Despite recent falls, house prices remain "stretched" for prospective buyers, and are around the top of the Reserve Bank's estimate of "sustainable levels".

The RBNZ makes this comment in an Update on the Housing Market, which will be in the central bank's six-monthly Financial Stability Report coming out on Wednesday next week and has been released early.

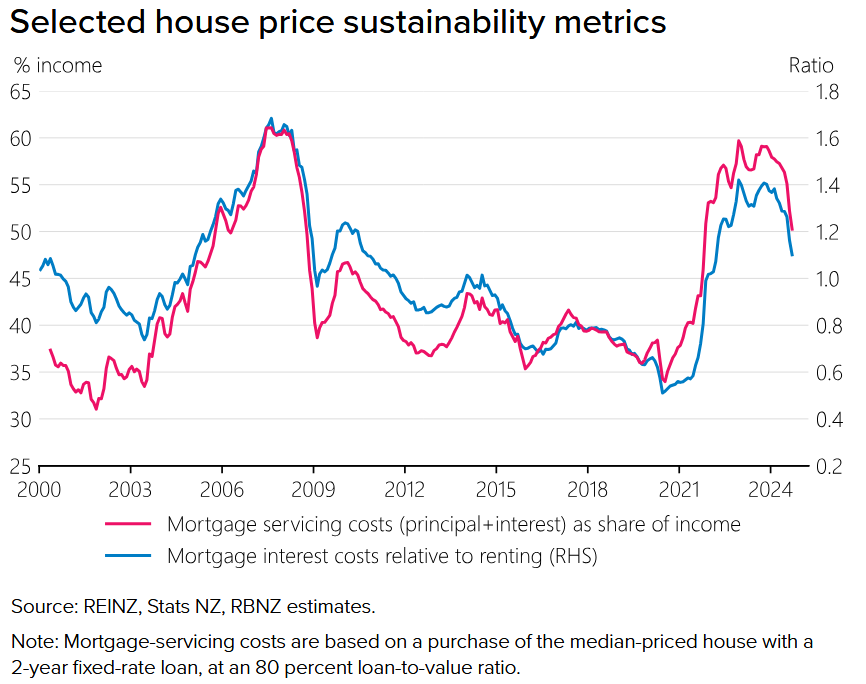

The update, authored by RBNZ adviser, financial system analysis, Charles Lilly, says to assess the sustainability of house prices the central bank considers the mortgage servicing costs for a new buyer, both relative to average household incomes, and relative to the alternative option (renting).

"These two indicators rose rapidly as house prices were peaking in late 2021, and they have remained at historically high levels," he said.

"Overall, our metrics for house price sustainability suggest that current levels are around the top of the indicator range. This assessment is based on interest rates returning to neutral levels," Lilly says.

Comparing New Zealand’s recent house price cycle with overseas, Lilly says our cycle "has been rapid", but with comparatively less financial system stress.

"Debt-servicing stresses are currently elevated and non-performing loans continue to climb. However, New Zealand has not yet seen the same widespread household balance sheet distress experienced in countries with similar house price boom-bust cycles."

He said banks’ lending standards have meant borrowers "have had financial buffers in place to handle shocks".

"Stringent testing of new borrowers’ servicing capacity has meant they have been able to absorb large increases in interest rates. Loan-to- value ratio (LVR) requirements, including speed limits applied by the Reserve Bank, have meant that borrowers can absorb substantial price declines without falling into negative equity."

"We estimate that less than 2% of the current stock of lending is to borrowers in negative equity."

Lilly also noted that house prices were at or near their peak level for only a brief period.

"This meant that a limited proportion of buyers from recent years purchased their properties at prices close to the peak. A prolonged period of purchases at unsustainable prices would have led to a larger accumulation of risk."

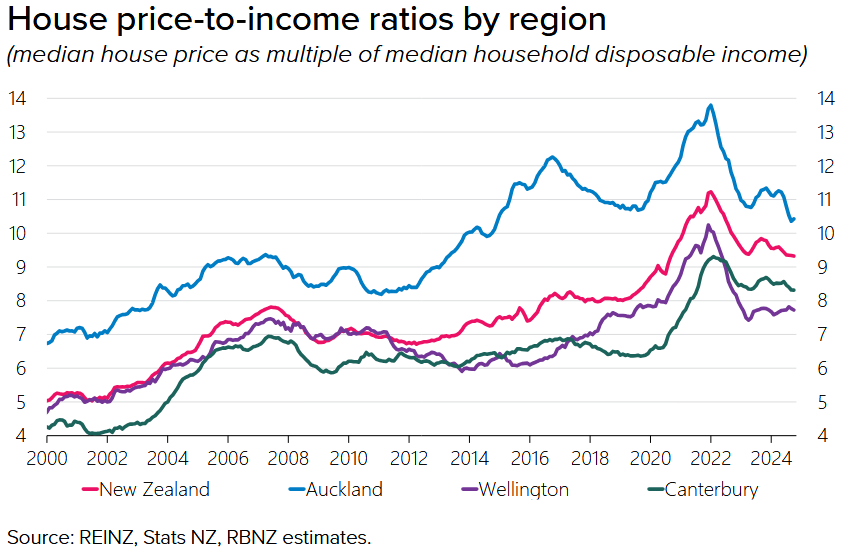

Lilly said from their peak level in late 2021, house prices have fallen an average of 14% nationally, although with significant regional variations.

"Auckland and Wellington prices fell 20% and 23% respectively, and have remained relatively flat over the past year. In contrast, prices in Canterbury experienced only modest declines, and have strengthened over the past 18 months. House price-to-income ratios have declined significantly from their peaks."

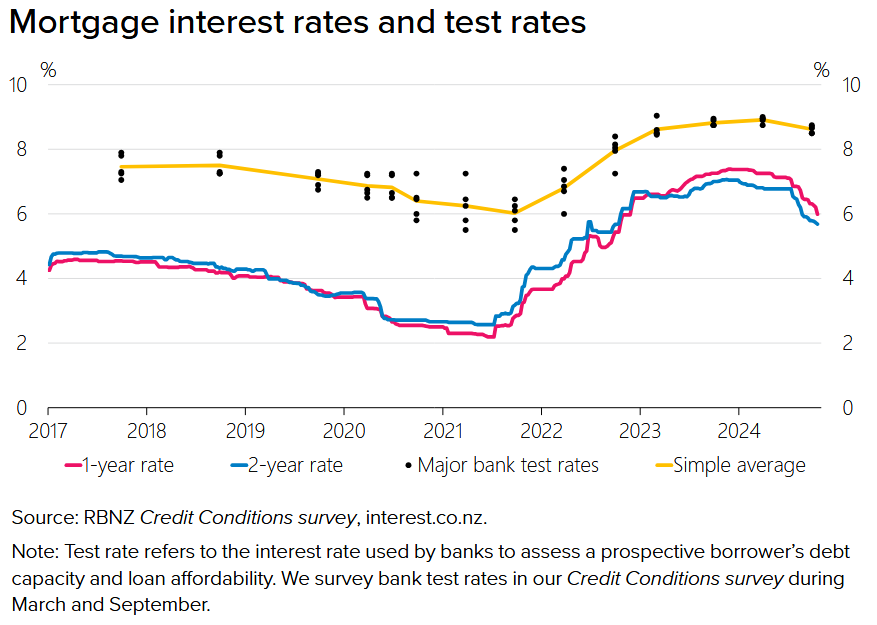

Lilly said advertised mortgage rates have begun to decline over recent months, but they remain at relatively high levels.

"This is continuing to constrain the borrowing capacity of potential homebuyers. The test interest rates that lenders use to assess borrowers’ debt-servicing capacity have fallen, from an average of 9% in mid-2024 to around 8% in October."

"Banks typically apply a buffer above the average of the 1- or 2-year fixed mortgage rate, although there is some variation in methodologies. Banks generally review their test rates on a quarterly basis."

"However, given the rapidly changing interest rate environment, some banks reported that they will review their test rates more frequently."

"Borrowers’ capacity to take on more debt could increase quickly given further easing in monetary policy."

Lilly said that with low overall lending growth, banks are facing "competitive pressures" to attract a limited pool of creditworthy borrowers. The slowdown in New Zealand’s population growth due to falling net migration is also dampening housing demand.

He said investor activity remains weak, "but may pick up following tax policy changes".

He notes that the deductibility of mortgage interest costs from taxable rental income will increase to 100% in April 2025, from 80% currently.

"Deductibility improves investors’ debt- servicing capacity and will increase investors’ valuations of existing properties."

Since July, the ‘bright-line’ period for assessing the taxable status of capital gains on investment property has been reduced to two years from 10 years.

"This change could increase speculative housing purchases, at the margin.

"In the short term, the change means that investors facing cash flow pressures from high interest rates may seek to sell properties they had been holding on to, due to the previous longer bright-line periods that applied."

Lilly noted that the annual number of new dwelling consents has fallen from its high of 51,000 in 2022 to around 34,000.

"This remains substantially above the level that consents fell to following the Global Financial Crisis (GFC), and is closer to a level that the construction industry can deliver on a long- term basis."

He said the large pipeline of consents from recent years continues to convert into completed houses.

"Industry contacts reported a potential glut of new townhouses in Auckland in recent months, given currently weak demand. A material share of the current property listings in Auckland and Canterbury are new build properties."

He said, however, that "prudent lending standards by banks" through the boom period mean that any surplus supply of new builds is unlikely to lead to material loan losses for them.

"Typically banks have required that the value of presales covers at least 100% of any borrowings.

"However, some non-bank lenders that provided additional financing, subordinated to the banks’ financing, may take some losses.

"Developers with unsold stock may also face equity losses if they are unable to achieve their desired prices."

Banks and industry contacts have reported that presales of new builds have been weak.

"Buyers in the current market have the option of purchasing completed new builds, rather than committing to lengthy waits for developers to build off the plans."

Lilly said banks have now generally eased their presale requirements for "high-quality developers who have established track records", to around 70% of borrowings.

"Banks want to maintain market share, and feel a competitive pressure to build back up their lending portfolios as projects complete and existing loans are repaid.

"The Government has announced an underwriting initiative to support new developments given the weakness in presales.

"The slowdown in the development pipeline, combined with some financial stresses among developers, has seen many firms exit the industry.

"Although this is to be expected at the end of a development cycle, a large drop in industry capacity would impair supply responsiveness to future increases in demand."

Lilly noted that in July 2024 the RBNZ had activated limits on banks’ high debt-to-income (DTI) mortgage lending.

Under the rules, banks can lend no more than:

• 20% of new owner-occupier lending to borrowers with DTI ratios greater than 6, and

• 20% of new investor lending to borrowers with DTI ratios greater than 7.

Lilly said DTI limits will act as "guardrails" on banks’ lending without needing the RBNZ to regularly adjust the limits.

"If interest rates decline, borrowers’ DTIs are likely to trend up, and the policy setting will effectively become tighter. This provides an offset against the potential build-up of financial stability risks."

120 Comments

I feel FHB's need to consider very carefully if they're nothing more than cannon fodder for the many who now want to exit this game and actually bank some gains while they still can. I think with a backdrop of rising job insecurity, it's hard to justify a sane case for any significant upside from this point in the medium term.

Hearing reports of property flippers and property traders being more active in the market as buy and hold isn't feasible (i.e negative cashflow) and self financing for most properties.

Have also heard of some non owner occupiers willing to buy negative cashflow properties for capital gains and hold beyond the brightline test period. (Of course their stated intention at time of purchase to the IRD is for rental income.)

@ CN - You seem to hear a lot. Shouldn't be so nieve as to believe everything that you hear.

How long should a young couple wanting to start a family hold off getting a house to call their own RP?

While mortgaged, the house belongs to the bank. Financially speaking, the more time invested in the preparatory stage greatly increases the chances of a favorable emotional and financial journey/outcome where the owner actually owns and the bank doesn't. Metaphorically speaking, would you want a car painter to rush the preparation stage restoring your classic, just so you can have it back sooner? These are worthy up front considerations and considering it's the biggest purchase of a lifetime, there need be no hurry to rush in and buy.

Again, I'm not saying don't buy as some here are trying to twist it.

i'm not saying don't buy i'm saying don't not think about buying.

What do you consider reasonable preparation to buy? 20% equity?

by RookieInvestor | 31st Oct 24, 2:10pm

i'm not saying don't buy i'm saying don't not think about buying.

Oh-boy, another one who finds rational up front considerations detestable.

I'm not saying don't buy. I'm just saying that if you do buy then you are likely to be cannon fodder.

TronMVP, have you ever considered the possibility that you're a selfish DGM? One that struggles to comprehend sound advice that's clearly tilted towards the wealth preservation of others than yourself? You're better than this surely.

Perhaps try and view things in a more positive light?

You lost me there, RP.

You are saying I'm a DGM on what basis?

You are saying I'm selfish on what basis?

You are saying that you give sound advice on what basis?

So you have no other option than to be obtuse? Really? Lets fill the thread with heaps of back and forth so you can complain about that too - LOL!

Deep down, I know you know where I'm coming from. As a house owner, I still consider the next generation and feel there's a duty to inform them of the growing risks.

@ Retired Poppy - You seem more bent on scaring & disincentivizing tenants from ever being owners themselves or striving towards home ownership, rather than "informing them of the growing risks". Why all the scaremongering around buying? Are you yourself guilty of trying to protect your hoarded wealth through property so to disencourage the next up & coming generation from purchasing? I would've thought someone advocating for more tenants into homes to paint ownership & the achievement of such in a much more positive light.

Reasonable preparation to invest well:

- Goals defined

- Financial forecast on a gross and net yield basis done for your leading investment scenario for every year up to your investment exit horizon date

- Stress test the financial forecasts

- agreed the criteria for staying the path vs exiting

- Rainy day funds put aside

- Due diligence list made with help of experienced people, and money put aside for due diligence on multiple properties

- Purchase if an opportunity meets your investment criteria

- Monitor the leading indicators where changes will need to be factored into your revenue or cost structure

- Consider value adds, BRRRR options

- Execute the exit strategy when the indicators head out of the allowable levels

Purposely didn't include deposits in the above, as they are simply an equity buffer for you in case of financial stress, and risk reducer for the bank

I'm not saying don't buy

By jove you could have fooled me!

@ Retired Poppy - "where the owner actually owns and the bank doesn't"

Anotherwords this suggests don't have kids until you not only own a home, which only just over half the country manages to achieve, but also until your home is mortgage free as well. Given that a good portion of owners still have mortgages well into their 50s, & some even into retirement, this not very practical advice. Do you have any kids yourself Retired Poppy?

Young people are damned if they do and damned if they don't. One things for certain, you cannot blame them for the housing market we have today.

- "Don't buy, wait for the crash" or "How long do you wait?".

- *Market takes off*

- "Why did you wait? Property prices always go up"

- *Market tanks*

- "Why did you buy? It was patently obvious the market would crash and interest rates would rise"

One things for certain, you cannot blame them for the housing market we have today.

Spot on.

"One things for certain, you cannot blame them for the housing market we have today"

Is the current housing market the unintended consequence of this policy decision in Dec 2016?

https://www.interest.co.nz/property/85201/reserve-bank-confirms-meeting…

The policymaker has since long left the scene.

Young people would be better off if the RBNZ told the banks not to lend to them?

"Young people would be better off if the RBNZ told the banks not to lend to them?"

Banks would still be lending.

Given that NZ house prices have risen by 130 percent since 2011, there are plenty of people who are happy owning the roof over their head - and avoiding paying rent. Taking a long-term view of the property market pays impressive dividends.

Those who listen to the doomsayers haven't got much to crow about. Sadly, as the years and decades roll on, they get further and further behind but still learn nothing .......

They go to bed each night - dreaming of owning an avocado.

TTP

Plenty of young Know are p##d of they got sucked in to the fear. Mortgaged to the hilt, in undesirable suburbs, want to start a family but the neighbourhood going backwards with ferals.

They cant sell, cant move, cant take out of town promotions. They fee completely f##d over because they got suckered in the the property ladder,,

Take a bow banksters, politicians, media and RE agents.

"They cant sell, cant move, cant take out of town promotions"

Some owner occupier owners are also unable to upgrade.

https://www.oneroof.co.nz/news/homeowners-loan-requests-rejected-they-h…

Others have had to realise losses

https://www.stuff.co.nz/business/property/301009099/new-zealands-unluck…

https://www.stuff.co.nz/business/property/301010041/the-wellington-hous…

@ Rastus - "Plenty of young Know are p##d of they got sucked in to the fear. Mortgaged to the hilt, in undesirable suburbs, want to start a family but the neighbourhood going backwards with ferals."

Really? Because I'm pretty sure the young who are renting, who got sucked into the fear of not buying are p##d that they listened to the chicken little sky is falling property skeptics telling them that there's never a good time to buy so don't even bother. Their rents have significantly risen in the process. Whilst tenants cannot sublet out to other tenants to help pay for the increase in rents, owners do have the option to rent out their rooms to help cover ant increase in costs associated with the rise in interest rates.

by tothepoint | 3rd Sep 21, 8:39pm - "NZ house prices are increasing - on a sustainable long-term trajectory"

Notice in 2021, Tim used the key word "sustainable" and yet he has never admitted on here he got this so fatally wrong. He dodges this by using BS like property does increase over the longer term. Yes Tim, most things do. It's called inflation.

Long-term trajectory is the critical point, Retired-Poppy.

But you still fail to acknowledge (or understand) the long-term and its relevance to property ownership/investment. The comments you make here are invariably trite/banal.

The reality is that property has performed remarkably well in the past and is destined to continue performing well across the longer term future. Indeed, the world's largest asset class may well become even larger.......

Your mentality/obsession with the short-term leads to the messes you continually get into here.

Successful property investment calls for a long-term focus, analysis and strategy. Seasoned property people are fully aware of that.

TTP

The current housing market is the unintended consequence of many economic policies and human decision making long before 2016.

One could also ask is it unintended?

@ CN - Nice try to blame a government from nearly a decade ago, for the last governments failures. Most people can see right through it now, hence why they lost the last election.

Debt to incomes ratios are now implemented.

It is well known that the government of unintended consequences was of course the last 6 years under Labour. It is their ill thought out policies such as no clause terminations, extension of brightline capital gains tax to 10 years, removal of interest deductability, failure to build the 100,000 homes they were solely elected in to do, that has caused "the housing market that we have today".

Like most decieved Labour voters, you don't hold your government accountable for their failures, instead choosing to scapegoat to governments from a decade ago as an excuse. By your logic, we cannot hold current governments accountable for any failures under their watch, but must instead blame previous governments. This means that any failures under the current National government can be blamed squarely at the feet of the last Labour government. Don't worry though, the majority will look forward to holding Labour finally accountable, since their decieved voterbase will not. "Let's do this".

https://www.newshub.co.nz/home/politics/2016/08/john-key-blames-helen-c…

https://democracyproject.substack.com/p/govt-housing-deregulation-is-a-…

https://www.nzherald.co.nz/business/who-wins-from-doubling-aucklands-po…

Let's see if we can keep the current mob accountable.

"Let's see if we can keep the current mob accountable."

Property owners would save about $800 million each year on tax, he said.

"That is money that will be divided between landlords and renters alike."

Checkpoint asked an expert how much property owners would save each week. The owner of a $750,000 property with a $500,000 mortgage could expect to see about an extra $160 a week, they said.

When presented with those figures, Seymour said he expected to see a "pretty even split" in how the saving was divided between landlord and tenant.

https://www.rnz.co.nz/news/national/511411/no-way-renters-will-benefit-…

At least one generation has been rooted by house prices already. What's another? But - if it wasn't house prices, it'd be ridiculous DTI's to manage the ever growing demand (immigrants need somewhere to live contrary to popular opinion) and lack of supply. You can't regulate your way out of fundamentals - either build more, reduce immigration, or both.

Allowing investors interest deductibility but not homeowners the same is going to push house feasibility out of home buyers hands. I don't think any debt interest should be tax deductible. The banks love it though, so we won't see that fix any time soon.

Alternatively bringing back land tax and using the proceeds to reduce GST and income tax would see a massive shift in investment, productivity and living costs in NZ. And I would have no problem with interest deductibility for landlords then.

CGT for investment properties, will come, along with more taxes on investment properties... further caps on immigration and a labour win at the next election.

We have to find a way to reduce the exodus of skilled young kiwis.. to do that we have to reduce house prices, improve public services and create interesting careers and businesses... and to do that we have to make a ton of changes to a ton of policies which I think will favor a more socialist approach.

Investing in property now is a fools game.

CGT only makes people less likely to sell their properties and does nothing to keep land values under control. It's not the solution to the housing cost issue. It does increase tax fairness a bit though. I agree with further caps on immigration until housing is under control in this country.

If you want to stop the exodus of you productive working people, bring back land tax, and decrease GST and income tax. That would solve so many problems.

Land taxes are likely to be annual, thus the tax would flow directly and immediately into rents. A well designed CGT only comes with a sale. See the difference?

If a CGT is seen as inevitable, then selling sooner rather that later would make sense. Especially if the CGT is 'well designed' and backdated to 1900 so it immediately starts collecting revenues.

At this point it should be abundantly clear that rents are set by supply and demand and tenant incomes.

As yields increase so do land values, so mortgages increase to absorb any increases in the rental market. You might have noticed that in the years after the GFC with falling interest rates, rents continued their inexorable rises, and they actually fell inflation adjusted as interest rates decreased. https://www.interest.co.nz/property/93555/rodney-dickens-doubts-landlor…

The actual impact of land taxes would be to reduce rents, when you have land tax you have pressure on landholders to develop as much as the market requires to maximise rental returns, which in turn creates more rental space supply and competition which actually reduces rents. Apply pressure to landholders, and we'd have plenty of housing. And the added burden on land of LVT would mean that yields per house are reduced in two ways, lower rents, and increased expenses, which would mean that land values would be significantly lower.

You are right, Ocelot. And I agree.

Where I disagree is that a land tax is the sole answer.

A 'well designed' CGT is far more comprehensive.

@ OldSkoolEconomics

A captial gains tax for investors already exists, called The Brightline Tax. It's been around since 2015, keep up. Your old school economics are clearly outdated.

The Bright-Line Property Rule (also known as the "bright-line test") is a law that determines if tax needs to be paid on profits made when a property is sold. It does not apply to properties acquired before 1 October 2015.

Like a capital gains tax, the bright-line rule calculates the difference between what you bought and sold a property for. It then applies an income tax charge on qualifying homes.

https://www.moneyhub.co.nz/bright-line-test.html

"The bright-line test is basically an objective capital gains tax for residential land bought and sold within a defined timeframe."

https://www.bdo.nz/en-nz/services/tax/the-bright-line-test?gad_source=1…

" a labour win at the next election" - You actually believe that? Sounds like you've had too much socialism not enough economics. 75% of the country chose not to vote Labour a 3rd time. That doesn't mean they voted National, but it does mean they didn't want Labour. That's a landslide fail for Labour. Unless Labour has a significant change, there will not be another Labour lead government for at least several terms minimum. Considering their current leader can't even define whay a woman is, & lies to the public on National TV about forced vaccinations "everyone made their own choice" he reckons, he clearly can't be trusted if he thinks the NZ public are that blinded to his constant contradictions. You speak for the minority when you wish for another 6 years of Labour, but the majority disagree with you, they voted that out. Labour expected businesses to operate out of charity, & kindness mantras, about as far from economics as one can get.

"a ton of policies which I think will favor a more socialist approach." - Again, we had 6 years of socialist policies, & it not only created the largest devide since the 1940s in our countries history, but also created the largest increase in both property prices, rents, emergancy social housing waiting lists, child poverty rates, family violence rates, retail crime rates, crime rates in general, & hospital health emergencies by the fastest growing margin in our countries history. Not to mention that Labours "great leader" called free speech an "act of war" & an "act of terroism" at her last UN conference towards the end of her tyanical reign. Many people also believed that Stalin was a great leader too, & he was pretty big on suppressing free speech & control as well.

This is well documented, but you socialists choose not to believe it as it doesn't fit your narrative. Socialists now choose feelings over facts. Your economics is outdated, you have replaced it with socialism & Stockholm syndrome. Take off your rose colored glasses, apply not only some basic business & economics, but some basic common sense as well. OldSkoolTyant would suit your username better. In the words of your great leader "Let's do this".

If homeowners are allowed to deduct interest, then they should also be required to pay tax on imputed rent. And renters should be able to deduct rent they pay.

"Allowing investors interest deductibility but not homeowners the same is going to push house feasibility out of home buyers hands. I don't think any debt interest should be tax deductible"

The previous policy of removing interest deductibility for non owner occupiers has now been reversed due to a desire by politicians to win the popularity contest overriding the policy needs of the nation to provide affordable housing. The property investors associations and their members lobbied their politicians, whilst there was no lobby group for those seeking affordable housing.

Before the interest deductibility was returned I was arranging to have my debts transferred to an Islamic bank that doesn't charge interest, only "fees". The expense was tax deductible. I expect banks in NZ would shift to islamic banking to accommodate the loophole. You don't need to be a muslim to appreciate being able to account for all your expenses in your annual tax return. Ironically, the removal of interest deductibility is a shift towards taxing revenue rather than profit. This is the exact same thing as GST which you want to see reduced.

Loophole? Seriously?

@ Ocelot - The reason why owner occupiers don't get interest deductibility that investors do is that home occupiers don't operate their home as a business. If home owners are prepared to rent out their spare rooms to tenants in need of accomodation, then they may have a justifyiable reason to seek interest deductibility. Currently they do not.

Every other business entity in NZ is able to claim interest deductibility. By Labour removing this right on property investing only, they were expecting that investors were to operate as a charity.

We as a society get to decide what gets to be tax deductible. Not all business expenses are allowed to be claimed. I think interest on debt against land should not be able to be claimed as a business expense. Just as I can't borrow money from the bank to buy shares, and claim the interest as an expense before I pay income taxes on the profits of the shares.

@ Ocelot - "Just as I can't borrow money from the bank to buy shares, and claim the interest as an expense before I pay income taxes on the profits of the shares."

Because your shares do not provide a service to the public, that's the difference. Your shares are only self serving. Now all businesses are self serving yes, otherwise they would be a charity, but businesses achieve this through a mark up on their service, as they are rightly entitled to do so.

"I think interest on debt against land should not be able to be claimed as a business expense."

We are dealing with facts, not feelings. I dislike tattoos, the permanent marking of one's body. It's often done young & dumb & many people tend to regret them later on in life, not to mention they look hideous on old singing skin. But despite how ever I feel about tattoos, & the service that a tattoo parlour offers, I cannot reasonably expect that a bunch of penalties are applied or that their ability to claim the same expences as other businesses are removed just simply because I don't agree with their service that they provide. We are dealing with facts here, not feelings.

The fact that your feelings are geared against the business of landlording & against the idea of then claiming an expence just as other businesses do is of course irrelevant.

Why do we need the RBNZ to tell u the obvious

Welcome back, Dgm

RBNZ is saying exactly the right things. Moral suasion is a legitimate part of its armoury. It's far preferable to outright coercion in the form of heavy-handed regulation.

Now is the right time for our central bank to talk down the housing market - strategically - given the risk of a bounce-back in house prices as (more) mortgage money becomes available at lower interest rates.

Kiwis' underlying fondness for houses remains intact - despite the risks of over-indebtedness. The latter can be ruinous to individuals - and badly damage the macroeconomy.

So I applaud RBNZ for keeping ahead of the game in order to preserve economic stability - and the welfare/wellbeing of all New Zealanders.

TTP

So I applaud RBNZ for keeping ahead of the game in order to preserve economic stability - and the welfare/wellbeing of all New Zealanders

ROTFLMAO! 🤣🤣

If you see National MPs offloading their investment properties, it might be a sign that CGT is on its way!

Wouldn’t that be a form of insider trading? (Ie illegal…acting on non-public information for personal financial gain)

What politicians say and do are two mutually exclusive things.

"Wouldn’t that be a form of insider trading?"

No. It wouldn't.

@ Chairman Moa - Do only National MPs own property? No wonder why Nationals governing, we don't want the entire country run by a bunch of entitled tenants like how they run their finances.

Those who bought in Auckland central at the market bottom midyear will be already enjoying the rising price trend. 4% up in the last 2 REINZ HPI measures.

Auckland leading the pack again, not so much job fear in the leafy suburbs 🌿

Another .50 or .75 OCR cut in a few weeks will be most pleasing! 🥂

No doubt there are National and ACT MPs who are selling properties to upgrade to more expensive properties - especially with interest rates falling.

TTP

We have yet to see any new purchases in the pecuniary interest filings, but its a good story TTP

@ TTP - If one is buying & selling in the same market, then any capital is counterproductive, as an increase in capital when selling likely means one will end up paying an increase in capital for the next property as well.

Why would National & Act MPs sell at the bottom of the largest property price decline in over 40 years, hoping to get top dollar to purchase a Mcmansion? This logic makes no sense. You sell when prices are high, you buy when prices are low. With financial advice like yours, you should stay away from investing in anything, & save yourself the trouble of loosing money too quickly for making the wrong decision of when to buy & sell.

Also, Do only National & Act MPs own property? Do all Labours MPs rent? They ran the country like renters, so maybe they do. What difference does it make if an MP sells their personal property, regardless of what political party they belong to?

Hi Côte d’Azur, a genuine question - will you be upgrading your account in March?

Or will you go back to using the Yvil account full time with the green tick?

Hi Côte d’Azur, a genuine question - will you be upgrading your account in March?

Or will you go back to using the Yvil account full time with the green tick?

Thanks for your input Yvil, and please forgive my scepticism but my understanding is:

- Yvil is French

- Yvil also lives in the central suburbs

- Yvil echos the same sentiment

- Yvil was in Côte d’Azur in September

I'll leave the reader to ponder this… around what time would Yvil start thinking about or planning his European vacation?

It turns out the Côte d’Azur account was created 16 months ago…

I think Yvil is Swiss, and I'm sort of playing the devils advocate here.... why the conspiracy?

He's Swiss-French

Way I see it : "cote-de whatever" is a troll. Likely one of the most pointless posters on here...absolutely pointless. I personally feel that Yvil is a decent poster, and agree or disagree has posted some thought provoking stuff over the years. My advice: ignore the trash, uptick the good. Way easier than going down the rabbit hole.

Nothing necessarily wrong with having the odd smurf account in general, although David's stance on the matter might be different?

Let's say it is Yvil. Means he can keep his quality commentary with the Yvil moniker and if he feels like trolling a bit, he can always switch to Côte d’Azur. Maintains the reputation of his main account and makes it unlikely to get banned if he pushes the envelope too far.

by Time Lord | 31st Oct 24, 12:17pm

Hi Côte d’Azur, a genuine question - will you be upgrading your account in March?

If you are truly a "Time Lord" should you not already know the answer to your own question ?

Hi Yvil,

I reckon he’s a Drug Lord, so forget his “Time Lord” bullshite. He’s masquerading.

No doubt he operates a cartel. As sleazy as……

TTP

I note there is no denial in your response.

Must be the excitement and thrill of potentially catching some stranger out on the internet for having a smurf account on a financial news website.

Aotearoans are somewhat myopic and I feel sometimes we need to look what's happening elsewhere for perspective.

For ex, in the US 30-year mortgage rates aren't slowing down. Now at 7.37%, the highest level since early July.

https://www.barchart.com/stocks/quotes/AFXY30US.RT

US banks are currently sitting on $750 billion in losses on real estate debt - a magnitude 7x greater than it was in 2008 when the housing bubble popped. As of now, 47 out of 1,027 American banks with assets over $1 billion have liabilities and losses exceeding 50% of their capital equity. This situation underscores the precarious position many banks find themselves in as they navigate through high exposure to real estate debt amidst fluctuating interest rates.

https://www.fxleaders.com/news/2024/10/27/u-s-banks-face-750-billion-in…

Quite the ray of sunshine today, aren't you J.C.? ;-)

But let's keep some perspective. (For those that don't know how bonds are valued, when interest rates rise, existing bonds fall in value, conversely, when interest rates fall, existing bonds rise in value.)

That second link says: "The extent of these unrealized losses depends on the direction of Federal Reserve interest rates.". Can you see the Fed not reverting to neutral? I can't. Although another energy shock could see yet another round of inflation (albeit it won't be as bad as the last as the global economy has re-structured quite a bit since Pootin invaded Ukraine).

That second link says: "The extent of these unrealized losses depends on the direction of Federal Reserve interest rates.

The Fed has already been bailing out the banks through the Bank Term Funding Program (BTFP), the lending initiative established by the Fed in March 2023, aimed at providing liquidity to eligible depository institutions like banks, credit unions, and savings associations. BTFP was designed to stabilize the banking system by offering loans of up to one year to eligible institutions that pledged high-quality collateral, including:

- U.S. Treasury securities

- Agency debt

- Mortgage-backed securities

These assets were valued at par, meaning the Federal Reserve would ignore market fluctuations in their value when determining loan amounts. This feature allowed banks to borrow against their securities without the pressure of selling them at a loss during periods of financial stress.

And yet here we are.

This feature allowed banks to borrow against their securities without the pressure of selling them at a loss during periods of financial stress.

This is insanity. It beggers belief just how many tweaks to the system and new lending miracle rules have been implemented since the derivatives market was invented to save the day at the time. It is clear, fiat is flawed and like an old car, there's only so many parts to be replaced and mods that can be done before the old girl carks it and many are left in the lurch.

Fiat itself isn't flawed. Money is merely tokens, their value is the ease of exchange. We've simply learned, been taught to believe they have more value. Much like gold.

At least with gold as the token of exchange we knew the limited supply kept things relatively in check.

Problem was even then we had alchemists pursuing the concept of turning lead into gold. They figured out how to do it with fiat.

The flaw is in humanity's beliefs, values and evolution. Instead of evolving and learning how to co-operate, create ways and means of wisely living together with each other and our natural environment, we went on the warpath of a dominance, master/slave mentality. All we've done is change masters.

Thank you.

Well put, though there are still many places that haven't caved to the individualism of the west in their core values. Places like these don't have the comforts and living standards of the west however, and whether this is a positive or negative depends entirely on your own values and interpretations.

Yep I realise that too. It highlights that the western colonialist mentality still exists only in a different form. The belief that we're lifting others out of poverty and everyone wants to live like the West.

The majority of Western travellers will visit familiar environments and never really experience other cultures, ways of living. A majority of U.S citizens may never leave their own state, only learning about the world from the media, or will impose their own values on to other "undeveloped" countries.

“"If interest rates decline, borrowers’ DTIs are likely to trend up, and the policy setting will effectively become tighter. This provides an offset against the potential build-up of financial stability risks."

Why would RBNZ even consider allowing DTIs to increase if interest rates dropped? That’s how we got into this problem in the first place. Their bungling and light touch regulatory approach has been driving all this fiscal risk.

For all the PhDs and fancy pants degrees hired at the central banks, you get the feeling that they're largely winging it within the boundaries of their bureaucratic protocols and dogma.

Debt to income is simply a ratio - the RBNZ can cap the ratio at a maximum the banks are allowed to accept, but cannot stop it trending up towards the cap. If you choose to borrow more as interest rates fall, the amount you pay stays the same, but your DTI rises. DTIs will rise until everyone hits the maximum allowed.

Holding the line on DTI when interest rates fall is the whole point of having a DTI limit. A backstop against the house price craziness we saw in 2020-21.

Then again, the RBNZ did ditch the LVRs at the first sign of trouble so they don't appear to act well under pressure.

Wouldn't lowering the DTI's as interest rates fall make more sense?

And why the higher number for investors? It's almost as if they're encouraging investors over owner occupiers. Or do they think they're protecting the FHB?

Excellent questions!

Were our central bank to answer them, we'd see how beholden they are to overseas banks.

RBNZ: "If interest rates decline, borrowers’ DTIs are likely to trend up, and the policy setting will effectively become tighter. This provides an offset against the potential build-up of financial stability risks."

I took that to mean the RBNZ doesn't intend to jerk the DTI Ratios around like they have with the LVR Ratios.

Ho hum. At 6 for OOs and 7 for 'investors', I feel they're just a little too loose.

Munny is like a water in a bath, sloshed around by the banksters. as to where it should be allocated (or not)

They know things are nothing like 2021 ....even bond interest rates are now back on an upward trajectory.

Interest rates are all about the "cost" of money, so if bonds go up, mortgage rates will follow (as the banksters have to make a profit - their prime "modus operandi") ....so anyone here wishing for mortgage rates beginning with a 2 or a 3 are just dreaming.

While if the banksters got desperate, they could lower rates to keep the "property ponzi party" going, but they have to find funds that can provide them with a margin, so to make their lending profitable..so fat chance there.

The "PPP" is well and truly over .... if the purchaser can get finance, they will be outbid for quality, well located property - while your damp, drafty sh*tbox, that has been rented for years with nothing spent on it, will keep going down until it "meets the market" where:

a) it can be renovated, without over-capitalising

b the purchase price and rent gives at least an 8% gross return

c) it will sit on the market forever, as the vendor won't reduce the price

c) would be the most likely scenario and already happening - so buckle up folks, sure house prices may not fall as much from now on - but they won’t be going up either !

The upshot of all this, is that the PPP was always based on "endless " capital gains !

While if the banksters got desperate, they could lower rates to keep the "property ponzi party" going, but they have to find funds that can provide them with a margin, so to make their lending profitable.

Wholesale funding from Japan. To some degree, this has already been happening.

Not a bad idea J.C. - but cast your mind back to a couple of months ago, when they raised interest rates by 25 basis points - Margin call !...and the aftermath that followed ...

I was aware. The water cooler crew in Aotearoa just yawn.

Australia is experiencing the same problem - new builds are simply not financially viable anymore, so even consented and approved developments are now being parked rather than proceeded with.

Shifman argues that every square metre of a new apartment costs three times as much as that of a good-quality townhouse, and four times as much as a new detached home in the outer suburbs.

“The only apartments that generate a suitable return on investment are premium boutique apartments targeted at wealthy downsizers,” he wrote.

... estimates that it is difficult to build even a mid-spec, 85sq m apartment in Brisbane for less than $1.3 million, and that only the upper end of the market can afford such a price.

The viability challenge has even stalled projects that have gone through the planning process and have development approval.

KPMG estimates that more than 34,000 new homes, largely in apartment and townhouse projects, were stuck in development approved limbo at June 30, with 12,000 of them in Sydney alone.

Exactly. This is why I was calling a resi construction crash two years ago.

Soaring build costs + Soaring interest rates = construction crash

yet no one at the water cooler was buying it, and still aren’t really

build costs seem to have come back maybe 5% over recent months. We will need the OCR to go south of 2.5% to get a meaningful pick up in dwelling construction.

Another recent headwind, with a frankly unbelievable lack of reporting given its likely impact, is the massive increase in development contributions across large parts of Auckland

A builder friend (who does medium to high-end builds and renovations) has just sold 2 investment properties. He didn't say why, but was pretty glum when I asked how things were going, so I'm assuming the medium to high end builds/renos pool is drying up.

Definitely medium to upper-medium.

My impression was high end was doing ‘Ok’

But the pool has always been small. It will be the medium to medium high that justify keeping the staff on.

Sounds like we need a lot more deflation in many areas of the economy to get back on track.

"85sq m apartment in Brisbane for less than $1.3 million"

That's $15k per sqm. That's a premium build, in a good area. Representative? I think not.

Even the reserve bank is caught up the real estate spin

The heading should have been 'House Prices not Sustainable at Current Levels'

As current interest rates are not at Neutral rates this comment below from a RB employeee becomes a misspeak

"Overall, our metrics for house price sustainability suggest that current levels are around the top of the indicator range. This assessment is based on interest rates returning to neutral levels," Lilly says.

Comparing current house prices with future interest rate levels is a flawed methodology.

Does anyone at the Reserve Bank stand back and check that these articles include common logic?

So it's ultimately a debt servicing metric not house prices? Which doesn't address that it's the debt/credit creation that's the problem.

They're too blinded by their own spin trying to maintain credibility.

Here in Christchurch, the prices of townhouses are dropping like a stone. Developers cant sell the new ones, and owners cant sell the existing ones. The existing ones that were bought a few years ago have more wriggle room in the price, so owners can discount them. Then the developers are forced to discount their new builds to compete with the older ones. As a result, in my area new build 3 bedroom townhouses are now selling for the same price as 2 bedroom townhouses were being advertised for at the beginning of the year.

Yes good comment again. Recent sales at the townhouse development I live in have seen 4-5 years old, three bedroom townhouses selling for less than advertised new build 2 bedroom townhouses near, with relatively similar qualities.Further emphasises the construction crash that has only just started playing out.

Woofbrook offering a 5 year rental guarantee via their PM company.

Have seen this sort of thing before by several apartment and townhouse developers. In most cases whenever the final contract settles and investor funding passes to the developer, the PM company mysteriously goes into liquidation. The premium paying investor then realise that the market rental is actually quite a bit lower than the PM company was paying, and thus they overpaid for the "investment".

Proceed with caution.

Careful you'll have Theman3 on your back for even suggesting Wolfbrook is in anyway something other than a money making rock solid company.

"Careful you'll have Theman3 on your back for even suggesting Wolfbrook is in anyway something other than a money making rock solid company."

Theman3 is quick to defend any comment that questions the financial resilience and liquidity of Williams Corp. They merely make assertions with no evidence to support their unsubstantiated assertions. There is likely to be some undisclosed vested interest involved with Williams Corp.

If there are little or no sales by developers, how are developers managing to earn sufficient cashflow to continue paying tradies, materials suppliers, lenders and other creditors?

When Wolfbrook or Willisms Corporation start not paying their tradesmen or miss an interest payment to their shareholders, then you can comment.

Truth is that they are both operating very well and are profitable.

Anything to say otherwise is just plain untruthful.

Good luck with your obvious investments, tied up in the Wolfies and Willies property dev sector there.....I just hope that not too many, are betting it all, on the Dubbyas.

I have to chuckle when I see the usual DGM's calling for a capital gains tax on investment property. It is an implicit concession that house prices are still going up.

Take another look or perhaps the majority of NZers are DGMs... I chuckle.

most want it as a detterance and limiter of growth, we will soon see what happens, luxy almost sold all his first...

It's a great emotional hedge. Prices stay steady - good, we like stable prices in our society. Prices fall - good, FHBs have more chance of buying which is good for society. Prices rise - oh well, at least we will get some funding for public services from the few who benefit.

I have to chuckle when I see the usual DGM's calling for a capital gains tax on investment property.

It's two thirds of society saying "houses are for owner occupiers to live in, not for the greedy to hoard in multiples"

This debate is not going to go away. CGT on investment property - it's coming. If you are genuine about providing an essential public service over the longer term, CGT will not worry you as it will be all about the yield - right?

Why would i worry about CGT when houses are going back to 2012 prices RP?

Is that a prediction?

@ Retired Poppy - A capital gains tax already exists in NZ called The Brightline Tax. It's been in since 2015, nearly a decade. I'm surprised that you were not aware of this, or that you do not understand how you works. Do try keep up. A lot has changed in a decade.

The Bright-Line Property Rule (also known as the "bright-line test") is a law that determines if tax needs to be paid on profits made when a property is sold.

Like a capital gains tax, the bright-line rule calculates the difference between what you bought and sold a property for. It then applies an income tax charge on qualifying homes.

https://www.moneyhub.co.nz/bright-line-test.html

"The bright-line test is basically an objective capital gains tax for residential land bought and sold within a defined timeframe."

https://www.bdo.nz/en-nz/services/tax/the-bright-line-test?gad_source=1…

The fact that The Brightline Tax is for 2 years & not indefinite is irrelevant. You don't get more "hoarded houses" onto the market at cheaper rates by applying an indefinite tax penalty for owning. This is just basic maths RP.

We already know what happened when Labour extended the Brightline Tax out to 10 years - it didn't dampen Landlord demand at all, as Landlords are in it for the longterm. The Brightline Tax was implemented to tax short term borrowers - ie property flippers or property traders who buy & sell in a short period of time. Instead, it disincentivized landlords from selling, dampening supply levels, rising pricing further. Again, simple maths. Add to that simple math some simple logic - you don't get cheaper houses by making it more expensive to sell. You also don't get more houses for sale if it is made more expensive to sell.

What you advocate for is another envy tax. "how dare they have more than me, that's not fair, tax them until they have as little as myself". Your advocating for an indefinite capital gains tax actually acts against assisting more tenants into homes. Making the landlord pay more to sell doesn't make the rent cheaper, doesn't make it easier for tenants to save for a deposit. Any tax on gains is also considered at sale time, & tacked onto the end of what ever profit one wishes to make. So in the end it is a tax penalty that a would be first home buyer will ultimately end up paying. Again this pushes prices up, furthering tenants from ownership.

You should be well aware that Labours taxing, penalizing, restricting policies acted negatively in everyway for tenants. The evidence over the last 6 years is overwhelming - you incentivize, not penalize. You do not get a donkey through the corn feild by continuing to whip it.

Being Retired I would have assumed you had some knowledge of basic business & economics.

The bright line test at 2 years is effectively an income tax on "traders" flouting the intention rule.

At 10 years it's effectively an income tax on landlords flouting the intention rule.

Not the best tweaks to badly written income tax laws, but no politician wants to address the origin of the flaws.

Don't let the use of words like CGT fool you. And don't let the likes of BDO fool you either. They're reliant on the tax flaws for much of their existence.

Have you studied the Income Tax Act inside out or do you just parrot what you read and hear? Don't believe everything you read and hear.

@ Meh - BDO is one of the top 5 accounting companies in the country. They are a specialized tax expert. If they flaunt the tax rules they would not be in business for very long, we would all hear about throughout the media. This has not happened.

Now BDO say The Brightline Tax is already a capital gains tax. Given BDOs prestigious record, if they back the claim that The Brightline Tax is already a capital gains tax, then it is so. Might pay for you to also swallow your pride on this one, & recognize when someone much smarter with much more credibility on the subject is telling you your wrong. It's a pretty safe bet to trust the experts on this one, rather than the envious screeching from random people on the internet who believe it is everyone else's job to carry them through life.

Your statement that no capital gains exists in this country is not only proven to be false, but stems from nothing other than envy. It's an envy tax you ultimately advocate for. Remove your emotion & deal with the facts. Socialists often choose feelings over facts, which is why our provlems keep getting worse. Need to bury how you feel, its irrelivant. Apply a bit of common sense instead meh - taxing something does not make that something cheaper to buy, or more abundant to buy. Making it more expensive to sell does not make the price cheaper when selling, nor does it incentivize those who already have to sell.

If the ultimate goal is more tenants into homes, you will not achieve this with an indefinite capital gains tax, quite the opporsite. We've already seen under the Ardern administration exactly what happens when restricting, penalizing & taxing policies are out in place in an attempt to punish those that have, for those that haven't. We ended up with the fastest rising property prices, rents, crime rates, retail crime rates, child poverty rates & government emergancy social housing wait lists in our countries history.

Your method of "tax the greedy investor more & it'll bring housing more affordable" that youve been trained as a socialist to parrot is deeply flawed & has already been proven wrong multiple times. The fact that you just don't like landlords because they have more than you & that's not fair is irrelivant. Facts over feelings meh.

Sounds like a lot of emotive feeling over fact in your rants, hence your inability to comprehend my comment. A lot of projection in your comments.

I am a tax expert and ex Chartered Accountant. I've worked with the "big 5".

Using the terminology of CGT over income tax is what is causing the great divide, and it's because of badly defined distinctions in income tax law. The whole argument is highly emotive and fear based.

Everyone wants their gains but they're more upset that they might lose a tiny portion of their wealth/money. I remember one client many years ago who got a little miffed by his $400k tax bill, my manager at the time pointed out that he still received $1M+ and to get over it.

If you think the big 5 accounting firms are so prestigious and credible you haven't been paying attention. It's a nicely manufactured status.

https://www.npr.org/2022/06/28/1108044858/accounting-giant-ernst-young-…

https://www.google.com/amp/s/amp.theguardian.com/business/2023/may/12/d…

@ Meh - "I am a tax expert and ex Chartered Accountant. I've worked with the "big 5"."

Really? Cant have been a good "tax expert" considering you don't seem to understand how tax works.

You have avoided explaining:

How you believe that taxing property indefinitely will somehow make property cheaper to buy for those that dont already own a property who wish to own.

How you believe that taxing property indefinitely will somehow actually incentivize more people to sell their homes when a larger tax take is on the cards

How you believe that taxing property indefinitely will somehow create more supply

Why you advocate instead for just another replacement biast tax system to the one you currently believe that we have.

As "a tax expert" you would understand that unlike opinions that both tax & profits are not biased at all as to who makes profit & how. Now a true fair & non biased tax system would actually tax either all forms of profit indefinitely, or no forms at all. This means that all primary family first homes, all kiwisavers, all intergenerational family farms, all inheritance, all stocks, bonds, mutual funds, reits, crypto currency as well as investment properties to all be taxed heavily & indefinitely, no matter how the profit is made. Because profit is profit.

But meh you dont advocate for a true fair & non biast tax system at all, you simply advocate to swap what we have with another biast tax system in favour of who you believe should be targeted the most. This is not only envious & emotive, but shows your real lack of understanding on tax, losing credibility thay you are "a tax expert" at all. A true fair & non biast tax system doesnt target individuals, it targets profit.

Like a true socialist you have taken the bait hook line & sinker, that you incoherently believe that we can tax ourselves to financial prosperity. You dont need to be "a misguided tax expert" meh, its just simple maths - making it more expensive to sell does not encourage people to sell, they insteat hold for longer, restructing supply further. Taxing one entity indefinitely also does not make it easier for the other entity who do not own.

You have also failed to explain how you believe that an indefinite tax on investors will see more tenants into homes. This is becsuse such a correlation does not exist. Therefore, your only evidence is your silent admission that this is an envy tax you advocate for to those that have more than yourself. If this is your only "sound reasoning" to bleat on about a capital gains tax, then its no wonder you got out of the industry as you clearly dodnt understand it. Up until today you wernt even aware that NZ already has had a capital gains tax called the Brightline Tax for the last decade now.

The fact is most people in NZ are over it - even investors across various forums agree things are massively out of control. As such change is imminent whether it's this govt or a promise made by the next to get in the driver's seat the writings on the wall.

The reality is the intention of every property speculator is to make tax free gains. As such any and all CGs are taxable, why the ird doesn't stand on your throats is beyond me.

Sooner or later the fatted calf will be slaughtered. Have your pivot ready.

@ Sluggy - You have confused the simple terminology between a property trader or flipper and a landlord. The two both dabble in property, but for different reasons. That's like confusing a book keeper & an accountant. Why this stuff isn't taught in schools is beyond me. You have been decieved Sluggy by the last leader, who deliberately set out to confuse different basic terminology between entities. One seeks the quick capital, the other seeks the cash flow.

A property trader flicks a property for quick gains, and is already tainted by the Brightline capital gains tax since 2015. I'm surprised that you did not know this. It's nearly a decade old. A landlord keeps their property long term for rental income.

Does not give you much credibility in any of your claims when you can't even get the basic terminology right. Apply less emotion of envy towards those that have more than you, & instead apply a little basic common sense - a tax of any sort does not make the commodity cheaper for those that dont already have it, nor does a tax of any sort make the commodity more abundant.

Issues with appts & townhouses in the provinces as well. Not all is well. Mmmm. It's going to be another interesting year ahead of us in 25, with macro influences to the fore me picks.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.