They say a picture is worth a thousand words, so this month we have six of them, in the form of graphs, to help explain what is happening in the residential property market.

Unfortunately they paint a very messy picture.

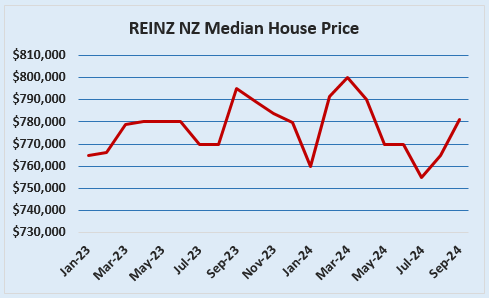

The two sets of housing market data that attract the most attention are selling prices and sales volumes.

The recent trends for both of these sets are shown in the first two graphs below. The median selling price firmed up slightly in September, which was expected, while sales volumes declined slightly, which was not.

The Real Estate Institute of New Zealand's median price has risen for two consecutive months, from $755,000 in July to $781,000 in September.

This is being proclaimed by some as the start of general rise in prices, but the chart suggests all that's happening is prices are following their usual seasonal pattern, but at a slightly lower level than last year.

Overall, prices are following their usual seasonal trends, but remain within a fairly narrow band with slight signs of weakness.

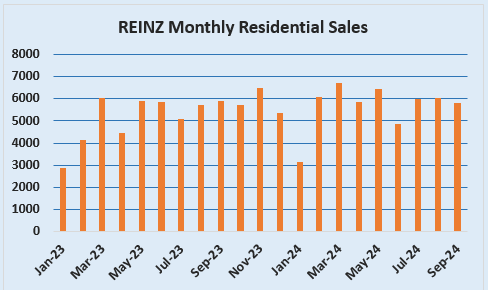

The sales graph below is also telling.

Sales dipped in September, but only slightly, declining from 6015 in August to 5816 in September.

But if you look at the trend on the graph for the three months to September and compare it with the same period of last year, there are only minor monthly movements and little overall difference from one year to the other.

What we are looking at is a sales pattern that is remarkably flat.

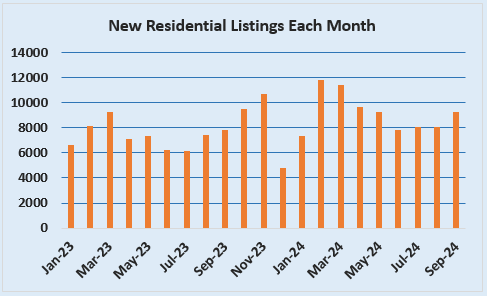

Then there's new listings coming onto the market.

These usually start picking up at this time of year as vendors anticipate a seasonal increase in sales leading up to Christmas and this year is no different.

However there are a few more of them this year than last, with Realesttate.co.nz receiving 9276 new listings in September, up from 7812 in September last year, an increase of 18.7%.

So buyers might be biding their time, but the vendors are keen.

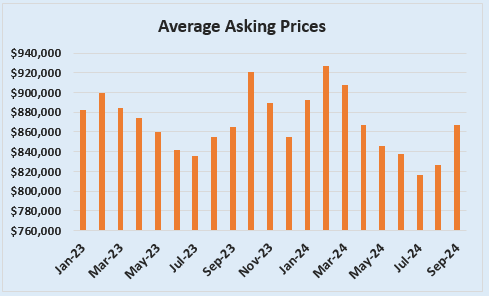

Vendor optimism is also showing up in the average asking prices on Realestate.co.nz (in graph below), which increased from $826,195 in August to $866,978 in September.

But that comes after the substantial declines that occurred from April to July, and asking prices have only bounced back up to where they were in September last year.

That suggests while vendors might be feeling more optimistic, they aren't getting carried away in their price expectations.

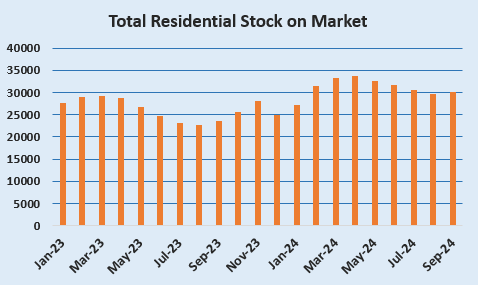

Then there's the total amount of residential stock on the market (se below).

This too is following the usual seasonal trends, but at much higher levels than previously.

There were more than 30,000 residential listings on Realestate.co.nz at the end of September, up 27% compared to the same time last year.

Put simply, stock levels are too high for the volume of sales being made, and if you don't know what that means for business, talk to a retailer.

It remains a buyer's market and they are taking their time making decisions.

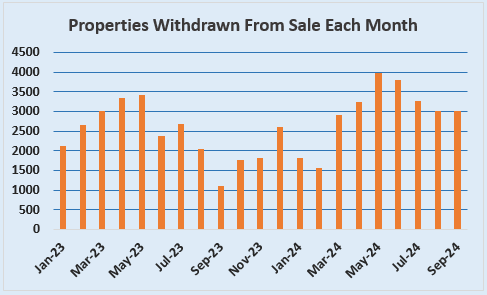

Even though stock on the market is currently at high levels, it would be even higher were it not for the number of properties being withdrawn from sale and taken off the market each month. (See graph below).

Interest.co.nz estimates that since April, more than 3000 properties a month have been taken off the market.

There are many reasons why a property can be removed from sale. But the odds on favourite is the vendor had unrealistic price expectations. And after several weeks of open homes and getting all the feedback from the agent and potential buyers, and then having their property languishing on the market unloved and unwanted, perhaps for several months, they decided to take it off the market rather than face reality.

However although these properties are no longer for sale, it's likely that their owners are still wanting to sell, making them a latent source of supply.

If you think stock levels are high now, wait and see what happens if market conditions improve to the point where they are tempted back onto the market to have another crack at it.

Overall it remains a buyer's market for sure, but it is messy and lacks any clear direction.

Buyers are active and will commit to a purchase, and falling interest rates will help in that regard, but vendors still need to be realistic on price and in some instances that will mean biting a bullet.

Otherwise their property will just end up on the heap with the thousands of others withdrawn from sale each month.

The comment stream on this story is now closed.

*This article was first published in our email for paying subscribers. See here for more details and how to subscribe.

96 Comments

Dead cats bouncing all over the place.

More bare, unhealthy bottoms exposed, than K-Road.

Better value and lower pricing coming in 2025/2026/2027.

If you must buy, offer only the 2018 valuations and older!

The bottoms are getting wider.. could be as a result of the messy housing market..

Until corrected, from wider, the bottoms will start getting deeper..

if its a "bottom" wouldn't that imply its a good time to buy?

A bottom before the next leg down.

In Eastern Suburbs in Auckland, what does sell appears to be selling around the 2021 RV. I’m all for negotiating hard and getting great deals, but 2017 RV or thereabouts sounds impossible unless there’s defects with the property.

I'd be very careful using a 2021 RV as a benchmark for buying in Auckland. Those valuations were completed at the peak of the market and things have moved significantly downwards since then - from a median $1.3 million peak in Nov 2021 down to a $970,000 median today. That's a 25% drop in median value.

https://www.interest.co.nz/charts/real-estate/median-price-reinz

The Eastern suburbs might be an exception but when revaluations are done again at the end of this year (November, I believe), there is a big downside risk. I'd wait until those revaluations come out in the AKL market, unless you can secure a good discount on 2021 RV.

But of course, that only matters if you are borrowing a good chunk of the purchase price.

"But of course, that only matters if you are borrowing a good chunk of the purchase price."

FYI, for those who don't know and unable to see.

Even a cash buyer who paid $1,300,000 at the peak for an asset (Peaker) that now has a market value of $970,000 has lost 25% ($330,000).

A counterfactual, if the cash buyer had waited:

1) they could have put the $1,300,000 in a time deposit and earned interest. This could be invested in a time deposit to offset the cost of renting. The balance after 3 years would be $1,294,647 (as cost of renting offset the interest income received after tax)

2) and paid $970,000 by purchasing at today's price ("Buyer Today"), they could have saved the $324,647 and put these savings on time deposit at a bank. Or earned 4.426% per annum for 10 years by buying a 10 year government bond which means that $324,647 would be worth $502,237 in 10 years time.

EDIT: remember in 10 years time, for Peaker and Buyer Today, the house price will be EXACTLY THE SAME.

The key difference being that Buyer Today has $502,237 in savings for their retirement that Peaker does not have. BT will have more money available for retirement than Peaker. Conversely, Peaker will have less money than BT at retirement. Buyer Today is in a better financial position - all due to that single decision to choose to rent and wait and then purchase their residential dwelling at a price which is lower by 25%. That single decision to buy in November 2021 would have cost $502,237 extra to buy the exact same house for Peaker compared to a Buyer Today.

I know of areas where house prices were around 1.3 at the peak in Auckland, they’re selling for circa 1.15.

Where are you pulling out 970k from? That sounds like very bad buying at the peak or riskier homes.

"That sounds like very bad buying at the peak or riskier homes"

Owner occupier buyers are a very different type of buyer compared to property industry professionals - (informed and educated property investors, property developers, property construction and property industry specialists)

Owner occupier buyers can and often do overpay especially under conditions of rapidly rising house prices causing a fear of missing out. As a result, in a property bubble, they can become collateral damage.

The $970,000 number is the most recent median house price. The magnitude may be different using $1,150,000 price, but the principle is the key point worth noting.

The numbers above are for a cash buyer. The numbers for a 80% LVR buyer have been previously provided by comparing a peaker vs a buyer today.

Here is the Peaker vs Buyer today for a 80% LVR buyer posted previously.

For those that are unable to see the mathematics between the Peaker and the Buyer Today (BT).

For owner occupier buyers: CAVEAT EMPTOR. Beware of those with their vested financial self interests.

1) Peaker

The median house price at the peak for Auckland was $1,300,000

With an 80% LVR, this is a mortgage of $1,040,000

The 20% equity is $260,000

2) Buyer Today ("BT") - Aug 2024

In 2021, the buyer who waited, deposited the same $260,000 equity into a bank deposit earning interest. Also BT would rent an equivalent house and have still saved money due to the rental being below the monthly P&I mortgage payments of Peaker - in 3 years the savings would have been about $20,000 annually. So a Buyer Today would have an amount of $340,233 to use as a deposit.

The current median house price for Auckland is around $950,000

Equity deposit of $340,233

The mortgage at this purchase price would be $609,767 (an LVR of 64%)

The Peaker has a mortgage which is higher by $430,233 (mortgage of $1,040,000 for Peaker vs $609,767 for BT). BT's mortgage is 41% lower than Peaker's mortgage.

Assuming BT, pays the same exact dollar amount each year that Peaker pays for their mortgage, as a result of that additional borrowing, Peaker is paying $1,232,229 more over the 30 years than BT (This is due to higher borrowing amount of $430,233, and total interest on this of $801,996 over 30 years). BT is mortgage free by the year 2037, whilst Peaker continues to pay their mortgage until 2051 (14 years later) - so after the year 2037, BT can save all that money that Peaker continues to pay on the P&I mortgage.

Assuming same incomes, and same living costs (food, travel, etc except mortgage) , BT can save the total $1,232,229 in payments that Peaker is paying. If BT invests the annual P&I payments that Peaker continues to pay after the year 2037 at 4.0% p.a, then in 2051 this amount will grow to $1,401,500.

Remember that at the end of 30 years, the house price will be EXACTLY THE SAME for Peaker and BT.

BT will have more money available for retirement than Peaker. Conversely, Peaker will have less money than BT at retirement.

That single decision to buy in November 2021 would have cost $1,232,229 extra to buy the exact same house for Peaker compared to a Buyer Today.

For those who haven't noticed, the situation for Peaker

1) Nov 2021 purchase

The REINZ Auckland median house price was $1,300,000

With an 80% LVR, this is a mortgage of $1,040,000

The 20% equity deposit was $260,000

2) Sept 2024 situation

The REINZ Auckland median house price is currently $960,000, a price fall of 26.2%

Mortgage outstanding of $1,040,000 (assumed to be interest only for sake of simple comparison). The LVR is now 108%.

The equity is NEGATIVE $80,000

They are in negative equity, with a loss of 131% of their initial deposit, which is likely to be their entire life time savings. In less than 36 months, their entire life time savings has evaporated.

Can they hold on? If they are unable to hold on, then the loss may have to be realised (and they may still have an amount owing to their lender)

Actually the auction figures give you that neatly - only around 30% of auckland homes are selling at or above their 2021 valuation figure.

So - 30% at RV - and a very small percentage above the RV.

Only about 10% of homes put up for Auction in Auckland sell for over CV.

Iceman: "I know of areas where house prices were around 1.3 at the peak in Auckland, they’re selling for circa 1.15."

Really? You know such areas? Unless you reference them, well ...

Those numbers (median prices over time) are from the charts here on interest.co.nz;

https://www.interest.co.nz/charts/real-estate/median-price-reinz

Select Auckland from the drop down menu and the hover your mouse over the points on the graph - highest point (peak) is November 2021 - and the $970K is the most recent number released.

Interest.co gets these numbers from REINZ and charts them.

Look at the above maths for a cash buyer of this property.

1) Nov 2021: purchase price $13,000,000

2) Current valuation: $7,180,000

3) drop in market value: $5,820,000 (a 44.7% fall from their purchase price)

$5,820,000 savings invested in a 10 year government bond today earning 4.426% would be $8,974,482 in 10 years time.

That is the cost of that single decision to buy in November 2021. The current owner may be oblivious to the financial cost of their decision.

Property value - 65 Marine Parade, Herne Bay - realestate.co.nz

The stupidest example on so many levels.

"The stupidest example on so many levels."

Please state your reasoning.

Where do you get the current valuation of $7,180,000 from? I see $10,200,000. EDIT: I see, from the realestate.co.nz link.

Yes. The $7,180,000 valuation is the automated estimate on the realestate.co.nz link provided.

The $10,200,000 number is the most recent council valuation (June 2021)

Note the automated estimate is 70.4% of the 2021 council valuation (i.e a 29.6% discount to the 2021 council valuation)

It's interesting to look at these examples, but the fact is no one knows what will happen in the future, while on the other hand, everything is very clear in retrospect. Had the purchaser known they would lose (on paper) 5 mil they might not have purchased of course (or maybe if it's a house they absolutely loved then that 5 mil is worth losing?). But in 2021 it looked like interest might stay low for a very long time, it's what people were told, so they were making decisions on the basis of those assumptions. Had those assumptions come to fruition, that 13 mil house could have been worth 15 mil now and everyone in these comments would pat them on the back for "making" 2 mil (on paper) over the last few years.

Regardless, I feel that if someone actually has the money to buy a 13 mil property then chances are that they are probably OK financially even if they lose 5 mil in paper value on an asset.

"It's interesting to look at these examples, but the fact is no one knows what will happen in the future while, on the other hand, everything is very clear in retrospect"

Several commenters on interest.co.nz were highlighting the high house price risks in NZ. Those who were suitably experienced and tuned in could see the conditions of high house price risks. The RBNZ highlighted the risks of taking on too much debt in Feb 2021. People chose to ignore these warnings and buy.

People are free to choose however they are not free to choose the consequences of their choice.

These examples are provided so that people can learn the lessons for the future. These are examples provided in real time. The likelihood of a broad public record written to document one of the largest asset bubbles in the history of NZ (house values in NZ have fallen over 70% of GDP) even well after this period has passed is low. The RBNZ might do a study in the years to come, but we are highlighting the observations in real time (and any study done in the future is likely to miss key points and come to incorrect conclusions).

"People who fail to learn the lessons of history are doomed to repeat them."

For the record, here were the arguments given at or near the peak Nov 2021 as to why house prices will not crash

With the benefit of hindsight, people can learn the lessons to see the flaws in the line of reasoning given here.

1) Tony Alexander - 19 reasons why there's no crash - December 2021

https://ndhadeliver.natlib.govt.nz/delivery/DeliveryManagerServlet?dps_…

2) Catherine Masters - July 2022

Why the New Zealand housing market is nowhere near crash point

https://www.oneroof.co.nz/news/why-the-new-zealand-housing-market-is-no…

3) Ashley Church - April 2022

Four reasons the housing market won't crash

https://www.oneroof.co.nz/news/ashley-church-four-reasons-the-housing-m…

4) Kelvin Davidson - Dec 2021

“But will prices actually fall? I’m not convinced because in the past a serious housing downturn has come with a recession, but no one is suggesting that and unemployment is low at 3.4 per cent.”

https://www.stuff.co.nz/life-style/homed/real-estate/127305870/what-lie…

5) Nov 2021 - Here's why it might be fruitless to pin your hopes on a house price crash

https://www.stuff.co.nz/business/300449314/heres-why-it-might-be-fruitl…

For the record, here were the warnings given by the RBNZ governor on the elevated house price risks:

1) Feb 2021: https://www.stuff.co.nz/national/politics/300238808/reserve-bank-govern…

2) March 2021: https://www.stuff.co.nz/business/124430525/adrian-orr-frets-over-soarin…

3) Nov 2021: https://www.rbnz.govt.nz/hub/publications/speech/2021/speech2021-11-02

4) Nov 2021: https://www.1news.co.nz/2021/11/24/first-home-buyers-encouraged-to-wait…

In light of subsequent house price changes, these warnings now may have a different interpretation by readers.

These warnings were similar to warnings by Civil Defense of a high risk natural disaster (e.g tsunami, earthquake, volcanic eruption, flooding, high winds, landslip, etc). People who chose to ignore those warnings potentially face the consequences of their choice.

People are free to choose, however people are not free to choose the consequences of their choice.

I’m not using it as a benchmark. In my view, the RV is meaningless. Any asset I buy, property or otherwise, is based on cash flow after debt servicing. My point is that transactions happening in a part of Auckland that is easy for me to observe is closer to 2021 RV, not 2017 RV.

My parents sold earlier in the year in Mt Maunganui.

A week or so later, the new council valuations were released.

The new valuation was 22.31% lower than the 1 July 2021 valuation.

Good timing for your folks, then again, lucky timing that someone offered an acceptable amount to them and had settlement prior to the revaluation.

Oh absolutely but they had also been a bit delusional on price and as a result, had been trying to sell since 2021

The revaluations have been delayed and won't come out until early next year. They were taken in May 2024 so they will reflect a lower point than 2021 CV but not as low as the market is now. Herald Article

Council valuations down in 2024, with rises in council rates.

Rate paying owners might not be happy with that.

If you must buy, offer only the 2018 valuations and older!

How rediculous... good luck trying this in desirable areas that include school zoning etc.

I get it.

You are so "wealthy and sorted" you can afford to live such areas. 95% of the country can't.

Haha & I’m sure there are just as many unhealthy bottoms hidden away 🫣…yesterdays CPI only galvanised my thinking that you’ve got about 6-12 months left on that soapbox Gecko…the need for a quick fix is getting more desperate with each release…print/slash/remove…$$/rates/restrictions…again, it’s not a good idea but they know that giving ole trusty the can a boot will bring on a wealth effect that will get the economy (maybe only at a false surface level) pumping…& then it can be a “meh, worry about it in 7-10 years” problem…you should be preaching for folks to start googling the specs on jetskis, Rangers & spa pools 🤔😉😂

Wealth effect can't be achieved with the flick of a switch. It could take multiple years for the housing market to recover back to late-2021 peaks for households and speculators to feel wealthy enough to spend like no tomorrow once again.

Rate normalisation alone won't expedite house price increases to recent highs, since it was a combination of very generous fiscal and monetary stimuli applied in bursts that got us there during Covid.

Don't forget that rating agencies will also be watching us closely as we already sit on >6% current account deficit to GDP and another bout of wealth effect-induced economic growth could push us into deeper deficits.

Yip the yield curve is only just normalising now - it is possible central banks have pulled a rabbit from their collective hat and deliver markets a soft landing but I’m still quite sceptical. It’s possible the recession is just about to start - remember the US share markets are hitting all time highs, unemployment is ticking up and central banks are cutting rates. This is the same/similar playbook or conditions to the 2000 and 2008 peaks and subsequent recessions/market crashes that took a number of years to recover from. We many actually see things get worse for another 12-18 months, not better.

I hear ya…but you don’t think if they get desperate enough to do something stupid (I mean, I think something stupid is more likely than something smart)…& they slash rates & pump cheap money into the economy again, alongside eased restrictions (I think DTI’s don’t apply to new builds as it is?)…then it won’t put a massive sugar hit into the economy? And it won’t happen fairly quickly? Hair of the dog/tomorrow’s problem kind of reaction to a complete cluster f**k of monetary policy is on the cards…let’s hope I’m wrong…but the longer it drags out the more likely stupid enters the chat surely 🤷🏻♂️😂

Granted another insane monetary policy response cannot be ruled out.

However, like I indicated in my previous comment, our current account deficit as % of GDP is already the worst in the OECD. Household debt to GDP/income is also very high, which is not uncommon in the developed bloc but most of the other nations are net creditors to the world, i.e., all have a high savings rate.

Gaming high housing inflation in the current scenario can only happen if households take on tens of billions of dollars of debt in a short span and consume their guts out, for which we could get seriously whacked by rating agencies and our foreign debt owners.

It would be interesting to compare the health of both of that statistics at previous boom/bust cycles to see if it has been something that has held them back from doing dumb sh*t in the past.

Hey, I would love to see this play out where the govt jump on board with some fiscal stimulus to give the economy a boost and get construction back on its feet, the RBNZ ease rates to a sensible NIR (around 3%ish I assume) leaving chalkboard rates sitting at high fours maybe so it'll give households a breather and put some cash back into the hospitality and retail sectors without firing up a cheap money mindset, DTI's/LVR's being used wisely to cap house price growth, maybe some rent-to-own options for FHB to get a home without the stress of the 10ish years needed to save a deposit, HPI to hopefully keep under wage growth for the long term so that we see affordability become slightly better.

But, I think they've f**ked it, went too low, started to hike to late, held too long...the state of the economy is shot, and that's why I think they'll revert to tried and try dumb quick-fix decisions...lets hope I am just being negative and you guys are right. The govt really need to join in and help Adrian out ASAP and maybe then my tune will change.

I agree in principle. All rational thinking goes out the window during a crisis in this country because of how ill-prepared we are with our meagre savings. 3.3% household savings of net disposable income as of December 2023. I bet it will be closer to zero or even negative for the bottom 25-50 percentile.

Government books have been in decent shape for a while but the sheer inability of successive governments to use fiscal headroom to improve economic outcomes with better infrastructure spending is annoying.

You forgot this graph Median Multiples | interest.co.nz

It's showing that the median multiple is trending lower, which will be a combination of lower prices and rising wage inflation.

As far as your retailer analogy goes, there is a fair bit of house/section retailers trying to dump stock that cost a lot to produce, before the newer more affordable stock (due to fast track and other policies coming) comes on the market in coming years.

Anybody buying now on the expectation of capital gains like we had in the past should be aware that this may not happen.

Select Auckland, between 2010 and now. The 'flatline' in in prices, 2016 to covid madness, while wages advanced, shows up nicely as a falling multiple line. Will it re-establish itself? Methinks maybe it will. Others disagree. We'll see.

With respect to NZGecko's point could you please include data points in the graphs back to 2015 so we can have a real pespective on "market" movements?

Done:

https://fred.stlouisfed.org/series/QNZR628BIS

I see many properties now transacting near 2017/2018 values ....... the slipnslide is still in action!

Yip and in real terms , prices bounced around with little to no ‘real’ growth for the 100 years before 1990. Since then we’ve had housing appreciating at 7% with inflation at 2-3%! (this isn’t sustainable’forever’ because peoples wages and rents (ie general economic inflation) are the cash flows that justify house price inflation - so one can’t inflate forever at 7% while the other only at 2%. It’s possible we are starting to deflate the mother of all bubbles in inflation adjusted terms. It’s quite possible we have housing returns that are less than inflation for a few decades which see house prices return to more normal (historically accepted) price/income ratios.

Not a certainty because who knows what crazy things governments/central banks may do if we start on another leg downwards in nominal terms with house prices - the wealth effect in reverse could trigger a very deep recession ie far worse than what we’ve just had the past 24 months.

Anecdotal story

A property trader had their property listed for sale for 18 months. Then took it off the market.

Another previous report

https://www.oneroof.co.nz/news/ex-cabinet-minister-pulls-house-from-sal…

Luxon seems to be doing pretty well selling up his properties...

He knows.....

Years back, I was at a dinner and sat next to someone I didn't know. As one does I asked "And what do you do?" His reply "Oh. I'm a politician (NB: A State one, not Federal). But that's not my main job. That's being a property developer". The inference I got, even back then, was that his political career gave him an insight into what his other job should be doing.

"Luxon seems to be doing pretty well selling up his properties..."

For those who own multiple properties, each property is a small percentage of his net worth. These properties might represent less than 20-30% of his net worth, so more willing to sell than wait? Or he knows something that we don’t?

For most residential property owners, that single property might represent 90 - 400% (due to leverage) of their entire net worth. In this case, they may be willing to wait and hope for higher prices (assuming no time constraints). For these owners there may also be an anchoring effect in force.

Gospel according to pink Floyd. Seems very fitting for Luxon situation

Money, get away

Get a good job with more pay and you're okay

Money, it's a gas

Grab that cash with both hands and make a stash

A lot of the politician's have rentals.Its documented here. If more of them start selling then surely a closer look is due.

Or he knows something that we don’t?

He knows that owning seven houses makes him look out of touch. Well he does now. But he should have figured that out before he became the national party leader. Sell them all and put the money in an ETF. Then have a go at being Prime Minister.

Was it greed or is he just actually out of touch.

Wonder if he owns any property in that muddy river creek, nera Whenuapai base?

It's to avoid CGT. He changed the Brightline rules so he could get his tax free gains before they bring in CGT.

"The Real Estate Institute of New Zealand's median price has risen for two consecutive months, from $755,000 in July to $781,000 in September.

This is being proclaimed by some as the start of general rise in prices,"

Are those proclaimations made by those with their own vested financial self interests?

Owner occupier buyers: CAVEAT EMPTOR

"It remains a buyer's market, and they are taking their time making decisions."

I'll disagree slightly.

"It remains a sellers' market, and they are taking their time making decisions."

All that's holding many vendor's back is... price. And for those with historical portfolios of any size, then now might be as good a time as they might get to cash-in. All that's keeping selling back is the fond belief that 'property always goes up' and given time it will again. If this article tells us anything, it's that The Market isn't behaving as expected.

i.e: "Put simply, stock levels are too high for the volume of sales being made, and if you don't know what that means for business, talk to a retailer."

To the tune of money for nothing, cost that's what it really is..

I want my...

I want my...

I want my capital gain

Unless the banks start liquidating the hopelessly in debt I just can't see another big drop. Banks want to keep sucking on your financial lifeblood, and are aware enough to keep the host from dying. Extensions of interest only, payment deferment, term extensions all keep this parasitic dynamic in play.

Imagine a world where housing stayed the same value, and people couldn't just leverage the increase in their house price to do Reno's or whatever they wished. Sounds bizarre, but also very positive in that people would have to look elsewhere to build wealth.

"Imagine a world where housing stayed the same value, and people couldn't just leverage the increase in their house price to do Reno's or whatever they wished"

Imagine a world where owner occupier buyers buying their primary residence were to have priority over other non owner occupier buyers in the existing residential dwelling market. Those households who wanted a non owner occupied residential dwelling beyond their primary residence had to build or buy in the new build market.

https://www.propertyguru.com.sg/property-guides/additional-buyers-stamp…

So not a NZ story in either example?

Interesting indeed, thanks for the link.

FYI, the tax policies of the previous government of incentivising non owner occupiers to build new, and buy new builds (i.e increasing the number of residential dwellings) were working and needed time to work out in its entirety (phase out of interest deductibility on existing dwellings over time).

These tax policies were pro owner occupier buyer policies in the existing dwelling market.

The policy was working however it was reversed by the current government and non owner occupier buyers (and syndicates of non owner occupier buyers) are now preferring to buy in the existing dwelling market over the new build market.

Here was a comment made in April 2023 by a real estate agent in Auckland.

"It is virtually impossible to find investor buyers for second hand properties due to zero mortgage interest deductibility"

Put simply, stock levels are too high for the volume of sales being made, and if you don't know what that means for business, talk to a retailer.

This speaks volumes - this lack of volume.......

To shift it you need to discount it!

43,300 listings on TM. Been rising consistently for all of spring. Peak for the last 12 months was ~45,000 in April. Wonder where we'll get to this time.

If you think stock levels are high now, wait and see what happens if market conditions improve to the point where they are tempted back onto the market to have another crack at it.

Tempted .... more like forced.

"More than 3000 properties being taken off the market.

In the hope of better days, that's a lot of people putting their lives on hold. It's funny when suggestions are made that FHB's do the same to build larger deposits, it's met with contempt from some here.

"when suggestions are made that FHB's do the same to build larger deposits, it's met with contempt from some here."

By those with undisclosed vested financial self interests?

Owner occupier buyers: CAVEAT EMPTOR

The purchase of a residential dwelling is likely to be the biggest purchase for most households, with the purchase price representing up to 1,000% (up to to 90% LVR) of the entire net worth and lifetime savings for first home buyers.

Good to see reporting on number of houses withdrawn from the market thank you

Interesting approx 10% of property is withdrawn

Yeah it is very interesting. We tend to focus on the properties that do sell, understandably. However the properties that don’t sell may also have a story to tell. I wouldn’t know how to describe the relationship statistically or if it could be done but it would be nice to know at what value those unsold properties would change hands between a willing seller and a willing buyer. Those figures might tell us how much the market has dropped in value.

I have looked at a few properties that have been on the market for over 6 months, the vendors are waiting for a 2021 price buyer. They refuse to believe it's worth any less.

Most of these people don't have to sell. I know what I've got, and I know what it's worth...

You know what they've got: A heavy rock that isn't shifting no matter how much they look at it and try and use the force to do so XD

In recent months many investors I know are withdrawing properties from sale simply because affordability to hold them has suddenly improved and they didn't want to sell to begin with. Looking at the cashflow void with rates at 7.2% is pretty ugly, but rates are now back around 2022 levels, and suddenly things look more sustainable. So they'll hold on.

Such properties won't come back to the market in a hurry.

We were in that position too, but our sale went through before we could pull out.

Another OCR cut will give it direction. Also everyone here concerned for FHB pls make sure they read that prices are still declining however not so fast - there is still no FOMO and stock levels are hight put in good offers. Honest opinion if you find a house you like and you can afford it please buy it :)

What do you mean by afford? I can more than afford what I'm looking for according to the banks calculations with my current deposit and income.

I will just have far less disposable income and a correspondingly lower quality of life than my parents had for a worse house. And I am far better qualified with a far better income.

Forgive me for, perhaps foolishly, holding out for further falls (not necessarily nominal) in the hope of a better for myself, my children and the rest of NZ society.

@1harlow1 - oh yes i see - dont buy keep renting - also good just stop complaining for the sake of yourself NZ and the wider society.

I think a missing statistic is the number of new properties coming to the market. That earlier this year there was 3,000 listed as 'new homes' on Trademe. Currently that number is closer to 3,750. and of course for townhouses a developer will list one but have five. So that number is increasing and there is still thousands of building consents in existence that haven't been completed.

There was commentary the other day on the number of rentals available. I think that many first home buyers have bought off the plans - and quitting their rentals as they move to their new home adding to the stock. In the year to May - Auckland Council issued a record 19,000 code of compliance. At that rate a further 10,000 homes were probably completed between May and Christmas - thats lots of stock into a slow market.

I think that the focus is too much on interest rates and not recognising that supply is exceeding population growth

From what I know of current conditions from developers I work with, nobody is buying off the plans right now. They haven't for a while now - that period of rapidly escalating build prices a couple of years ago saw banks fairly reluctant to lend non-fixed-price contracts and developers had to pivot to selling completed units. By the time fixed price house and land packages were possible again, people couldn't afford them. Now I suspect it's just that people think there's better ability to haggle down an unsold finished unit that's hurting the developer than to try to get in there early and pay what the developer wants.

Put another way, buying off the plans requires an element of FOMO. If the development isn't likely to sell out before completion, why not wait and see what the finished quality's like? In a stagnant market it's not likely that waiting will cost you anything.

"From what I know of current conditions from developers I work with, nobody is buying off the plans right now."

1) Without a sufficient level of sales, how long can these developers hold on?

2) Will these developers, builders and construction businesses have access to additional capital to buy time (e.g Fletcher's rights issue) or will they become cashflow stressed and be unable to repay debt as it matures?

3) What about suppliers to the developers such as tradies and building materials suppliers ? will these suppliers get paid or will they face cashflow stress?

Well the government did just introduce an underwrite scheme didn't they!

The developers I know are not developing anything they can't do with cash on hand, which means low volume stuff. Banks are still friendly with the top tier guys, but those aren't the ones I know. It's really tough. These guys are sitting on some pretty expensive land bought in recent years where the houses have been demo'd but construction won't begin until the fundamentals are there.

Interestingly Williams Corp is still going door to door around where I live offering to conditionally buy people's properties, subject to DD and giving themselves 2 years to commit or bail. Actually quite clever - they're not promising anything except what appears to be a reasonably generous purchase price. Sneaky low risk hedging.

"Well the government did just introduce an underwrite scheme didn't they!"

Details of the eligibility criteria are key. How many developers are eligible? For those that are ineligible then there might be cashflow stress.

The programme announced on Friday 4 October aims to de-risk large developments by underwriting construction of residential developments of 30+ homes.

The underwrite is largely targeted to main centres (Auckland, Hamilton, Tauranga, Wellington and Christchurch), however developments in other locations that meet the full criteria may also be considered.

“The new Residential Development Underwrite (RDU) will help support residential construction activity in the near term by enabling credible developers to access finance that they otherwise wouldn’t have gotten. This also has the benefit of ensuring there are houses ready to go for buyers who enter the market as interest rates drop,” Housing Minister Chris Bishop said.

“For a development to be approved for the underwrite, it must have a minimum of 30 houses. The developer must have a proven track record of successfully building and selling houses of a similar size and scale, have ownership or use of the land (or an option to do so), and have all the required resource consents for residential housing.”

There will be no price caps or eligible buyer restrictions, and the programme will cover all types of dwellings: standalone houses, townhouses and apartments.

“In addition to providing a recent market valuation from a registered valuer, the developer must also be able to provide satisfactory evidence that underwrites are needed for the development to proceed within 6-12 months – for example, evidence that reasonable attempts have been made to market the development, that finance approval is conditional on pre-sales, and that the required workforce is available.”

https://www.eboss.co.nz/detailed/building-industry-insight/government-r…

"Banks are still friendly with the top tier guys, but those aren't the ones I know. It's really tough. These guys are sitting on some pretty expensive land bought in recent years where the houses have been demo'd but construction won't begin until the fundamentals are there."

How long can they hold on until selling prices recover?

Meanwhile if they are leveraged to finance the purchase of the land, there are holding costs such as interest and rates to pay until the project becomes financially viable. The interest may be capitalised currently. When the loan matures, will the borrower be able to refinance?

Or if they are unable to continue the costs of financing and ownership hold on to the land, they sell the property - potentially at a loss. Seen a few of these losses realised in the last few years, resulting in lower land costs for new owners of future projects.

When everyone's so bearish you know the bottom is in.

Interest rates keep getting slashed, a few more will take the chance on buying, fomo will set in and we are off to the races

some of us have been in the market for several cycles. In previous times of slow to difficult selling a lot of the stock was put on the rental market. This time we are still operating to Labour laws ie unable YET to give 90 day notice to end bad tenants. Also many mum and pop homeowner’s houses are not up to standard for rentals. Ie no heat pump and no insulation and extractor fans. So grandma can not sell her home and cannot let it. So the properties sit empty. Not all of them but enough to make a difference.

"So grandma can not sell her home and cannot let it. So the properties sit empty"

Just trying to understand you here.

Grandma cannot let it her home currently as it doesn't meet Healthy Homes standards, so it is currently empty? and she cannot sell it?

If my understanding above is correct, then why is grandma unable to sell?

Granny can........just the old delapidated 1970s pad, has to go for 2015 to 2018 prices......

Property Leader has his eye on a property that he wants to lowball offer an old lady widower that doesn't know the property's true worth.

But unfortunately it doesn't meet Healthy Homes Standards and he doesn't want to spend any money improving it before renting out.

Bingo. It always makes me laugh when people get grumpy about healthy homes costs. I get it' it is an expense for the owners, but failing to have the basics is essentially signalling that they expect someone to pay premium rent for a cold shitbox which the landlord(s) are ok with as it benefits them. Clear indication that they aren't considerate of the tenants, or they have a bigger portfolio they have to spend on all for them at once and hence the gripe.

"More than 3000 residential properties a month are being taken off the market" ... and being added into the rental pool because 3000 is about the number of house owning kiwis leaving our fair shores?

"So buyers might be biding their time, but the vendors are keen" - I can smell the desperation growing.

"Vendor optimism is also showing up in the average asking prices " - hopium increasing.

Comment section, as usual, filled with copium from the usual suspects.

The headline of this article on the front page reads, "The housing market is messy and lacks direction".

Maybe. But the RBNZ's rate cuts has given fools plenty of direction, right?

I see that the Queenslanders are complaining about the price of their properties with them going up $1000 per week in many places .

90% of the suburbs have increased substantially this year.

The prices 30km from Brisbane median is now getting up to $1m

Reality is that property prices in NZ in most places are still very realistic and are not going to decrease.

know that the steady Chch market is going to increase now that the interest rates are heading south.

I do appreciate that it can be difficult for some to purchase property due go prices however there are ways of achieving it if you are prepared to work!

The NZ market is tanking faster, than the fearfull landlording goldfish can flee, to a hopium supporting puddle!!

The economy is contracting, many company profits are back -10 to -30%, with constant staff culling.......faster than possums dropping on SH1.

The vast Moa roaming swamplands of ChCh, are one shake away, from muddy wet slippers in the lounge........

Look on the bright side...... realistic yields of 7 to 10% are appearing nationwide. Rejoice.

Seriously Gecko, with respect, you actually speak more rubbish than anyone on interest.co.

Moa’s in swampland in ChCh!

You really have no sense of reality when it comes to real estate, you are delusional if you think prices are going to drop in the happiest city in NZ,

Agree, Christchurch is a great place to live and especially get started and have a young family. I live in Auckland and discourage the young to try and get started off here - I tell them the numbers don't work

"Look on the bright side...... realistic yields of 7 to 10% are appearing nationwide."

Gross yields. yeah. They are appearing. But let's not get carried away. They're still rare. And many are thoroughly undesirable as a longer term proposition. And as you say, nationwide, including small towns where the population is stagnant, or falling, or just one plant / factory closure from disaster.

After reducing the OCR house market is a one way ticket, UP!

Or simply extending the decline.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.