There was a big jump in residential auction activity over the week of 16-22 November, with interest.co.nz monitoring the auctions of 517 properties around the country.

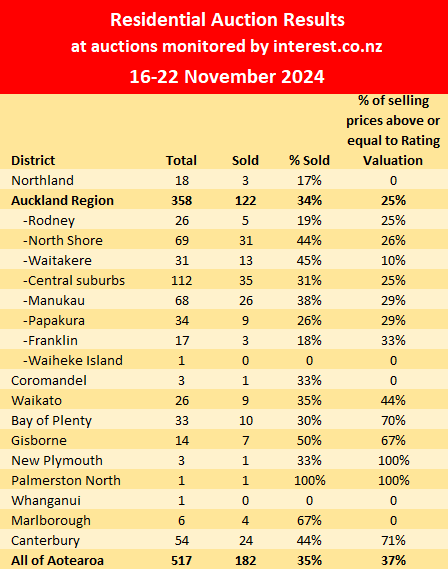

That was up 14% compared to the previous week, and was the first time the number of properties on offer has exceeded 500 since the summer peak in mid-late March.

However, the increase in the number of properties going under the hammer was not matched by the number of properties being sold under the hammer, which increased from 175 to 182.

That pushed the overall sales rate down to 35% from 39% the previous week.

It was also the fourth week in a row the sales rate has declined since it peaked at 44% at the end of October.

The higher number of properties being offered and the lower sales rate reflects the overall market, which is overstocked, meaning buyers can be choosey and strike a hard bargain on price.

Details of the individual properties offered at all of the auctions monitored by interest.co.nz, including the selling prices of those that sold, are available on our Residential Auction Results page.

The comment stream on this story is now closed.

You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

136 Comments

It’s a roller coaster out there….happy that NZ inc have finally started building more homes. Waitākere is still doing well -

So the hot, summer siźling, market peak was last month in October.......well that's spring......the NZ HOUSING MARKET IS ENTERING THE NEXT LOWER STEP OF ITS OWN, CHINESE STYLE, GARBAGE TIME.

For this supposed housing market recovery to have 1/3 sold by the REA SPRUIKED hammer throwdown.......and a measerly 10% or so matching CV...... the NZ MARKET IS DEAD AS A MOA.

The pricing expectation will need to adjust downwards in a BIG way to clear this overburden and glut of flood prone town houses and stale dated boomer, retirement funding pads.

The California dreamin, green shoots asmokin, high prices asked, in many cases is so far out on a spindly tree limb, the only way these will sell, is when a Berry fattened and drunk Wood Pigeon makes an ill fated landing and breaks the mofo to the ground........

Call that real world, Pigeon housing economics!

@nz gecko - morning and good to have you back as always enjoy your messages - they crack me up - wood pigeon comment is your best work yet -

The housing market is in the dumps.. anyone wanting to pick up one needs to have prior training in garbage collection

@ nz gecko - interest.com should make a glossary with all you wise cracks and turn it into a book for the coffee table - I definitely would buy it 😀

Good to be back SAH.

Trust your holding on ok? and have other investments/jobs that are keeping the ever hungry wolves from door?

Good idea! I could use the funds from a forth job, helping the good Interst Team with a few moments of Geckofun. Whoever said Geckos were boring, slothlike, fly gorging, tree freeloading creatures?

I'm back just to wish TTP well, in his latest, in vain, spruikerthon, trying to reanimate the housing ponzi, that's in its late stages death rattle.

@NZGeko - I am doing Ok - yes having a job is certainly a good thing- will do allot better when interest drops to 5% whole sale - its been a rough 4 years - however my feet are taped to the property investment bike - its not been easy - however everything considered i would still have done it. However anyone who enters the world of property investment get good advice (it is possible to make money) - its not easy. GEKOFUN love it (4th job) where do you get all this stuff. Go well and do me a favour give us old spruikers a rest over the Xmas period hahahah

"yes having a job is certainly a good thing- will do allot better when interest drops to 5% whole sale - its been a rough 4 years - however my feet are taped to the property investment bike - its not been easy - however everything considered i would still have done it. However anyone who enters the world of property investment get good advice (it is possible to make money) - its not easy"

Thank you for sharing your experience. In order to sell their services or products due to their vested financial self interests, property promoters highlight the upside and benefits and frequently omit or understate the potential risks and difficulties.

Is there anything you wish you had done or had known 4 years ago?

I would say - read rich dad poor dad the principles worked for me - don’t get leveraged more than 50% also know that governments can change and rules change with them - do interest rates at 7% and make sure you run your sums without interest tax deductibility to ensure you stay afloat - final rule make sure you never have to top up more than 60% of your income to keep properties topped up I think you can survive a couple of years on 60% ideal in less than 40% ….. pay down debt when times are good

Thank you for sharing that.

Many people won’t learn the lessons that you've shared and they will learn the same lessons the hard way. That is entirely their choice. People are free to choose, however they are not free to choose the consequences of their choice.

Each new wave of highly leveraged investors learn the same lessons learned by previous generations.

https://www.oneroof.co.nz/news/s-we-cant-afford-this-homeowners-fear-th…

https://www.nzherald.co.nz/property/mortgagee-sales-customers-revolt/G5…

Predictably, the DGM have become over-anxious - and are frantically trying to talk down the housing market. (See their outbursts below and above.)

Nobody should take any notice of the DGM...... Remember, they go to bed at night and dream of their future ownership of an avocado.

TTP

Problem is most his comments are just variants of the same thing. Despite the number of comments he makes, you could summarize into a single laminated A6 sheet.

Fair go NZD......I speck from a Geckos perspective and it is really varying.

The dominant overlords of my forest patch, need to reign in their speculation and excesses.

You can only charge so much for a tree perch and the inflation adjusted cost of forest living is high. The lovely jubly, tasty flies and forest bugs, has me watching my dietary intake at the leaf litter shop checkout.

Laminated, that's quite subtle NZdan. I suspect that went over NZGeckos head.

I'm just a humble Gecko.

I'm nothing, compared to the intelligencer on roids, master spruiker, overlord class of Zwiffy.....

Let's refrain from poking holes in our precious NZ wildlife and get back onto your favorite topics of the awfully bad selling results of the NZ housing Ponzi:)

This market overhang and heavily pregnant list of properties for sale, is but a beleaguered Dam, waiting for the expendable souls to venture close enough, to trip it and send it crashing into the valley, far below.

NZ Dan could well have been making a comment about his own commentaries!

Good on you Gecko! Nice to see a commenter with no ego.

Very true. Mine would likely consist of how retirees in high paying jobs shouldn't receive Super, but I think my comments are a little more broad than Geckos so could do it on an A4.

Anyway, was just a light hearted bit of jest, I'm sure Gecko's doing just fine and didn't need you to white knight.

Went to an auction to support first home buyers.

Talk about full bore pressure. They were successful. At every turn the agents were pressuring to increase the offer. We helped them get it under RV in line with recent area sales. Not easy.

FHBers are being penalised. This market is unsustainable. It’s out of balance.

There should be some duty of care in the industry.

Their hunger for dollars is harming future generations.

Remember the agent works for the seller not the buyer ,when we all sell we want the best price in whatever market you are selling in.its call capitalism which seems the only system that works even thou it isn't perfect but effective.

@timutei - I think the world need more people like you - I think when wealth tax kick in and CGT - more first home buyers will need your skills

Greed mate Greed.. both from agents and speculators...

Hopefully this time around they will get burnt

Solution is - don't buy at an auction. Take your time, look around at some houses with a price tag, and make a reasonable offer. Auctioneers pump up the buying temperature- they always have done and they always will. If you really want to see crazy stuff, go and attend an art auction " do I hear $100 million for the Monet?"

Personal experience is best to buy at Auction!

often no competition and motivated vendors is recipe for buying right with upside.

Auction works best for me. If you are already cashed up you simply put a maximum price on what you are prepared to pay. Its cuts out all the bullshit and it shows what the market is prepared to pay. The vendors get motivated to sell when the price doesn't meet expectations. I clipped the next highest bidder by $50K, they could see the market wasn't going to pay anything higher.

"I clipped the next highest bidder by $50K, they could see the market wasn't going to pay anything higher."

When you're at an auction and know what the last bid was why would you bid $50k more? You may have paid $49k more than you needed to for the property.

"When you're at an auction and know what the last bid was why would you bid $50k more?"

To meet the vendor's auction reserve price?

For those don't realise, an additional $50,000 financed by a 30 year mortgage at 6.0% is a total amount paid over 30 years of $108,973.

Paid cash

I met the reserve and the reserve just happened to be what I considered the house to be worth. I got sick of looking at places well over $1million that were not as good in my opinion so I ended up spending way less for something better, pretty rare when I start looking at other types of purchases.

Spot the agent.

As expected, this top heavy market, at best, is going nowhere. It appears the presence of a sustainable floor to clear the bloated inventory is proving elusive. With joblessness still rising, it's entirely understandable the diehard Spruikers are now anxious about where prices are headed next winter. or worse, post some random global shock. It always was simplistic to believe that cheaper money alone would repair the market in a jiffy. With the backdrop of a skyrocketing cost of living, upward momentum is lost, there is little to fuel it and despite falls to date, prices remain unaffordable.

As expected.

Didn't you expect a great big crash this year?

So now the "expectation" is that house prices won't shoot to the stratosphere anytime soon. That's kind of an easy one, because very few people expected that.

Until we resolve new housing supply, housing affordability is going to be a constant issue. While the populace gravitates towards division and Boogeymen (spruikers/landlords, boomers, the supermarkets, employers), the masses will gather no meaningful progress.

@painter - great comment

Much compared to the 70s, adjusted for inflation, it can be argued that prices have crashed. Weren't you the one that said quote "FHB's have a Death Star" trench opportunity to conquer the housing market? Yes, I recall it was....

Cue more reckons...

Great comment safeashouses😂🤣

Much compared to the 70s, adjusted for inflation, it can be argued that prices have crashed.

Is this in line with your prophesies of 2023 and early 2024? And has the rising inflation negated the subdued pricing for home owners, or prospective buyers (i.e. have rising CPI prices killed off any real savings?)?

"FHB's have a Death Star" trench opportunity to conquer the housing market? Yes, I recall it was....

And that's exactly what it's turning out to be. A small sliver in time where prices, interest rates, and employment market health offer greater than typical conditions in FHBs favour.

As opposed to the paradigm shifting Perma crash being promoted on here.

You've obviously spent several restless nights putting all that together - well done 😂

You're giving too much credit to the energy required to dispell much of your claims.

I think you've become consumed. You could have easily read my post, or not, then simply moved on.....😂🤣

One of us is definitely consumed. Years of the same theme, with an ever changing interpretation as old punts are dispelled.

@ painter - you are on fire 🔥 today - good work

😂🤣😆

Retired-Poppy can't let it go .....

He's a victim of his own narcissism - and the obsessional behaviour that's part of it.

Watch - he'll be back again soon.

TTP

Waylon Smithers vibes.

"Until we resolve new housing supply, housing affordability is going to be a constant issue. "

The listings for sale and inventories are at high levels.

1) Why are auction clearance rates low relative to historical levels?

2) Why are they taking longer to sell?

Because access to credit is constrained, and the economy is sick.

Your questions don't address my words you quoted. Interest rates and markets fluctuate, but the core problem is that house prices, particularly for existed stock, are dictated by the cost to produce new housing, and how much there is of it being produced.

" the core problem is that house prices, particularly for existed stock, are dictated by the cost to produce new housing, and how much there is of it being produced."

So the cost of production / construction puts a floor on prices in the existing residential dwelling market?

Is my understanding correct? (of your point above)

Assuming there's demand, yeah.

If there were eventually no buyers, so somewhere like inner Detroit, then it's moot as new or old houses aren't worth anything.

But if there's buyers, and a fairly mediocre new house on a postage stamp is a million bucks, the demand for an older place, is probably pretty high.

Conversely, if the new house cost $350k, then the old house is unlikely to fetch more than that, like for like (i.e. same location, size, and house size).

"Assuming there's demand"

That assumption is the essential condition required.

If someone wants to make a case that demand has disappeared indefinitely they're welcome to.

In the meantime, many less new houses will be built over the coming years, given the *current* conditions.

If things are going to be bad forever then we've got a lot more to worry about than buying houses.

"If someone wants to make a case that demand has disappeared indefinitely they're welcome to"

Was merely reminding people of first principles and underlying assumption being made implicitly by most people.

Demand differs depending upon geographical location.

Demand will very likely recover in the big cities.

Some smaller towns might see a structural decline in demand for housing. Here are some examples:

1) https://www.rnz.co.nz/news/business/526432/people-already-moving-out-of…

2) https://www.rnz.co.nz/news/business/533227/the-most-exposed-towns-the-a…

Also areas where insurers refuse insurance and insurance is unavailable or where insurance premiums are high.

https://www.nzherald.co.nz/nz/maps-reveal-nzs-hot-spots-for-extreme-coa…

If there is a large earthquake, then that might also decrease demand for housing in the affected areas if there is no rebuild.

"In the meantime, many less new houses will be built over the coming years, given the *current* conditions."

Why will less new houses be built over the coming years, given the *current* conditions? Is it because house prices are selling below current construction cost?

I agree with Painter. And it’s largely because of the cost of construction.

It also doesn’t help when Auckland Council is increasing the development contribution charge to 100k per dwelling, or more, in some large areas of Auckland flagged for new development and intensification.

If / when the OCR is cut to below 2% we are likely to see another little building boom. But not nearly as big as the recent one.

"And it’s largely because of the cost of construction."

Just want to confirm that my understanding is correct.

There will be less new houses built in some geographical markets (e.g Auckland) over the coming years as the current house prices are selling below construction cost?

Yes, that’s a significant part of it.

Where I live, several of the townhouses (4 years old) have sold for around 100k less than what the very same townhouses would cost to deliver to market today as new builds.

"Where I live, several of the townhouses (4 years old) have sold for around 100k less than what the very same townhouses would cost to deliver to market today as new builds."

Thank you for sharing that.

So it seems that the commonly held belief and frequently repeated conventional notion:

1) that house prices do not sell below current construction cost

2) that current construction costs is a floor for house prices

is incorrect.

Exactly

And to add - this is a massive conundrum. Many / most developers will need price signals that existing house prices are rising significantly before they embark on projects in earnest. It’s no coincidence that the biggest building booms since 2000 have occurred during house price booms. So you actually need to see house prices increasing significantly- ie. getting less affordable - to see meaningful upticks in supply, to ‘theoretically’ address ‘affordability’. It’s one of several reasons why supply side theories are flawed.

Housing affordability in the ownership market can be improved in 3 ways:

1) falling house prices in the existing residential dwelling market - more inventory and listings for sale vs active buyers

2) increasing household incomes

3) changes in debt to income ratios

Most likely some combination of all 3.

So you are also a supply skeptic?

I am only a partial supply skeptic. I think large increases in supply can moderate rental inflation, and also house price inflation - but only up to a point.

"So you are also a supply skeptic?"

I don't know how that is defined, or your definition of the term "supply skeptic"

The demand and supply dynamics of the existing ownership market and rental market differ.

For example, some market observations:

1) non owner occupier property owners can increase supply of houses for sale to the existing dwelling ownership market (leading to lower prices in the ownership market), whilst at the same time they're decreasing supply to the private rental market (leading to higher rental prices) - this is what happened when the previous policy of interest deductibility being removed was being phased in

2) non owner occupier property owners can increase demand in the existing dwelling ownership market (higher prices in the ownership market) whilst at the same time increasing supply to the private rental market (leading to lower rental prices) - this is what is starting to happen with the current policy of interest deductibility being re-introduced. Seeing indications of some non owner occupier property owners focused on capital gains and willing to go into negative cashflow re-enter the existing dwelling market.

‘Supply Skeptic’ = someone who is skeptical that significantly increasing new build housing supply will make a meaningful difference to the cost of housing.

’supply skepticism’ is a minority, but solid, position within the economics community. Dr Cameron Murray, in Australia, is probably the most prominent supply skeptic in Australasia.

I am not convinced by his viewpoint. Neither am I convinced by the dominant position. I think the truth lies somewhere between the two positions.

note - despite what it might seem, none of the above was written with any reference to AI!

Thank you for sharing that definition.

Here is a thought experiment for people to think about - imagine if mortgage interest rates unexpectedly rose to 17% - 20% p.a like in the late 1980's and there were no new dwellings constructed as house prices in the existing dwelling ownership market were well below construction cost.

What would be the likely outcome of the prices of houses in the existing dwelling ownership market?

Undoubtedly a crash. Although there might be mitigation through people not moving as much?

Unemployment would skyrocket, which would force many people to move, though.

Crash - no brainer!

Edit - perhaps more complicated than what I have outlined. If interest rates were that high then wage inflation might be very high too. So perhaps a crash in real terms, but not nominal. Like 1970s/ 1980s

RFNS.. (Regret For Not Selling) will kick in by next winter..

RFNSHP (Regret for not seeking a house to purchase) will kick in by May

You missed a'T'... so you know you're absolutely wrong..

The problem with these predictions 6 months out is that we will both have forgotten about them by then. So here's one for now. October was the bottom of the market, and when Novembers numbers (for house prices) comes out, we will see rises across nearly all regions of New Zealand.

"the bloated inventory"

FYI, current number of properties listed for sale on trademe:

A) Residential property

1) total listings for sale in NZ - 52,960

2) new homes listed for sale - 7,035

B) Commercial properties listed for sale - 27,567

Don't worry, Orr is on his way...

Are you sure on the Orr?

Or will he lash out at the burgeoning inflation expectations and permutations and hole your already wet bilged waka?

Hope he does not have you paddling up the lonely landlords shist creek?

@Nifty - or is on his way i would agree - and believe it of nor its not my vested interest that make me say this - manufacturing is suffering layoffs up to 25% of staff - mills into liqudation - pie shops shutting down - 0.75 is the only way to give people some sort of hope to keep the doors open and keeping Kiwis in NZ

Agree about the grim business climate in NZ.

All but a few industries will be downsizing, I fear.

Now the humanity of it!! A great pie shop is closing down in NZ (in the land full of pie worshipers!)

This is the dead canary, that all thought would be ironclad. This should have us all worried!!

But if the ORR gets stuck into big rate cuts.......inflation will just zoom up, as all imports/energy prices rage higher.

Let's pray he knows what Golden Veined Creek to paddle the junkstyle NZ rusty trawler up?????

I see the easy get gold, so to speak, is already got within NZ.......so no easy way out of the economic Dodge city doldrums...... without taking a few bullets.

But if the ORR gets stuck into big rate cuts.......inflation will just zoom up

Is that what happened when rates were dropped and kept dropping through the 2010s?

The NZ economy was crawling through the mined ground and barbwire of the economic collapse, post GFC, IN THE EARLY 2010S!

Some seem to have learned very little from their excessive greed, binging, AND HOUSING SPECKU-SRUIKULATION leading upto the 2008 GFC.

So, some of us humans...... repeat the same stupid!

Most of us repeat the same stupid.

Hammering out endless, caps riddled, thunderbolts and lightning posts.

Or trying to reason with the above.

The fact you have to yell all the time would say you have anger. Why do you feel the need to constantly use capitals?

Peace and love only from Geckos. Relax Pointybits.

Lets resort to some extreme metaphors and accusations of making anger laced posts. Yeah that'll work.....

@ painter - another good comment I bought a house in 2011 interest rates was 3.99 inflation was under control and everything was babbling along (exodus of kiwis to AU) till about 2014/2015 when NZ hit rock star - there is similarities - time heals all

Winding down now for Christmas, you really wouldn't want to be trying to push the legal stuff through before years end, its stressful enough as it is. Big OCR announcement on Wednesday this week, its going to be critical for sentiment going forward over summer.

@zwifter right you are …… 0.75 …. For the love of pies and for everyone who still has a job

The Pies are Toast. Sad.

This economy needs retail mortgage rates of 3.5% to have any dead ponzi/commercial business resuscitation success.

Soz.....not happening soon or soon enough.

Agree re 3.5% ( I would say 4%) I find it surprising that no economists seem to be saying that is what is needed for resuscitation. Most seem to be thinking 5% will be enough

No I think that it will go down another 50bps, anything more is a bit of a sign of panic to be honest. My TD is coming out at midnight, will be up locking it away for 6 months ASAP.

why do you hold TDs when you could be getting great interest rates at fisher, Milford or Jarden funds?

Seems a bit crazy to want to speculate on housing but be safe with cash funds in TDs?

I'm not speculating on housing. I just don't get the fact that everyone who owns a house is somehow a speculator on here. I'm not interested in making more and more money, I don't need it. I can run the whole show on an oily rag and still enjoy it. I realise that I am quite unusual but that's the way I roll.

I just don't get the fact that everyone who owns a house is somehow a speculator on here

Now that gem of a post says more about you than anyone else on here Zwifter. Perhaps it's paranoia or it might even have something to do with what you post rather than your asset.

Home prices are down 20% from their peak, and the NZD has dropped 20% against the USD since November 2021, sliding from 0.71 to 0.58. It’s proving to be a poor store of value relative to the USD, and the crash isn’t over yet.

I would say the crash is just starting..

So you hope all the FHBs will loose badly and go into default and investers will sit on the sidelines and buy up all these homes when they come up for mortgagee sale? I am hoping for their sake that prices remain stable for their sake.

You're pointless..

You mean For your very own sake!!

@dgm I think most people do what’s good for them and their family what’s left over they do good for their community - what do you do that is do enlightening ? Except sounding like misery that needs a friend

what’s left over they do good for their community

Are you serious?!?!??? You think people use their wealth to help others after they have satisfied their basic needs?!??!? Are you taking the piss?!?!??

If that were the case we would not need a government, public services, police or taxation. We have to organise ourselves with governments, bureaucracies, laws, taxes and law enforcement that try to reflect our social norms to make sure society doesn't collapse.

You think the super rich are happily spending the 98% of their wealth that they do not need to meet their basic needs (plus some) helping community? They are not. They are using it to hoover up an ever increasing piece of the pie.

Unless we put rules in place to literally stop wealthy and powerful people hoovering up the fruits of society's labour that's all they would do.

I mentioned yesterday that my 25 year old nephew is looking to buy a studio apartment in Stockholm. The one below is one he’s interested in. About NZ250K. And interest rates are sub 4% there.

We really hate our young people in NZ, don’t we?

https://www.svenskfast.se/bostadsratt/stockholm/stockholm/skarholmen/sa…

It's quite a way out from the center. Freehold? (edit: yes) Just 34 m2. A bit cheaper than central Auckland where most similar sized apartments are. Body corp $6,654 / year.

What's a comparably sized apartment going for on the outskirts of Auckland?

That would be at least 450-500K in non central Auckland

It’s only about 10km from the city centre

That's smaller than my internal double garage. Would I want to spend $250k on just my garage ?

It looks tidy and pleasant to me. Plenty of natural light, a good sized balcony. For a young single person or couple, why not?

Well it works in you 20's and 30's I guess, why not.

Exactly, and that’s the point. Of course, there are plenty of single people in their 30s or much older who it could also work for as well.

Unfortunately, construction costs are way too high to deliver this in little old NZ for 250k. Would be doing very well to deliver it in the late 300’s

Why not, I mean some idiot just paid 10 million for a banana taped to the wall and people on here complain about house prices.

Kudos. It's hard to beat someone who just made a delicious $10m selling a banana to someone who thought it small change. It would have been more appropriate had the proceeds gone to a worthy charity.

Anyway, this sort of overexuberance serves as a timely warning of what's coming.

"I mean some idiot just paid 10 million for a banana taped to the wall "

So based on the most recent comparable market transaction, the valuation is $10 million for the next banana taped to the wall?

Is it a bargain, if the next banana taped to the wall is offered for sale at a price of $5 million? (i.e a whopping 50% discount to the most recent comparable market transaction)

Note:

1) the market for banana's taped to the wall is very illiquid

2) can we replace "banana taped to the wall" with real estate?

Ha-ha-ha :)

For those interested

Full auction here:

https://www.youtube.com/watch?v=6Qd-H1ktGnw

You can be easily build 34m2 for less than 250k in NZ. As someone said that is the size of a garage. And if it’s 10km from the city, the land would be almost free by the time you divided the cost by many apartments.

The main thing that is lacking in Auckland is a decent rail line with plenty of flat developable land within walking distance to stations that are 10min from city. The southern and eastern lines are almost useless (most stations surrounded by hills, sea, motorways and reserves), the western line better but still not great. Light rail up the middle of the central isthmus is what we need to enable this type of build (and before you say I love light rail as it would be near me, even if it stopped miles before my place I’d still support it just because it makes sense).

I am assuming the place in Stockholm is somewhere near a “vanity project” rail line?

Land starts at 250k due to council

You do realise that the sales price of an apartment comprises much more than its construction cost?

For a 35 square metre apartment in Auckland:

Land: 50k

Construction: 200k (including a portion of common areas ie. halls and walkways )

Fees and charges (professional and council): 20k

That brings us to 270k. Then a developer will typically be looking for a 25-30% profit margin. That brings us to circa 350k. Then add 15% GST and we get to a nudge over 400k.

This is a simplified picture, designed to educate you

"we get to a nudge over 400k. "

There are over 153 freehold apartments currently listed for sale below this sale price point in Auckland on trademe.

1 apartment has 96 sq m and listed for sale at an asking price of $369,000.

Properties in the existing dwelling market do sell below the selling price charged by a builder / developer for an equivalent newbuild.

Selling prices for comparably sized new apartments listed for sale in Auckland are all above $500,000.

Good point.

perhaps there’s some good buys in the CBD. Many of the CRL/related closures are ending, the centre is starting to look better.

there’s a fair few bums around but it’s not that bad and doubt that would get worse.

I would just be cautious just to check that there’s not social housing in an apartment block, especially the cheaper ones

Probably well built and close to good transport links too.

And then Putin pops some mach 5 rockets through the window. No thanks

No one is forcing you, or anyone, to live in an apartment.

And then some KO tenant puts rocks through your window......

The property was sold in Jan 2024 (10 months ago) and the price is TBC. Is this due to settlement not yet completed?

Click the 'sold' link.

Is that bad Chris ? you would need to know the entire financial situation of the sellers. It could be loose change for them, some people are on million dollar salaries, just saying. For starters you average Joe couldn't afford that $3.2m house to start with. Some people are loaded and your whole outlook changes.

That must be it. Clearly a multi-millionaire bought it and doesn't care they dropped so much. Nothing to see here.

Obviously a multimillionaire did buy it, it cost over 3 million, it was hardly going to be a FHB was it.

Plenty of FHBs are multimillionaires.

Immigrants buying for the fire time in NZ are classes as FHBs, rich families buy their kid's first homes or provide the deposit for them, quite a few of the clever ones have accumulated a lot wealth buy not buying a house early and instead of loading up on expensive debt to the bank for an overpriced shitbox, instead have invested in their business so when they do buy they buy cash.

Seeing so many good properties pass in, indicates that there is no appetite for housing.. more pressure on downward prices

Yes indeed. There are many qualified buyers out there for the upper brackets, just not at these prices. More buyers are of the discerning type with a patient eye on quality. Currently, the lower bracket is being weakly supported by low equity borrowers and those downsizing (by choice or not). This market is looking so top heavy under a glut of overpriced homes and with fiscal tightening in play everywhere alongside rising joblessness, there little factual basis for sustainable upside anytime soon.

edit.

"Remember the last time they crashed 40%? Here"

Yes in inflation adjusted terms. They didn’t fall that much in nominal price terms.

This is the first time since the 1970's that house prices have fallen over 20% in nominal prices in Auckland and Wellington.

The current adjustment isn't even near finished. Stressed owners still straddled with soaring ownership costs are only just now getting limited relief from lower mortgage rates as they rollover. In the interim, expensive "fixits" such as payment holidays, interest only and term lengthening have continued to eat away precious finances on an asset that's declining in value. This isn't progress at all.

I think FHB's should think carefully before they sign. Leave the emotions at the door. Take the time to build a decent interest saving deposit. Consider all the risks associated with being the caretaker of the banks asset.

This isn't progress at all.

It is, because interest rates aren't still climbing.

For someone who extoles the benefits of not rushing into anything, you have some interesting expectations of how quickly things should improve.

How unusual. Pa1nter doesn't agree with one of my posts - LOL!

Not because it's you.

Because it's bollocks.

😂🤣 I am so relieved. I might have taken your opinion seriously...

Baby boomers trying to offload houses they haven't spent a dime on for 30 years and expecting top dollar

Worked for this one. 51 First Avenue, Kingsland The gross annual rate of return was around 8.8% if memory serves. Just goes to show what a spending very little can achieve (heavy sarc by the way as it is a deceased estate sale).

And yet multi-unit redevelopment may be very challenging due to the low density zoning. Go figure. Great location near Kingsland

A seemingly different narrative on clearance rates by Oneroof.co.nz (CAVEAT EMPTOR as they may have a vested financial self interest)

That was reflected in the clearance rate at auctions, which were in the 60s rather than last year’s when they were in the 30s.

https://www.oneroof.co.nz/news/its-busy-busy-warning-of-auction-crush-a…

So that does not match the sales each week reported on Interest.co.nz

its not busy busy busy ?

The article is reporting on a different reality?

Oh Dear, How sad, Never Mind........

Maybe he meant that they where busy busy busy, not the buyers.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.