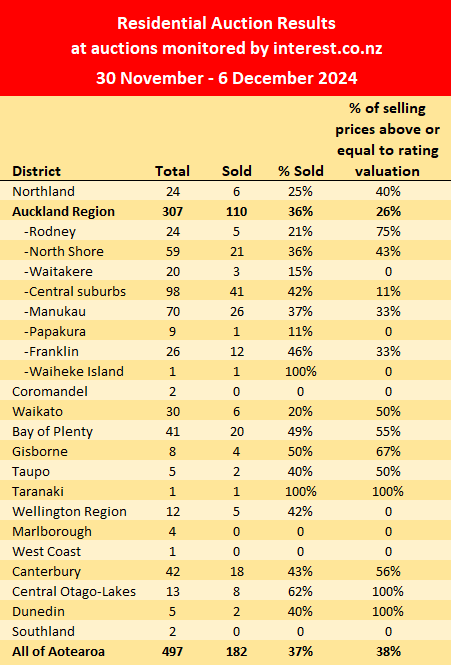

Auction activity remained at a very high level over the week of November 30 to December 6, although it dropped back slightly from the levels of the previous two weeks.

Interest.co.nz monitored the auctions of 497 residential properties over the last week, down from 504 the previous week and 517 the week before that.

However, there was almost no change in the number of properties that sold under the hammer over that three week period, with their numbers remaining in a very tight range of 182-187.

That gave remarkably flat clearance rates of 35% to 37%.

Of the properties that sold at the latest auctions, 38% achieved prices that were greater than or equal to their rating valuations.

Aucklanders appears to remain the most cautious on price, with just 26% of sales in the region achieving their rating valuation or better.

The table below shows the regional results from around the country.

Details of the individual properties offered at all of the auctions monitored by interest.co.nz, including the prices of those that sold, are available on our Residential Auction Results page.

The comment stream on this article is now closed.

66 Comments

So, if you take Auckland and Wellington out of the equation, 68.66% sell above RV.

You really do not want an Auckland, or wellington, rental portfolio from the peak, disastrous.

Do these results confirm medium prices will be dropping for a tenth consecutive month ?

What about rare and well done prices?

So, if you exclude most of the New Zealand housing market, we're actually doing fine.

For some, the best form of defence is denial. If that fails - attack.....

Lower interest rates have not proved the quick broad based and sustainable panacea.

Usual type of useless comment from you. I am just pointing out that Auckland and Wellington markets are languishing whereas it seems everywhere else is at the RV mark. A run down house typically sells below and reasonable houses sell above.

Attack!....case in point.

Grow up.

Any AI platform and a ten year old with prompt engineering skills could research the facts to tell you the ROI on property investment in NZ is dead and buried. It’s only the blind and heavily invested who will tell you otherwise.

My point is that the Auckland and Wellington markets are not doing as well as the regions

Basically what I have been saying since Covid. Things changed post Covid with the shift to working from home or at least working from home a few days a week. The regions suddenly looked pretty attractive with far better quality homes at much lower prices.

Your correct, history tells us the center falls first then the regions.... the regions just have catching up to do.

Some may see some positive flow based on how overpriced the center is, witness reefton etc

So AKL has fallen seriously while Turangi is a star... I think not... its just about to correct in 2025

Another forward looking indicator as to the state of the residential market is Rymans and Fletchers share prices. They've had that many false starts and yup, heading down again....

You're right ITG, it's happened before. Aside from obvious employment insecurity in the regions, if one wants to shed the big city obligations and head to the regions and you can't get that price, the regions will suffer too - eventually (including Tauranga)

"If you take half the country out of the equation, 68% of properties sell above their far more recent CVs"

No shit sherlock.

So, if you take Auckland and Wellington out of the equation, 68.66% sell above RV.

Now do it as the percentage of properties auctioned that sold over CV rather than the percentage of those that actually sold.

So 80% of auctions are not selling for under CV...

lol I see what you did there

I would be interested in readers views:

(1) is capital gains (above inflation) in residential housing over for the foreseeable future (5 years +) ?

(2) if the answer to (1) is yes, is it better to not own a house, put savings into a diversified fund, and rent ?

It seems pretty likely we will get a CGT in the next 2 terms (labour has all but signed up to it as a primary policy), immigration is slowing and emigration is continuing (of our brightest next gen), our biggest trading partners have slowing economies which will get worse when Trump starts trade wars. The global outlook is pretty dismal (us is struggling with inflation as it's economy rebounds). Trjmp and musk are gonna rip into the usa defecit.. Etc.

Expecting nz house prices to just keep rising because they always have.. looks quite unlikely.

Smart money is in tech and supply chain businesses to replace China.

Toast wasn't asking about a CGT, he just asked about expected capital gains in the next 5 years.

lets just pretend CGT will never happen, fixed it for you....

It will probably have family house excluded at average values, so the slobs impacted are investors... therefore CGT will help FTB compete with Investors... end of story

If they are crazy enough to bring in a CGT on rental property there is without any doubt to be major consequences!

There is going to be a major shortage of people providing housing to those that need it.

rents will increase and house prices will increase.

Personally wouldnt be worrying us as prices in ChCh do not give enough return for renting out.

Be very careful what you wish for.

You have a great plan, as Mike Tyson said...

Why would a CGT on rentals matter? After all, rentiers are in it for the yield and to provide a public service, right? It's not like they're just in it for the deductibility-backed-interest-only-mortgage-subsidised-by-tenants for future tax-free capital gains, right?

You make it sound like rentiers have amazing advantages!

they will not once CGT for rentals, hence PM is selling... he was only investing for yield... honest

Personally, I fully support a comprehensive CGT on houses aside from the owner occupied family home. Willis is struggling to find viable revenue streams and our debt continues to unsustainably rise. It's now time to milk a cow that has helped place this country in the fiscal unproductive state that it's in today.

Bring it on. It's long overdue and portfolio reducing Luxon knows it.

You don't really want it RP, you are just virtue signalling. Everyone knows this is just s slippery slope that will eventually include the family home, its not going to fly in this country and any party that suggests it will be toast come election time.

Zwifter, who are you to decide what I do or do not want? To suggest it would be linked soon after to the family home is a convenient scare tactic (born of the housing besotted) that will be well worn out come Election 26. Have you stopped to consider the ever rising Local rates are really a form of CGT too? CGT/wealth tax in some form from Central Government is gaining support, it will float provided it excludes the family home.

Like I said, bring it on.....

edit

Not gonna happen. Any fool can see it will eventually include the family home, that's just the way it works, theft by stealth.

Any fool can see it will eventually include the family home

So remind me again, who are the two-thirds of public that support CGT in some form here then?

Why do you think you can comment on behalf of anyone let alone everyone? It's not a slippery slope, Australia, UK and Canada don't have capital gains tax on the family home so why would NZ?

I really think the upwards pressure on rents is the major consequence of a CGT that most kiwis overlook. Overseas at comparative countries with CGT the rents tend to be noyably higher.

When you add a tax to a service, the consumer will be the one who eventually pays.

It seems pretty likely we will get a CGT in the next 2 terms (labour has all but signed up to it as a primary policy), immigration is slowing and emigration is continuing (of our brightest next gen), our biggest trading partners have slowing economies which will get worse when Trump starts trade wars. The global outlook is pretty dismal (us is struggling with inflation as it's economy rebounds). Trump and musk are gonna rip into the usa deficit.. Etc.

Expecting nz house prices to just keep rising because they always have.. looks quite unlikely.

Smart money is in export stuff, displacement tech, supply chain manufacturing businesses to replace China. Etc.

Labour will stay signed up for a CGT as long as internal polling tells them that they should stay signed up for it. That is how long that policy is going to last.

Hi Toast, unfortunately, you're unlikely to get too many balanced replies, there will be the anti-housing posters telling you not to buy and the pro-housing crowd telling you to buy.

Here's my view. From your question, it looks like you're asking about a house as a home to live in. Therefore there are many more aspects to consider than just the financial aspects, which, as much as we'd like to say that we know where house prices are going in the short term, we actually just don't know.

I would buy as house to live in if I could reasonably comfortably afford one (i.e. 20% deposit and repayments no bigger than 40% of your income). My reasons are:

1) You get security of tenure, no one will ask you to move out, this gives you certainty and peace of mind in life.

2) The principal repayments of the mortgage are a forced saving scheme. We can have the best intentions for saving, but it's very easy to spend money elsewhere. A mortgage forces you to save

3) From 2), comes that you will end up with a freehold house worth well over $1 million

4) You have the freedom to do what you like to your house, renovate it, add a bedroom, sell it etc...

Edit 5) Pride of ownership, which goes a long way towards happiness and achieving other goals in life.

The capital gains, and you will get capital gain in the long term, will simply be (a very handsome bonus) over the above points.

Cheers.

You also get comments from the heavily committed property club. All points are valid and are often used by the vested interests to justify today's crazy prices. I would offer the following...

Tenure. You can also contract this in a way but the real issue is poorly capitalised speculation chasers (to much debt) trading or being forced to liquidate. Ask your landlord their debt exposure.

Reducing debt is a form of saving. Often the return on each doller reduction saves you more than other investments would make you. Note. You need good surplus invome to really make this work.

Not all houses are worth 1m. Good tools avail today to get a quick general idea of value. Also clue into sqm construction tion costs so you get a view on replacement alternatives.

Freedom. Watch Braveheart.

What…? What a confused post, which does't answer Toast's question at all (how is asking his landlord for his debt exposure help Toast decide to buy a house or not?). Lastly, by the time Toast repays his house, in 25 years, even an entry level house will be over $1 Mill, so he will be a millionaire.

Oh what an attractive prospect that will be in 25 years after extensive bastardisation of the currency.

Oh you’re a millionaire!

I agree that being a millionaire in 25 years' time is not as good as being a millionaire now, and especially 25 ago, but still, it's a lot better than having nothing.

Yes and with the right assets or risk appetite you could have so much more.

Unfortunately housing is not the same game anymore, it’s a shit investment for the most part (at least for a while) and appeals to thickest of our population as a path to wealth.

"you’re a millionaire! "

What many people may not see is that over the course of 30 years, the owner paid more than a million dollars to own an asset worth a million dollars.

So what ? You're still much better off than the people who spent their money renting for 25 years and have nothing to show for their expenses. You see, you're focusing on the wrong part, look at what you're getting out of it, rather than the others. I'd happily pay you $ 10 million if you return me $11 million in one year.

"You're still much better off than the people who spent their money renting for 25 years and have nothing to show for their expenses"

Yes, for those who do not have fiscal self discipline this may be a method of enforced savings.

For those who have fiscal self discipline, there could be alternatives with better financial outcomes.

Can you show your calculations as evidence that it is better to buy and the comparison you are making.

"I'd happily pay you $ 10 million if you return me $11 million in one year. "

That isn't the proposition that is currently being offered. Here are some calculations.

Would a fiscally disciplined person be willing to pay $1.4mn over 30 years, to receive an asset in 30 years time worth $1mn? That is the example referred to above and the situation currently.

Here is something that most people may not be able see:

Purchase of house: $600,000

80% LVR mortgage: $480,000

1) total mortgage payments over 30 years: $1,046,144

- pmts $670.61 per week x 52 weeks x 30 years for 80% LVR mortgage of $480,000, 6.0% mortgage interest rate and 30 years.

Note that the total interest paid over 30 years is $566,144.

2) total rates, insurance, maintenance over 30 years: $199,816

3) initial deposit $120,000

Total payments over 30 years: $1,365,961

House value after 30 years $1,000,000 as above.

Is that a good financial outcome for retirement? What if the homeowner needs to move closer to family or downsize (into a retirement village or more easily maintained property), or needs to sell for their aged care?

Could that total payment over 30 years of $1,356,961 be used elsewhere for an improved financial outcome after 30 years?

Each person has their own situation and should do their own calculations.

People are free to choose, however people are not free to choose the consequences of their choice.

https://www.nzherald.co.nz/business/house-prices-buying-at-peak-continu…

much better off to buy at the bottom....

"Yes, for those who do not have fiscal self discipline this may be a method of enforced savings"

All your calculations and best intentions are pointless. Ultimately, there is no better fiscal discipline, than being foced to save by repaying the loan monthly.

If you're truly very financially disciplined, you can own your house AND invest in other asset classes.

Sorry, but your calculations, whilst not wrong, are just good intentions and theoretical fluff.

Repaying a loan that, with inflation, sees the payment burden gradually reduce over time from the ability to increase repayments when you get a pay rise. I've shortened my loan term by 6 years in the last 3 years just from increasing repayments by 5% each year at pay rise.

Meanwhile....

The consumers price index data showed rent had increased 4.5% from September 2023 to September 2024.

https://www.stuff.co.nz/money/350454120/renters-continue-suffer-despite…

Well done for shortening the term of your loan and thereby reducing the amount of interest you will pay! And yes, you make another good point about the rent rising over time.

And don't put your mortgage to the max because you want a boat or a new car.

"your calculations, whilst not wrong, are just good intentions and theoretical fluff. "

People are free to choose to dismiss the calculations, however people are not free to choose the consequences of their choice.

Let's take a look at "forced savings" by buying their own residential dwelling for a buyer in a low income neighbourhood - Manurewa in Auckland.

A) Peaker:

1) Nov 2021:

Median house price in Manurewa: $1,025,000

Purchase with 90% LVR mortgage: $922,500

Equity deposit:$102,500

2) Payments for 3 years to Nov 2024

1) Total P&I payments for 3 years: $133,108 (2.6% fixed interest rate for 3 years P&I payments of $44,369 per year)

2) Total payments for 3 years for rates, insurance, maintenance:$12,673 ($4,100 for first year, rising at 3% p.a)

Total payments over 3 years: $145,780 (note that the amount is likely to be higher to to the low equity risk premium interest rate to be charged which is not included above)

So over the 3 years, they have paid

1) equity deposit $102,500

2) total payments for 3 years: $145,780

Total payments of $248,280 since purchase

3) Situation at as Nov 2024:

a) Median house price in Manurewa: $792,672 (price fall of 23% over 3 years)

https://www.realestate.co.nz/insights/auckland/manukau-city/manurewa

b) Mortgage after "forced savings" of $64,145 due to P&I payments above: $858,355

c) Equity position: NEGATIVE $65,683 (i.e negative equity)

So the owner occupier buyer has paid a total of $248,280 over the last 3 years to have an asset with NEGATIVE $65,683.

That initial equity has evaporated as they were told to buy a house for "forced savings"

B) Buyer today

1) Nov 2021

a) Chooses to rent, pays $92,171 over 3 years ($28,392 in 2021 increasing by 8% per annum)

b) saves $0 (spends the surplus $53,609 as they are spenders - $145,780 paid by owner occupier buyer above less $92,171 in rent) - a financially disciplined household can save that surplus and invest it.

c) keeps 10% deposit in a bank account - $102,500 - earns no interest.

2) Nov 2024:

Equity position: $102,500

This can be used to buy a house at the current median house price in Manurewa of $792,672

90% LVR mortgage: $713,404

Equity position: $102,500

For buyer today, the mortgage is lower 22.6% (by $209,096) compared to Peaker. Peaker had an original mortgage of $922,500 (29% higher) vs Buyer today's mortgage of $713,404. Peaker will pay $455,717 over 30 years (at 6.0% p.a mortgage interest rate) for the larger mortgage, that Buyer Today will not have to pay. For a financially self disciplined household, they can take that $455,717 and invest for their retirement / financial future. Peaker does not have that choice available.

As a result of that single decision to purchase in Nov 2021, Peaker is in a more vulnerable financial position and at risk if they experience a fall in household income (job loss, fewer hours for wage earners). They may be unable to maintain mortgage payments and may face financial stress, and mental stress. If Peaker is forced to sell, then they are less likely to financially recover, they are likely to have lost their entire lifetime of savings, and they may need emergency housing, social housing or accommodation supplements in future.

So which position would people to choose to be in?

1) Peaker who was told to buy due to forced savings : equity position NEGATIVE $65,683

2) Buyer Today: equity position of $102,500

There are conditions where it is better to rent, and there are conditions where it is better to buy. The common widely held belief is that buy under ALL conditions. That is not the case.

Very few of these personal stories of Peakers in NZ are being reported in the media.

Here are some current stories being reported in another real estate market where there was a house price bubble.

These are likely to be similar to experiences of people who got caught out in previous house price bubbles around the world (Japan 1990's, Ireland 2006, US 2006, etc). Unfortunately there will be some who got caught out and will choose to self harm.

Examples of owner occupier collateral damage from falling house prices elsewhere around the world:

1) https://www.investorschronicle.co.uk/2012/09/20/your-money/property/ove…

2) https://youtu.be/iKPG_l1P7lk

3) https://youtu.be/ugBKnP2FKDM

4) https://youtu.be/fiCXsu_4BoA

People who fail to learn the lessons of history are doomed to repeat them. What we have learned is that people fail to learn the lessons of history.

The financially illiterate pay a high price for their financial illiteracy. People should get financially literate. People should learn and practice financial self discipline - if they choose not to, then they face the consequences of their choice.

Owner occupiers: CAVEAT EMPTOR. Do your own calculations for your own situation.

Okay, so are you suggesting that someone who held off buying in 2021 should buy today because it makes greater financial sense to buy today than 2021?

"are you suggesting that someone who held off buying in 2021 should buy today because it makes greater financial sense to buy today than 2021? "

There is no such general recommendation. Each geographical market is different, each household's circumstances and time frame are different.

The examples were provided to illustrate that there are conditions where it is better to buy and there are conditions where it is better to rent. The widely held and common belief that buying under ALL conditions is flawed - beware of those property promoters with vested financial interests and their repeated marketing messages.

The message is:

1) get financially disciplined

2) get financially literate

3) each household should do their own calculations that are specific for their own situation, and make a fully informed choice.

4) each household should ensure that they are able to continue debt service payments under ALL conditions (e.g rising interest rates, job loss, income reduction, rise in living costs such as having children)

5) owner occupiers should avoid purchasing when house price risks are extremely high in the geographical market that they wish to purchase.

6) beware of those motivated by their vested financial self interests - CAVEAT EMPTOR

The purchase of an owner occupier dwelling is the largest purchase of their household. The purchase price may represent 500% - 1000% of their entire net worth (and potentially lifetime savings). Under certain conditions, their entire life time of savings may be at risk.

"All points are valid and are often used by the vested interests to justify today's crazy prices."

Remember these reasons back in Nov 2021 as to why house prices won't crash? https://ndhadeliver.natlib.govt.nz/delivery/DeliveryManagerServlet?dps_pid=IE79655584

Notice how those with their vested financial self interests only provide a qualitative reasons on why they should buy, supported by historical house prices growing for a long time frame (e.g based on available price history perhaps the last 50-80 years). The key assumption is that house prices from current price levels will grow at the same historical rate. This led to the commonly repeated mantra by those with vested financial interests that house prices double every 10 years (7.2% growth p.a). From current house price levels, that house price growth assumption for the future may prove to be incorrect.

Each person should do their own calculations based on their own circumstances.

Owner occupier buyers: CAVEAT EMPTOR

Hi Yvil,

Your post above is highly worthwhile. It captures the key benefits of property ownership across the long-term:

i) Tangible [income and wealth], and

ii) Intangible [household security/stability, autonomy, pride of ownership and a host of other factors]. Unfortunately, the intangibles are frequently (and often deliberately) ignored here - despite frequently being the principal reason for a property purchase.

In the time I've been visiting this site, Yvil's timely contribution is probably the best I've come across.

TTP

We initially chose to rent so we had freedom of movement. When we wanted security of tenure, we went for fixed-term tenancies.

But, that doesn't necessarily make it the best choice for everyone, or even for us, for that matter. Even the 'freedom' to move is likely a false argument - and once we had kids, it actually became more difficult to move as a tenant, as it could take months to find a new rental (yes, it's illegal to discriminate against children, but it's very common and nigh unprovable - except in the case of the landlord who stupidly told me that was his reason in writing but I couldn't be bothered reporting him to the human rights commission).

Pride of ownership alone leads to far better mental health and a more enjoyable life. Just look at the renters on here they are rabid full of pent up anger that they’re stuck renting. I rented for 18 years felt stuck and absolutely hated it.

Well put, a good view that aligns with most FHB.

Funny how a "spruiker" actually supports the idea of people buying their first home more than most th dgm's.

Note the quotation marks around spruiker.

1. Mild gains once retail Interest rates are below 5%

2. Agree with Yvil’s comment

Hi toast, I'm expecting zero real CG for the next 5 years. Nor for perhaps 10, and quite likely even longer. (All bets are off if the RBNZ embarks on silliness again though.) My reasons are as I've posted previously re supply increases due to intensification, zoning, etc.

(1) is capital gains (above inflation) in residential housing over for the foreseeable future (5 years +) ?

(2) if the answer to (1) is yes, is it better to not own a house, put savings into a diversified fund, and rent ?

Need to compare the cost of renting vs buying.

Also need to consider:

A) Buying

1) other costs of ownership such as rates, insurance, maintenance (and cost increases over time)

B) Renting

1) the cost of renting (and increases over time)

2) the returns on the money invested that is not used in the purchase of the residential dwelling (e.g 20% deposit)

Each person will have their own unique circumstances and needs to do their own calculations.

There is more discussion on the rent vs buy choice in the comments section here

https://www.interest.co.nz/property/131123/home-ownership-rates-are-inc…

Another one bites the dust?

"Abeykoon is a customer of house building company JNJ Homes, which appears to have stopped operating, leaving several unfinished projects and tradies who say they’re tens of thousands out of pocket."

https://www.stuff.co.nz/nz-news/360508066/angry-home-owners-tradies-cha…

Well this weeks results seem rather similar to the preceding however many weeks, a market bouncing along the bottom with a few little blips up and down. Nothing to see here. And nothing to really suggest significant rises or falls anytime soon. In my view slightly more downside risk than upside in the short to medium term but nothing to get excited about.

And another one gone (reported 5 December), no tradies effected though because the land wasn't even bought but 52 buyers are owed their deposit for the failed Babich Road/Cassiny development in Auckland. Many agreements didn't have a clause protecting deposits so highlights the importance of good legal advice.

I will sleep better tonight knowing that Christchurch is doing okay. Or so they say!

Ex agent, there are building companies that go broke every year and there will be more.

I keep saying that you just can not build property now that gives a decent return if you are going to rent them out!

Hence existing property on good size sections are becoming more valuable.

Chch still has plenty lf building going on but in the New Year there will be more hurt for many.

The RB left rates too long and too high, but then they did say they wanted more unemployed

If CGT come into play - all good as long as interest stays tax deductible - and not ringfenced - it will remove specuvestors haha it might also put mom and dad investors off….. guess what - rental return will improve ? So yea go for it -

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.