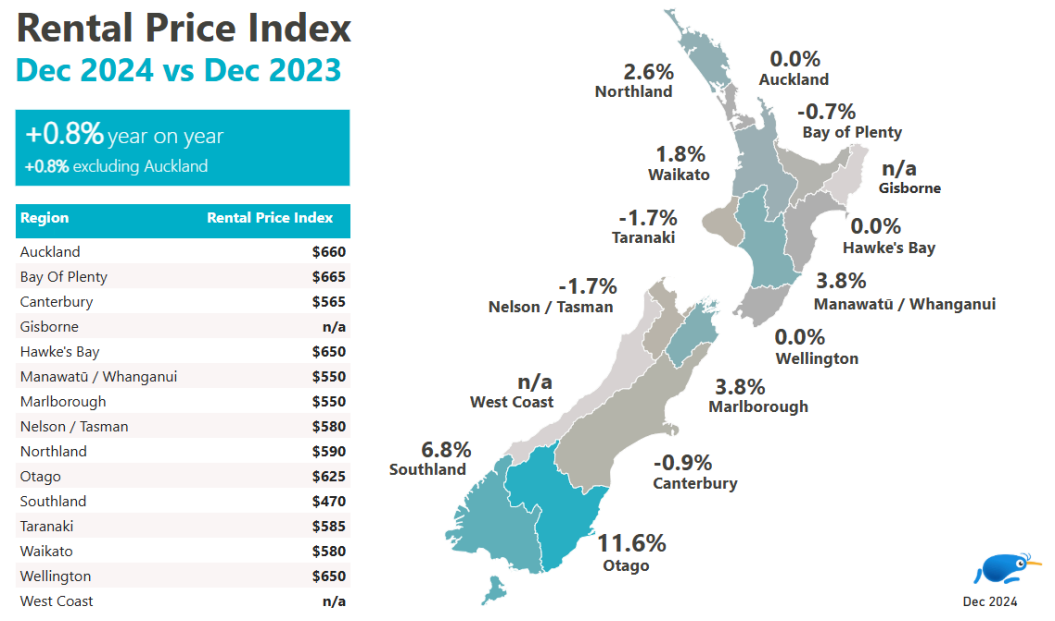

Landlords will have little to cheer about in the latest residential rental figures from Trade Me Property.

The median asking rent for Auckland properties advertised on the website declined 1.5% in December from November, and was unchanged from a year ago. This suggests a lack of rental growth in the country's largest rental market.

The situation was even worse in the Bay of Plenty, another very popular rental market, where the median advertised rent also declined 1.5% in December and was 0.7% lower than in December 2023.

On an annual basis rents were also weaker in Canterbury -0.9%, Nelson/Tasman -1.7% and Taranaki -1.7%, while advertised rents were unchanged from a year ago in Wellington and Hawke's Bay.

Increases in advertised rents were largely confined to the provinces, with Otago posting the biggest monthly increase of 4.2% in December.

However, the sharp rise in Otago's asking rents should not be a surprise. The region's rental figures are dominated by the student market over the summer months as thousands of students return to Dunedin and sort out their accommodation for the coming year.

Because many student flats are larger properties that can accommodate bigger groups of flatmates, this tends to push up Otago's median rent at the end/beginning of each year.

So it will likely be a couple of months before a clearer picture emerges of the rental trends in Otago as the market settles back down to normal rental activity.

The comment stream on this story is now closed.

132 Comments

So the rental market is completely saturated with properties and the rents are now starting to fall.

So lets evaluate - if you are investor and buy a property at current prices in one of the main centres you are:

- Struggling to rent out your home

- Once you rent it out, topping up up the rent to pay the mortgage, often substantially so

- While the value of your property is likely dropping, particularly so when you consider inflation and opportunity cost.

- While rates, insurance and other maintanence costs are at historical highs and still increasing considerably every year

Yikes.

not a good time to buy an investment. good time for a FHB.

Why would a logical FHB think its a good time to buy? Taking into account what I listed above and adding the state of the economy, low net migration and an interest rate cycle that is almost at its bottom, do you think house prices are to suddenly increase for some particularly mysterious reason?

many people struggled to get anywhere near close to buying a home over the last 10 years. now is a time where there are a good amount of affordable properties are on the market without investors to compete with them.

being bottom on the interest rate cycle means it is a good time, FHB aren't overly concerned in house prices increasing in the next 2-3 years.

- Struggling to rent out your home doesn't apply to FHB

- Once you rent it out, topping up up the rent to pay the mortgage, often substantially so Also Doesn't apply to FHB

- While the value of your property is likely dropping, particularly so when you consider inflation and opportunity cost. prices have already dropped and are plateauing, hence why its a good time.

- While rates, insurance and other maintanence costs are at historical highs and still increasing considerably every rates insurance and maintenance will never, if not very unlikely to come down so this will always be a cost.

for someone looking for a home, and can afford it with good financial reasoning, now there is plenty to chose from.

Denial, anger, bargaining, depression and acceptance. We are at bargaining.

thoughtless comment.

Nah, well known stages of denial.

Cycle of Acceptance - Tool/Concept/Definition

I'm not so sure we have even reached bargaining stage myself.

he changed his comment, the original said "wow".

It's true, I was in utter disbelief and left speechless by your previous comments.

Its hard to believe reality when you are delusional.

Developers are at bankruptcy stage , falling over see

https://www.nzherald.co.nz/business/developer-of-multi-million-dollar-o…

Recent Investors are mainly denial or at least mental bargaining (you do not make a loss until you sell BullSh&^)

Long term investors are at ( I am ok I bought a long time ago, and this is valid) but I am not willing to add until the market starts rising

This is smart (NEVER ADD TO A LOSING POSITION)

Rookie should not even be commenting as his approach is to buy yesterday and never sell.

All professional traders know the adage When in trouble double

we have all seen these guys carried out of the room as well,

Make know mistake leveraged investment is trading.

Rookie should not even be commenting as his approach is to buy yesterday and never sell.

so you're not a fan of buy and hold?

never the less, anyone is entitled to comment, most commenters here are just copying what a few others say. reading the same narrative is boring.

discussion and argument provide contrast to contemplate.

You be a more experienced investor and had more properties. But I can't help but feel you might be out of touch with the younger generation of FHB and their situation.

Developers are at bankruptcy stage , falling over see

https://www.nzherald.co.nz/business/developer-of-multi-million-dollar-o…

Development project is loss making as they sold pre-COVID at fixed prices and got squeezed due to rising construction costs.

Inland Revenue owed $2.3mn - likely to be GST on the sales proceeds

"Ngaiwi Developments owes Inland Revenue $2.3m, NZ Mortgages and Securities $793,000, Edenbay Properties $270,000 and unsecured trade creditors $479,000, the report said.

Total debts are yet to be quantified but the only assets are $25,000 cash in the bank, according to Tony Maginness and Jared Booth.

Stewart had the liquidators appointed when various factors combined to mean his company could not continue."

Inland Revenue chasing more cases of unpaid outstanding taxes.

Inland Revenue is fulfilling its promise to go “full throttle” on compliance work after last year’s Budget boost, with applications made already this month to liquidate companies for unpaid tax

The Gazette showed that on January 10 and 13, IRD applied to High Courts to liquidate many companies.

The first six companies on this list are associated with Gulati Group of East Tamaki and directors Onil Kumar Gulati and Penoy Gulati.

IRD has this month applied to liquidate these companies and others:

- Gulati Holdings, a commercial property investment business incorporated in 2021;

- Onilco Petroleum trading as Mobil Kumeu, a service station company incorporated in 2020;

- Vienna Hotels, a hotel company incorporated in 2021;

- Vish Energy, a service station operation incorporated in 2022;

- PP Energy trading as Mobil Morrinsville, incorporated in 2012;

- PP Fuel trading as Mobil Frankton, the service station business incorporated in 2020;

- Jondee, an Invercargill customs agency and broking service incorporated in 2015;

- E10, a real estate agency service company incorporated in 2021;

- Applejacks 2019, a restaurant operation incorporated in 2019;

- N S Wholesale, a vehicle business incorporated in 2009;

- J & P Drainage Contractors of Massey, incorporated in 2007;

- Handystacks, a firewood cutting and retailing company incorporated in 2015;

- Kitchen Story, a furniture manufacturing business of Hobsonville, incorporated in 2018;

- Smiles Roofing, a Titirangi business which does guttering installation and roof repairs.

https://www.nzherald.co.nz/business/inland-revenue-going-full-throttle-…

Interesting to see another real estate agency in the list - E10

Contagion lift off countdown on.

Interesting.

Good to see some more coverage of companies' owners dodging millions of what they owe to the government/other taxpayers, in addition to all the coverage of "such and such got overpaid Working for Families and now owes $20k".

Interesting the percentage that were incorporated 2020 onwards

Whether people could buy or not, many don’t care at this point and have lost interest when they see each month getting better.

Why pay what are still majorly overinflated prices when it will be cheaper tomorrow?

I’m not sure people these days are so cavalier about just signing up for extreme leverage on a dog box when they could have something nicer if they leave the market to fall over and pick up the pieces later…

For those watching their share/fund investments going up, I imagine drawing it out for the privilege of paying interest the bank is looking less and less attractive

i think you're better off looking at market cycles, we are at (or very close to) recovery.

We've been hearing that since August 2022.

So when is it actually coming again?

good question, there are a lot of crystal ball holders here.

But if you are in your 30's (even late 30's for the average FHB) are you gonna sit around waiting for 5 years for something that might not happen. or act when the situation fits your needs?

For someone in their 30s, it might make more sense to continue investing their deposit in higher-yielding investments rather than tying it up in NZ property with debt servicing costs. With house prices stagnant their deposit is likely growing faster elsewhere, while they can benefit from renting a larger, better quality home for less than the cost of owning.

Meanwhile they can see property listings sit, get added to, or return to the market in tandem with rental listings increasing and rent asking prices declining. All while the NZ economy continues to struggle and the NZD weakens. The case for waiting becomes even stronger.

Have you calculated the opportunity cost incurred when you rushed into purchasing your first home as soon as your deposit was ready, instead of leaving it in the stock market or another investment?

hey look, im not going to deny that if i invested my deposit in the SNP500 and waited 1 year ish (to date) and waiting till the very end of the buyers market, even you can even figure out when that is going to be. i might have an extra 20K for a deposit (if i was lucky). who knows what happens to the SNP500 anyway? there's always a risk

But no one is perfect and its unreasonable to criticize someone for making a decision inside there financial means and fits their needs., also i have been looking and for me to get something i would be interested in now would cost an extra 40-50K. so really its hard to say if it would have been better to wait at this point.

i wouldn't say 3-5 years is rushing either.

The other elephant in the room here is at the time of writing you account for 26 of the 80 comments on this article. 33% off the total comments.

You’re constantly on every property article trying to convince people:

- Now is the right time to buy

- Why wait to buy?

- The recovery is here (or it’s close)

- We’ve reached the bottom, all up from here

Can you please help us understand, if you are happily now in your first home, why do you feel the need to spam the property article comments section every single day?

i love a good argument. intellectually stimulating. especially with people who are constantly negative on the NZ economy.

i like to provide an alternative view as it stimulates ideas.

i'm also up for mortgage renewal soon so i've been keeping up with what's happening in that area.

- We’ve reached the bottom, all up from here

not all up from here, more so the crash is over.

Cognitive dissonance.

many people struggled to get anywhere near close to buying a home over the last 10 years. now is a time where there are a good amount of affordable properties are on the market without investors to compete with them.

Who is to say there won't be more properties on the market at more affordable prices 6 or 12 months from now? Again, what is driving this miraculous recovery?

being bottom on the interest rate cycle means it is a good time, FHB aren't overly concerned in house prices increasing in the next 2-3 years.

Yeah but they should be concerned about prices dropping further if they have learned anything from the 2021 fiasco, you clearly have not.

Struggling to rent out your home doesn't apply to FHB What makes the prices stop dropping?

- Once you rent it out, topping up up the rent to pay the mortgage, often substantially so Also Doesn't apply to FHB - What makes the prices stop dropping?

- While the value of your property is likely dropping, particularly so when you consider inflation and opportunity cost. prices have already dropped and are plateauing, hence why its a good time. What makes the prices stop dropping?

- While rates, insurance and other maintanence costs are at historical highs and still increasing considerably every rates insurance and maintenance will never, if not very unlikely to come down so this will always be a cost. What makes the prices stop dropping?

Yeah but they should be concerned about prices dropping further if they have learned anything from the 2021 fiasco, you clearly have not.

now you're just speculating....

Who is to say there won't be more properties on the market at more affordable prices 6 or 12 months from now? Again, what is driving this miraculous recovery?

Who is to say there wont be less?

And you are not speculating?

about what?

You're embarrassing yourself again.

Its his thing.

that's your only contribution?

Rookie do you have a successful pattern of past trading experience in any market that you could perhaps share?

Stocks, bonds, FX , options, property?

stocks, and crypto, mainly stocks.

Some stocks i owned was VOO, INTC, CE, MMM, XOM, FBU (guess which one i lost on :D), LNZA.

overall did pretty good, double my money on a rather small investment 20K ish.

had some decent losses too.

i sold my stocks and crypto so i had a 20% deposit to buy a property than i had been trying for 5+ years to be able to do and the time was right for me.

now after 1 year i have saved 6 months of income as an emergency fund i will start investing back in to stocks and crypto again.

One of the biggest reasons i wanted a property is i had been thrown around 5 different rentals in a year i was sick of it, very happy so far.

i'll tell you this for sure, i have learnt a whole lot during the process of everything, about finance, law, contracts, maintenance on property, tax, tenancy, managed funds and ETFs.

So really the elephant in the room is that you bought a property and you couldn't handle it if it went down another 10 or 20%?

i was looking forward to a response from someone who adds value, grow up.

Take a hint from the distribution of upvotes about where in the value chain you sit

i have no problem having a different opinion than others, rather than following the herd like a sheep.

Shouldnt that be flock instead of herd...?🤔

(Edit...no I'm wrong. https://savvyfarmlife.com/what-do-you-call-a-group-of-sheep/ always thought it was just flock for sheep. Learn something new everyday...)

Respect for not editing the original post

I feel for the younger people who entered the market during 2020-23. It’s gonna be tough to talk this market up with all the headwinds Toye pointed out.

why do you feel for them? there's less investors for them to compete with.

Now I'm starting to think you are a troll

what are you're investments? why are you so interested in the housing market?

DW i don't expect to get an honest reply to this.

I don't like to dox myself on the internet but I don't pay rent nor do I have a mortgage so you can draw a picture from that.

In other words you have no grounds to stand on, living at home with the rents?

Really "on point" with your conclusions just like the rest of what you've put up today.

if you need any advice on how to save and invest so you can move out of home, i'm happy to give some advice.

Give us a rest. $20k spread among a number of investments including FBU does not make you capable of giving sound financial advice. I have been investing in equities for 40 years and retired at 58 but I am still careful about who I talk to about investing.

yep, absolutely agree. I'm not giving financial advice, just discussing different opinions.

I would not take financial advice from anyone here, that would be irresponsible.

You said you were happy to give some advice about investing. That is a very clear statement from you. You cannot walk back from it. I can see English is not your first language. Maybe you should be more careful next time.

i can give some advice, consistent contribution in to a well diversified managed fund or etf, would be a good start?

You said you were not giving advice now you are giving it. Make up your mind. You are on here a lot. Should you not be working. Or rather working honestly for an employer rather than blogging.

I don’t think he’s a troll. I think he’s just a young person who bought into the hype. 2020-2021 was peak fear and peak hysteria. At my workplace, I saw young people in their twenties buying townhouses at their limits.

wrong! like many of your other opinions.

Rookieinvestor google Dunning Kruger effect.

If it doesn't resonate then you are no hope.

If it doesn't resonate then you are no hope

That is your opinion, thank you for sharing ;)

Lordy, when you're in a hole ...

I think the quote was "No, no, Dig up stupid!"

But they already bought…. At peak Values

oh well, yea i do feel for the ones who bought at the peak.

more accurate to say 2021-2022 though, prices are still up from 2020 and 2023 was after the crash

sorry IT GUY,

i was actually looking forward to a response from you on this but the cannon fodder got in the way.

post question below so many posts I lost context

by IT GUY | 24th Jan 25, 12:13pm

Rookie do you have a successful pattern of past trading experience in any market that you could perhaps share?

Stocks, bonds, FX , options, property?

by RookieInvestor | 24th Jan 25, 1:30pm

stocks, and crypto, mainly stocks.

Some stocks i owned was VOO, INTC, CE, MMM, XOM, FBU (guess which one i lost on :D), LNZA.

overall did pretty good, double my money on a rather small investment 20K ish.

had some decent losses too.

i sold my stocks and crypto so i had a 20% deposit to buy a property than i had been trying for 5+ years to be able to do and the time was right for me.

now after 1 year i have saved 6 months of income as an emergency fund i will start investing back in to stocks and crypto again.

One of the biggest reasons i wanted a property is i had been thrown around 5 different rentals in a year i was sick of it, very happy so far.

i'll tell you this for sure, i have learnt a whole lot during the process of everything, about finance, law, contracts, maintenance on property, tax, tenancy, managed funds and ETFs.

so you have dabbled , did you use leverage or CFD?

Did you have a trading system or gut feel, did you use tech analysis or fundamental or just gut?

I have the advantage of sitting on DB, CitiGroup, Koch oil trading floor, Solomon smith barney etc for over 25 years....

Good luck to you IMHO you are misreading the signs I do not think its the bottom here, it may be wrong but I trade knees to shoulders on the lift, I got out right at the top its more important... the valleys at bottom always test my patience.

I also do not see much gains to be had from current prices, I am more interested in bigger cycle and Gold, BTC here, suggest you get a trial Saxo acc to look at the other options apart from property, these guys will give you 20 to 1 leverage (more then a mortgage)

Trading is a skill that IMHO is very hard to learn

you buy and hold is not an acceptable risk management strategy but I will you luck, our paths mat cross but not at these price levels.

I have the advantage of sitting on DB, CitiGroup, Koch oil trading floor, Solomon smith barney etc for over 25 years....

A quick search, doesn't seem like those stock have done very well? am i wrong?

the valleys at bottom always test my patience.

Did you have a trading system or gut feel

i researched how to read a balance sheet, i learnt about Discounted cashflow analysis, i researched what other people were saying about the stock, i had some industry info about celenease stock and saw a good business and double my investing, and i gambled on others.

this is an interesting topic, i was just having this discussion, how long can you sit on the bottom for? i supposed i depends how much you understand what you invested in.

I also do not see much gains to be had from current prices, I am more interested in bigger cycle and Gold, BTC here

fair i dont expect huge gains in 2 years, although i think we are at the bottom or near it, i think the economy is on the brink of a recovery, my property is based of somewhere to call my own and an asset i can borrow against or get cash flow from in the future, i like BTC and will be investing in it shortly, and have always like gold (personally i think silver has more utility , but let price do the talking).

Good luck to you IMHO you are misreading the signs I do not think its the bottom here

fair, ill take that in to consideration with my decisions.

im not interested in trading, im interested in DCA, long term investing and value investing.

What don't you like about Buy and Hold? worked well for most investments, the return you make just might not be as good as another investment.

"suggest you get a trial Saxo acc to look at the other options apart from property, these guys will give you 20 to 1 leverage"

CAVEAT EMPTOR: EXPERTS ONLY

20:1 leverage is definitely not for inexperienced novice buy and hold investors - people have lost more than their entire net worth very quickly using this amount of leverage in financial markets.

definitely not interested in leveraging to buy stocks. at this stage.

ahh saxo is a trading platform, not my kind of investing

Guns don't kill people, people with guns kill people.

leverage is the same.

People playing with Saxo who do not know what they are doing is like a clown playing with matches in a fireworks factory.

Same could be said of people who think property can only go up, even from here.

I'm interested to understand why you consider paying double in home ownership costs (could be more, could be less but will almost certainly be considerably more than rent) than rent for a below average home is affordable? I'm not sure all or even most FHB understand that the money they pay on their mortgage is mostly interest and very little goes to paying off the principal in the early years. As far as I can tell FHB often seem to overpay to get their offer accepted; then are on interest loading as they are under 80% LVR. So, the huge costs of home ownership compared to renting may not be building up equity & have possibly lost equity. I am fast forming the opinion that the current interest by FHB may not be sustainable.

Those FHB I have known over the years sure didn't understand table mortgages. Had an interesting conversation with 2 a while ago:

The first, after ~8 years of holding had paid off ~9% of principle.The second, after 5 years had paid off .. well, would have been 2% if they hadn't extended their mortgage by buying toys using the increasing paper equity.

Also have FHB friends who are in deep doo-doo, after we watched them desperately try to buy anything and everything as prices rose and interest rates dropped.

Meanwhile, we lived in decent rentals that cost us 40% of what our landlord's mortgage repayments would have been, and didn't have to worry about rates, insurance or maintenance bills.

We're now approaching a point in life where buying, even if more expensive than renting, might almost be the better decision (to insulate us from our landlord's exposure, and allow our children freedom to redesign as they please) - but we won't be doing it in NZ.

The recent/current FHB interest is solely driven by the 211,000 people who suddenly got permanent residency visas and therefore qualified to buy a house, funded by taxpayer grants and Kainga Ora loans.

absolute bollocks, this is so incorrect.

I have an acquaintance, a FHB, who recently bought a two bed, new build townhouse. Better than average, ok design, one off street carpark. The developer was getting a bit desperate to offload, and my acquaintance got it for what I thought is a pretty sharp price ( 15% below advertised price, 7-8%below what I consider a reasonable price)

The guy is getting a reasonable 6 month mortgage rate, and got a decent cashback

That’s why in my opinion there are potentially good opportunities for FHBs right now

I don’t think FHBs need to panic, but at the same time some of these opportunities may not be around in 12-18 months

but this is just my view!

that's how i see it.

https://www.oneroof.co.nz/news/first-home-loan-scheme-is-open-to-abuse-…

Brokers tell OneRoof that most of the applicants are new arrivals to New Zealand.

Loan Market mortgage adviser Dave Williams agrees that the First Home Loan scheme is a “no-brainer” for first-home buyers, noting that it opened up home-ownership to people who would otherwise struggle to save a 20% deposit on a house worth $750,000 to $800,000.

However, more than half of the clients he’s working with are on residency visas and he does not know why more citizens aren’t accessing the scheme.

Kiwi Mortgages mortgage adviser Jatinder Singh has also seen an uptick in new residents accessing the First Home Loan. “Most of the new residents who recently got their residency are actually buying a lot of houses,” he said.

“I don’t say that no one [citizens] is buying, yes there are a few, but if you are talking about the ratio then yes the ratio for resident visas are buying more first homes than the citizens.”

Harcourts Mount Roskill business owner Nick Kochhar says that of the first-home buyers active in his area, more than 60% would be new residents with First Home Loan approvals.

The recent/current FHB interest is solely driven by the 211,000 people who suddenly got permanent residency visas and therefore qualified to buy a house

more than 60% would be new residents hardly solely

he does not know why more citizens aren’t accessing the scheme

Because it had ridiculous requirements. Particularly the income limits.

It was [not] joyous being told we would have to front up 4x the deposit of someone earning half our income, purely because I'd worked hard to get a good salary. But please, keep paying your landlord's mortgage meanwhile - they can't afford it.

It's a ridiculous scheme anyway. Why is the taxpayer providing welfare subsidies to benefit property speculators via higher prices being paid?

"Brokers tell OneRoof that most of the applicants are new arrivals to New Zealand.

“I don’t say that no one [citizens] is buying, yes there are a few, but if you are talking about the ratio then yes the ratio for resident visas are buying more first homes than the citizens.”

Is this still the case currently? The date of the article was Aug 2023 - so 15 months ago - unsure if this is still happening currently.

If rents are dropping and investors (in this case speculators) are topping up then the price is higher than present value of estimated future cash flows which would indicate likely more downward pressure on prices unless some sudden boost in credit lending into the market.

I generally agree. Subject to caveats and assumptions such as job security etc

Why would a FHB want to take on all those costs, when they can rent for about half the cost? All whilst saving the difference, and investing it in the stock market where they can get 7-10% total returns on low risk investments. At some point in the future, they can then sell their stocks and buy a house with 100% cash like I did.

You mean rent instead and invest your savings into the overpriced stock market that many consider to be a humongous bubble at current prices? Yea, that's also an option. Problem is that if the stock market will crash then a few years from now people will be saying, "I don't understand why FHBs didn't just buy houses which dropped in price, but instead bought into a severely overpriced stock market".

Just quietly, I trust our stock markets to value sensible companies a huge amount better than NZ 'property investors' value what they buy.

Just sayin'

Yes but you are forgetting the joy and satisfaction that investors feel when contributing to society via providing those less fortunate with accommodation. /s

Investors, or in a down market, the bagholders, are performing a valuable service to society.

@kraken - very true comment - sarc or not sarc -

I really mean it. There are people out here taking losses and providing others with something valuable.

Many will claim they're doing it for altruistic reasons, when in reality they made a very poor investment decision and are trying to save face by suggesting it was all planned. They're "so wealthy" they can take the hit for the sake of philanthropy, while being a 6 week vacancy away from an uncomfortable letter from the bank.

Sometimes the greedy get what they deserve.

"topping up up the rent to pay the mortgage, often substantially so" - that is starting to reduce with lower rates. For example the interest component of a $500k mortgage at 5.39% is $518 a week. Add in rates and insurance and you may just break even. Then you can use inflation to pay off your mortgage for you - make the lowest possible repayments you can (interest only if they let you).

Not saying its a good investment, but its certainly less of a bad one than it was a year ago.

Great news for renters and for inflation. New Zealand house prices dying by way of a thousand cuts. Where I live listings are pouring on daily and hardly any are selling especially the higher priced houses. Vendors are going to have to really cut their prices.

I'm confused if its only 0.8% according to Trademe, why is it showing at 4.2% in the CPI calculator? I can't imagine they'd have such a distortion between the two?

Different points of measurement maybe - TM is going on listed tenancies. Not sure how rent rises for existing tenancies could be formally measured though.

@Greg Ninness any ideas or someone else on here if they know? Given it was a major factor in the core component would be good to know

GC is correct - different datasets. Trademe is using the asking rent prices from their listings. CPI is using tenancy bond data from MBIE.

How rent prices are calculated in CPI, HLPIs, and RPIs

Rent prices for private rentals are measured in the CPI, HLPIs, and RPIs. They are all priced using tenancy bond data from the Ministry of Business, Innovation and Employment (MBIE). A fixed-effects window splice regression model is used to measure change in rental prices derived from MBIE’s tenancy bond data.

Rentals for housing: A model-based estimator of inflation from administrative data has more information about this method.

bonds do not move up if your landlord puts the rent up tho do they?

few landlords ever drop, tho the new rent agreement may be lower then the old...

I think its hard to get a completely accurate view but it smells like rental growth stagnation across the entire portfolio

When we rented private, our bond didn't increase with the rent.

When our rental was managed, rent increases came with an accompanying bond top up. Which the manager conveniently 'forgot' about when time for the refund claim came.

Tiny sample though - we moved to a new rental far more often than we had rent increases. Consistent with the stat that the average tenancy is ~18 months.

Good point - digging further it looks like Statistics NZ uses tenant surveys to fill this gap in the bond data. The CPI uses stock measures and flow measures:

Stock measure tracks rents across all tenancies (ongoing and new) using survey data from tenants. This captures existing rate increases in existing tenancies.

Flow measure tracks only new rental agreements from the bond tenancy data. This captures current market conditions.

The tenant survey data is pulled from the Household Economic Survey (HES) which also captures household income, expenditure, and housing costs, including rent payments.

The target sample size of the HES is 20,000 households. However it varies each year:

2022 8,900 households

2023 14,100 households

The HES includes both renter and non-renter households and I can’t find how many of these respondents were actually renters. However, Stats NZ data shows that around 35% of New Zealand households rent their homes.

Using this proportion, you can estimate that renters make up about 35% of the HES sample. For 2023, this would mean approximately 4,935 renting households were surveyed.

This equates to around 0.88% of the total renting households being captured in the HES sample for 2023.

That's a good sized sample though. I wonder how it's collected - thinking that there's ~200 working days in a year, that's ~70 samples per day, or 9 samples an hour. If collected by phone (and likely along with other data) and considering non-answer/responses, that would suggest 2-3 people working full time on it.

Actually the 14,100 households that completed the HES includes both renters and non-renters. I’ve just further clarified and corrected that above.

The collection method is actually in person interviews using CAPI. Interviewers visit the selected households which makes it far more cumbersome, yet improves data accuracy, response rates, enable visual aids and reduce misunderstandings.

TradeMe is new rental listings. CPI will be tracking existing rental payments, in which rental increases will be disproportionately loaded into the Oct-Dec quarter due to the long rental freeze implemented by the Labour Govt during Covid which was then locked in permanently due to the law that says you can only put up the rent once a year. Thus a lot of existing rentals get their rents increased to current market rent in Oct-Dec.

A lower inflation number on the way for Q1. LFL.

facts.

Yeah

I am very bearish on the economy. I think inflation is dead

The only real risk is the currency and fuel prices, but they haven’t shot up much so far

I still think the OCR will only be cut another 100 BPs, however I think 150 BPs is a 25-30% chance

Trump will lower the fuel price, or at least stop it from going up.

Sure he will. /s

Inflation's a zombie though. It might only be dead for 6 months.

i do wonder what the consensus is on inflation returning, and when people realistically think it will happen.

Hi Rookie, I don't think inflation is dead so advised my partner to fix her mortgage at 5.49% for 2 years from February.

appreciate it, confirms what i was thinking of doing in april

You may have a better idea how its trending by April, we needed to make a decision right now. You have the advantage of knowing the outcome of another two OCR reviews. My pick is the RBNZ will have to start raising rates, or best case just hold in the medium term.

fair, ill keep that in mind, 1st sign of inflation and ill lock it in

"Inflation's a zombie though. It might only be dead for 6 months."

It may also be dead for the next 6 years. Or twelve. Or longer.

In NZ what kicks inflation off is shocks. The most obvious being energy shocks, i.e. higher energy prices. Sometimes it is storms or cyclones but their effects are actually quite limited.

The big issue - and no one ever mentions is - once energy prices come down .... Why do prices remain elevated?

NZ government had the chance to implement 'windfall gains' taxes. What did they do?

Absolutely fucking nothing.

"We must protect the rich" has bean translated to "we're a small trading nation that must bend over ..."

Not sure rental prices are flat in ChCh for homes?

We have put most of ours up by 5 to 10% minimum and no one has declined for price.

Think tenants in ChCh are staying much longer than they used to.

A lot of 2 bedrooms are probably falsifying true rents in Christchurch

Bang on cue, The Man is the exception to the actual data. Christchurch is the new Riverhead.

They quoted Canterbury prices, not Christchurch a different kettle of fish!

Chch is big enough to quote rather than Canterbury that has a lot of very smaller areas

As I have said many times it is only the ones that new bonds are taken so new rentsls and not the existing ones that have raised their rents without an increase in bond, and that will be thousands of them!

At the end of the day, if you are happy to continue to sit on the sidelines and moan then that is your choice.

The ones that are doing well financially are the savvy ones, who do well in every market.

So you keep telling us which only highlights your fear and anxiety.

the caliber of your comments also tells me a lot about you. very typical sales person.

Ex Agent, no fear of anything and no anxiety.

Just merely telling the facts which so many on here do not want to hear or understand

People are not moaning. They can smell bulldust easily and call it out. If what you say is true and many on this site doubt it as you defend your so called position incessantly it just shows you are a one trick poney. You miss out on so much wealth because of your inability to give something else a go. I did and retired early. You are still mucking around with tin pot rentals in poor old Christchurch.

I did and retired early

Wow you're so impressive, heaps of people retire early.

/sarc

Again you are wrong as always. In New Zealand some retire early. Wages and salaries in NZ are poor compared with many other countries. One reason why so many are leaving NZ to get ahead. Most New Zealanders cannot retire or semi retire until National Super kicks in at 65. In fact New Zealanders are often working past 65 as they do not have enough income to live like they did while working. Rather than trying to impress people I would be the first to admit I have been bloody lucky. I was born 69 years ago, had a good education including university that did not cost a lot, had 30 years of well paid work and assets including my home and equities in public and private companies which I started buying in 1984 have had a good run. I never felt the need to leave NZ.

The youth today have:

- High cost tertiary education

- High asset prices

- Low wages

- Less employee benefits than comparatively offered in your career

I appreciate your admission of lucky, and that you’d appreciate the youth of today looking at the comparison and seeing the world being less opportunistic.

The abject nonsense above?

Clearly most are not actual LLs. Get with it! Tenants are weird. People are weird. LLs are weird. Get used to it. The exception isn't the rule. Most are 'normal' people.

Or, some posters may actually be LLs - but new ones who have not been that smart and are leveraged, and hopefully (but are unlikely to) know that past capital gains won't be coming back for a generation or more - and are now screwed? (Sorry. But not sorry for you.)

This thread ABSOLUTELY exemplifies why NZ is screwed.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.