Pauline Christianity?

Yeah, I’ve been seeing the same pattern in a few other regions too. Feels like a waiting game—buyers holding off, and sellers adjusting slowly. I came across this breakdown of what’s happening in different markets, thought it was a solid overview: https://www.opespartners.co.nz/property-markets. Be interesting to see if things shift again later in the year.

Just one more cut bro. I promise bro, it’s going to turn around. Hold in there. Don’t list.

Take it easy bro, which part of your body are you trying to cut?

And so it begins...

https://www.nzherald.co.nz/nz/kumeu-flooding-crisis-leaders-push-for-to…

All foreshadowed first in the USA. Extreme weather events, Insurance increases, denial and attempt to rebuild, finally acceptance. But remember climate change is definitely a hoax.

I wonder how his piece of dirt will revalue once they abandon the local township.

A stampede of buyers who don't believe in climate change will descend like vultures and make a killing, maybe?

Before we left NZ, we were [quite seriously] talking to an RE about a flooding swamp to put a houseboat on.

In hindsight, ablutions might've been a problem though, no one wants a flooded septic tank.

We determined the asking price to be 3x what we thought it was worth, so left it alone.

Can apply this framework provided (courtesy of IT Guy), to those affected property owners.

The five stages of grief:

1) Denial: A defense mechanism that helps people protect themselves from shock. People may refuse to accept the reality of the loss.

2) Anger: People face the pain of their loss as reality sets in.

3) Bargaining: People dwell on what they could've done to prevent the loss.

4) Depression: People face the inevitability of the loss and may feel intense sadness and despair.

5) Acceptance: People come to terms with the loss

Natural disaster forces owner to sell dwelling and accept price offered by local government. The only buyer of the dwelling is local government.

Local government buys damaged house in flood zone from residential dwelling owner and the amount paid is below the outstanding mortgage amount. Forced into negative equity due to natural disaster and price offered by only buyer.

Refer 3:09 of the audio

https://www.rnz.co.nz/national/programmes/morningreport/audio/201897224…

I've thoroughly enjoyed reading this article comment sesh, but have now stayed up well beyond bedtime

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.