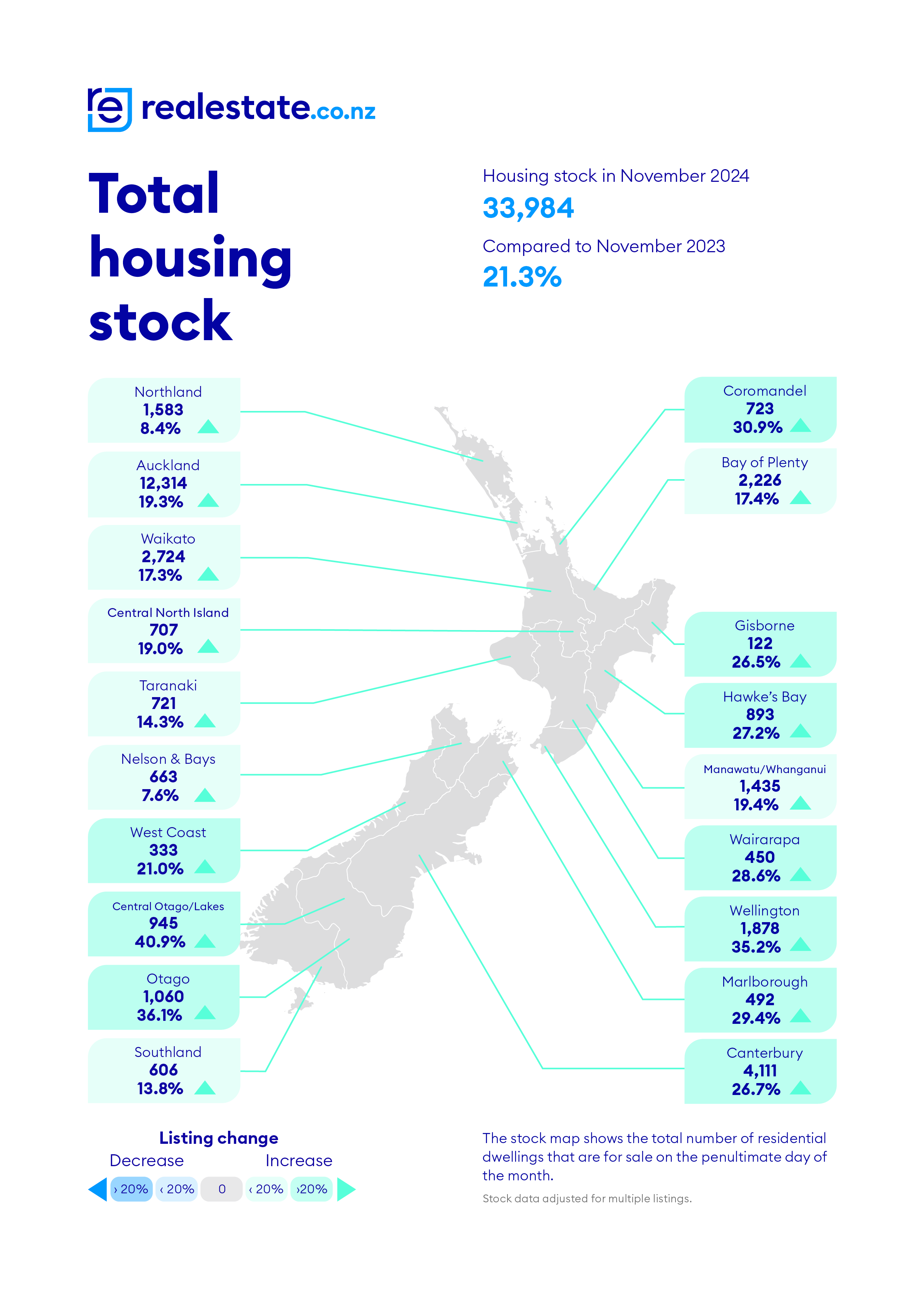

The sheer weight of housing stock for sale appears to be starting to push down prices, with vendors having to bite the bullet on price if they are wanting to achieve a sale.

Property website Realestate.co.nz reported having a whopping 33,984 residential properties available for sale at the end of November. That's up 21.3% compared to November last year, and was the most properties the website has had available for sale in any month of the year since April 2015.

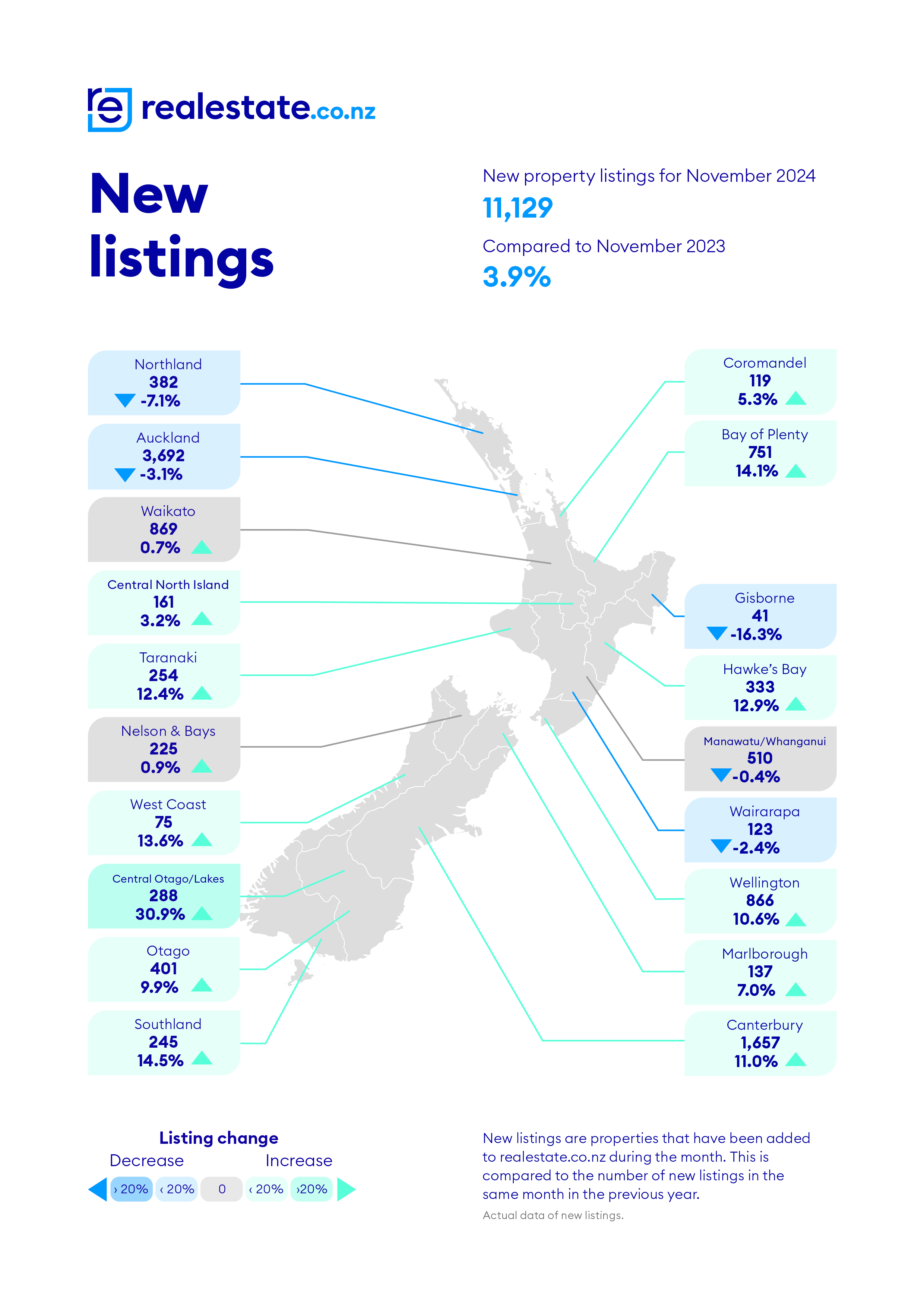

That was achieved even though the number of properties newly listed in the month of November was down 3.8% compared to October, and down 3.9% compared to November last year.

This suggests properties are taking longer to sell.

With the market now leaning so heavily in buyers' favour, it's probably no surprise the weight of properties for sale is starting to push prices down.

The national average non-seasonally adjusted asking price of the properties for sale on Realestate.co.nz was $863,503 in November, down $29,854 (-3.3%) compared to October.

That slide in asking prices was almost nationwide, with only Gisborne, Manawatu/Whanganui and Wairarapa bucking the trend and posting gains for the month.

That at least suggests vendors may be becoming more realistic in their price expectations and are adjusting asking prices downwards in order to achieve a sale in an extremely competitive market.

Buyers on the other hand, continue to be spoiled for choice.

The comment stream on this article is now closed.

106 Comments

Yesterday prices were up in a story (B&T) and today they are down. Hard to predict anything with the data coming through

Thats comparing asking price to price when sold (median). Would love to know how they source the asking price from vendors. If its only from vendors who have an actual asking price on their listing then the sample size must be small, especially in Auckland.

Advertisers have to specify a price to the platform in order to be put into the correct search engine range. This price is visible to the platform but not to viewers of the ad.

Lies, damned lies, and statistics.

We're all taught early on to be dilligent little consumers, and watch out for "up to" 50% off sales, or prices ending in 9s. But when it comes to things like property and politics, we're easily fooled.

Fools are an integral part of the food chain it appears https://www.stuff.co.nz/home-property/360504662/pm-christopher-luxon-se…

This one is about asking prices so is dominated by all the unsold shitboxes that no-one wants. Yesterday's article was actual sales, decent houses in decent neighbourhoods.

Anecdotally seems the case. Landlord mate has just sold his last they all went quickly. Moderish homes, good areas and he does the full makeover - new carpets etc, whatever it needs he does it. So yeah good stuff moving, but I'd pick the unsold lower c##p will eventually drive everything down.

Same in my area - nice family homes in the best school zone are selling for record prices. Tiny townhouses with no garages are piling up unsold, and even discounting the price is not moving them.

"tiny townhouses with no garages"

Sounds like every medium density 8 per section development here in Chch over the last few years.

And what happens when those tiny townhouses get discounted to the point where they become of interest to those currently competing for the nice family home..?

They don't, nobody that wants a decent home is interested in poxy shoeboxes in manurewa or whatever the local equiv is.

Nah they’re not. You’re probably mistaken or coping. The townhouse will drag down the value of the whole market.

lol no. That doesn’t make sense. Prices change at the margin.

You’ll find it better if you ignore every article post about property prices , with the exception of REINZ HPI. That’s the only one that matters, and anything else is just a waste of time.

Your comment is straight from the mouth of Spruiker Extraordinaire Tony Alexander. REINZ are the real estate industry. They have a vested interest in spinning prices to look better than they are - and that is what they do. REINZ said prices are up to Oct. Core Logic says prices down to Oct. Core Logic are not independent either - but more independent than REINZ.

And your comment is straight from the mouth of someone with perhaps limited mental capacity. The HPI is a stat, and considered the most accurate stat for house values as it factors in market composition on types of housing rather than medians and averages. The stat in itself is independent of any bias around it and doesn’t lie. You’re welcome to pick different entities to look at housing reports that align with your feelings better but everyone knows the REINZ HPI is the superior tool to use.

The HPI is an index there is no vested interest it’s an accurate index as it accounts for the mix. It’s well known to be the most and probably only accurate account of what the market is doing John from Bunnings is absolutely correct.

The REINZ HPI is based solely on the prices of properties that have successfully sold. This represents a minority of the overall property stock.

It does not account for the majority of properties that are listed but fail to sell.

I never said it doesn’t have its limitations. It’s still however the most accurate tool we have available in NZ.

Interesting, you're acknowledging the REINZ HPI has its limitations, yet still suggesting that everyone should ignore all other articles and data inputs to understand property prices?

Yes. Can you provide another tool that is a better measure for property prices, and if so, name which element makes it a better measure. Thanks I'll wait.

Well asking prices provide a broader view of the total property market because they include the majority of the properties (the ones that didn’t sell). Factoring both asking prices and HPI can help you understand supply-side dynamics and seller expectations.

At Bunnings, do you just sell one tool to get all jobs done?

Seller expectations are whatever they think they can juice out of the buyer. Obviously people are selling for the highest price possible, so there’s really not much to understand here. This makes asking prices an utterly useless metric, you’re wasting your time looking at asking prices. For something as volatile as house prices, what gets sold is the only way to know it’s true value, and the most accurate way to determine the value of other similar items using that information is utilizing a method that factors in as many things as you can, to avoid skewing of data as much as possible.

Sellers might aim high, but widespread drops in asking prices often signal shifting market conditions. Your comments suggest either strong cognitive dissonance or a vested interest in protecting a particular narrative.

“But widespread drops in asking prices often signal shifting market conditions”

and that information about “market conditions” is unable to be derived from the actual house price values themselves..? I think you need to verse yourself better on statistics then you may understand there’s no practical benefit to any other metrics other than cold hard figures mathematically derived, accounted for as many errors as possible.

Also what is with this vested interest/spruiker accusation for referring to the REINZ HPI? Earlier this year when the HPI was dropping monthly everyone unanimously agreed it was the gold standard for measuring house prices, but now because there’s a slight change in data all of a sudden people are spruikers for referring to it ? this site never fails to amuse me.

The problem isn’t the REINZ HPI - it’s that you’re telling people to completely ignore other data inputs while simultaneously admitting the HPI has its flaws.

Are you trying to understand future price direction, or are you only concerned with last month’s SOLD prices?

Is it because falling asking prices don’t align with your vested interests, or does it challenge your perceived reality of future price direction?

Wow !!! Handbags at ten paces.

You make perfect sense John, but you're wasting your time with TL.

You’ll only place you’ll find sober commentary on our property market, is from international sources. They’re all laughing at the dumb bogan country bidding up the biggest property bubble in the world.

Yesterday prices were up in a story (B&T) and today they are down. Hard to predict anything with the data coming through. [Mypointis]

It's a pretty safe prediction that interest rates will continue falling ......

And that's what's whipping the DGM into a frenzy. (Just read their comments.)

TTP

It's a pretty safe prediction that interest rates will continue falling ......

That would depend on which echo chambers you're flitting around TTP

Generally house prices rise quicker during inflation. There are two types of inflation affecting house prices: 1 price inflation 2 people inflation.

It seems both net immigration and prices are not rising, so it is unlikely house prices will rise quickly in the near to medium term.

What emergency measures can be taken to reinflate the ponzi? Oh, they’ve already been applied.😯

Looks like a redistribution of the population is happening, is there any data on this ?

Who would have thought?

You should try it sometime.

You're coming across as totally frustrated... You can still enjoy your home when it's falling in value.

Not at all. You just need a new hobby.

You're main hobby seems to be reading RP's posts..

You must be in love with RP

Lol, I hardly ever read his nonsense, because it is nonsense mostly.

You on the other hand follow him round like a lost puppy upvoting all his dribble. Perhaps you should try looking in the mirror?

Oh no..baby is crying again..

Grow up man

Lol, again, look in the mirror

Well I'm a pretty casual user of this site, and of the 3 articles I've read over the last couple of days, you've been under his comments on each one, and stood out as being particularly emotional..

That would be very long odds indeed. A quick scroll through the last few days posts of the front page and I didn't see many posts from RP at all, and not a single one i'd responded to.

Bit of a contradictory post there Pragmatist.

Property vampires sucking out all disposable income from tenants are unable to reflect.

You're wrong, DGM, in your comment above .......

RP's in love with himself.

TTP

Tim, you and the housing market share a lot in common. You have episodes of frothing, people often come away feeling disillusioned, you're rather top heavy and right now there are plenty off you. Also, you regard your services as essential but in reality, they're still grossly over priced.

This is a sign that house prices are well on their way up.

-Zwifter

The low clearance rates are just adding to the misery of unsold homes..

Prices up in 2125..

Exactly. That's a lot of unsold stock. Over 4k in Canterbury, nearly 2k in Wellington - yikes!

Centrix reported very low levels of mortgage arrears yesterday. However, around 12% of the eligible population had fallen behind on their consumer credit repayments last month. Business liquidations are also at an all-time high with plenty more expected to come.

In this situation, cash is king!

If you own an ok house in a good school zone. Easy sale for a good price.

Else you are in for a wait and a low price.

Issue seems to be that there are fewer cashed up wealthy middle aged families and more low skilled poor peeps.

My pick is that in the near future the nicer communities will increasingly be gated and have security. The rest will be working for, and stealing from ..the wealthy. Lol

Auction clearance rates are close to their highest point for three years, DGM.

TTP

So:

- not even at their highest for the last 3 years

- The last 3 years have been absolute dogshit clearance rates

Tim the Crim, a relentless turd-polisher extraordinaire.

There's never been a better time to be a buyer & seller...

Vanessa Williams, spokesperson for realestate.co.nz, said it was “the perfect market.”

“After 18 years of tracking the property market, this is one of those rare moments where certainty and opportunity align, creating a true ‘Goldilocks’ market that benefits buyers and sellers.”

https://www.stuff.co.nz/home-property/360506754/falling-interest-rates-…

Lol.. you should be her PA

Cool... might be some cleaning jobs going for you in their office.

I don’t kiss arses like you do

Her customers just need listings at prices people can afford to eat and live. What else would she say?

Property people clearly using an AI search along the lines of:

'Write me some sentences that talk up the market as being in perfect equilibrium with prices rising, while the reality is the opposite with dropping prices and rising stock levels'.

Actually I decided to enter that into ChatGPT and got:

"In a flawless demonstration of market equilibrium, we see prices climbing, signaling a thriving economy, even as stock levels climb higher, signaling an oversupply that's actually driving prices lower."

So the rule of supply and demand applies.

End of the day the banks are still restricting access to credit vs the bonus driven lolly scramble of the last ten years. Add in rising rate and insurance, and future tax payer continuing to vote west, it's no surprise.

Greed is great in a sellers market. In a buyers market it is just delusional.

Banks are clearly hawkish on rate cuts at this moment and don't share the same beliefs as many "property economists" who insist RBNZ will cut OCR to the floor to restart the Ponzi.

The US economy posted a record number of job openings, so the Fed rate cut path is also going to be gradual.

Do you think that sickly GDP growth and rising unemployment will be tolerated by the powers that be, especially when the CPI is well within target band (and most domestic inflation that does exist is not influenced by the OCR)?

As B. Clinton said ‘it’s about the economy, stupid’

That was his advisor James Carville that said that.

This was literally an article yesterday saying the opposite:

The Reserve Bank's forecasts for the Official Cash Rate are "too high and too hawkish", according to Kiwibank's chief economist Jarrod Kerr.

Kerr says because of the the RBNZ's forecast OCR track there are not enough cuts being priced in by wholesale interest rate markets.

"We believe the RBNZ will be forced to lower their track (again), and deliver faster cuts," Kerr said.

https://www.interest.co.nz/economy/131057/kiwibank-chief-economist-jarr…

If only we had Polymarket for NZ resi RE. We could all bet how much something will sell for, provide a valuable market signal while doing so and make money on the way up and down. Why does this not exist?

Great idea.

Edit, Come to think of it, it wouldn't work, because no one would ever put any money on house prices going down, because these people are typically too scared to put their money on anything.

With such bloated inventory, all that Agent commission seems so close, yet is so out of reach...

Bloating...sounds like an issue a retired DGM would have.

🤣😂 Who are you referring to? We both work full time.

Retired-Poppy says he works full-time.

Stay tuned for more of his bloated nonsense.

TTP

Tim, step away from the keyboard. You're just embarrassing yourself 😂🤣

Maybe he considers himself commenting on interest.co.nz a full time job...

Still waiting Nifty ( ) All this inventory with nowhere to go....

Prices are increasing, more investors are in the market, rates are predicted to drop further, bank test rates are dropping- lending getting more affordable. All playing out as expected...

You're entitled to your own "reality" to what constitutes a sustainable recovery......

A reflection of my name is the current state of the market...

When prices are back in balance, the market will resume traction, until then it's a dead man walking

New name suggestion: Dreamer.

The salty tears of spruikers make me feel there is hope for New Zealand. Keep em coming.

Better to be a Dreamer than an unscrupulous bloke like Niffy is

Much will depend on how long Auckland investors can tolerate poor yields / top ups . Not sure even bargain prices would be enough to tempt Auckland investors into expanding . Could be a very long wait for those magical offsetting CG's to surface...If Auckland does reflect the true face of RE in NZ the larger economy will have to significantly move up before anything remarkable happens to RE. The idea that cheap lending rates will fire up an RE frenzy appears somewhat far fetched given the dismal current economy. First home buyers need to be careful they dont end up getting sucker punched by those looking to dump their problems onto others... my 10 cents

The truth of this price 'adjustment' trend has not yet gone full mainstream. Most don't follow property closely and are oblivious.

The big drops will come when the masses believe houses will be cheaper tomorrow and decide to wait.

We haven't got to this point yet.

"The truth of this price 'adjustment' trend has not yet gone full mainstream. Most don't follow property closely and are oblivious. "

In Auckland, it will be interesting to watch the impact on house price growth expectations of the general public when the updated council valuations are released.

When Aucklanders get their new CVs there will be tears.

From the analysis I'm doing, it appears the $2m+ bracket is becoming slightly - ever so slightly - more 'lively', i.e. CAGRs are a tad better than they were but still nowhere near 'doubles every 10 years'.

on a bright side, the dropping property price and increasing income level will makes the property market healthier down the track.

My observations on Queenstown listings rocketing were correct. I think you can rule out any capital growth there for a while.

Might it turn out there is a connection between low airfares and Queenstown/Wanaka house prices etc?

Luxon sells third property in 2024 here

The writings on the wall - CGT

Well if he doesn't introduce one Labour seems to be interested in the idea.

Labour will probably introduce one at the next election. It might even seem reasonable at the time. However, I can almost guarantee that any coalition agreement with the Greens and TPM will turn a reasonable CGT into a punitive wealth confiscation tax. What you think you are voting for will be very different from what they deliver.

Scaremongering based on vibes and pre-conceived prejudices.

So if property prices keep going down we will get tax write-offs against the public purse? Great!

I think removing interest deductibility was a better measure - at least in terms of effectiveness.

An even better measure would be to ban interest-only mortgages entirely. Though I can't imagine there's too many of those while future house prices gains are off the table and yields are low.

"An even better measure would be to ban interest-only mortgages entirely. Though I can't imagine there's too many of those while future house prices gains are off the table and yields are low."

Percentage of loans on interest only (Oct 2024)

1) owner occupiers: 7.4% ($20.4bn)

2) non owner occupiers: 33.5% ($30.9bn)

3) business: 37.6% ($46.8 bn) - some of this may have gone into non owner occupied residential property

Another case of mortgage fraud coming to light - borrower and mortgage adviser gaming the system. The borrower gets the finance to purchase the non owner occupied property and the mortgage broker gets their commission.

Borrower pursues claim against mortgage adviser when property deal incurs losses. If the property deal had been profitable it is likely that the claim by the borrower would not have been made.

The lender told the adviser it would approve the loan if the couple could show they had savings or cash of $100,000.

The couple told Financial Services Complaints Ltd (FSCL), an ombudsman service for financial services providers, that the adviser helped them to borrow $100,000 from another lender as a personal loan.

They said the adviser told them to get a family member to sign a gift certificate saying he would gift them $100,000.

They complained to FSCL that the adviser had come up with the "deception plan" and led them to believe it was not uncommon. But FSCL said the evidence showed that the adviser came up with the plan and knew the couple were borrowing the $100,000.

"Although the adviser said that he was not seeing emails in his inbox while he was overseas, it was clear he had seen some emails because he personally replied to them. This raised doubt about the adviser saying he had not seen emails about the $100,000 loan being for [the couple] not [the woman's father]."

"The adviser's staff clearly knew that [the couple] were simultaneously borrowing a further $100,000, and getting a gift certificate signed. The fact they did not raise this with the adviser suggested he knew about the deception plan."

But FSCL said the buyers were not "unsavvy" and they decided to continue with the plan knowing it was wrong.

"We also took into account that [they] must have deceived the third-party lender about the purpose of the $100,000 loan."

FSCL said it was fair that the couple and the adviser should bear half of the losses each.

It said the couple lost $164,000 including loss in the value of the investment property, less 15 percent to account for market forces outside the adviser's control, the interest they paid and the losses from the cost of buying and selling the property such as a builder's report and real estate agent fees.

https://www.rnz.co.nz/news/business/535422/mortgage-adviser-told-to-pay…

If Nats lead a CGT then the left would have to support Nat's in the house on a Nat's policy. That would be comical and probably eliminate any chance of the left regaining power.

There are plenty of implementation choices for CGT still to argue over

And he lowers bright line just before selling up his stock…labour should be all over this.

100% we are getting capital gains tax. National will probably bring in, at terms end to knock labour off.

"Vendor in tears, crowds gasping in disbelief - the auction that just went on and on"

https://www.oneroof.co.nz/news/vendor-in-tears-crowds-gasping-in-disbel…

I was not in the room, but I reckon its a 100% certainty that was two Asian bidders going head to head. That's what happens when neither wants to "lose face".

Seen it too many times before:

563 Borman Road, Flagstaff, Hamilton City - For Sale - realestate.co.nz

Sold for 305k over CV in 2022, been on the market for 6 months through 2 different agencies, would be hard to even get 100k under CV today or ~400k less than paid.

.

Record levels of copium being purchased in the CBD areas of all major towns and cities. With the biggest concentration of purchases happening within 50m of real estate offices.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.