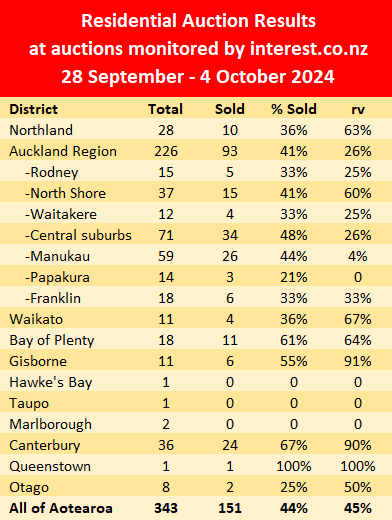

There were slightly fewer properties on offer at the latest auctions monitored by interest.co.nz, but the sale rate firmed a bit.

Altogether interest.co.nz monitored 343 residential properties from around the country over the week of 28 September to 4 October, down slightly from 356 the previous week but still well up from where things were at the beginning of last month.

However sales were stronger with 151 properties selling under the hammer, up from 141 the previous week.

That pushed the sales rate up from 40% to 44% at the latest auctions.

Overall we are seeing a modest but steady improvement in auction activity and this is likely to continue as we move from spring to the summer selling season.

However buyers remain cautious on price with just 45% of sales making their rating valuations and in Auckland that was just 26%,

Details of the individual properties offered at all of the auctions monitored by interest.co.nz, including the selling prices of those that sold, are available on our Residential Auction Results page.

The comment stream on this story is now closed.

You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

66 Comments

45% at or above rv. Improving rate

Don't really venture into these property threads much anymore, as they seem like a masterclass in what not to do.

The highly promoted 2024 property bargain basement discount bonanza looks like it had an opportunity window as narrow as a Death Star trench run.

Oh well kids, maybe wait another 15 years.

A decent 50bps drop is still required on Wednesday but I still think that the RBNZ will drop that one, its as easy as killing Womp rats in a Riverhead swamp.

Yes these threads are boring and mostly just filled with silly squabbling

Retired Poppy vs Iceman

Retired Poppy vs Yvil

Retired Poppy vs Pa1nter

There's one thing these squabbles have in common!

Indeed. About a year ago I decided to weed out people who don't add anything to my life, both on Interest and in person. So I don't see RP's comments anymore thanks to another reader's "patch" which allows to hide comments from certain posters.

I'm very happy I don't have to waste my time with argumentative people anymore.

It's sorta tricky, I have a wide group of people I interact with in real life, we enjoy each other's company, and have a good time.

But I also have an interest in subjects many of them aren't overly interested in. So having an online resource for discussion of some of this stuff is a useful thing.

This is really the closest thing I get to social media. So some of the attitudes and behaviour here are a bit outside of what I encounter most of the time. A large majority, would fit under what I'd call fault finding minds. I get the feeling this has become part and parcel of the digital life, where anonymity brings out the worst and people, and negativity captures eyeballs way more profitably than seeing the wonderful sides of life.

Good comment Painter. I come and go from comments for similar reasons - not at all a criticism of content of articles which are generally excellent, but some of the commentary gets tedious especially the personal criticism for someone holding different views. Perhaps this is simply digital life as you say, but I don’t find it in comments of say FT.

Painter, it is far easier to be negative going by many on here unfortunately!

Interest.co is meant to be a site that is designed to inform people how to make sound financial decisions I was under the impression going by the slogan?

There are too many that post that really do not have any experience with investing of any type snd are just disillusioned with the cost of housing because they do not own!

They feel that it is their given right to be able to own their own home.

I can assure you that it has never ever been easy to own but it does normally become easier once you actually do it, you make it work.

Investors that provide accommodation deserve to be financially rewarded because it is not just about buying and doing nothing.

there is so much that we do that we dont get compensated for straight away.

Not complaining but complaining from so many achieves nothing, wishing that investors go broke is pointless but if they feel better about that then it is their loss.

Very well said!

Well I will take any good news - for me Wednesday is the day. .25 drop will be good - however .50 will turn on the burners

BuyLowSellHigh + FlyingHigh = safeashouses. I can already smell you cooking from here....😂🤣

@retiredp. Well the person you describe there was something I aspired to - however the opposite it true - honest comment its been an absolute humbling experience the equation is more like (Assets depreciating + Assets constantly needs to be maintained ) + (Negative Cashflow + High Interest + ringfenced loss' ) = most of my salary goes to topping up mortgages. Honestly anyone wanting to be a landlord get good advice it ain't easy.

Mainly because many have been paying way to much to get there pre ringfenced tax loss.

perhaps - i was hoping to hear from you Averageman - do you remember our conversation about a month ago and me metioning that interest rates was going to drop to 5% wholesale by March and you ask me to put a reasonable argument forward since interest in Sept was almost 7%?

get good advice it ain't easy.

It's obvious to all you deeply regret not getting the right advice, yet in the first instance, you followed the advice of the likes of Wingman. Why do you now sing their praises?

@retiredp. maybe i am being to honest this morning. I like Wingman's comments that's about it. I have no in depth knowledge of Wingman / Iceman / Cote there is another few I feel my comments on here is more aligned to how I perceive life (as I said I dont know them)....... NZ Gecko / yourself / averageman - also have cracking comments - and i enjoy reading them. For me it comes down to this: Its easy to do nothing, a person just sits there and do nothing- its not so easy to have tried something that you perceive is worth while so I generally gravitate that way - all said and done, from 15 years of experience be careful becoming a property investor PS I am not deeply regretting my property journey at all. I am just saying its not easy and I have made mistakes this last 4 years was tough - however not regretting it. I have learned allot from the last 4 years and I will incorporate that going forward in my investor journey - rules change and that can catch you out.

maybe i am being to honest this morning

safeashouses, you can never be too honest! Based on your comment, you don't seem to be "Spruiker" material as the truth is much easier to remember.

Lesson number one: Always treat a Property Spruikers advice with the greatest of suspicion.

All the very best :)

Yes SAH seems a good sort...... unlike the old dawg Winger, has a sense of realism and humanity/humility.

Winger would happily lead numpty Lemmings over the cliff........in his "make a fortune" buying next to my Riverswamp paradise ........

He is just as bad as the Tones the Comb.....and Ash Churchless.

Interesting to see the US Govt yields rising strongly last few days.......is this the bottom of the recent rates dropping?

It’s certainly interesting with the US unemployment rate improving from 4.2% to 4.1% for September.

This along with Powell’s latest comments suggest the US rate cut cycle is already over?

Or they’re fluffing the data for the election and we should expect more downward revisions.

Mate, don’t even waste an ounce of energy on some people on here that do and know very little yet have strong opinions or advice to others. They’re basically insecure or probably jealous having missed out on investing in property some time back and try to put their insecurities on others. They will always proclaim doom!

Just laughable.

Well said safe as houses. Honesty is a great virtue and it’s refreshing to hear a bit of it. I genuinely hope things get better for you and stuff works out. Keep chipping away at it and all the best.

Not a dig at safeashouses or anyone in particular, but why would anyone not want to be honest on here? It's an internet discussion forum where you don't know anyone.

ego?

Denial / cognitive dissonance?

Undisclosed vested financial self interest?

They are already toasted.. burnt, ready to be discarded

94 Station Road Papatoetoe, Manukau City (https://rwmanukau.co.nz/properties/sold-residential/manukau-city/papato…)

Last sold 1999 for $190k. This sale $1.351 million. Annual rate of return: 8.16%. This place did "double every ten years". But not the house. Just the land - Mixed Housing Urban zone means big terraced houses or possibly 4 standalones can be build on its 1024 sqm section. Article says it sold to an "investor", a.k.a. a land bwanker. I'd guess they'll do an internal makeover and rent, while the land appreciates further while waiting for it to be re-zoned even higher, thereby maximising their tax free capital gains.

So folks, that's how it is done. i.e. Buy the land, spend nothing on the house, while growing older and older for 25 years. And the new owner will land bwank thereby removing the land from the available pool of developable land and forcing up the price of land ... All for the tax free capital gain.

Anyone else see a problem with this market dynamic?

it worked well for me, not so sure that property is as cheap now as it was in 2000

No. Over that period Papatoetoe became more desirable as Auckland developed to become a Beta+ Global City. All Auckland suburbs increased in value more than usual and it also extended to Tauranga and Hamilton as Auckland became less affordable.

Where’s the proof? Paper losses or real losses from selling?

Or just your guess?

You didn't even bother to read the first two sentences??

"More than 50,000 property investors are losing money on their rentals, Inland Revenue data shows.

"Information released under the Official Information Act shows that there were 53,350 taxpayers who reported negative rental income..."

Didn’t realise it was a clickable link, thought it was related to this article.

But yes. High rates which were (yes already past tense) temporary being the culprit is not rocket science. Enjoyed profits in the past few years anyway. Basically becomes Irrelevant with long term capital gains in any case. It’s all about the bigger picture, and during the journey every investment underperforms at some point. One would be naive to think otherwise.

In usual Iceman form, his keyboard comes before his brain. Can tell you were triggered and preparing to go nuclear depending on the response you received.

Edit: Beaten.

"Information released under the Official Information Act shows that there were 53,350 taxpayers who reported negative rental income..."

With higher mortgage interest rates, the number of taxpayers reporting tax losses has declined by over 50% since 2020.

A newly released paper, prepared for the Ministry of Housing and Urban Development Minister, Megan Woods, in December, said that 37 per cent of property investors, or 107,530 taxpayers, reported an annual loss to Inland Revenue – meaning the rent received did not cover their costs. The average loss was $9000.

https://www.stuff.co.nz/business/property/300288828/govt-crunches-numbe…

Also note that more will be cashflow negative due to principal payments on P&I financing.

I know I shouldn't be, but I'm surprised at how little discussion this Ministry report got.

Let's be clear, residential property 'investors' making cash losses year after year can only be banking on one thing: a big untaxed capital gain.

(That statement won't be obvious to some. Let me explain. The losses can be carried over to offset tax on profits in future years. The bigger the losses. The longer they last to offset tax. And no tax get's paid. It's even possible they last until the property is sold as their owners can no longer manage them. At which point IRD should be asking, "why did you 'invest' in the first place?". The only believable answer is they were there for the capital gain. At which point the intent to profit from the capital gain is clearly established and they should be taxed on it.)

Spot on

Shows the scale of the tax rinsing seminar model. Those making a loss will only be the late to the ponzi party members, as those at it for a while only had to quit a house or two at peak to be well in the black.

Agree clearly shows it was all a out capital gain.

Remember one tax filer could own multiple residential properties.

In 2021, over 22,100 properties were owned by a small group of owners.

https://www.stuff.co.nz/life-style/homed/housing-affordability/30041526…

I know of one non owner occupier owner who owned over 60 residential properties. They were promoting residential real estate investment whilst at the same time selling their entire portfolio in 2020.

What's driven the increase in homeownership, and can it last?

Stats NZ reported on Thursday that the number of households who own their home increased in the latest census.

It was the first lift in ownership recorded since 1991 - 66 percent of households are homeowners, up from 64.5 percent in 2018.

https://www.rnz.co.nz/news/business/529882/what-s-driven-the-increase-i…

Rising interest rates makes housing investment less attractive to investors from a cashflow (and capital gains) perspective.

Simultaneously it has caused prices to drop meaning deposits saved by FHBs go further (smaller mortgages required = less debt risk/interest rate risk). Those who buy now have significantly smaller mortgages than those who purchased a few years ago - they will become mortgage free years before those who purchased before them and the total interest paid will be significantly less = much better investment decision.

I remember people arguing with me on here a few years ago that rising interest rates wouldn’t help FHBs whatsoever- that it would make it impossible for them to buy - I argued otherwise. Investors couldn’t ever perceive prices falling significantly, nor would it appear they want FHBs to gain home ownership rights because that removes another renter from the pool (ie someone who can pay their rental mortgage) and it’s one less property available for them to buy to turn into a rental for their own gain!

The self interest of this type of thinking is perverse and not good for a healthy society.

Those who buy now have significantly smaller mortgages than those who purchased a few years ago - they will become mortgage free years before those who purchased before them and the total interest paid will be significantly less = much better investment decision.

Once you factor in years of principle paid vs mortgage paid, the equations become very muddy. You have to essentially cherry pick your sample of buyers with someone who bought at the absolute peak tippy top of the hot market who also got burned on a short term low interest rate that near tripled overnight.

Agree - but it proves a point that the best time to buy property isn’t always yesterday.

Sometimes patience does pay.

But clearly if the RBNZ keeps on cutting, the time to buy is now. Sooner or later you have to pull the pin, you cannot afford to just keep on waiting. If you currently have the required deposit available, then you should be currently very active in the market looking to buy. You have until Christmas if the cuts keep on coming, lock in a 6 month mortgage.

I didn't know this about the use of mate, in the UK the use of mate is more a call to reasonableness, like when someone has argued themselves into a hole "seriously mate?" it gives them an out to take a moment and know that they can back down safely. Sounds like champ is similar in UK and NZ, it's used in an ironic dismissive way when you've given up trying to argue.

Learnt something new about kiwi culture today.

Yeah the old sarcastic endearment. As you say, passive aggressive behavior that seems to be quite trendy with highly insecure kiwi men.

If the RBNZ keeps cutting then it means the economy is in dire shit. It will not be the time to buy. Prices will (in my view) likely keep falling as the RBNZ cuts because more businesses will be failing/defaulting, unemployment rising, risk of deflation increasing - all of these things are very bad for asset prices.

2020 and the COVID response may have confused you somewhat about how economies and asset prices really work in tandem. Dropping rates means economy is getting worse = no economic growth = headwinds for asset prices/cash flows.

The time to buy will be 6-12 months after RBNZ stop dropping rates.

And if you are correct and house prices jump again significantly then my suggestion to FHB would be to leave the country permanently as you are being setup to be bagholders for a completely dysfunctional country/society/economic settings and policy.

Some chuckles from that one, I_O.

"If the RBNZ keeps cutting then it means the economy is in dire shit. "

Or you can look at it as I do, "The economy is in dire shit, so the RBNZ has to keep cutting." If two years of near zero growth, rising unemployment, etc isn't 'dire shit' then I don't what is. ;-)

"The time to buy will be 6-12 months after RBNZ stop dropping rates."

(Said in Admiral Akbar voice: "It's a [ponzi] trap!")

I think you meant: The time to buy is when yields are sufficient to deliver one's target return on investment. ;-)

Dire shit is growth with a negative sign in front, unemployment significantly higher than where we are at present and more business failure.

You know we’re in dire shit when National decide that it’s time to start spending. Ie they reverse course on their election promises.

We are not there yet.

Auckland steady on 10% of properties auctioned selling over RV. Nothing to see here.

I've been in since 1990.

The Govt have done their best to kill the golden goose over the past twenty years. To a large degree they finally succeeded. No doubt that ethic will continue in future years. Essentially it's like going into a long term business with constantly changing Govt policy.

There is still much to gain from property, but that certainty as it was, is far less now.

Still feel it's a time game, better to get into while you are young. The worst thing you could do is enter retirement carry large (or any) debt. Don't get into property when you are anywhere near approaching retirement.

I think you meant: The time to get into property is when yields are sufficient to deliver one's target return on investment.

That's what you meant, right? ;-)

No. If you get to 65 and you are not freehold you are royally f**ked.

For 20 years I've been hearing people make cases for holding off, because they thing some government policy is going to magically make it more affordable.

The inverse has occured. National are finally making noises about fixing housing supply, but like any government idea it'll be long in the tooth and not comprehensive enough when it arrives.

You mean mortgage free or unencumbered rather than “ Freehold”!

Freehold is a state of tenure rather than being mortgage free!

Solid advice, generally. I'm planning on buying in the next year or two, as I hit 50, but will go in with a minimal mortgage. I save more than house prices appreciate (pandemic period was nearly an exception). Work/live overseas so no drastic need for a house in NZ yet.

Why not buy now and rent it?

Rent pays mortgage. There's a few perks involved in renting, but there's risk too, pick your tenants carefully. I like to pick them myself, not let a renting agency run it.

Sure, but I'm not living in NZ and need to have a solid look see next time I'm back before I pull the trigger.

Can this possibly be right?

I get the Herald each Saturday, and there's a column today that says, "Car sales on the road to recovery".

"It was the third consecutive month of improvement for the new vehicle market, which has faced considerable challenges in 2024, MIA said."

I keep reading here that we're all on the brink of economic ruin and a crashing property market - which is obviously all a figment of the imagination of some posters.

I don't have the Herald, so I can only go off the first paragraph/Google results. Here's what I read:

September's sales reflected a 12.8% improvement over the average monthly result for the year to date.

But year-to-date registrations are down 16.1% (18,057 units) compared with the same period in 2023 and 23.5% lower than in 2022

Still terrible figures compared with the recent past. Ask any dealer. Electric and plug in hybrid cars are the worst category especially second hand.

The problem with many figures of the past few years is COVID distortion. There were massive shortages for vehicles amoung other things, so we got big sales numbers posted as inventory arrived.

Probably better to compare most things with 2019 and a guess what their natural movements might have been for the coming years.

For those interested. I don’t necessarily agree, but it’s worth thinking about the drivers and the constraints.

The Economist’s article on the “house price supercycle” explores how a variety of long-term factors will likely drive house prices upward for decades, despite short-term economic fluctuations.

The article highlights three key drivers. First, demographic changes are playing a crucial role. An increasing immigrant population, especially in developed countries, is raising housing demand. Research shows that a 1% rise in immigration can boost house prices by up to 3.3%. Despite some political efforts to curb immigration, the need for labor to support aging populations in these countries means immigration will continue to fuel demand for housing.

Second, urbanization remains a major factor. Despite predictions during the COVID-19 pandemic that remote work might reduce the appeal of cities, urban areas have retained their draw. Cities are still economic and social hubs, and employment rates in capital cities across many countries have even increased, adding pressure to already strained housing markets. The limited housing supply in dense cities means prices are likely to keep climbing.

Finally, the third factor is infrastructure challenges. In many cities, poor transportation options and rising congestion are preventing people from living further away from their jobs. This pushes up demand in already crowded urban centers where new construction is slow, exacerbating the housing supply crisis.

In the long term, the convergence of these forces—demographics, urban demand, and infrastructure limitations—suggests that house prices will continue to rise faster than incomes, with only temporary fluctuations based on interest rate changes and economic conditions. Interest rates, which fell to historic lows over the past few decades, have made borrowing cheaper, further pushing up house prices in many developed markets.

This article indicates that we are likely still in the early stages of a housing “supercycle,” with rising prices to be a persistent trend for many years to come.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.