Early signs are emerging the glut of homes for sale that has dominated the housing market for the last 12 months may finally be moving back to a position where supply and demand are better balanced.

The much anticipated spring surge in sales finally materialised in October, with the Real Estate Institute of NZ recording 6681 residential sales for the month. That was up 10% compared to September, and up 20% compared to October last year.

Perhaps more importantly, two key indicators of the long-term movements in supply and demand have been showing signs the big oversupply of properties that has created a strong buyer's market, are starting to shrink.

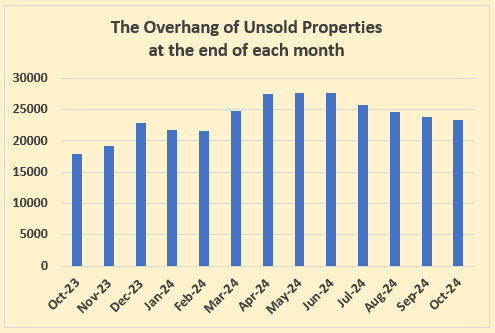

The first is the overhang of unsold properties at the end of each month. While still at a relatively high level, it has been steadily declining for the last four months, from 27,727 at the end of June, to 23,347 at the end of October.

That's a decline of 16% over the last four months. While the overhang is still high - up 31% compared to October last year, at least it's now moving in a more promising direction. See the first graph below for the trend.

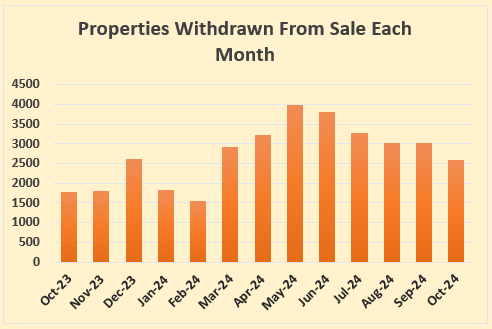

The second set of numbers that's looking promising is related to the first, and that's the number of properties being withdrawn from sale each month.

This peaked at 3981 in May and then steadily declined to 2580 in October. However, it still remains elevated. See the second graph below for the trend.

So two of the most important recent trends for picking the direction of the market have been fewer unsold properties at the end of each month, and fewer unsatisfied vendors taking down their for sale signs.

But hold the champagne, those signs are still very tentative and there is one set of figures that has the potential to disrupt those trends. That's the number of new listings coming on to the market.

According to Realestate.co.nz, new listings surged to 11,572 in October, up 21% compared to October last year. That pushed the total stock of properties advertised for sale on the website to a 10-year high.

Which means there will need to be particularly strong levels of sales in November and December for supply and demand to keep moving closer to being in balance.

Otherwise the market is likely to move even further in buyers' favour.

And there is only another month to go before the market shuts shop for the Christmas/new year break, which means crunch time draws nigh for both vendors and buyers to make decisions on a sale and purchase.

The comment stream on this story is now closed.

You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

173 Comments

Sharp recovery underway.

Especially pronounced in Auckland central suburbs with fewer townhouses.

Looks like even the bland cookie cutter townhouses are selling now!

Thrive in 2025 and beyond! 🥂

We won't be hearing from too many DGM today.

TTP

One day Tim gets restless when "DGM" make too many posts, the next not enough. I suggest it's more a case of recurrent separation anxiety.

A sustainable floor may be near, a sustainable rise in prices is something else altogether. As the article suggests, it's too early to break the champers.

In your case, Poppy, Champagne is destined to remain a mere figment of the imagination.

TTP

RP and TTP (aka Tim) should once and for all settle their differences like any married couple.. scratch their eyeballs out!

Or go to the pub, have some beers and talk about their cats rather than properties

It should be settled with a dance-off!

Our health system is already overworked, not sure we should be encouraging RP and TTP to go dislocating things..

😂🤣, the solution is actually quite straight forward. On 01-March, will Tim and the bulk of his ilk still be commenting here?????

@Retired poppy - ILK sounds negative ?

probably not, you will be left to make comments on your own posts.

@Poppy and Rookie - btw whats happening on 1st of March

Starting on Saturday, March 1, 2025, you will need to be a qualified supporter to comment. And you will need to be a qualified supporter to receive our daily and weekly email newsletters - here

Such a waste of oxygen reply. Why bother?

Actually, the figures still underestimate supply. TM listing back over 15,000 in Auckland. Most importantly, TM listing of ne homes up to 3,800 (up from 3,000 earlier in year). And as this developers list 1 townhouse when they have 10, a lot of new supply to address. And that new supply isn't upgrades, or rental tenants becoming purchasers, it is new supply.

AAuckland prices will be within 2% of where they are now in a years time.

Yawn was so predictable and summer and the next OCR cut has not even arrived yet.

Cherish the next one, it may be the last for a while.

Trumpy person will have his final say on OCR in Jan 2025!

Trumpy person will have his final say on OCR in Jan 2025!

It's OK to say Trumpy. Or Trumpty Dumpty and The Orange. He won't care.

But referring to Jacinda Ardern as C _ _ _ _ y is misogyny and something to do with living rent free in your head.

It's a funny old world.

Have you still not moved on?

You'd have to admit, there does appear to be a lack of consistency

Not really. Trump loves to dish out, ergo he's fair game in return. Ardern never did (at least publicly or from a pulpit). ... I don't see any lack of consistency.

On here

Such and arrogant prick (Ardern on David Seymour)

It wasn't intended to be a public comment, she was making a private comment to a colleague that was captured by the microphone. So no, that isn't a good example.

what a weird post!

Which article were you reading? The market is still trashed. The crash rolls on.

and on the same day

https://www.interest.co.nz/economy/130870/updated-treasury-forecasts-wi…

This will be a very slow recovery

and there is an exodus of people leaving.

Please can you provide the share of FHB, upgraders and Investors who bought in October.

Would be interesting to see where the "uptick" has come from.

I suspect investors are jumping back in on the back of lower i.rates and a housing frenzy focused government in national. Get in before DTI's get pushed through.

RBNZ C31 might provide some clues. From Jan 2022 to June 2024 the average monthly loan commitments to investors was $945m. July, August, September 2024 was $1.35b per month.

https://www.rbnz.govt.nz/statistics/series/lending-and-monetary/new-res…

"I suspect investors are jumping back in on the back of lower i.rates and a housing frenzy focused government in national. Get in before DTI's get pushed through. "

This property in the existing dwelling market was purchased in the last couple of weeks by a non owner occupier and listed for rent. A first home buyer on a single income (a single mother) was outbid by the non owner occupier buyer.

https://www.realestate.co.nz/property/21-dampier-avenue-awapuni-palmers…

21 Dampier Ave, Awapuni, Palmerston North. Listed for rent at a 6.7% gross rental yield.

https://www.trademe.co.nz/property/residential-property-to-rent/auction…

This is the potential unintended consequences of the reintroduction of interest deductibility by the current government. If there was a zero interest deductibility policy that would have been phased in under the previous policy,

1. would the non owner occupier buyer have bought (and provided a public service as they claim)

2. would the single mother have been less likely to have been outbid?

Who cares? Its a good thing. People who can afford to buy houses can afford to rent houses. Taxpayers have to worry about the people who cant afford to rent houses, because they are the ones who end up in emergency accommodation, and on the public housing waitlist. So now a family can move out of a motel and into a $620 a week four bedroom home instead of paying $690 a week for the new build 3 bedroom home. Saving themselves $70 a week so they can now afford to feed their kids breakfast and provide a school lunch. #winning.

And what happens to the single Mum who was hoping to buy it? Does she move into the motel that has now been left vacant? Or does she stay in her current rental? Given that an investor buying the Dampier Ave house doesn't change the overall amount of accommodation, wouldn't it have been better if the single Mum bought it and the motel family moved into her current rental? Because taxpayers also have to worry about people who get to pension age and don't own their home, because they almost definitely can't afford to rent anywhere on the pension alone and either require accommodation supplement or social housing.

"Because taxpayers also have to worry about people who get to pension age and don't own their home, because they almost definitely can't afford to rent anywhere on the pension alone and either require accommodation supplement or social housing. "

The fiscal cost to the government of reintroducing interest deductibilty for non owner occupiers is estimated to be $2.92 billion until 2027/2028 tax year (conversely, this is the benefit to non owner occupier owners in the existing residential dwelling market given by government and tax payers)

https://www.taxpolicy.ird.govt.nz/-/media/4f742049bc7b437a9a8b98520a582…

What could the government do with this money instead?

Improve existing infrastructure, invest in new infrastructure, improve health system, build more social housing. Make lives better for all New Zealanders rather than a small proportion of New Zealanders.

Have you ever bothered to think that the renter actually pays for the house but never gets ownership?

How p##d off would you be doing that?

$620 for a house like that in Awapuni seems pretty extortionate as well, especially given the state of it.

That area of Awapuni was rough as gut..

One Roof reporting this today:

The latest CoreLogic Buyer Classification data showed that first-home buyers remain a strong presence in the market, growing their share of purchases from a touch less than 27% in Q3 to almost 28% in October – a new record high.

Meanwhile, the gradual re-emergence of purchasing by mortgaged multiple property owners (i.e. investors) continued in October, with a 23% share of activity, up from a lull of less than 21% back around April.

26@Main - tell them about your successful bitcoin mining and the eye water profits you made and no tax paid? No consideration for enviroment - just your unrelented greed - also dont you like to tell people to move to AU? give them a bit more of your widsom?

Bitcoin gains once converted to NZD, are taxed as personal income though (?)

Absolutely. But many think tax evasion is acceptable by not declaring it. For now the IRD doesn't seem to care much, but knowing they can go back 7 years, if they wake up things could turn ugly.

P.S: I do declare my crypto gains, taxed @39% (last bracket)

If the price of an essential goes up we should break out champagne?

Certainly, property owners/sellers will break out Champagne.

Buyers have had a decent chance during the market downswing of the past 3 years....... Those who seized the opportunity are already benefiting from lower interest rates and avoiding rent - as well as enjoying a more secure existence.

TTP

What about the people that weren’t in a position to buy then, or couldn’t afford those interest rates?

Next time your power bill goes up, maybe break out a bottle of champagne on behalf of the power companies.

Honest question, why would property owners break out the champagne? If they aren't planning on selling, they aren't actually making anything, right?

I generally never comment here, I just enjoy the fighting amongst commentators, but this one has me genuinely curious.

I'm going to a BBQ this weekend with some friends. On the Friday before such event I'll typically log in to my banking app and check the Valocity valuation. If it's gone up considerably then it becomes a solid talking point on the day.

It's a great way to flex my foresight and intelligence for buying a house that in the very short term has increased in value, even if I've lost 20% since purchasing 3 years ago.

"Honest question, why would property owners break out the champagne? If they aren't planning on selling, they aren't actually making anything, right?"

Possibly the original commenter commented from their own perspective, and speaking from their own perspective as a commission earning real estate agent and celebrating the commission?

It's just occurred to me what a strange thing it is also

It’s celebrating an enlarged ego - ie many NZers have developed an ego attachment to their net worth or value of their house/housing portfolio.

My personal perspective is this is pretty sad, but it’s fairly commonplace glitch in the human operating system. Definitely a bug and not a feature.

Hi TTP,

For the last year I have been renting a c. $2m house paying $950 p/w (c. $50k per year) and earning interest from having my savings in TDs. How much rent would I have saved if I bought this house with a $1.5m mortgage instead of renting it (excluding rates, insurance, maintenance, etc.)?

"For the last year I have been renting a c. $2m house paying $950 p/w (c. $50k per year) and earning interest from having my savings in TDs. How much rent would I have saved if I bought this house with a $1.5m mortgage instead of renting it (excluding rates, insurance, maintenance, etc.)?"

That is the point missed by many people who are financially illiterate. Here are the numbers for an owner occupier owner vs renter:

A) annual payments difference

1) P&I payments of $108,973 per year - $1,500,000 mortgage at 6.00% p.a mortgage interest rate on 30 year term

2) rates and insurance potentially another $8,000 -$10,000 per year

3) maintenance costs - say another $2,000 per year

Total cost for owner occupier: $118,973 - $120,973 per year

Total cost for renter: $49,400 per year ($950 per week x 52 weeks)

Net Annual savings by Renter: $69,573 - $71,573 for current year.

B) interest income deposit

Interest income on deposit of $500,000 ($2mn house less $1.5mn mortgage above):

1) Deposited at big 4 bank in 1 year time deposit at 4.8% p.a - interest income of $24,800

2) Less Tax at 33% rate: $7,920

3) net interest income on deposit $16,616

Total bank deposit after one year: $516,616

Net annual savings by renter: $69,573 - $71,573

plus interest income after tax: $16,616

Total cashflow benefit to renter vs owner occupier: $86,189 - $88,189 in current year

Conversely owner occupier pays $86,189 - $88,189 more than renter for the same use of the house.

C) Amount to use as a deposit in one year:

So after year 1 for a renter:

1) Total savings from renting: $69,573 - $71,573

2) Total deposit: $516,616

Total bank deposit (that can be used to purchase a residential dwelling in future): $586,189 - $588,189

Beware as the previous commenter has a potential undisclosed vested financial self interest, so they have a different motivation by telling people to buy.

CAVEAT EMPTOR

You conveniently left out the part where property would increase in value on average 5.3% annually.

Quite an important factor in this situation.

"You conveniently left out that the property would increase in value on average 5.3% per year, quite an important factor in this situation"

That is pure speculation on future capital gains. Remember at Nov 2021 when the high profile property promoters were espousing the house prices double every 10 years (i.e average 7.2% p.a)?

https://www.oneroof.co.nz/news/double-your-money-new-zealands-surprisin…

People were willing to bet 500% - 1,000% of their net worth / life time savings on this scenario. (i.e 80 - 90% LVR mortgage)

People forget the warning given on investments: Past performance is no guarantee of future returns.

People are free to choose their expected house price growth rates, however people are not free from the consequences of their choice. Look at the buyers of 2020 - 2023 period who bought in Wellington and Auckland, especially those using high levels of leverage.

"Remember at Nov 2021 when the high profile property promoters were espousing the house prices double every 10 years (i.e average 7.2% p.a)? People were willing to bet 500% - 1,000% of their net worth / life time savings on this scenario. (i.e 80 - 90% LVR mortgage)"

For those who don't realise, the financial consequences of a Peaker and "Buyer Today".

1) Peaker

The median house price at the peak for Auckland was $1,300,000

With an 80% LVR, this is a mortgage of $1,040,000

The 20% equity is $260,000

2) Buyer Today ("BT") - Sept 2024

In 2021, the buyer who waited, deposited the same $260,000 equity into a bank deposit earning interest. Also BT would rent an equivalent house and have still saved money due to the rental being below the monthly P&I mortgage payments of Peaker - in 3 years the savings would have been about $20,000 annually. So a Buyer Today would have an amount of $340,233 to use as a deposit.

The current median house price for Auckland is around $950,000

Equity deposit of $340,233

The mortgage at this purchase price would be $609,767 (an LVR of 64%)

The Peaker has a mortgage which is higher by $430,233 (mortgage of $1,040,000 for Peaker vs $609,767 for BT). BT's mortgage is 41% lower than Peaker's mortgage.

Assuming BT, pays the same exact dollar amount each year that Peaker pays for their mortgage, as a result of that additional borrowing, Peaker is paying $1,232,229 more over the 30 years than BT (This is due to higher borrowing amount of $430,233, and total interest on this of $801,996 over 30 years). BT is mortgage free by the year 2037, whilst Peaker continues to pay their mortgage until 2051 (14 years later) - so after the year 2037, BT can save all that money that Peaker continues to pay on the P&I mortgage.

Assuming same incomes, and same living costs (food, travel, etc except mortgage) , BT can save the total $1,232,229 in payments that Peaker is paying. If BT invests the annual P&I payments that Peaker continues to pay after the year 2037 at 4.0% p.a, then in 2051 this amount will grow to $1,401,500.

Remember that at the end of 30 years, the house price will be EXACTLY THE SAME for Peaker and BT.

BT will have more money available for retirement than Peaker. Conversely, Peaker will have less money than BT at retirement.

That single decision to buy in November 2021 would have cost $1,232,229 extra to buy the exact same house for Peaker compared to a Buyer Today.

Note the equity positions as at Sept 2024 also:

1) Peaker: NEGATIVE $90,000 (negative equity, assuming interest only - house price of $950,000 vs mortgage of $1,040,000) - a loss of over 130% of their initial equity (and likely life time of savings).

2) Buyer Today: $340,233

Owner occupier buyers: CAVEAT EMPTOR

So you're saying now is a good time to buy? I agree :)

"So you're saying now is a good time to buy? "

Each person is in their own unique situation and needs to make their own assessment based on their needs.

That is pure speculation on future capital gains

Actually no, its not speculation.

Its statistical data over the past 34 years.

Here is a source for you.

Actually no, its not speculation.

Its statistical data over the past 34 years.

Thank you for sharing those historical price statistics.

Remember, past performance is no guarantee of future returns. There are many examples of this in history, yet many people continue to use historical price statistics and historical house price trends to develop their future house price growth expectations. That is how house prices can reach levels with high house price risks.

Here is a calculation from Dec 2019:

https://www.oneroof.co.nz/news/average-house-price-in-auckland-could-hi…

In their property investment calculations, Opes Partners uses 6.0% p.a house price growth for Auckland and 5.0% p.a house price growth ex Auckland.

https://www.opespartners.co.nz/property-markets

People are free to choose the future house price growth expectations to use in their calculations, however people are not free to choose the consequences of their choice.

You’re kidding right? You think 34 years of past data that you probably don’t really understand is going to be a good predictor of the future? And you’re prepared to bet an enormous amount of money on that guess? Good luck pal.

Last 5 years (despite covid it has gone up 3.5% pa in Auckland. So less than interest.

Reminder of these property price calculations for Auckland back in Dec 2019 for the next 20 years to 2040.

https://www.oneroof.co.nz/news/average-house-price-in-auckland-could-hi…

With respect, anyone that rents out a $2m house csn not be classed as an intelligent investor.

If they intend to rent it out ss investment at $950 pw then I would be advising them to quit it and buy 3 or 4 houses as the rental return will be more like $2000 pw and capital gain would be far greater as well.

What is the address of this property or area?

"I would be advising them to quit it and buy 3 or 4 houses as the rental return will be more like $2000 pw"

What would be the net rental yield for these properties? i.e (annual rental less rates, insurance and maintenance costs) / property purchase price)

Not that great but far better than renting out a $2m property.

Return would be approx 4% after rates insurance etc, that's why we are not buying to rent out now, as the numbers do not add up.

This is going to continue to cause issues in regards to rental accommodation.

You would be financially not very bright if you are building to rent out to tenants.

"Return would be approx 4% after rates insurance etc, that's why we are not buying to rent out now, as the numbers do not add up."

Under current conditions, what net rental yield level is adequate for you?

We are fortunate that our average rent yield is probably around 10% on purchase price but if worked out on current market value then probably 3 to 4 %, hence why we do not buy to rent out now.

Better ways of making a profit nowadays.

We only buy to improve property now but if buying to rent out, would want in excess of 5.5% yield plus have to be big upside.

Devonport. It wasn't purchased for $2m but the smart thing to do would be to sell it.

"If the price of an essential goes up we should break out champagne?"

If you're the owner of said essential asset, yes, if you're wanting to buy it, no.

Compared to Oct last year (as the stock is also seasonal) we are still looking very heavy on listings.

The fall over the last few months is primarily through withdrawal, not sale. The thing is withdrawn properties have to go somewhere...

"Coincidentally" Auckland and Wellington now have historically high stock on the rental market. And guess what, renting out a house is increasingly difficult and rents are now falling.

I'd wager the overhang will flatten out or even grow in November as rentals go back to the "for sale" column.

This country's obsession with house price increases is quite frankly disgusting, and will be its destruction. There are a number of small-minded, self-centred individuals who post prominently on this site that cheer for any and all news regarding price increases. Little do they realise how decimated the tax-paying base is getting for the future and how this will impact them. There is no such thing as private acute healthcare - they will rot in the same run-down, understaffed hospitals as the rest of the country. They will be the victims of criminality as increasing wealth inequity pushes people to desperation. They will need to use the same potholled roads. They will be exposed to the rising numbers of drug-abusers and homeless. Auckland will look like San Francisco or Toronto over the next decade. Any New Zealander with an in demand qualification, with future high earnings potential and subsequently high tax-generation potential is jumping ship. There will be no money for anything (and there already isn't as per our revenue minister a couple of days ago).

This isn't sour grapes - my partner and I do not own a house. We easily could as we are both doctors, but have decided that the NZ ponzi scheme isn't for us, and will take our skills (and heavily government subsidised educations) to Australia as we finish our training over the next couple of years.

Be careful what you wish for.

Yip and anyone who desires a more even playing field for FHBs and a reduction on systemic financial risk (caused by a highly leveraged/expensive market) is belittled by these people as ‘doom gloom merchants’ who are just ‘envious of others success’.

Get real is all I can offer these types of views. Our housing market (like many across the world) has turned ugly - it isn’t something to cheer about but more something we should be ashamed of.

Look at the extremely low fertility rates across the world and especially in places where housing has become extremely expensive - if the sign of success is the local population failing to procreate because they don’t think they can afford to then you are living in lala land. It’s a sign of a species/society in decline - not good news at all. The success of those calling others ‘doom merchants’ is the real doom and gloom.

This is a consequence of the current policy settings.

This property in the existing dwelling market was purchased in the last couple of weeks by a non owner occupier and listed for rent. A first home buyer on a single income (a single mother) was outbid by the non owner occupier buyer.

https://www.realestate.co.nz/property/21-dampier-avenue-awapuni-palmers…

21 Dampier Ave, Awapuni, Palmerston North. Listed for rent at a 6.7% gross rental yield.

https://www.trademe.co.nz/property/residential-property-to-rent/auction…

This is the potential unintended consequences of the reintroduction of interest deductibility. If there was a zero interest deductibility policy that would have been phased in under the previous policy,

1. would the non owner occupier buyer have bought (and provided a public service as they claim)

2. would the single mother have been less likely to have been outbid?

"Until recently, many investors steered away from existing properties after the previous Labour Government lifted the Brightline test to 10 years and stopped them from claiming tax deductibility on their mortgage repayments when offset against rental income."

New housing was left under the old rules making it more attractive to investors for rentals.

New Zealand Mortgages managing director and head of lending Nathan Miglani says his business has seen a big uptick in the number of investors. “The number of property investor loans we have done over the past two months is the same as we did for the whole of last year.”

The majority are looking at existing properties now the Brightline test has been brought back to two years, he says. “Buying an existing house with land with the potential to renovate or subdivide in the future is looking extremely attractive to investors.”

He says first home buyers will be back to competing full on with investors next year.

https://www.landlords.co.nz/article/976523746/competition-between-inves…

Agreed, and thank you for (before you're off) contributing to ease the current pressures in the medical system to the best of your abilities. I wouldn't want to be a doctor at present given the sate of healthcare and especially mental health in NZ, add in the the lack of credence given to doctors capabilities by a growing percentage of the public. Keep up the good work :-)

Hear Hear! Well said.

That is the kind of insightful, well informed perspective sorely needed at this time in our nation's growth.

Agreed - however why choose Australia who are just obsessed about houses as we are?

Hah good one. Obviously for the $$, and (mostly) better climate.

So he's not moving because of house prices...

Our reasons for picking Australia are two fold:

- Comparable medical system that is well-resourced with transferrable qualifications

- Lower cost of housing RELATIVE to the income that we will be earning

That point has been made repeatedly to Jimbo and it never seems to sink in.

Also 6% Super minimum - some employers do 10 or 12%. Generally lower cost of living, especially fuel

Aus house prices are slightly lower relative to income (depending on where you choose). But many other places are way lower. Why not Houston? (edit: maybe because "with transferrable qualifications?")

Yes, but for certain professions the ratio of house prices to income are significantly better (ex Sydney)

I got asked at HR why Australia and not the US (where HQ was)?

1. Requirement for sponsored H1B, which the company weren't offering.

2. I've seen the 'at will' contracts the US staff have, and a whole department let go overnight. No thanks.

(Reason for moving was wife's instant full registration vs the onerous ever-changing NZ reqs which had kept her provisionally registered for 8 years, and seen a number of friends and family quit entirely).

Everything is better in Australia (except in Melbourne, which is pretty dire at present). Even driving for hours is a pleasure - no potholed roads, no speed humps, no stupidly low speed limits, no bad drivers. Compared to a drive up the south island recently - almost took my axle out on a pothole and got a chip in my windscreen from a rock.

People (may just be Queenslanders) are more friendly, the weather is fantastic, the beaches are beautiful, and council rates are a third of what they are in NZ.

and the wildlife is deadly:) you forgot that part.

"Everything is better in Australia (except in Melbourne, which is pretty dire at present). Even driving for hours is a pleasure - no potholed roads, no speed humps, no stupidly low speed limits, no bad drivers. Compared to a drive up the south island recently - almost took my axle out on a pothole and got a chip in my windscreen from a rock.

People (may just be Queenslanders) are more friendly, the weather is fantastic, the beaches are beautiful, and council rates are a third of what they are in NZ. "

Since you speak so fondly of Australia and think it is better than living in New Zealand, what is keeping you in New Zealand?

So its not a Ponzi as long as you are earning enough money, ok got it.

Better working conditions (because they have a good tax base that can actually fund healthcare properly). Also better pay - means that we can buy something nicer and have it take up a lower proportion of our income, instead of spending 1.2 mil on a rundown 70s bungalow in an average part of the North Shore and paying that off for the next 30 years.

If I bought a house on the Gold Coast for the same value as what I own here, I would save $6000 a year in council rates. Its not just the cost of the house in NZ thats shocking, its the ongoing yearly costs to own it.

You'll be paying more than 1.2 mil (and 50k+ in Stamp Duty) for a run down bungalow in Sydney's equivalent of the North Shore suburb. And you'll be living far away from your parents/friends (if they are in NZ).

"instead of spending 1.2 mil on a rundown 70s bungalow in an average part of the North Shore and paying that off for the next 30 years."

Wherever people choose to work, if the house price risks are high in that location, then it might be better to rent rather than buy.

Refer example of Peaker vs Buyer today.

Absolutely dreaming. I lived in Sydney for 8 years my income was almost double what it is here and I could only afford to buy way out west not in the nice northern beach suburbs and certainly not inner city. Even then it would be a terrace or a duplex with neighbours on top of you and no land to get a trampoline in and a huge bonus if you got off street parking.

At least the earnings are a lot higher and cost of living lower

And those self-centred individuals here probably exist in the hundreds of thousands across the country. I know many who display varied levels of this self-centredness

I suspect you'll find those people are also heavily concentrated within a small band of birth years, approximately 18 years wide.

Yes you have described the reality of our likely future well. I have spoken along similar lines on numerous occasions only to get shut down and labeled a DGM. It seems many are more than happy to simply take the money and then live in their gated compounds with security 24/7, private health care, private schools etc.

It is a real shame we are losing the likes of you and your partner, along with many of our best and brightest however it seems that is the price many are willing to pay simply for personal financial gains.

"It's a shame that we are losing best/brightest........price many are willing to pay simply for personal financial gains"

The young doctor and her partner are planning to leave NZ for FINANCIAL GAINS too, make no mistake. They will deserve to be blamed for NZ declining as a country even more than "the evil real estate investors". At least the Real Estate investors in NZ pay taxes back to NZ (and provide rentals or develop new properties which the country needs more of), while the young couple will happily 'receive' from NZ while they are studying and then run off to Aus when it's time to give back to NZ.

Ironically, the young couple will learn that there are even bigger real estate investors in Australia who they as a FHBs will need to complete with, just like in NZ.

while the young couple will happily 'receive' from NZ while they are studying and then run off to Aus when it's time to give back to NZ

I strongly suspect that those studying medicine here already intend to leave NZ when they start studying as all they have to do is look up the earnings of the average doctor and calculate how long it will take to pay down their student loan vs if they went to the likes of Australia. the financial benefit of leaving NZ is magnitudes greater, so why wouldn't one leave to pay down their NZ debt. Perhaps they might come back sooner once their student loan is gone and they can save quicker to purchase a house. You can't fault this logic as unless the govt stipulates that graduates have to do X number of years in NZ after study then there's no way to stop this continuing.

Dear MassiveNerd11

As I grow older, your exceptional care will become increasingly vital to my well-being. I deeply hope you’ll reconsider leaving, as your skills are truly irreplaceable to myself and my peers.

Sincerely,

Baby Boomer

And I need your tax money to pay for my super that I supposedly paid tax for all my life.

Now, now, you listen here Jumbo. Where do you get off talking like that.

I have paid taxes all my life. We didn't have participation trophies. We didn't job-hop, we stuck at the same employer for 40 years because we knew of loyalty, respect and were committed to hard work. I have darn well bloody earned my Super so hands off.

Lol

And I had to put up with 18% interest rates in the 80s. It lasted six weeks but that is beside the point...

Good one...

MassiveNerd, you fail to understand that this is a financial website, aimed at making money. It's not an ethics and morality site, aimed at making the world better in your eyes.

Edit: and yes, you're right, it's sour grapes.

Yvil is back :) missed your comments.

Note massive is doing the best he can for himself, not NZ. Just like everyone else here

Well said, but he thinks he stands on a higher moral ground.

I enjoyed his post. It's relevant. He speaks of the consequences of investing in property on society. It just doesn't fit your opinion Yvil.

It doesn't fit Interest's motto: "Helping you make financial decisions "

They literally shared their story of how they’re making a better financial decision.

Also, if your financial decision makes you personally rich but causes so much pain to the rest of society it breaks the social contract you may find that the financial gain was only short term.

: Ha ha, I caught and ate the only chicken on the island, you only managed to get an egg. I'm richer than you

: Yes, now we will not have any more chickens or eggs.

: this is a financial website. I win.

The 2 - 3,000 year old scrolls say it is better to be poor and to live with integrity.

So western civilisation, that is founded upon the truths of these scrolls, would argue against your position and say that ethics and morality are highly intertwined with our financial decisions. If we make bad financial decisions collectively our society gets worse..if we collectively make good decisions the quality of our society improves.

My argument/opinion/view is that we haven’t been making our financial decisions with integrity (which requires good ethics and morality) hence why our housing market and society have become such a shambles (and this feeds into issues with mental health, inequality and social instability/lack of cohesion).

Just because you don’t want to see something does not mean that it is not true (ie you think financial decisions are only about making money - but that is because you wish to ignore the consequences that have occurred as a result of these previous decisions and the second order effects of them).

@IO - you have no idea how poor proterty investors are at the moment - the burden would crush you - you obs done have the stomach for it - however complain you will

"you have no idea how poor proterty investors are at the moment"

Is that due to a combination of the following factors:

1) non owner occupiers paying too much for the property? (due to their continued expectation of tax free capital gains and a willingness to have negative cashflow property in the short term?)

2) taking on too much debt to finance their overpriced purchase?

That would be called investment risk.

Most cash buyers in the 2020 - 2023 years would not be under any cashflow stress.

If buying up houses during a housing affordability crisis is walking in your path of righteousness then good for you. Just don’t looking for anyone’s pity if you claim you’re poor financial (if not morally). Those same houses could still be on the market or owned by a FHB and you wouldn’t have the debt, nor claim to be poor.

The scrolls (the proverbs) will save you from your suffering when you are ready.

Those "poor proterty investors" should get out of the game then.

My best investments have gone only forward, I cut the rest, its called risk management, solely leveraging property when the world is your oyster is like believing only Catholics go to heaven...

You really mean leverage gamblers. Yield based investors are all fine.

Yvil, 18th Nov 24, 11:19am (on the piece about the treaty).

Same rules for everyone seems pretty fair to me.

Yvil, 18th Nov 24, 4:39pm

this is a financial website, aimed at making money. It's not an ethics and morality site, aimed at making the world better in your eyes

@Massive Nerd

So you are happy to use NZ taxpayers money to fund your education, and then move to Australia so you can earn 50-100% more?

Do you care about New Zealand?

Do you not know that Australia also has a housing ponzi, and Australians are obsessed with property?

Please do some research, and then you will realize that there is crime, homelessness and drug abuse also in Australia.

So you are happy to use NZ taxpayers money to fund your education, and then move to Australia so you can earn 50-100% more?

Think of it like landlords being happy to accept higher rents due to the accommodation supplement and you'll find the moral dilemma dissipates.

Do you care about New Zealand?

Be careful, you're on dangerous ground as Yvil is pounding the corridors looking for comments that exhibit a hint of morality!

I'm asking Nerd, not you, Murray. He/she was the one who brought up the issue of using taxpayer money. He/she is trying to justify going to Australia. They should just p### o## there now if they want to go. But, oh no, just do a bit more training here.

God do you ever read your own comments?

Children are raised without a choice of where they're raised. They are raised in NZ. Reach early adulthood and realize this country is not the place to be if you want to have any chance of a normal life, like starting a family and enjoying time with your kids.

Your take is "you got education here so you must stay and pay it back to society". How does that work? Deluded as can be.

Oh and btw me and my partner are out too, feels great leaving and not contributing to a society that doesn't want you to have a chance.

I didn't say that you must stay, we all have a choice. You too, leave as soon as possible.

Some people tend to focus on the negatives of New Zealand, whereas others focus on what an amazing country is to live in.

I'm a young person too, plan to have kids here. I too could move to the lucky country (rich in natural resources, pumping the economy) but it won't be anything to do with property prices if I do go.

You make being raised in NZ sound like being raised in the Congo or Indonesia.

You're deluded.

Is that a professional or amateur opinion?

Now you are resorting to ad hominem attacks.

I thought we could have a reasoned debate, but doesn't look like you are keen on that.

@21 Trillion - time for you to to to AU boy -

You ask others if they really care about New Zealand, while also telling a couple of kiwi doctors to hurry up and p!ss off out of NZ.

You stand proud stating your willingness to raise kids in NZ - but will your kids share your outlook and choose to stay in NZ?

I've stated that those who have already made the decision to leave should leave. To other doctors, I would encourage them to stay.

My kids might want to leave NZ, and that is fine as it would be their choice to do so, and seeing other countries will widen their experiences. But I would be disappointed if they said it is awful here etc etc. If they become doctors and complained, then I would say to them go work in the UK NHS, or work for MSF.

Australia is easy money for everyone - it's not called the lucky country for nothing. And if you have read my posts you would see that I have wished the young couple good luck on their future in Australia.

What about you, Time Lord? Are you staying or going? And what are your reasons for the choice?

Depends if that "choice" is made under duress because the economic landscape in this country is so heavily stacked against them.

You resort to comparing to a worse off system to elevate the situation of NZ.

It's a poor way to approach speaking honestly about large issues.

If we are going to compare ourselves to the worst of the worst, why should we even bother trying!

I wish you the best of luck, truly, I came in blunt as you seem vulgar about people leaving, almost as if it's upsetting you deep down inside, perhaps some kind of resentment?

I'm quite willing to have a genuine debate. Unfortunately insults tend to be hurled around on this site, which doesn't help the debate. Sorry if I ended up getting vulgar, I agree it probably wasn't right for me to be so.

I could leave for Australia next month and earn 50% more, as could a lot of people here. I wish people could just say that, rather than give NZ a good kicking. I'm proud of New Zealand but not blind to its faults.

I'm sure you are a decent person, and if we were chatting over a beer I'm sure we would be having a better discussion than we are exchanging comments on a website.

@Tron - you only reacted to what that kid threw down there was no debate @21 thinks he is the judge of morality spouting oh here who is righ tor wrong (thats not a debate) actively telling people that NZ is Bad (so not a patriot, lack of a better word) further more he then spins here how much he makes on a resource heavy bitcoun and dont pay tax - he will take your beer and drink it and compain.

The self righteousness is strong. Complains about the greed of property investors and the ponzi in nz. Moves to another country with exactly the same ponzi where he can earn more money.

Yes - I am perfectly happy to do so. I have worked 8 years in crap conditions for relatively bad pay at significant personal sacrifice - the average person has ZERO idea what being a doctor involves. I work 60 hours a week. I am constantly sleep deprived. I am stressed, and I am making life or death decisions literally every day. I have to study when I come home. I have delayed starting a family because of my job. I have missed more christmasses than I have attended since starting work. I have given this country more than enough. And I feel zero guilt about leaving.

You also do realise that all university education is subsidised to some degree. And so your argument applies to literally every young, educated person leaving the country. Expecting young people to stay in a bad situation for your benefit is the definition of entitled. I am not martrying myself for generations of older people that have enriched themselves at the expense of younger people. How about instead of pointing the finger at people like me, people like you take a step back and ask why the people that form the basis for our country's future have no interest in staying here?

I don't expect you to stay for my benefit - if you want to go, just go. Please don't say that you are leaving NZ to escape the Ponzi cos you will find out that it is worse in Australia. I wish you and your spouse good luck wherever in Australia you choose to go. But, as Six60 sang, don't forget your roots my friend.

Well said. I am a specialist rural GP in nz and my wife and I echo the same re moving to AU. Why spend $1.2m to buy a shit rundown 70s house with a 30 year mortgage? It just doesnt make sense. Like many of our peers, we're only in NZ due to family. I'm just riding out my time in NZ and doing extra training to boost the cv for AU. See you on the other side.

You are kidding me, right?

1.2 million can buy a fantastic place in rural NZ.

Ok, go to Bondi, and get a s##t place costing $4million

Just remind me why you became a doctor in the first place?

I can predict what they're going to say. They became a doctor to help people. Perhaps for the intellectual challenge as well. However they are struggling with the increasing workload and moral injury of working in a crumbling system where the resources just aren't there to get people the help they need. They're getting paid enough to buy a house, but it is not at all comensurate to the value they bring to society. They are sick of referrals to specialist services being declined, and being left to manage problems that need to be addessed at the specialist level. They are burned out. And despite being a good person, and hard-working, and trying their best, if they had to stay in New Zealand, it could not be as a rural GP. Because that would not be sustainable for their physical and mental health for the long term. And so the best decision here is to go overseas where they can still help people, but the medical system is functional and they are compensated adequately.

Next time you have to wait 6 weeks for a GP appointment or 8 hours in ED, maybe you can use that time to reflect on why you feel that young doctors should stay in a crap situation for your personal benefit?

Next time you have to wait 6 weeks for a GP appointment or 8 hours in ED, maybe you can use that time to reflect on why you feel that young doctors should stay in a crap situation for your personal benefit?

People like Tron do not see the link between a government giving landlord's a 3 billion dollar taxbreak so they can continue to try to keep house prices high and young talent leaving the country. It's infuriating but that's culture war narratives for you.

Young people were leaving in droves during the Labour government's time in office, and that was when there was no tax-break.

Young talent leaves because it is more exciting in Australia and there is more money to be earned.

We've been hearing about the brain drain for like forever - it's nothing new.

Next you will be telling me that Bruce McLaren left because of high prices.

It's like you didn't even read the post of the actual young people above who are leaving and just made up your own story.

Like I said, culture war narrative. Evidence and facts are optional. Feels and anger at 'the other' are truth.

He didn't make up anything, Hipkins welcomed the mass exodus when he announced,

Prime Minister Chris Hipkins has welcomed Australia’s historic decision to provide a new direct pathway to citizenship for New Zealanders living in Australia, saying it will bring the two countries closer together.

kiwis did not leave to Australia because of interest deductibility. lol.

Agnostium, I'm not sure if you have any evidence or facts, and you resort to ad hominem attacks rather than reasoned debate.

"Why spend $1.2m to buy a shit rundown 70s house with a 30 year mortgage?"

Wherever people choose to work, if the house price risks are high in that location, then it might be better to rent rather than buy.

Refer example of Peaker vs Buyer today.

Dear Doctors who are leaving for Australia. Let me give you some hot tips.

1. Salary sacrifice everything you can. As health care professionals you get automatic industry wide salary sacrifice benefits so that the first $30k you earn is effectively tax free. But you can usually salary sacrifice up to $50k a year without incurring FBT, and everything salary sacrificed (car, mortgage, child care, food bills etc) is a 45% saving (the top tax rate).

2. Doctors qualify for special mortgage deals, such as lower interest rates, and being up to borrow 95% without paying LMI.

3. Buy an investment property and negative gear against your personal income, again saving money by reducing the 45% top tax rate.

4. Obscene money is on offer if you are prepared to work in remote or rural areas, particularly in the NT.

. Height of properties being withdrawn was mid year. Many will have been put into the rental pool leaving them unlisted for sale for another perhaps 6months+ waiting on the hope that the market picks up. It'll be interesting to see if there's another uptick in listings early 2025 from those withdrawn mid-2024.

This Friday I feel a few banks will jump to the sub 5.5 wholesale :)

Champagne, brought to you by L E V E R AG E.

Wow, almost 100 houses per day being withdrawn from the market as they didn't sell.

I called the bottom as October / November. Looks like I might have been right, but let’s give it a few months and see

It was July.

Really? I feel like you mocked me a few months ago when I said we were near the bottom...

Selective memory happening yet again Jimbo?

Refer my comments on 20 August, and the rubbishing they got from IT Guy 😂 Near the bottom of the thread. And I said it on several occasions

https://www.interest.co.nz/property/129287/house-prices-continued-tumbl…

Yeah wait and see. I don’t see much in this article or anywhere else that suggests house prices are going to start rising quickly again, and I hope they don’t. I’ve got three well educated kids in professional jobs and I would like them to be able to have kids and stay in this country so I can enjoy my grandchildren. I want to see a general reduction in living costs and an increase in standard of living and I can’t see either of those things happening if self centred arseholes are hellbent on exchanging ever increasing amounts of money with each other for non productive assets.

If your kids are well educated in their 20s they won’t be staying in NZ. They’re much better to go OS no matter how affordable you want property to be here. When they’re ready to have your grandkids they will be back. Mid to late 30s. 10-15 years OS with great experience and savings they will be able to live in a very desirable area. That is how it goes for most.

I think we can make the call now we were both right.

by Zwifter | 20th Aug 24, 9:24am

Tauranga pretty much stable. Expecting a rise from here. Probably a bit late now to see my predicted 3 to 4% gains this year but a few more OCR drops will see that happen next year.

by JimboJones | 13th Aug 24, 8:39am

I don’t think there was a big lag last time Orr lowered rates. There are plenty of investors and FHBs ready to jump in and get a “bargain” once they feel the bottom has been reached.

I am not making any predictions as I’ve been wrong many times in the past on house prices (normally too pessimistic!), but I certainly wouldn’t bet against this being close to the bottom assuming interest rates drop. It will probably take a while to clear the inventory this time.

https://www.stuff.co.nz/nz-news/360487972/developer-argues-660-affordab…

take a look at the flood photos, this is such a stupid idea, how and who will insure these sites?

In Auckland

https://www.rnz.co.nz/news/national/531808/catastrophe-in-the-making-fa…

Potential future financial risk for council (and future rate payers).

"Hills said the council was currently buying out 900 homes damaged in the storms and deemed to pose an "intolerable risk" to human life."

This is the site I've mentioned previously a few times. Some commenters thought the developers got a bargain buying that land at ~$1M/Ha (don't have the exact numbers to hand). The sellers would have been laughing all the way to the bank.

I have chosen to simplify the numbers so people can work out if there is a recovery or not:

30 houses for sale at the start of Sep

+9 new listings

-6 were sold

-3 didn't sell and were withdrawn

= still 30 houses listed for sale at the end of the month

Add (000) to the above and thats the NZ market!

Oct will be similar

How do the numbers stack up?

- 11,572 new listings

- 6,681 sold

- 2,580 withdrawn

That's 9,261 properties out, 11,572 in, or a net gain of 2,311 properties. Yet the article says the stock declined

What am I missing?

nothing

Really? I thought I'd missed something too. Maybe Greg can answer?

Someone can spot the framing effect.

Approx. 4,000 cases of arson.

What am I missing?

Journalistic value add?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.