The housing market has made a difficult start to spring, with sales numbers declining significantly in September.

According to the Real Estate Institute of New Zealand, 5816 residential properties were sold throughout the country in September. That was down 3.3% compared to August, and down 1.1% compared to September last year.

The drop in sales appeared nationwide, with sales in Auckland down 2.7% compared to August ,and sales in the rest of the country (excluding Auckland) down 3.6% compared to August. See the chart below for the full regional sales trends.

Although sales were in decline, the number of new listings received in September rose 20.4% compared to a year earlier. That pushed the total inventory of homes for sale up 1.5% for the month and up 27.8% for the year.

In another sign of an increasingly difficult market, the number of days to sell stretched out to 49 nationally in September, compared to 40 days in September last year. In Auckland it was taking 10 days longer to sell than a year earlier.

However although fewer properties were sold in September, the prices they were achieving remained more resilient, with the national median selling price of $781,000 up 2.1% compared to August, but down 2.3% compared to September last year.

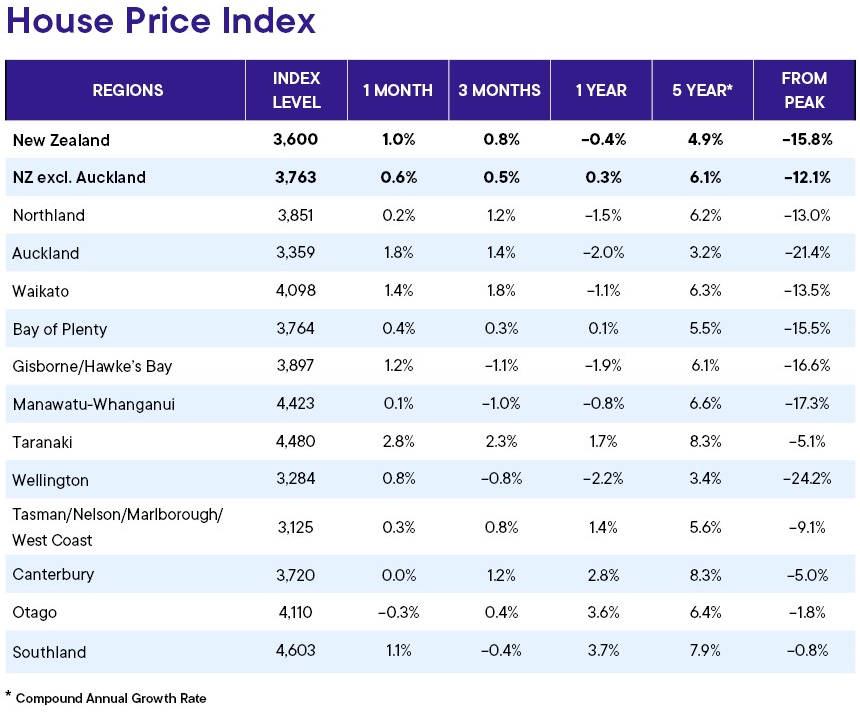

The REINZ House Price Index (HPI), which adjusts for differences in the mix of properties sold each month, was up 1% compared to August but down 0.4% compared to September last year.

Around the country, all regions posted an increase in the HPI compared to August, apart from Otago which had a -0.3% decline. (See the regional price charts below).

"The signs across the country are largely of stability, with slight decreases [in price] year-on-year, and the median price increase of 2.1% compared to August a slight improvement," REINZ chief executive Jen Baird said.

"Even though we are seeing another year-on-year decrease, this is in line with what we expect at this time of year, so the market is doing what we would expect, another sign of stability," she said.

The comment stream on this story is now closed.

Volumes sold - REINZ

Select chart tabs

Median price - REINZ

Select chart tabs

You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

168 Comments

Here we go again...

@Yvil - in what regards please ? Just property comments in general?

100 + comments to justify what one wants to happen.

Folks, this is Yvil's contribution. Enough said.

However although fewer properties were sold in September, the prices they were achieving remained more resilient, with the national median selling price of $781,000 up 2.1% compared to August, but down 2.3% compared to September last year.

There's that word, resilient, popping up again. 🥺

TTP

Going down the only road we've ever known ... (arguing about where the housing market is headed)

Brace.......

Sales numbers dropping, stock increasing, days to sell rocketing up.

Enjoy the smallest of dead cats before the usual service of drops continues.

The proportion of working-age Kiwis on main benefits reported in September 2024 was just shy of the previous peak in 2009.

Perfect time for young folks sitting on the sideline to take out a 30-year loan, am I right?

You need to look at housing on the basis of a longer term horizon. Property is not a short term investment. Look at the five, ten, 15, 20, 25 and 30 year property value changes\trends when considering buying or selling.

For the same reason Canterbury\Christchurch was a smart place to purchase five years ago and Wellington and Auckland was not so smart as a property investment (rather than a place to live), we will look back in five-ten years time and feel Auckland and Wellington was an opportunity about to happen in the next year or two.

Property cycles repeat consitently time and time again. The time to sell an investment such as property is not when it has just dropped 20-25 percent. If you do those drops are locked in forever.

All the best to fellow investors. Sometimes you just need to ignore the noise and back why you originally purchased!

With a crashing birthrate, what will property demand be like in 30 years? It might be a long-term decline (unless immigration saves the day).

No NZ goverment will allow immigration to reduce to the point where population growth was negative. That would be political suicide. They sometimes talk about immigration control but none are in a postion in the polls where they can afford do do antything meaningful to reduce it.

Even Winston now that he is in govenment has gone quiet on this one. Complete reverse of his historical ramblings.on immigration settings.

China almost has unsurmountable problems with longer term growth and balancing the books with it's ageing and reducing population. In NZ it is lower risk, as long as we are a more attractive place to live than the majority of other places we will attract immigrants and political governments know that without a small poulation increase our GDP growth rates look far less attractive to the populace. I do not think NZ can fall that far and that fast and the attraction and immigration settings will make sure at least the GDP and growth figures look acceptable. If you do npt also believe that, now is is the time to think about looking elsewhere!!.

"Even Winston now that he is in government has gone quiet on this one. Complete reverse of his historical ramblings.on immigration settings. "

That's Winston First for you. Once he gets in he enjoys the baubles of office. That said he is still an above average FM for NZ. I voted for him this last election but never expected that much from him. Shane Jones is certainly making the right noises.

The problem is that we can only afford to have immigration if the incoming people can afford to pay their share of the infrastructure and public services via tax. Else the govt will simply lower the standard of living for he existinf population for every new immigrant.

Nats recently turned off the tap for relatives of immigrants.we are losing skills young kiwis every day.

I am not sure I understand how the government will attract skilled young people who add value.. if our infrastructure and wages are lower than other countries (who want the smart kids to go there) the health service sucks and houses remain expensive.

Unfortunately we have to take a pain pill and reduce the cost of living (housing) to attract the right immigrants.

I suspect it's why 7 house luxon is now 5 house luxon. I a not sure he would pay to dump an asset he expected to continue to rise in value.

The DGMs on here cannot comprehend what long term thinking is. Their daily dopamine fix is to jump up and down on headlines like these instead. Retired Poopy is a great example of that.

No they do, that’s why many here have already saved multiple 6 figures on their future mortgages by not participating in a market that is currently collapsing under its own stupidity.

Your version of long term thinking is just a futile attempt to maintain the status quo.

There is zero rush, patience has and will continue to be rewarded for the foreseeable.

Yes ofcourse, this time it’s different, and ofcourse you can time the market perfectly with your crystal ball.

Exactly. Old mate here knows exactly how and when to pick the bottom but has only come up with a dirty finger.

In 20 - 30 years most people on this website will be retired some will be eating jelly others will be pushing up the daisies leaving house portfolios for family to fight over, would it not be better to give the younger generations a chance to have own home I know many couples who just cannot afford to have children and buy a house.

Great point.

The west seems to have a strategy of growing our wealth simply by borrowing from the next generation... finance, climate, health. Who have to live with the debt and high costs.

Seems very immoral and perhaps it says a lot about the characters of humans.

Ultimately it doesn't bode well for any of us.

If you did look at the long tern horizon you could read it as house prices just reverting to their long term track after the silly bump up of the last few years.

Which means they have a way down to go yet. Reverting to normal.

Not that I trust any prediction of mine.

"Shiver me timbers" - adjusted for inflation this is not good for sellers. Job uncertainty dictates this is a great buyers market for some time to come.

RP

Of course you would know lots about "adjusted for inflation this is not good" due to your beloved term deposits . . . and that's even considereing the extra negative of the tax take on td. You will be really being going backwards on house and term deposits.

....but we also own a house. Much like a few other debt addicts here, you seem too overly concerned with TD's. Enough to keep mentioning it over and over.

RP

Woopsie . . . . I really hit a nerve there. You were the one continually going on about TDs for years and years and infact you continually highly recommended them . . . clearly such a bad an experience for you its now something you no longer want to hear or be reminded about.

Cheers

printer8, even though it's been a "terrible" financial experience, we're sorted. Perhaps concentrate your gallant efforts on sorting your own affairs????

Yawn RP... it's almost been another full year of you doing the same comments.

Yawn RP... it's almost been another full year of you doing the same comments.

Nifty's contribution. Act bored but be triggered enough to tell us nothing of use - LOL!

Keep 'watching this space RP' - it's playing out just as I thought after RBNZ/Govt changes...

RP

"Perhaps concentrate your gallant efforts on sorting your own affairs" - dont worry about me as there are no problems there.

I'm eight years retired and comfortable - my only financial issue was last year paying a marginal tax rate of 39%.

More importantly, what do you make of this?

with sales numbers declining significantly in September.

This does not bode well for prices going forward now does it? As it's a buyers market, FHB's will find this encouraging and are being spoilt for choice. This is great news for the next generation - right?

"Even though we are seeing another year-on-year decrease, this is in line with what we expect at this time of year, so the market is doing what we would expect, another sign of stability," she said

🤣🤣🤣🤣🤣🤣🤣🤣

It is unsettling that these bozos who are fine with sounding stupid on public media rather than dropping the "silver lining/green shoots" commentary have so much influence on government policy.

Prices won’t spike just yet, but don’t get too comfortable. By the time the headlines shift, it’ll already be too late.

Too late I tell you....

I reckon real estate moves quite slowly. You can see a boom or bust coming with at least six months warning.

Getting your timing wrong has a greater impact at the top, the price gradient at the bottom of the valley is less then at the peak.

Even a month late at the top may mean 3 months on the market as it falls 2-3% a month

"You can see a boom or bust coming with at least six months warning"

What leading indicators do you look at?

I went to a few open homes on the weekend and was surprised by the amount of interest in the properties. If vendors are willing to sell for 2019 prices they should have no problem selling at all!

Likewise open homes the last few weeks and they are dead. Auckland if it matters.

Looking at buying? It's surprising how many on here spend time visiting open homes. Not sure I can think of many worse ways to spend a weekend.

Researching my own area. You can't really tell from photos what a home is really like. I often drop into random open homes and like to see how the sales go, knowing a little more about it. Sometimes a sale may look like a bargain but if you have seen it you know why.

I've only started reading this stuff since I started looking at buying. It's a confirmation bias thing. All the people here are interested in property for one reason or another.

Mine were Auckland but the lowest end in very good locations. B&T units.

Friend in Christchurch last Friday put her brand new 3 brm single level 2 bathroom house on the market Sat open home 7 couples threw Sun open home 10 couples threw. Expecting 3 offers today. She was asking (not auction, fool if you go to auction) enquires above 700k. A high percentage were Aucklanders glad to be looking at a stand alone 3 brm single story house not a 2brm 2 storied s...t box

Nice, one level, brick houses with double internal entry garages, appear to be good sellers.

a good mate bought for over 2 mil in one tree hill in 2018, tells me he would not get that back now, so 2019 prices are not achievable in some locations, its a stunning modernised bungalo on 800 sq m

Seriously?

TK look up 32 Alexander St Christchurch Central. The lady that owns it is 75 she lives in the house behind she has owned this site many yrs had an as is on it. She got it knocked down built this. She owns 12 plus houses did it all her self on a single income.

Has a very "gang pad" street appeal to it. But nice on the inside.

Incredible that a 75 year old lady on a single income has done so well. Must've put in 60 hours a week for 50 years?

@anyone - does anyone know how open homes are tracking in Palmerston north?

empty , people have driven up to boghead as its more desirable

You haven't been reading the news.

The Minister for Building and Construction, Chris Penk, wants to build a new high school at Riverhead on part of the Fletchers/Neil/Matvin land. The Ministry of Education has no objection, neither do the developers. It was in the local rag last week.

Another massive project for the West?

Will have to take your word on it. Most local rags tend to have an online presence, I couldn't find anything online in the last week however. Not even on Chris Penk's Facebook page.

Here's the latest OIA release on potential schools in that area.

https://fyi.org.nz/request/26957/response/102228/attach/4/1329484%20res…

I am writing to draw your attention to the urgent importance for a high school to service the rapidly growing areas of Kumeu, Huapai, Riverhead and their surroundings in West Auckland.

The Ministry initiated negotiations for a Kumeū site in February 2023. There are two sites that comprise the potential College site and negotiations with the second landowner have not yet commenced.

There are currently no construction or design plans underway for the new high school in Kumeū, as any planning is subject to the acquisition of a new site and the subsequent development of a business case.

I've been into the recycling bin to recover it...

"Thinking about other options,I have also written to suggest that a parcel of land in the Fletchers subdivision at Riverhead - earmarked by the developer to host a school - should be utilised to establish a secondary school. Fletchers themselves are amenable to this."

Chris Penk - Kumeu Courier - October 2024.

I am grateful that Fletchers have acknowledged this point and so now the ball is in the court of the Ministry of Education. I will keep you posted.

Where's the bit that states the MOE has no objection? I mean I guess they haven't actually objected to it, nor do they even have immediate plans.

https://www.kumeucourier.co.nz/uploads/issues/Kumeu%20Courier%20October…

The only way I see that we can get the housing market back on track is to open investment in housing back up to foreigners, encourage mass immigration and allow interest rates to drop further thereby allowing those newly minted NZ'ers to take on jumbo mortgages.

This has been our "growth" model for the last few decades and it's been wonderfully successful in transferring wealth to the Luxons amongst us as well as turning green pasture into suburbs.

"What's your primary export NZ?"

"...Rent"

And Kiwis that are getting squeezed out

You have to ask why any foreign capital owner would want to invest greenfield capital in NZ over other countries. We don't have the markets, high skills, infrastructure, etc. that they can leverage amid the high cost of doing business here.

Also, the government of the day prefers paying down debt over investing in the country's future but expects foreigners to risk their capital here.

We have the tax incentives to suit landlords. The stable regulatory environment. Geopolitical safety. I'm sure there's other reasons. But these are also reasons why we need to protect NZers from foreign landlords pushing housing and land out of affordability for citizens who aren't just financially invested here, but also have their entire lives and families here.

It is on track.

I've spent a lot of time looking at charts to try and assess when market lows are hit. Obviously its not that simple, but this does not look anything like a bottom to me.

Bottoms come in all shapes and sizes

Why not? Prices up a tad over the past month.

Yup and over three months half of all regions are up. And those are winter months before rate cuts. There's an easy narrative either way if you want it.

With equities for example, whats happened in the last few days is usually irrelevant, you need to zoom out to see the trend and where it might go.

If you look out further on the Auckland chart you can see the past month or so of flat to up is equally meaningless. The trend is still very much down as we retrace the covid gains. I'd need a lot more confirmation of a reversal. We could equally bounce along the bottom here for quite some time.

with equities 95% trades at open or close, with so little sales relative to listings you have to be very careful in how you read the sales price.

Its telling you that sellers and buyers are only agreeing on value on a small % of listings.

The Market has not reached a point where there is agreement, hence clearance cannot happen.

Without clearance happening pressure is building in the market.

The odds that it will expose itself as lower prices is high, as there are way more sellers then buyers.

I agree completely. Prices are much more likely to break down than break up.

If there was some fool-proof way of detecting market bottoms, we'd all be very rich, but there isn't .

Wow looks like green shoots already up 1.8 in AKL.

And for all the huffing and puffing done by the renters over the whole year AKL is down a massive -2%.

No doubt Retired Poppy et al will keep spouting the same wisdom he has for the last decade on here “adjusted for inflation” pretty desperate stuff now.

If you cannot face adjustment for inflation then you cannot deal with "sales numbers declining significantly in September" either then? Spruikers loved it when house price increases exceeded the CPI in the past. We heard all about it!

Oh - dear.....

I said prices would bottom out in Spring. That was rubbished by one person in particular. Let’s see where we sit over the next couple of months.

Council delays release of Auckland property valuations until early next year

Auckland council delaying again for some reason...wonder why?

https://www.nzherald.co.nz/nz/council-delays-release-of-auckland-proper…

In summary: "Let's ensure very high accuracy but never mind that the values will be almost a year out of date by the time they are finally released!"

Minister to Valuer-General: "We must wait for further interest rate cuts to restart the Ponzi. Delay! We don't want to frighten the pigeons."

Valuer-General: "But its most likely a bull-trap!"

Minister: "I don't care what it is! Don't frighten the pigeons."

Drink some Kool Aid. Half of all regions rising in price since July. All but Otago rising in last month. 2019 prices are the vibe.

Interesting choice of headline with the national median up 2.1% and HPI up 1%.

This is not Oneroof or the Herald but independent high quality journalism.

Don't miss the forest for the trees.

So the market has already turned upwards. Price declines have already been wiped out in Tauranga its on the up. More rate cuts and summer on the way its going to be 3 to 4% gains for the year. Time to buy a house if you can find a remaining bargain, there has been a few down here if you were quick.

Even the local rag isn't so sure.

"According to CoreLogic’s hedonic Home Value Index, Tauranga’s house prices decreased by 0.3 per cent in September despite falling interest rates....A clearer loss of momentum was recorded in the last three months with 17 suburbs declining since June, including Papamoa Beach down by 3.1%.... Values are still....almost 18% below the peak"

For instance https://www.sunlive.co.nz/news/352459-rate-cuts-haven---t-pumped-up-hou…

And of course, it's all about location!

"A seaside boom town known as a haven for retirees, holidaymakers and day trippers would be a “death trap” in the event of a tsunami....Pāpāmoa’s rapid growth could end up being its downfall....there’s a huge population and only two roads out. If there’d been a tsunami, there would have been thousands of deaths"

https://www.stuff.co.nz/bay-of-plenty/300841852/ppmoa-the-holiday-hotsp…

There won't be a Tsunami or storm surge because climate change is fake and so are earthquakes ...

I dunno I got a call back from an agent yesterday after a lowball offer was resoundingly rejected 2 months ago, asking if I was still interested.

It’s pretty rough out there! Net 55% of manufacturers reported layoffs last quarter, the worst hit since records began back in 1961. In this balance sheet recession, with asset values dropping while debts stay high or climb, folks are really zeroing in on straightening out their finances in this uncertain job market.

Looks like we might see plenty of forced changes in ownership in the next year or two.

I concur. The engineering sector is reporting low service demand across the board and, in response, are culling thousands of jobs. More importantly, there has been a sharp pullback on hiring new grads this year and hundreds of unfilled jobs previously listed are being scrapped.

Unemployment stats aren't effectively capturing these labour market trends because thousands of impacted workers are jumping on planes and going across the ditch, although the large outflow of Kiwis says it all.

Add in all the recent arrivals (eg nurses) who are here without work but do not qualify as unemployed.

How many of the 200,000 migrant arrivals year to date would have just happened to parachute into addresses that are captured in the household labor force survey?

Bugger all I would say.

We would have no idea of there current employment status. The IRD knows what is coming in on a monthly basis in terms of PAYE. That is the key employment indicator.

People can already see the light at the end of the tunnel. There will be a few forced sales but most will do whatever it takes to get through the next six months until the relief arrives in the form of lower mortgage rates.

Beware the bull-trap. (hint: rises lag falling i-rates)

It's quite repulsive seeing all these ghouls popping out of the woodwork rubbing their greedy little mitts together about house price rises. They even have the audacity to mock others for their "doom and gloom" outlook and ridicule the renters they extract their profits from.

How myopic does one have to be to think that the inability for an average family to buy a house is a good thing?!

For goodness sake Ghouls really?

Most owners are other families just like you except they bought and got on with their lives instead of incessantly venting on here about how houses should only ever be 3x income and cheerleading every piece of negative market news. I’ve heard it all here for more than 10 years it’s the exactly the same types over and over again until they buy and then disappear.

The other families just like me aren't the ones on here crowing about the price of their house increasing exponentially and locking others out of the market.

It would be nice if most families could just buy and then get on with their lives as you put it. Unfortunately most can't which is the problem..

"It would be nice if most families could just buy"

If the voting public choose to prioritise home ownership for owner occupiers then perhaps vote for a government who is willing to implement a stamp duty system and stamp duty rates in line with Singapore in the existing residential dwelling market and more incentives for non owner occupiers in the new build market to increase underlying supply of residential dwellings. This is one way to address the syndicates of non owner occupier buyers outbidding owner occupier buyers.

A capital gains tax will likely result in more hoarding of residential real estate by non owner occupiers.

If more owner occupiers are able to buy, then fewer cash needs on government finances as well as social issues

1) accommodation supplement

2) social housing needs

3) emergency housing

4) decreased rates of homelessness due to housing affordability.

5) couples delaying having children due to the high cost of housing and lack of affordability of housing.

I don't think you understand incentives. Stamp duty doesn't help anyone buy houses. It just reduces people's likelihood to sell. The only tax that puts land into the hands of those who would utilise it the best is land tax. It would resolve the landlord issue in short order.

"The only tax that puts land into the hands of those who would utilise it the best is land tax."

Can you give some examples of land tax in use in other countries and the rates of land tax in use?

What is the objective and purposes of that policy? What issue does that address? Does that solve for the issue of insufficient affordable housing for owner occupier buyers and consumers?

A friend in Singapore told me that due to the rates of additional buyer stamp duty on foreign buyers, many Chinese citizens have not purchased there. Not sure about other nationalities. This means that foreigners are not outbidding local resident owner occupier buyers. The issue that I want to find a solution for is more housing that is affordable for owner occupiers and consumers who are NZ residents, not necessarily for best use of land (whatever that means or however that is defined).

One of the drivers of high prices in the existing residential dwelling market is non owner occupiers buyers and syndicates of non owner occupier buyers outbidding owner occupier buyers motivated by tax free capital gains. Can you tell me how a land value tax would address this issue in the existing dwelling market?

I can understand land value tax impacting land bankers, but not non owner occupier buyer syndicates in the existing residential dwelling market that are outbidding local resident owner occupier buyers. Perhaps you can enlighten me on what I am not seeing.

The only people celebrating higher house prices should be those with multiple properties, or those looking to downsize/sell. For those of us with one home, it largely makes life worse as upgrading gets more expensive, and obviously for those with no home it makes the future even more bleak.

We should never celebrate the cost of living increasing.

Was expecting house prices to keep sliding all the way into 2025. Not going to lie, this is not the data I was expecting. North shore up an eye-watering 2.8% MoM is quite a shocker.

Friends just bought on North Shore after waiting for 3 years. Did it with one salary. Feels like market has met the buyer at least for North Shore.

You need to also look at what is not selling and you'll see the bigger picture.

I'm not surprised by the housing market in NZ, its practically bullet proof. Learned my lesson from Covid, predicted house prices would fall 25% and they did the exact opposite and went up 25%. Never making that mistake again.

I think most people were predicting that house prices will come down just before Covid. Then, as you said, we all got the reverse of that, unfortunately.

"I think most people were predicting that house prices will come down just before Covid. Then, as you said, we all got the reverse of that, unfortunately."

Most people are unaware of the rule changes that occurred during COVID which stopped mortgagee sales by lenders that would likely have caused house prices to fall.

Had the rules remained unchanged, it is very likely that there would have been a huge increase in mortgagee sales and very likely, falls in prices of residential dwellings as there would have been very few buyers active in the market. The economy would likely have fallen into a deep recession and unemployment would have spiked.

Hmmm ... Three months of small prices rises = a trend reversal?

I think not. But hey - don't take my word for it. Bone up, people. It'll save you $10,000's (probably more).

Beginner's guide: Reversal: Definition, Example, and Trading Strategies

I don't think its a trend reversal. We aren't going up fast but i do think a floor has been found for certain regions.

A floor? After just 3 months? And spring-time at that. I'm not so sure.

Maybe we'll enter a trading range? I.e. the price just bounces around between a floor and ceiling, flatlining in a trading range for years?

Meanwhile, if one buys too early, one's hard earned capital is going nowhere fast and the negatively geared are losing money hand over fist topping up their rents to pay a mortgage. Does that sound like good plan? Hardly! That's a classic bull-trap.

A beginner's guide to trading ranges: Range: Definition in Trading, Examples, and What It Indicates

Come on Chris I told you this was the bottom, time to move on and start predicting the market for 2025. I'm not going for big gains next year, personally I think we will see a bit of FOMO over summer and then the market will be pretty flat next year with a bit of a hangover after the party. I don't see the big gains the banks are predicting, more of a very slow climb out of the hole we have been in.

And "a very slow climb out of the hole we have been in" (your words) is exactly what'll lose people money if rents don't 110% cover the mortgage !!!

Rent doesn't need to cover the Mortgage. You need to look at the big picture on where you will be in 10 years time if you are still renting when you were in a financial position to buy a house right now. Trust me you will not look back in 15 years time and wish you were still renting.

And:

"In Tauranga, the average rate of home value decline has increased.

The city’s average home value reduced by 1% in the month of September – compared to a 0.4% reduction in August – with its three-month rolling rate of decline now sitting at 2.1%."

https://www.sunlive.co.nz/news/352618-spring-marks-subtle-shift-in-mark…

"Come on Chris I told you this was the bottom..."

With respect Zwifter, I find your words, in general, and on most subjects, entirely devoid of reason or worth.

If you're going to be condensing and patronizing to me, please forgive me for responding in my usual caustic fashion. ;)

Fear of missing out? Can you not read? More houses coming onto the market than selling, housing stock increasing, days to sell increasing. How in gods name do you get fomo out of that zwifter?

Agree. A little lift over summer, then flatness until spring ‘25. Could be a 3-4% lift Spring / Summer ‘25/‘26

Did you mean FOOP?

Well we will see Chris. No need for the hotlink. It makes you look a bit foolish and aggressive.

Your opinion is noted. I wasn't directing my comments at you per se. Many people read these comments and I was doing my utmost to counter overtly optimistic price rise comment with some general information that would counter the 'reckons' we see so much of.

fair enough

We've been actively looking to help some first-home buyers in Auckland.

We are finding a mixture of brand-new-town-house-style housing (terraced or shoulder-to-shoulder) and old-stock housing with similar pricing expectations.

The new homes are priced above the limits of the LVR. The developers say they need to recover the cost of the build. Some are selling one and holding stock back as the market is dire.

The old homes need work. And there lies the rub. They are priced at the land value. At the required mortgage levels to buy (even with the slightly lower interest rate), there is no money left to renovate (or time as the couples are both working).

So unless you're in the game of renovating, the stock is not attractive at the current price points. It's effectively a wealth transfer situation that most don't wish to undertake. (luckily the LVR is in place to stop the previous stupidity). Couples that sign up are committing to a lifetime of not only overpaying for potential land value but as much in interest again.

Good houses will sell to those who have enough money or where the vendors have to meet the market. Those purchases (natural churn) sustain the market.

So in effect, we have a waiting game.

Ironically while bringing interest rates down will alleviate the financial hardship for those who over-committed, it will also lengthen the waiting-out period for vendors that expect the current premium pricing. Extending the stand-off.

It will be interesting to see what Auckland's four-yearly valuations show. They've been delayed for some reason. I do hope they've tweaked the AI engine to not value all land in the same way. Properties grafted to sides of hills with no geoengineering might not be worth the same as the flat site down the road.

Also a final question. Why isn't it a requirement for property owners to provide the housing reports? Talking with several FHB aspirants they've made offers only to be let down due to wetness or problematic construction. That would go a long way to right-sizing value expectations

"Why isn't it a requirement for property owners to provide the housing reports? "

Totally agree! They should.

It would also ensure they either fix the problems (properly one hopes), or adjust their price from the get-go so less time is wasted (and money gets wasted.)

I ask the vendor to pay for one, done with an agreed inspector, and will refund them should I purchase. Ditto when I've had to pay for basic geotech studies. Even if the vendor doesn't agree, I ensure the agent has a copy and insist they know what is in it by discussing the results with them. Just doing my bit.

I ask the vendor to pay for one, done with an agreed inspector, and will refund them should I purchase.

The only problem with that is it likely prevents you accessing the inspectors PI insurance in the event of a mistake or oversight.

Even if the vendor doesn't agree, I ensure the agent has a copy and insist they know what is in it by discussing the results with them.

Definitely everyone should do this with all reports so the agent/vendor must disclose! Some people have a misguided notion that they don't want to share something for free which they paid for, but it benefits everyone in the long run and help keep price expectations grounded.

"The only problem with that is it likely prevents you accessing the inspectors PI insurance in the event of a mistake or oversight. "

Yes. Good point.

Although the cost to taking action can sometimes be more the building's remedial cost from the horror stories you read.

I've some knowledge of building practices and costs so that thought never occurred to me. And I won't go near anything that's even remotely significant unless my intent is to demolish. Maybe get a builder friend to look over the report and do another site visit with them? (Most builders I know love critiquing the work of others.)

Although the cost to taking action can sometimes be more the building's remedial cost from the horror stories you read.

Yep. Another reason why not to buy an apartment or certain townhouse developments!

It's certainly a lot easier if you have even just a basic understanding of construction, the real lemons are easy to steer well clear of.

I think vendor financed pre-purchase inspections have their place, but the industry needs at least a modicum of regulation before the average person should consider relying on one.

"Another reason why not to buy an apartment or certain townhouse developments!"

Steady on. :-)

Buying an apartment in a building that's had few issues after 15+ years is not risky at all. But always get hold of the body corp minutes and read them thoroughly as all buildings need maintenance. With new, and newer, apartments, only buy from the best developers that have used the best builders and have a track record of few to no issues. Their track record is critical. Much the same can be said of older terraced houses but again, take your builder friend. ('townhouses' are just ordinary houses?)

With newer terraced houses, pull the council file which will have the consented building plans, and should have all the Council inspection reports. If these inspection reports show many issues - walk away. Then share with a builder, then take your friendly builder for a walkover (as per above). Be aware that terraced houses have unique issues, especially the middle ones, and be know what they are and how to evaluate them.

Apartments & terraced houses are where the bulk of the people in cities live. They can't all be wrong, right?

Anecdotal story of a friend who bought a newly built apartment in Auckland in 2005. Had a builders report with no issues identified at time of purchase.

Ended up requiring extensive repairs. Don’t know how he financed the cost of repairs as he had a large mortgage.

Also had to move out whilst repairs undertaken, meaning additional payments of rent and the mortgage. Took a toll on their mental health .

Lucky he was still working and able to continue to make payments. After mortgage payments, and repair costs, compared to the current market value, he has made a loss after 19 years of ownership.

Retiree owners may have been unable to afford the repairs and been under pressure to sell and realise a much bigger loss.

As you rightly pointed out - the risk words were "newly built".

Was the developer and builder well established with a good track record? Did the person who created the builder's report use the full council file, or just wonder around peering into corners and looking knowledgeable? The words 'caveat emptor' apply just as much anything 'newly built' as to something that's been standing for years.

But sometimes, no mater how careful you are, you end up with a lemon. I feel for your friend.

"mixture of brand-new-town-house-style housing (terraced or shoulder-to-shoulder)" Still substantially overpriced (at least 10%) as far as I'm concerned.

"The developers say they need to recover the cost of the build. Some are selling one and holding stock back as the market is dire."

I hope they burn. Cut your price and cut your losses.

I'm hoping that the market, specifically in Akl, for these types of accommodation will fall further.

Older stand alone house with some garden/land any day over a new terrace. No comparison.

Your opinion & the wealth with which to buy said item, is noted. ;-)

Surely this is just combination of prices unwinding due to more normal debt costs vs the stupidity of covid 2% debt, and increased concern around unemployment during recession. Those with low debt and secure income will yawn on keep on their way. Those leveraged to the eyeballs under historical tax avoidance gambling will be increasingly sweating.

Some will pick the swings and position well, some will not because when someone wins financially some one else is losing.

Popcorn.

The month on month sales comparison isn't accurate as every month the number of sales for previous months gets updated to account for sales received by REINZ AFTER the stats cut off date.

For example the number of sales reported by REINZ when they released their August stats last month was 5685. Once adjusted for "late" sales that increased to 6015 (in the chart above).

So the "significant decline" this month is comparing an incomplete September month to a complete August month. The revision is typically in the 3-4% realm (last months was high in comparison) so I suspect that once next months data is released, the revised September number will be ~3-4% higher, and the "significant decline" will disappear....

No surprise that the Real Estate Institute who act for agents say the market is stabilised even when stock levels are through the roof.

Then central Auckland agents continue with the quote lie to both vendors and buyers, then wonder why their properties don't sell

The law, in NZ, says the agent is working for the vendor alone to get the best price. And while doing, so must be honest & diligent with all parties. The sale is an outcome from which the agent collects a commission.

The REINZ may have spun the facts to help sales - or help the market balance itself so a new equilibrium is found - but their statistics are almost certainly above board.

The national median days to sell increased by nine days to 49, and excluding Auckland, it rose to 50 days.

It's hardly a market poised for a rebound as some here are Spruiking. This looks like a new normal that's plagued by income insecurity. What an amazing opportunity for the next generation to get a foothold by amassing decent deposits (interest saving - risk mitigating) first. Why risk becoming cannon fodder?

Houses are for living in and not speculating on. edit.

Careful with reading these data. "increased by 9 days" is compared to this time last year. Compared to last month DTS fell (albeit by just one day).

How long do you think they have to amass these deposits? At the moment I would seriously avoid giving advice to anyone looking at buying because it’s on a knife edge…GDP/job security is poor so makes a compelling case for continued decline in prices…rates are getting cut heavily which makes a compelling case for improving sentiment, & potentially improving activity, if that’s the case then those could switch rapidly…I read your comment as “sit on your hands & keep saving”…you’re braver than me to dish out advice…I have a feeling, but not a crystal ball 😬😂

Let's see how Gecko spins this into a tirade about how no one should pay more than 2015 CV

True that:)!

So If I read the HPI correctly all regions had an increase in the last 5 Years?

Yes, nationally by less than 1% per annum compounded.

You're going to need 14% p.a. increase consistently here on out for the next 5 years to hit the fabled "prices always double every 10 years in NZ."

Great point, I never considered how dire the market has been until you pointed out there has only been a 1% gain per year over the last 5 years

What has inflation done over the last 5 years?

Awesome comment. The maths is strong in you.

Anecdotal but been looking casually for the last year (FHB). I stopped as soon as the RBNZ started cutting. For me the current "optimistic" mood just means no chance of vendors or agents meeting my price range in the near future. The data this month seems consistent with that: those that are desperate to buy can pay a little more now that borrowing is cheaper, but there aren't many desperate buyers left,and meanwhile every other buyer has less chance of finding a deal that makes sense to them. I think the RE industry, if they had more brains, should be pretty concerned about where this is heading because imo it's likely to mean an extended period of low turnover with both sides feeling little urgency to engage, and perhaps a degree of trepidation about the risks of doing so.

"the RE industry" you mention is by and large mortgaged past their own eyeballs to have their very own portfolio of 'can't lose' investments. The last thing they are concerned about is turnover. It's price appreciation that matters - and that's all.

To use a well overused expression - they have drunk their own coolaid. From the politicians that set the rules; the agents that hawk the product, the bankers that provide the Debt, the expert economists with clairvoyant expectations, to the real estate agency cat that watches it all go on. They all have a portfolio to enhance.

Owner occupier buyers: CAVEAT EMPTOR.

Just out, and why are we going to be any different?

"Household spending falls as Australians use cash to pay down debt....the only spending categories to rise in September were all essentials, indicating that increased take-home pay from tax cuts is largely being used to pay down debt and on staples, not spending on discretionary items"

We aren't. Lower mortgage rates are going to do the very thing that the economy is not designed for - have less Debt. Any additional disposable income is going to be used to lessen risk. And as Gross Debt falls, less will be applied to things like - buying property.

Lower interest rates are going to be much more meaningful to mortgage holders than the pittiful tax cuts. I'd say there's a fair few out there that can't wait to have a good time & spend after years of being slammed with high interest rates, cost of living etc...

What many people in NZ may not be seeing with respect to the conditions of the housing market in Sydney.

https://www.realestate.com.au/news/100k-nosedive-home-prices-fall-in-ha…

Australia hasn't had a rate cut... the article even states...

“Once we see a rate cut, it’s likely the market will go up as buyers will have bigger budgets.

“A cut will also boost confidence. We know one of the biggest concerns for buyers is an increase in rates and a cut would give them more certainty.”

That was the same blinkered thinking as here. And what are we seeing? If you, say, have a mortgage and the rates have given you payment relief, what are you doing with the 'surplus'? Spending it, or just letting the repayments reduce your Debt faster?

Will house price changes in NZ follow house price changes in Japan after their peak after interest rate cuts?

1) Japan interest rates

https://fred.stlouisfed.org/series/INTDSRJPM193N#

2) Japan residential price index

https://fred.stlouisfed.org/series/QJPN628BIS

Hard to see that. But the Japanese buyers of 1988 couldn't see it either!

And that's the point. No one ever does. No one in New Zealand today thinks that's even remotely possible. And yet we share a number of similarities with Japan - our location on seismic plates being the obvious one. Like Tokyo, we know that Wellington will get hit again. It's just a matter of when and how it affects the wider economy.

Indeed. The right play was to use 2% rates to paydown/pay off your debt. Those that chose to leverage themselves to the eyeballs at 2% only have to look in the mirror for who to blame for any financial woe they have.

Works well for those with job security, but the net effect is more people losing jobs and less debt payed off with the economy crumbling

Why is this sort of thing happening today?

"Cash, a new car, three years of guaranteed rent, free furniture or a low-interest loan are being offered as incentives to buyers of new homes at the $210 million Wirihana estate in south Auckland."

Answer: So that the prices of the properties themselves don't have to be reduced to attract buyers. That's the last thing any vested interest wants to see - further price deterioration.

"So that the prices of the properties themselves don't have to be reduced to attract buyers. That's the last thong any vested interest wants to see - further price deterioration."

Want to keep the headline most recent and most comparable transaction price stable to avoid falls in market value for previous buyers in the development.

Correct.

They are very desperate, and I bet my bottom dollar they will be going for the government underwrite. And that the government will have to buy them out.

One move up doesn't equal a bull market/bottom nor does one move down equal a bear market/top. If I were to read this chart like any other asset, the market has been neutral/ranging this entire year. The high is $800k (previous support) and the low is $755k, close to previous resistance of $747k.

There's a slight bear case in that we've been putting in lower lows but I'd argue that bulls are in charge if we break through $800k and bears if we break $750k. However, while we continue to range between those levels it's basically a coin toss as to where we go from here, if going by the chart alone.

I think the fact that neither the bears nor the bulls have been in control this entire year reflects the ongoing bickering in this comment section. So based on this chart alone, until we see a clear move in either direction, I don't see an issue with FHB's biding their time and continuing to save to reduce the size of their eventual mortgage.

My charts told me with absolute certainty that October 19th 2023 would be a pivotal point in the markets. And given the historical timing of past such events, a break to the downside after a period in decline looked ominous. It was the 19th October alright, but......so I've put my pencils back in their case for a while! (Who could have foreseen NVIDIA. Or maybe that's why it coincidentally came out then? Who knows. But it's all easy looking back)

A big elephant in the room remains Auckland Council’s new development contributions policy. Hardly received any journalistic coverage. Developers with interests in a number of areas in Auckland are effectively saying it will be ‘game over’.

Sure it’s not across all of Auckland but we are talking about a number of large areas. Met with one of the bigger developers today, they are worried. And they can’t appeal council’s decision. Only judicial review in the High Court possible, and that’s only on flawed process. High bar.

Gonna be a new headwind on supply over coming years

Won't they just develop in areas with lower DCs? Are you talking about Greenfield in Drury?

The recent plan changes have opened up loads of potential sites in Auckland.

Keen to hear your take on this.

Yeah sure, there are still plenty of brownfield areas with lower DCs. But we are talking some big brownfield areas AND greenfield with much higher DC’s.

Brownfield:

- Tamaki

- Mt Roskill

- Manurewa / Papakura

Greenfield:

- Drury

- Westgate

- Red Hills

- Whenuapai

So it certainly could be worse on the brownfield side. However if plan change 78 progresses (and it’s a big IF) there’s likely to be many more big hikes to come on DCs in brownfield locations, in order to address infrastructure deficits to support intensification.

Interesting, thanks. DCs are really interesting, they make sense in theory (new growth pays for the cost incurred in upgrading infra to meet that growth) but the more I dig into it, I see a whole bunch of unintended consequences. Not sure how to reconcile, targeted rates, flat DC rates, more direct negotiation with developers?

A more bespoke system would be fairer and lead to potentially better overall urban outcomes but would be expensive for AC to administer and for developers to pay for in time/ plans which would then potentially aggravate housing affordability. There is definitely a balance there between ease of administration and certainty for developers and fairness/outcomes.

The conversations on these matters have been going round in circles for decades!

I quite like special rates, in principle. For me a mix of those and DCs is perhaps the best option. Developers often don’t like special rates as it is a perpetual burden for owners, and therefore can be a bit of a turn off for buyers. Yet ultra high DCs obviously presents an entry barrier.

What's your definition of "special rates"?

Would it be loading the standard rates for 10 to 20 years to claw back the equivalent of DCs from the ultimate beneficiary, the owner?

If so, I think that's an excellent idea. (And places overseas do this, for exactly the reasons I mention below.)

Up front DCs charges are market-distorting in that they force the initial price of new-builds up, lifting all prices, while making new-builds less price attractive, harder to sell, so fewer get built. But banks love them - lots more interest collected forcing 100% of the DC cost into a single year.

(Council's employ economists. But either the economists don't do much, nobody listens to them, or banks have too much power.)

According to the council’s consultation document on the changes, they don’t think hiking DCs from circa 25k to 100-120k in a number of locations will push new build prices up, the idea being that land prices will need to adjust downwards to accommodate this. Internal economics advice apparently.

I don’t really buy this at all, although it might occur to a certain extent, but then I am not an economist. What do you think?

Meanwhile Council and watercare have brought the development properties to a sudden halt. No building in RED zones due to lack of services Infrastructure,

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.