According to housing market portal Realestate.co.nz, the 2024 property market ended on a very weak note.

They say the activity slowdown in December was more than just the seasonal pullback. In their terms it was 'exceptionally lukewarm' or 'record-breakingly quiet'. Others might say it was downright cold.

New listing activity was low, and the national average asking price was almost its lowest since February 2021 at just $820,250, down -$34,500 for the year. (Realestate.co.nz prefer to use 'seasonally adjusted' levels - $842,476 - but it is unclear why house prices need seasonal adjustment. Sales volumes and listings, yes. But prices? We prefer to report the actual levels, as the selling agencies do, and making them more relatable to metrics from others.)

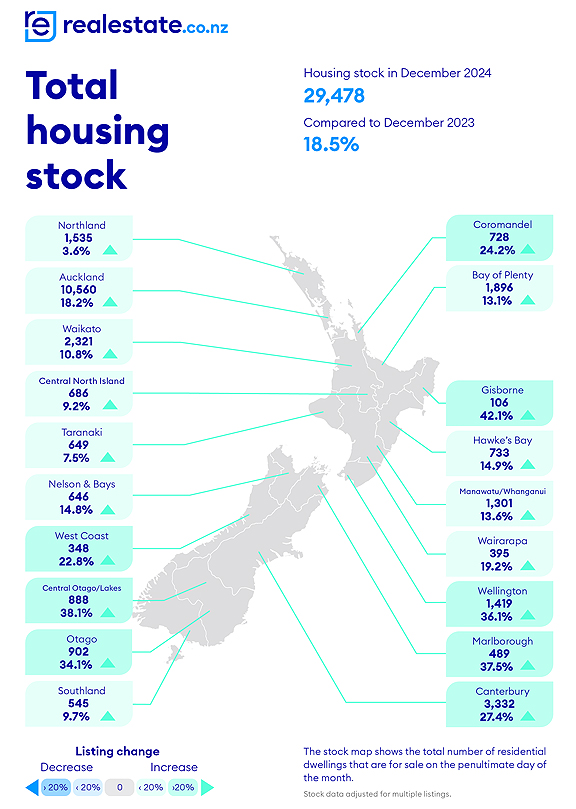

Despite the low new listing level, there were still 29,500 properties for sale at the end of the year, after peaking at almost 34,000 in November. Year-on-year that is +18% "more choice" than a year ago, which itself was near a recent high.

The comment stream on this article is now closed.

As usual, there were significant variations between markets. Eleven of 19 regions saw average asking prices decline year-on-year. But the outsized rises and outsized falls mostly occurred in the smaller regional markets.

In Auckland, the average listing price fell to $961,529, down -5% from a year ago, down -9.2% from November.

In Wellington, the average listing price rose to $844,667, up +2.2% from a year ago, and up +3.3% from November.

In Canterbury, the average listing price fell to $678,722, down -5.1% from a year ago, down -7.1% from November.

As was noted last month, the sheer weight of housing stock for sale is pushing down prices, with vendors having to bite the bullet on price if they are wanting to achieve a sale. And clearly more sellers are.

Buyers continue to be spoiled for choice.

The average time to achieve a sale (by the selling agent) is still 23 weeks nationally, the same as it was a year ago. In Auckland it is 27 weeks (24 weeks a year ago), in Wellington 12 weeks (14), and in Canterbury 16 weeks (14).

The following two tables were supplied by realestate.co.nz and the first one uses their 'seasonal adjustment' calculations.

Housing inventory

Select chart tabs

147 Comments

Nearly half way then, on the slow journey back to affordability.

A grand time for counter-cyclical buyers.

TTP

Please go ahead and catch the falling knife.. don't think ACC will cover people that get hurt doing foolish things

Buyers take your time to build finances and find the right home. There is no hurry.

Those depressing individuals that have done their best to create an atmosphere of FOMO have gone chameleon or simply been silenced by indisputable facts.

This is an awesome time to be a buyer and will be for some time to come.

This is an awesome time to be a buyer and will be for some time to come.

I disagree with this part of your statement, while wholeheartedly agreeing with the first part. As DGM points out, buying now is like catching a falling knife. Buying in a year will increase your deposit while asking prices continue to drop.

Buy in several years as the bottom of the cycle will be around that

Nina, you are hilarious. How do you make your predictions?

Property cycle downturns usually take 6 years to reverse. Nina's on statistically sound ground. You are not.

And just to rock your boat even further, I've been saying we'll be flatlining in real terms for 20-30 years thanks to central government stamping down hard on local government NIMBY'ism by allowing far, far higher densities that'll take 20-30 years to work through.

No worries, Chris, we will see over the next 6 months that the bottom has been reached. Check out your thoughts with Jfoe if you disagree with me (which you obviously do).

The tide is just turning, how back it goes, is too early to predict..

Keep rolling back while the

- rates are HFL

- migration turning negative

- unemployment rising

Mortgage rates at a "just right" 5.49%

Migration still positive

Unemployment rise much lower than predicted.

Exactly, nobody knows how far these price drops will go. Or even if interest rates will quickly go up again. Encouraging first home buyers to over leverage their asses off at this point, is egregious. They could lose all they have and still be left in debt. Right now there are a lot of destabilising factors world wide. Spruikers are either wishful thinking or hoping that someone will buy their problem from them. Or just plain evil.

"first home buyers to over leverage their asset"

Remember that the purchase price of a house can be 500 - 1000% of a household's net worth and entire savings. It is the largest purchase of most households.

Leverage amplifies house price changes - both on the upside and on the downside - those with their vested financial self interest don't mention or downplay the risks, whilst highlighting and emphasizing the upside.

Owner occupier buyers: CAVEAT EMPTOR

Also note that unlike other investments such as shares, funds, an owner occupier buyer is unable to dollar cost average on their purchase price of their purchase of residential real estate.

My bad, 'asses' was auto-corrected to 'asset'. But effectively means the same.

"migration turning negative" - what's your source on that? The figures I can find still have net migration at over 50k inwards. TY.

Dgm makes up stuff, and somehow gets 20 plus up votes - it's hilarious 😂

What is really interesting, is if you compare the inflation adjusted average asking price in Q4 2019 ($700k ish = $904k in Q4 2024 dollars) to the current average asking price of $820k:

Inflation adjusted 2019 $700k value is $904k compared to the current average asking price of $820k.

This also shows that AVERAGE prices are actually 10% lower than 2019, once inflation is taken into account.

Using the RBNZ housing inflation calculator data. Housing prices have a long way to go to even break even with 2019 values. I doubt we will see average values, exceed 2019 inflation adjusted values, anytime soon. I'm picking at least 24 months. Only time will tell. Once the govt recognises building codes/approved products from other countries then we can hopefully expect to see some significant drops in building costs per m2.

I’m beginning to think that I am wrong about significant further house price drops. (This is a post where I really hope to be proven wrong.)

Despite affordable housing being a good thing for society, I fear that even long term this may never again be the case.

There are three main reasons why I am possibly changing my mind:

- The typical measure of house price affordability (house price to income ratio) of 3-4 times the average wage may no longer be applicable. Was that measure not based on a tradition of single income households in an exceptional era of cheap energy and abundance? The new norm may well be housing be 6-7 times the average wage because any competitive advantage is lost if there’s only one income per household.

- An erosion in the quality of democratic institutions. Governments everywhere around the world represent more and more special interest groups and elites over what’s best for the greater good. They would rather devalue fiat currencies rather than see asset values fall. Does this explain why property prices were removed from the consumer price index?

- The rich are getting richer. This has been proven beyond doubt. When this happens, they snap up assets (which include houses.) This happened worldwide during covid. Economies everywhere injected cash into the system which caused a classic example of the trickle-up theory.

If this is correct then the speed that ordinary people have to run just to stay on the housing treadmill has permanently increased.

It’s been theorised that if productivity drops and unemployment rises due to a recession, then property prices will drop. However what may play out instead is an asset grab by the rich, while ordinary people lose their homes.

We live in the asset economy where ownership of assets is incentivised by the tax system and govt institutions over being a productive member of society. This is how the middle class gets eviscerated.

Inequality is increasing worldwide and needs to be considered more when discussing asset price drops. In my view, inequality must be addressed to avoid a neo-Victorian era.

A good thought inducing concept. I however believe that in NZ atleast, there are less examples of the ‘super wealthy’ buying up all the houses and it’s more a case of what might have started out as a bunch of mum and dad investors in the 70’s 80’s 90’s 00’s who stumbled upon an investment that was incentivised via the tax system and success was throttled by capital gains. We should remember in this example that for these investors, YIELD was a huge consideration in their initial investment along with subsequent purchases.

The situation I believe we have now (exaggerated) is a country where:

1 - Cost of the average house (in main centres) is too expensive for the average person to buy and therefore there is less NEW competition in the market.

2 - Rental yields don’t make sense on the average house.

3 - Maintenance costs are going up

4 - Insurance and rates going up

5 - More mainstream talk about a CGT being applied to houses, reason being used as a possible way of financing the cost of our aging population (which is a double edged sword as this means

6 - Even if interest rates drop, due to increased running costs, both investors and home buyers have to take this into consideration when setting a budget to buy.

Now getting back to those successful ‘mum and dad SUPER investors’ - How old are they? What is their retirement plan? Are their kids going to follow the same tradition or throw in the towel and start selling properties to fund their own chosen lifestyle?

I for one know some seriously successful individuals aged 45 and under and can confirm I don’t know ONE who owns more than 3 homes and those that do (historically best positioned to keep buying more) - do not want to add to their portfolio.

2025 another 5% drop in my eyes as a continued controlled sell off happens while the cost of living stays front of mind for the majority of the population.

People are leaving the company I work for in AKL and going to Aussie in droves, so far its been Melbourne, Perth, Brisbane... we have lost about 5% of the IT department in the last 6 months. That's about 9 people, not seen this before towards Aussie.

Most staying away from Sydney due to cost of housing. I suspect the Ponzi cannot even hold current prices with new entrants either not buying First home here or more not stepping up the ladder.

This second point is very important you can live in a typical First Home for a long time, sure kids may have to share a room etc, so the lowest quartile is somewhat protected, but the layers on top totally need new entrants to facilitate boomer retirement, most have their house as there main retirement asset... and its normally not in the lower Q.

Equity is burning like a bushfire.

As Melbourne house prices keep falling, its attraction to New Zealanders will grow. In Australia, a FHB only needs a 5% deposit, and they can apply $15k of their Kiwisaver transfer to that. If they salary sacrifice $15k (pre-tax income) of extra contributions a year into their super fund, they can withdraw that as well ($15k per year, up to $50k max, per person). So $100k is available for a 5% deposit after a couple of years of working there.

Then there is the ability to then rent that property out after 6 months of residing in it, which then picks up a 6 year exemption from CGT, along with the ability to offset any rental losses against your personal income. Before 6 years is up you sell it, and use the equity as the deposit on the family home that you want to buy.

Most Kiwis have no idea how to financially advance themselves in Australia, because they are not used to having a tax system that works for them rather than against them. Hopefully they'll learn. There is much more to Australia than just higher wages.

Interesting thanks KW, sent you comment to a young fam member who moved to Aus.

Just make sure that the contributions are made in seperate tax years as there is a $15k cap per year. So Kiwisaver transfer in Year One, then start extra super contributions in Years 2, 3 and 4. Also note that the super fund will pay 15% tax on contributions (instead of you paying 30%+ on it) so when you come to withdraw the amounts you can only withdraw 85% of what you contributed each year. So work out how much you need to contribute each year, over how many years you need, so that you have the full $50k available when you want to buy a house.

https://www.ato.gov.au/individuals-and-families/super-for-individuals-a…

Most Kiwis don't know that they can be exempt from paying any CGT except for Australian investment property. The main criteria is that you aren't weren't there before 2001, you don't have a spouse who is a permanent resident, and you stay on the SCV visa (do not apply for citizenship). I'm thinking of going back there because of FIF tax here as most of my money is in foreign stocks.

Very true, would also add foreign sourced income (ex salary and wages) does not need to be declared in Australia if you are a non-protected SCV as well. (plus all the other criteria you mentioned)

Australian tax system is very lucrative for Temporary resident SCV.

✈️✅

SBS and AucklandBattler, both thought provoking comments, thanks.

Agreed. It’s a ticking time bomb, housing affordability waning will only increase crime/poverty and the further breakdown of the nuclear family unit. However people may be surprised at just how much time is left on the bomb, and just how much this can stretch out. A pressing issue contributing to this problem for western developed countries right now is immigration. Hard to see any revolutionary changes in the next few decades when there’s so many people from the third world that would murder their family members to participate in the status quo.

The world makes a lot more sense when you think about society and people working for the top few per cent. They need:

- Worker bees without worker power to do the work. These worker bees are made up of (i) domestic renters doing menial work, so their wages flow straight back to rentiers through housing costs (and monopolies / duopolies), and (ii) slave workers offshore making cheap goods to keep everyone happy. Low welfare, a nice level of unemployment, and prison keep the domestic worker bees in line. Border controls, global institutions (IMF etc), and foreign / trade policy keep the slaves poor and offshore.

- Educated domestic drones to manage the worker bees and do a range of mostly bullshit jobs. The primary role of the drone is to take on mortgage debt, which expands the private sector balance sheet and inflates property prices - creating the flow of credit that keeps the housing ponzi and the whole economy going. The net flow of credit has to be sufficient to satisfy the desires of the top few per cent to accummulate cash, which they use to buy more rent extraction assets.

- Companies to get stuff to consumers and do other dull stuff like building stuff for the poors and manufacturing things - there needs to be enough activity to make it look like we have a functional economy in the traditional sense. Critically, the real role of companies is to take on debt and provide shares and equity that can be held as assets by the top few per cent (again, to facilitate rent extraction).

Hapy New Year.

All the while destroying the environment, just to line the pockets of the top few percent. Nevermind everyone, have a soma and go back to watching your parlor wall

Yup. Time for a New Deal.

And sadly we vote for it year after year

So cynical, yet so true Jfoe.

Though Mr Luxon appears to be betting against the housing market. Watch what they do, not what they say. As they say.

Seven houses Luxon had a bad ring to it. Three houses (and one electorate office that I rent to the taxpayer) Luxon sounds way better. Not

I wrote to Luxon in 2022 saying I'd never vote for him while he had 7 houses. I do not flatter myself that he read my letter and took it on board. I'm more for the "watch what they do" reason.

Yes I did the same - basically said national appeared to be the party of landlords and property speculation and not much else.

Yes, not much else, apart from

- dairy

- promotion of exports to other countries (ie new trade deals)

- law and order

- getting children back to school

- reducing thuggery at KO houses

- utilizing our natural resourse (eg gas fields)

I could go on.

Fair point (and favourable things which I agree with) but in terms of fiscal spending, the biggest winners were by far landlords in the national budget.

And as a result, rents not only stopped going up, but in fact are now starting to fall. Therefore the biggest winners by far were tenants.

On the right track that's why everyone is staying..

So you would prefer to vote for people that have no financial ability to invest?

No wonder Labour got thecountry in the mess they made!

Other political parties are available to take your vote.

I would say it has more to do with having to downsize from a $4,000,000 a year salary, to a $479,000 a year salary. He now needs to conserve cash outflow in order to maintain his previous standard of living.

We live in the asset economy where ownership of assets is incentivised by the tax system and govt institutions over being a productive member of society. This is how the middle class gets eviscerated.

This is correct, and the precise reason why the tax system needs reform and incentive for investing in housing needs to be dissuaded by targeting capital gains and more useful a LVT. However, this in mind, those that already have will not be so impacted by a CGT or LVT as they have already accumulated assets and can simply make less profit, but still consistent as they aren't as reliant on a higher yield to justify an investment by means of having lower, or no mortgages.

This would all sound plausible, if it happened every where but in jurisdictions that have less restrictive land use policies and have had exactly that same things happen as you are saying, they have remained at low median income multiples.

Housing wealth is driven by middle class demand and speculation. Look at wealth split up by asset type of each income class. The super rich have a small minority of their wealth in real estate. Even deca/centi-billionaires are only going to have 10 to 20 houses each.

Real estate isn’t a good way to become super rich. They don’t care that much about it. They have access to far better returns.

Who's watching the bond market sell-off? UK 10Y at 4.81%, US 10Y at 4.69%, AU 10Y at 4.56%, and NZ 10Y at 4.55%. The era of easy money is over, expect higher taxes ahead.

Be back down by March.

I’m calling it: the US 10Y will hit 5% by March.

Interested in your thoughts why, Jfoe?

It's a treble bet that (i) Trump will go nuts with tariffs and domestic deficit spending AND (ii) this will drive an increase in the overall price level (inflation) AND (iii) the Fed will respond by keeping rates higher for longer.

I don't think this chain will hold.

The chain not holding, meaning another financial crisis?

Except it's not all about the Fed and Donald Trump, there are plenty of other factors influencing rates. Central banks still have to operate within the framework of a global economy. They can't just arbitrarily set rates at whatever level happens to suit them.

The Fed can.

The Fed has no control over the long end of the yield curve, anything beyond the 2-year mark. And your point is that Trump won't push as hard on tariffs? The bond market was already selling off even before Trump's tariffs were mentioned. Also, consider that a higher USD (DXY at 109) is inflationary for the rest of the world. Other countries will need to import that inflation, and their central banks might have to hike cash rates to protect their currencies.

Geoffrey Gundlach would suggest the US2Y controls the FFR not the other way around....

They might like to think they can. I think you'll find they're still subject to the same market discipline as everyone else though.

Not at the short end....but yes eventually when enough damage is done (outside the US) then the penny will drop. Interested to know why you think by March JFoe?

by Jfoe | 10th Jan 25, 7:40am

Be back down by March.

Do you think that Trump will act fiscally responsible enough to stop the rise in yields... I somewhat doubt that myself.

See above. Fiscally responsible relative to what? Biden has been deficit spending at 6% of GDP or thereabouts (same as Trump did during his first term). And, this time Trump has a shrink the state agenda, which will lead to some spending reductions. I'm no fortune teller obvs.

I think yields are rising, asking for a risk premium, due to excessive deficit spending.

I think trump will talk to it, but the US will keep borrowing more then the market wants it to, hence interest rates will go up further, i think China are perhaps missing buyers so rates move higher as less buyers. Also I think oil money is moving into gold and BTC as well as diversifying out of USD.

Its possible that NZ rates at 10y could be lower then US 10y if NAct holds the course to a 2028 surplus....

restraint here may actually be the best course of action.

China's yields are falling because many are predicting extremely low inflation (maybe even outright deflation) in China for quite some time. Or put another way, simply holding 'money' makes money as the prices of other stuff falls - a classic deflation cycle. So in many regards (but not all), what's happening in US bond markets is the exact opposite of what's happening in China's bond market.

2028 surplus...? How...

i'll give you 10 to 1 odds on a 2028 surplus!

I'd love to take that bet.

But morally - I can't.

"this time Trump has a shrink the state agenda, which will lead to some spending reductions"

I think this is just an excuse to cut/underfund the bits of state that he doesn't like, while overall spending will remain high/higher

Yes, Trump is a spender and will likely support US equities if he can, but he hasn’t promised a higher stock market. Bonds are becoming a very attractive "risk-free" alternative. He might get frustrated with Powell, but Powell is staying in place until May 2026. I see Trump pushing inflation higher while Powell keeps rates steady, with no cuts in 2025.

"Do you think that Trump will act fiscally responsible enough to stop the rise in yields... I somewhat doubt that myself."

An asset swap from a declining sharemarket may though.

Buffet and Burry seem to know.

One would assume they are holding their cash in bonds or treasuries of one duration or another...10 year though??

Edit...thinking about it no reason why not 10 year.

People like him hold their cash in money market funds that invest in the Fed's Overnight Repo facility, paying the Fed interest rate (currently 4.25%). The rich ARE different.

Found this article re Buffet

"As Buffett sells stocks, he's been putting the funds into a very specific investment: short-term Treasury bills. These are Treasury bonds that mature within one year. Buffett prefers those maturing within six months or less. Through the first six months of 2024, Berkshire Hathaway padded its Treasury holdings by $94 billion.

The company held a total of $277 billion in Treasury bills and cash as of the end of the second quarter. Even as Buffett has sold shares, Berkshire's core operations continue to produce operating cash flow of roughly $12 billion to $13 billion each quarter. On top of that, Berkshire will collect roughly $3.5 billion in interest from the Treasuries it already holds. Add it all up, and Berkshire's position in short-term Treasury bills is rapidly approaching $300 billion (assuming Buffett hasn't found a great company to buy in the last 2 1/2 months)."

https://www.fool.com/investing/2024/09/16/warren-buffett-has-nearly-50-….

So Buffet unlikely candidate for longer dated....unless he sees need to change strategy...but there will be plenty looking for the safety of bonds if the US stock market looks like taking a dive.....and things are not as flash as painted in the US at the moment.

Thank you.

I'm very new to thinking about the US treasury market, but do you think a likely situation is that yields will increase upwards towards, or over, 5 in the short term? With the caveat that if, perhaps when, a share market downside occurs the yields will decrease as money seeks a relatively safe haven?

HFL my friend...

Broken record, my friend

well they are not moving in your direction at the moment are they?

the curve is steepening

Most of it is Trump speculation. There's little in the long term fundamentals to suggest inflation is going to become a pandemic-level problem again.

Great news to see both asking prices and sale prices plumb new depths, at the end of 2024.

It sets up the continuing NZ housing market crash of the modern ages. So epic, Poets will write of it, in the future.

Then for the continuing NZ property slump into 2025/2026/2027.

These property crashes take on average 6 years to play out, or longer. Then we go into the long, scraping bottom.

Bottom to hit perhaps, in 2028?

Fact: "Every bubble busts, completely". NZ bubbled to worst and the bust is just merely, midway.

https://www.visualcapitalist.com/cp/mapped-global-housing-prices-since-…

I'll take that bet. The turning point was 12 months ago and average new mortgage amounts have continued to rise. People spend as much as they can afford to get a weatherboard palace in the right suburb, and FOMO plus lower rates will do the work from here like they always do. Unless something changes in tax / LTV / DTI of course. It won't though - our economy is dead without a decent flow of credit money.

Timespan looks convenient…

Housing is doing badly by itself... a CGT now will kill it completely.

NAct is smart enough to change nothing while the boat is drifting in irons.

We need some headway before course could be changed, though I see nothing from NAct that indicates they have any course changes in mind. I am watching closely the UK situation, things are bad here as well but more focused on private debt for housing.

"Unless something changes in tax / LTV / DTI of course. It won't though - our economy is dead without a decent flow of credit money. "

Negative net migration?

I think the next major thing for NZ will roll in from offshore, like a tsunami....

an appreciating USD?

JFoe, quite a lot of new supply being soaked up and they all need mortgages.

yes, but it only takes a whisker of competition and a well-trained agent in a suit to get the prices moving. i might be wrong - and, if I am, I will be more pleased than anyone!

I expect you to be wrong. The quantity of unsold new builds is significant, the message about 'supply' is now out there and residential property investment isn't the only game in town anymore, more so with a CGT coming?, and I don't expect any number of "well-trained agents in a suit" to change anything much. Welcome to a 70s housing market? We'll see.

Correction, the quantity of unsold new build townhouses is significant.

"Alive in 25" Kiwibanks estimate...NZD @ 55 cents ? OCR falling below 3%? An improvement in rental yields (currently 3.9%)? Squiggly 6% house price growth/decline (I cannot determine if thats a negative or positive symbol? maybe they used squiggly to cover the field...lol) Unemployment rising thru into 2026...Households are a few pay rises away from real income growth...lol, It will be a year of 2 halves with 2.2% growth ...lol There is an expectation of a housing market recovery . Fingers crossed it goes to plan ...lol ...

https://www.kiwibank.co.nz/business-banking/thrive-hq/kiwi-economics/co….

This section seemed eerily possible

Tariffs and conflicts: A downside scenario

A downside scenario is one of stagflation – high inflation and low growth. Rising geopolitical tensions are a significant risk to the outlook, with implications for the macroenvironment. Our downside scenario assumes a global shock that leads to a reacceleration in international inflation. This may be characterised by tariffs imposed by the US as proposed by US President-elect Donald Trump, an escalation in the Middle East conflict or other black swan event. Against this background, import prices will likely spike and, by consequence, our terms of trade will deteriorate. The exchange rate will also weaken as a result. A reacceleration in imported inflation will likely see headline inflation breaking back out of the RBNZ’s 1-3% target band. High inflation will necessitate restrictive monetary policy for longer. The RBNZ will have to keep the cash rate above neutral. Economic growth will likely deteriorate, falling back into recession, and lead to a deeper deterioration in the labour market. High interest rates and rising unemployment will weigh on the housing market.

Yes a cut in Feb is required perhaps 50bps, but imho after that its going to be on data watch, they will want to cut but need to be very aware of offshore events. of that cut IMHO on 2y and longer mortgages you may well only see half of it passed on

We made a decision that none of it will be passed on if there is a cut in Feb, or I should be clear it will only be passed on for short term rates, the longer term rates will stay the same or possibly even begin to rise from here.

NZ has been relying on imported deflation to offset the ~5% domestic inflation. Once that deflation turns into inflation again, the overall number is going to be well out of the 2% range. The RBNZ will be hard pressed to claim that this is "transitory".

.

49 comments already on an article about asking prices over the Xmas break. Lol.

Best reading around!

It's better than arguing with climate deniers over on the daily

Even old Warren Buffett has 25% of his total capital under management currently held as cash. Interesting because he is often quoted as saying holding cash is bad. Quite a vulture fund none the less.

He also says the key factor in over valuation is low interest rates, leading to easy access to cheap capital, fueling over leverage and speculation. Sound familiar?

Role the dice out there in 25, but clearly he thinks value not supported by income is a sucker's play.

Even old Warren Buffett has 25% of his total capital under management currently held as cash. Interesting because he is often quoted as saying holding cash is bad. Quite a vulture fund none the less.

Anyone who understands Buffet will know that he's always been partial to crony capitalism. Buffett's investment strategies have often intersected with government policies, especially during times of economic distress. For instance, during the GFC, he made significant investments in the Vampire Squid (Goldman Sachs) and General Electric. These investments were made with the expectation that the U.S. government would intervene to stabilize these institutions through bailouts. Critics argue that Buffett's ability to profit from these situations exemplifies crony capitalism, as he leveraged his political connections and the government's willingness to support failing companies for his benefit

In 2011, Buffett invested $5 billion in Bank of America, acquiring warrants that allowed him to purchase common stock at a favorable price. This investment eventually turned into a paper profit of around $12 billion as the bank recovered from the crisis.

I once idolised Buffet but I now see him as a bit of a money/power obsessed psychopath who to his credit gamed a corrupt system to receive extreme wealth for himself which in a better system wouldn’t flow so easily away from those who really need it to those who really do not need it.

(and yes I’m aware of his philanthropy but what has been gained doing what he has done, only to give it away? He gained an ability to determine where and who received his capital but what other benefit has his behaviour achieved for humanity? I’m sure there are some positives there somewhere)

17.6% below their January 2022 peak

That means my two neighbours houses asking prices are 18% too high, or $150k and $180k respectively. No wonder they've been on the market for 6-12 months without a sale.

Well if you invested in Ryman Healthcare in Jan 22 you have been cut in half.

I think one wants to move into a Summerset home in the big smoke and is holding out for a number, not a market signal.

Well if you invested in Ryman Healthcare in Jan 22 you have been cut in half.

Not sure where you get data from but Ryman's only down 21.5% from Jan 2024. I agree that it's a directional barometer of the health of the Aotearoa Ponzi and the generally messed-up economic vision of a predominantly middle-class Pakeha culture.

Jan 22.

Or 70% down from Feb 2020

Gotcha. I wouldn't touch Ryman with a barge pole. But I'm out of step with the financial advisory community.

The NZ Superannuation Fund is one of the largest shareholders, holding approximately 18.65 million shares or about 2.71% of Ryman's total shares. Cooper Investors Pty Ltd is another significant holder, this investment firm owns around 6.53% of the company. Forsyth Barr has a stake of about 6.42%.Harbour Asset Management has approximately 5.00% of Ryman.

If I understand correctly after vacating these 'homes' there is a set buy back price (after fees). This causing all sorts of grizzles during rising house rises and leading to calls for Govt intervention.

But this may bit them on the bum if they have to drop onsell prices - as they will.

Or perhaps I am mistaken and the buy back price is not 'set' at a minimum?

These Ryman/Somerset villages are the canary in the coal mime for housing.

One of the most pressing problems for Ryman is financial performance - a dramatic 98% drop in net profit for the fiscal year ending March 2024, falling from $257 million to just $4.8 million. This decline was attributed to substantial one-time costs and a decrease in property values, alongside rising operational expenses that outpaced revenue growth.

- The Ponzi was flat in 2023 so not sure why property values were supposedly falling. Probably because they were overvalued to begin.

- Anecdotally, I hear Ryman management are making out like bandits personally while being very average to poor businesspeople.

https://businessdesk.co.nz/article/finance/ryman-burned-through-hundred…

There is no "buy back" price. You get back what you paid them, minus 20% which is their deferred management fee. Although now they have upped that to 30% for new village entrants.

Ryman then "refurbishes" the units (seen what that entails, and I would dispute the use of that term) and sells it again at current market prices.

So someone who bought a unit for $500k five years ago will get back $400k and Ryman will then resell the unit for $800k. The new resident will get back $560k at some point in the future when they move out.

"move out"

LOL!! Good spot!

To a better place

Unless they end up in the hospital wing on palliative care and burn down the equity paying for it before they pass on. Not sure exactly how it works (I was not privy to the finance) but had a family member do that, leaving the surviving spouse a pauper.

They should just burn down to $284,636, at which point the government threshold kicks in and the taxpayer covers the cost of hospital level care. This threshold drops to $155,873 if the surviving spouse is still in the family home and they elect to not include the value of the home and car in their total assets.

While this is officially administered by MSD (Ministry of Social Development), it is easier to read the Eldernet website, so here's a link:

https://www.eldernet.co.nz/knowledge-lab/residential-care/who-pays-for-…

yes, thats what i mean about buy back price. I appreciate you do not own the unit, you lend them cash and get a right to occupy of sorts. And you get less back (buy back price i refer to)

If i recall they don't pay interest for tax on this 'loan', nor on the cap gain on resale(or something like this). Hence the tax profit is way less than the accounting profits.

They don't pay interest on the loan, correct. But there is no capital gain because they are not selling an asset, they are licencing it. So the "resale" amount is treated as revenue, and they pay standard income tax on whatever profit they make (which in Ryman's case, is not much).

They don't pay standard income tax - they borrow money, provide accommodation in lieu of interest and no tax occurs on the transaction.

Re-selling a licence again and again at profit seem pretty much a core income activity for them.

IR issued a Binding Ruling.

It would be nice if house prices stayed high and we can sell them and all be rich, but the problem is that it costs the nation too much. That cost is in the repayments of around $360 billion and the need to increase this by almost 4% per year to just maintain the current values. Unemployment is rising, our productivity is one of the lowest in the OECD and we aren't even close to paying our way in the world with a massive government deficit. A halving in property prices and a redirection of money to the production of wealth is probably the best way to become a viable economy again.

These views are labelled as ‘doom and gloom’ NinaK by those with a vested interest in prices never falling. But I agree with you.

The debt will still be 360bil if property halves as few will get out ahead... we are 17% down already , few got or can get out without decent haircuts. It will be a drag on the economy for a generation, who will likely leave for greener pastures.

Nats are real bad for the economy per the graphs 15 years ago & now

Housing best investment. Rates. Insurance. Maintenance. No tax advance. And deposit gone.

At the risk of being called a spruiker, this sounds like house prices may have turned the corner. Reduced listings will reduce supply.

The market turned in December like I said it would.

Just like you said it turned the corner when it peaked? Or can you only call the bottoms of markets and not peaks?

You mean like you first commented August - October 2023 was the time to buy because prices would rise when National were elected? And then Tauranga prices would rise around 5% in 2024, yet Core Logic reported they declined 3.77% year on year? But a stopped clock and all that.

he has had more bottoms then freddy mercury

Supply is coming many just still asking too much so withdrew, they will be back as it continues to fall.

Much more housing supply comming in 2025, as the greed of developers knows no end and they will eat themselves alive, with building supply still flooding the soaked, falling and increasingly flaccid housing market.

Good employment news in USA.......IS BAD NEWS FOR NZ!

We are now importing +5% inflation overnight.....with oil surging and NZD IN THE DUNNY.

RBNZ needs to emergency hike the OCR, TO DEFEND NZ FROM THE INFLATION MONSTER!

I’ve a question, for everyone. My wife and are selling a house in March, or trying to. Debt free. Rv $820 000. We are aged about 50 and live in a farm provided house and have other savings. What do we do with the cash?

Get a safe and secure 4.5 to 6% and spread it about the biggest banks ....... and trust your 100k per institution is a secure by the soon to be - Deposit guarantee. Bank offerings % are likely to start increasing soon too with worlds interest rates about to start a hiking cycle.

Or into a productive business that you fully control and is recession resistant.

Your other option is to flick it back into the hellishly overpriced and (and half collapsed) low yielding NZ housing Ponzi or the overpriced world Share markets.

All are rolling the dice apart from the more secure large main bank deposits.

Your money, your risk, your call.

How about Kiwibonds?

I can supply you with a bank account number to transfer it too, but seriously just put it in a Term Deposit at a major bank and earn some interest on it while you decide what to do with the rest of your life.

Zwifter !!!!! ....

"but seriously just put it in a Term Deposit...." WTF !!!!

Stop giving people financial advice. You are not qualified to do so.

Hey stupid, please explain the risks to me of putting it in a TD for say 6 months while you evaluate things ? I suppose you think it would be cool to put it all in Bitcoin right now ?

Seek professional financial advice....and then triple check everything you are told.

"Seek professional financial advice"

Seek an individual who is acting with a fiduciary duty who is truly acting in your interest and not a commission motivated sales person seeking to sell a financial product due to to their vested financial self interest (and uses the label "financial advisor" who may really be a wolf in sheep's clothing)

Seen some friends get sold financial products where they lost a large proportion of their life savings.

Understand ALL the risks of their advice clearly.

10 questions to ask financial advisor:

https://www.nerdwallet.com/article/investing/10-questions-ask-financial…

CAVEAT EMPTOR

Why are you selling the house?

If it is freehold, why not just rent it out for some income? It doesn't sound like you have any particular plan for the cash from the sale, and you have other savings, plus it is a tough time to sell, so it is hard to see what incentive you have to sell up.

We are in the south and the house is 11 hours north so very difficult to do anything with it. It’s been rented out since we have owned it and was supposed to be our retirement home but plans have changed. The sad reality is that the rental yield on the house is less than the return from our term deposits when all costs are taken into account. It was bought prior to covid as a mortgagee sale so capital gain has been good, though capital gain over the next few years looks low to negative in my view. Better places to put the money I think.

take the cash

Fair enough. Im 75% cash and but don't know what to do with it.... Maybe I should buy your house :)

All houses are freehold unless they are crossleased!!

He means unencumbered!

Just shows you that many that make comments, really should not be commenting or giving any advice?

I guess it depends on what your end goal is and owning a house is a necessity. I think this is pretty true "Someone is sitting in the shade today because someone planted a tree a long time ago." Warren Buffet

"owning a house is a necessity"

That is the conventional and commonly held belief.

Shelter / accommodation is a necessity - assuming people are in a financial position to choose, people can choose to buy or rent their accommodation / shelter.

Under what conditions is it better to choose to rent over buy?

redacted

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.