The days of buying a stand alone, three bedroom house as a residential property investment may be drawing to close, with interest.co.nz's second quarter update of indicative rental yields and cash flows showing the yields for investors on three bedroom houses are poor and the cash flows they're likely to generate are even worse.

The figures also show investors are likely to find much more attractive options among multi-unit properties such as apartments and home units.

Interest.co.nz tracks the Real Estate Institute of New Zealand's lower quartile selling prices for the three main types of residential investment properties; three bedroom houses, two bedroom apartments/units, and one bedroom apartments/units, in each of the country's main urban areas and updates them quarterly.

These are then matched with the weekly rents charged for new tenancies in the same types of properties in the same districts over the same time period.

Those figures are used to provide a gross indicative yield for these types of properties in each area.

Interest.co.nz also calculates how much money would be left over from the rental income once mortgage payments on the properties were paid, assuming the mortgage was for 60% of the purchase price and over a 20 year term, to give an idea of likely cash flow. - both sets of figures are displayed in the tables below.

Both figures suggest three bedroom houses are likely to provide investors with pretty poor returns.

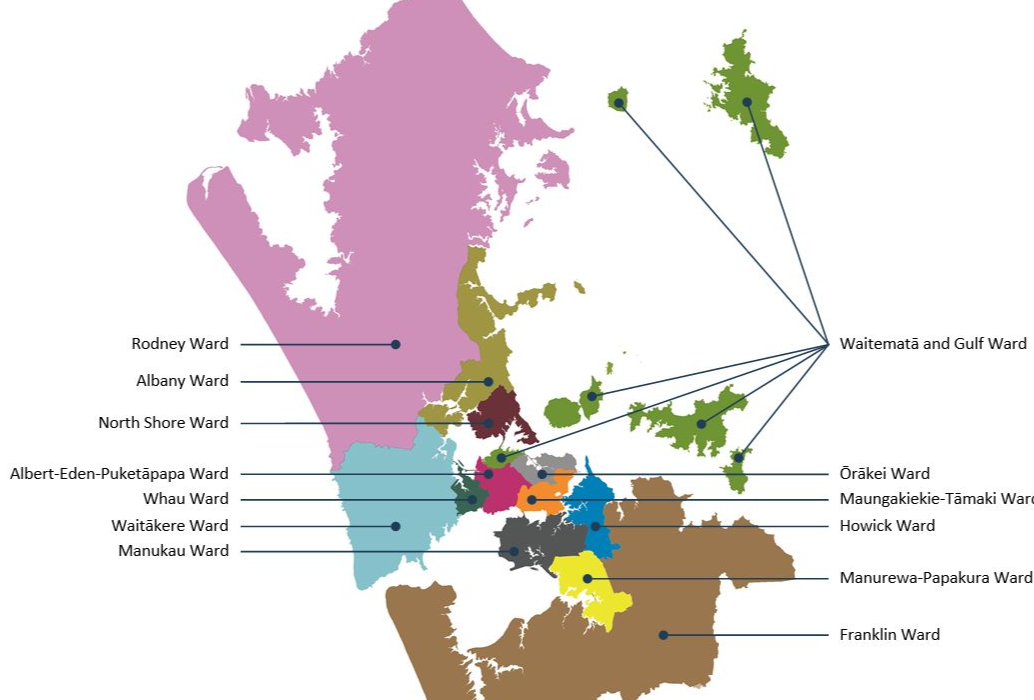

The gross yields on three bedroom houses ranged from 3.4% in the Waitemata & Gulf and Orakei wards in Auckland City, to 6.8% in Invercargill (see the map below for the location of Auckland Council wards).

Whanganui, Dunedin and Invercargill were the only districts where the yields were above 6%.

The yields for three bedroom houses were particularly low in Auckland, averaging 4.6% across the region, and ranging from 3.4% in the Waitemata & Gulf ward to 5.2% in the Manurewa-Papakura ward.

The average yield across the entire country for three bedroom houses was 5.8%.

While the yield figures suggest pretty meagre returns, the cash flow figures are disastrous.

Of the 40 urban districts tracked by interest.co.nz, 18 would have produced negative cash flows once the mortgage was paid (three bedroom houses only).

Essentially the rent would not have been enough to cover the mortgage payments, assuming the mortgage was on the terms outlined above.

The cashflows ranged from minus $553 a week in Auckland's Waitemata & Gulf ward, to plus $103 a week in Invercargill.

And even those places where cash flow was positive would probably be looking at negative cash flows once other expenses such as rates, insurance, repairs, maintenance and periods of vacancy are factored in.

Those figures suggest that anyone buying a three bedroom house as an investment in the second quarter this year was probably having to put their hand in their pocket to meet the outgoings in the hope of making a capital gain at a later stage, and that probably hasn't gone to well for them recently.

However, both the yields and cash flows for multi-unit dwellings look much more favourable for investors.

The average gross yield for two bedroom units was 7.3% nationally in the second quarter, and gross cashflow was a positive $159 a week.

That still wouldn't leave much to play with once the non-mortgage expenses are paid and an extended period of vacancy could be disastrous, so it should probably be described as marginal, but at least its not underwater.

The stars of the show for investors are one bedroom units.

On average these provide an average gross yield of 11.1% and average gross cash flow, after mortgage payments but before other outgoings, of $238 a week.

At that rate investors might even make a few pennies.

The comment stream on this story is now closed.

| Indicative Gross Rental Yields & Gross Cash Flows | ||||||

| For Residential Investment Properties | ||||||

| By Main Housing Types | ||||||

| Q2 2024 | ||||||

| District | Three Bedroom House | One bedroom unit/apartment | Two bedroom unit/apartment | |||

| Gross Rental Yield | Gross weekly cash surplus/deficit after mortgage paid | Gross Rental Yield | Gross weekly cash surplus/deficit after mortgage paid | Gross Rental Yield | Gross weekly cash surplus/deficit after mortgage paid | |

| Whangarei District | 5.8% | $45 | 8.2% | $137 | 6.3% | $70 |

| Auckland Region | 4.6% | -$128 | 15.4% | $313 | 5.7% | $37 |

| Rodney Ward | 3.8% | -$265 | ||||

| Albany Ward | 4.2% | -$201 | 5.1% | -$27 | 4.7% | -$84 |

| North Shore Ward | 4.1% | -$231 | 5.4% | $7 | 4.5% | -$129 |

| Waitakere Ward | 4.5% | -$124 | 4.4% | -$97 | 4.9% | -$52 |

| Waitemata and Gulf Ward | 3.4% | -$553 | 24.8% | $376 | 22.1% | $470 |

| Whau Ward | 4.2% | -$187 | 8.7% | $176 | 5.2% | -$13 |

| Albert-Eden-Puketapapa Ward | 3.6% | -$385 | 6.0% | $54 | 5.2% | -$17 |

| Orakei Ward | 3.4% | -$491 | 5.8% | $40 | 4.4% | -$139 |

| Maungakiekie-Tamaki Ward | 4.0% | -$266 | 6.1% | $62 | 5.6% | $32 |

| Howick Ward | 3.8% | -$312 | 4.9% | -$47 | 5.0% | -$51 |

| Manukau Ward | 5.1% | -$42 | 5.9% | $40 | 5.9% | $56 |

| Manurewa-Papakura Ward | 5.2% | -$27 | 5.5% | $13 | ||

| Franklin Ward | 4.7% | -$97 | ||||

| Hamilton City | 5.2% | -$25 | 5.7% | $18 | 5.1% | -$24 |

| Taupo District | 5.4% | $5 | ||||

| Tauranga City | 5.0% | -$46 | 5.3% | -$9 | 5.8% | $52 |

| Rotorua District | 6.0% | $60 | 7.5% | $156 | ||

| Whakatane District | 5.4% | $2 | 5.0% | -$32 | ||

| Hastings District | 5.9% | $58 | 5.8% | $38 | ||

| Napier City | 5.6% | $33 | 8.6% | $218 | ||

| New Plymouth District | 5.9% | $57 | 8.5% | $138 | 6.0% | $49 |

| Whanganui District | 6.4% | $82 | 7.6% | $103 | ||

| Palmerston North City | 5.7% | $40 | ||||

| Kapiti Coast District | 5.4% | N/A | 5.2% | -$25 | ||

| Porirua City | 0.0% | N/A | 7.4% | $195 | ||

| Upper Hutt City | 5.7% | $41 | 5.6% | $19 | ||

| Lower Hutt City | 5.8% | $54 | 8.4% | $170 | 6.6% | $115 |

| Wellington City | 4.9% | -$76 | 7.8% | $147 | 6.8% | $132 |

| Nelson City | 5.3% | -$9 | 5.8% | $29 | 5.7% | $26 |

| Marlborough District | 5.5% | $10 | 4.5% | -$31 | ||

| Waimakariri District | 4.9% | -$54 | 0.0% | -$108 | ||

| Christchurch City | 5.3% | -$9 | 7.8% | $134 | 6.4% | $87 |

| Selwyn District | 4.8% | -$68 | ||||

| Ashburton District | 5.7% | $26 | 0.0% | -$289 | ||

| Timaru District | 5.6% | $18 | 0.0% | -$449 | 5.2% | -$10 |

| Queenstown-Lakes District | 3.8% | -$354 | 9.1% | $225 | 6.4% | $121 |

| Dunedin City | 6.1% | $74 | 6.5% | $71 | 7.4% | $131 |

| Invercargill City | 6.8% | $103 | 8.6% | $152 | ||

| All of Aotearoa | 5.8% | $47 | 11.1% | $238 | 7.3% | $159 |

| Notes: All indicative yields are based on the REINZ's lower quartile selling price and Tenancy Services median rent for each property type in each district for Q2 2024. Where a field is vacant, it is because there were insufficient sales/tenancies for that type of property to produce a reliable yield/cash flow figure. All figures are gross and do not include any allowance for insurance, rates, repairs, maintenance or other expenses or periods of vacancy. Figures are based on properties being purchased with a 40% deposit and 60% mortgage. Mortgage interest rate used was 6.50% with a 20 year term. | ||||||

Auckland Council Wards

- You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

77 Comments

Renters are all being funnelled into Govt owned social housing and foreign owned Build To Rent high rises. The days when low income people could still enjoy a traditional Kiwi lifestyle of raising their kids in a nice house in a decent suburb, are over. This is how you perpetuate inequality and fuel the increasing resentment that can then be harnessed by Left leaning political parties pushing identity politics and socialism as the "solution".

Spot on, you can just see all the public and private social housing providers rubbing their hands with glee as their social empire (and their self-importance) grows.

As C S Lewis noted:

“Of all tyrannies, a tyranny sincerely exercised for the good of its victims may be the most oppressive. It would be better to live under robber barons than under omnipotent moral busybodies. The robber baron's cruelty may sometimes sleep, his cupidity may at some point be satiated; but those who torment us for our own good will torment us without end for they do so with the approval of their own conscience. They may be more likely to go to Heaven yet at the same time likelier to make a Hell of earth. This very kindness stings with intolerable insult. To be "cured" against one's will and cured of states which we may not regard as disease is to be put on a level of those who have not yet reached the age of reason or those who never will; to be classed with infants, imbeciles, and domestic animals.”

Must be so tiring seeing boogeymen in every shadow

"There are none so blind as those who cannot see"

"There are none so blind as those who REFUSE to see".

It's deliberate ignorance that the phrase highlights.

"Renters are all being funnelled [sic] into Govt owned social housing and foreign owned Build To Rent high rises. "

Got some facts to support that assertion, K.W.?

No? I thought not.

Funneled == government and BTR outfits who are actually building more housing, are offering renters a better deal than whatever speculators of suburban houses do.

This is somehow bad

How is it a better deal? Being forced to live in social housing ghettos alongside gang members, drug addicts, and sex offenders while being wholly funded by taxpayers is good? Raising kids in high rises with no space to play while all profits are sent offshore to foreign owners is good?

I'd take the old Kiwi lifestyle of a suburban house any day thanks.

We could have that suburban dream if only wages had kept up with land house prices.

Unless there was a supply response, then all higher incomes would have done is bid up the price of existing housing.

For there to be a supply response of a suburban form there would have had to have been either highway projects like 60s america, demolishing swaths of the existing city for highways plus sizable %'s of GPD spent on roading. Or flying cars.

See this is the bit you're willfully brushing over. Pretty well anyone can choose the old kiwi lifestyle of a suburban house, if you move to small town.

People don't want that. They can get a hand up in the city, they want to live in the largest cities in the nation, where they can live a much better life overall. Raising kids in a insulated warm apartment with no mold on the walls within a 15 minute walk of the premier parks, playgrounds, pools, courts, sports centers in the city would be something that many kiwi kids could dream of.

If the New Zealand owners of capital don't want to build anything, then they shouldn't be protected from foreign competition eating their lunch. Not sure why this is controversial. Yes I'd absolutely rather see some enterprising productive foreign company earn a crust here providing a good product than some stagnant local petty oligarch provide a rubbish one.

There are parallels in ending protection for rent seeking local industries for consumer goods, cars, TV's. The more this happens in housing the better.

See this is the bit you're willfully brushing over. Pretty well anyone can choose the old kiwi lifestyle of a suburban house, if you move to small town.

But we want to live in the throngs of hundreds of thousands, if not millions of other people, but feel a sense of space.

People want to live on 2000sqm of landscaped land, in a warm heritage house, where they don't see hear or smell anything of anyone around them. But simultaneously want to be walking distance to services provided in the urban core of cities of hundreds of thousands or millions of residents. This is obviously geometrically impossible for most people.

Prices and choice in the market let people make the tradeoffs themselves and reveal actual preference over stated preference.

Most parents would probably prefer to be able to send their kids out to the backyard to play for a few hours while they get a bit of peace and quiet, instead of having to supervise their kids in public every second.

In terms or mental health, social development and spatial cognitive development, suburbia is literally the worse place to raise kids.

I think almost anywhere in the 2020s is.

Suburbia is supposedly better for birth rates but.

What do you think happens when Govt policies make it financially unviable to provide private rental housing? When the only providers left in the market are the Govt and the foreign corporates who get huge tax incentives and subsidies to undertake BTR developments but then operate at a "loss" forever while the cash is repatriated offshore tax free to owners?

What policies are those?

.

"What do you think happens when Govt policies make it financially unviable to provide private rental housing? When the only providers left in the market are the Govt and the foreign corporates who get huge tax incentives and subsidies to undertake BTR developments but then operate at a "loss" forever while the cash is repatriated offshore tax free to owners?"

Doesn’t NZ need more new housing for its residents? If New Zealanders don't want to build it (given the change in interest deductibility for existing dwellings making new builds less attactive) then should we let those who want to build do it?

When you refer that BTR operate at a loss, are you referring to the depreciation deduction that they get for tax that current buyers of new builds get ring fenced? (Interest deductibility is available for buyers of new builds for current buyers of new builds in the long term and short term rental market.)

That's just capitalism.

It's obviously financially viable for the big corporates and financial institutions.

Do you not see the flaw in your argument - operating at a "loss" forever - is how residential property investment is done.

Tell me you care about providing private rental housing when you invest in property.

"Renters are all being funnelled into Govt owned social housing and foreign owned Build To Rent high rises"

Where do you get this information from please ? I'm genuinely interested, as I'm an accommodation provider for the needy.

Thanks.

Translated, "this Government just shafted my asperations involving emergency accommodation and I'm scratching for another teat to suck on"

RP, how dare you cast aspersions on ....... oh wait, I just noticed you have a Green Tick...

As you were!

😆🤣

The days when low income people could still enjoy a traditional Kiwi lifestyle of raising their kids in a nice house in a decent suburb, are over

That was doable because of left leaning politics of the Savage Labour govt. plus a different attitude of the population. It was doable before we got brainwashed/indoctrinated into rentier and finance capitalism - everything we were warned about.

We haven't had a true "left wing" since. Most govts have become more authoritarian whether left or right.

"Both figures suggest three bedroom houses are likely to provide investors with pretty poor returns"

To the benefit of FHB's owner occupiers this is further confirmation there need be no hurry to buy. This would suggest this segment will certainly underperform in the capital gains department. This in itself will motivate more short sighted investors to exit. For the near future unsold inventory will just keep piling on.

You have got it wrong as usual RP. All that will change is the very slow move away from 3 bedroom houses as rental investments. Like I said the other week, 3 bedroom houses on decent bits of land will continue to outpace townhouses in house price gains, its pretty obvious really. There will be no unsold 3 bedroom house inventory piling on because 45% of all new builds now are town houses. The figures are just a sad reflection that house price gains have outstripped wage growth in this country and yes you are now going to get funnelled into a townhouse as the only affordable option.

"All that will change is the very slow move away from 3 bedroom houses as rental investments"

So you agree but it's going to happen "sloooooooowly". Funny how your focus has shifted to 3-bedroom houses that sit on their lonesome on large tracts of developable land - how convenient. Is this the only way a FHB can purchase a 3-bedroom house?

I think my original point still stands. Given the current state of this market investor exit cannot be quick without colossal loss. On the ride down, housing can prove notoriously illiquid as an investment if one is trying to exit. Why be the bag holder of an underperforming investment? Through their usual shortsightedness, many will have already decided other ways to invest. As soon as they possibly can, they will give it a shot. It's a long term overhang -edit

.

That is correct, and its certainly happening in my area. Standalone family homes are sky rocketing in value (not helping my rates situation!) while the market is flooded with unsold 2 bedroom townhouses crammed on to sections. There are very few new houses being built in my area, so the value of the existing ones keep going up. And as the prices of them go up, the rental yields become ever more ridiculous. I'm considering renting my house out and going to QLD but I would get a 2.8% gross yield if I did that. That makes it a no brainer to just sell up and go, and put the extra cash in the stock market for a 5-6% net return.

In your case it's likely location dependent though, you've commented that you pay over $8k in rates so you likely live in an old, established and desirable area of Christchurch where not a lot of new standalone houses will be built due to the price of the land.

Up to $9,400 now. And yes, its a desirable area. But you used to be able to buy an old dunger in the area (plenty of them post earthquake), bowl the house, and build something new (which is how I have a 2016 built home). Now every old dunger is suddenly worth $2M because a developer can put 6 townhouses on the section. No new family homes are ever going to be built now.

https://www.oneroof.co.nz/news/quake-damaged-house-smashes-elderly-owne…

6 homes, including many happy families, is better than one.

Sorry, the (local) government no longer gets to prevent those buyers / families from getting what they want (a townhouse in a great location)

2 bedroom, 70 sqm townhouses are not "family homes". They are for people getting off a plane with a suitcase, who own nothing else.

That is a rich persons patronising tripe. Most people cannot afford the big section nowadays - end of story unless land falls dramatically in price - no hope of that occurring with our immigration.

Well you commented your rates were $8.4k on 25 July. You proved my point, 22 Clissold Street in Merivale had a CV of $1.18 in 2019 and $1.8 in 2022 ($1.43 land value) so it's only the wealthy who are buying it to demolish and then build a new standalone house. It was a developer who bought it recently to build townhouses and I agree with the poster above, more families are now able to live in desirable locations like Merivale and that's a good thing. Your house in its desirable location was built in 2016 so completely different times when land and house building were cheaper. Perhaps Zwifter would like to tell us how much his house CV has gone up in value over the last 3 years and we can see if it has gone up by $700k, I suspect not.

If it were a functional house that was liveable it would be worth $1.8M. As an "as is where is" it would have been worth a lot less before developers got in on the action. It would sell for land value only - so max of $1.4M even today. Probably less, as you can pick up a decent size section in Fendalton for around a million at the moment. Thats what home builders would have expected to pay - but outbid by developers.

Even a million dollars for a section is a lot of money, only the wealthy are buying sections at that price and then building on them. It's interesting you live in a desirable area with $9k rates and yet there are "tons (sic) of crappy townhouses sitting unsold". This could be a good thing though, if these properties don't sell and they need to, prices will drop until they're sold and this will pull down prices around them as well.

Sounds like the market is encouraging efficient use of desirable land.

Except the irony is, is that they build them and then cant find anyone to buy them so they sit empty. Tons of crappy townhouses sitting unsold in my area, because for the same price people can go buy an actual family home in a nearby suburb. The street over from me has four developments on it - the first to complete at the beginning of this year is still trying to offload them. The second one is having to discount prices. The third one has just hit the market, while the fourth still has to complete the build. The jokes on the developers now. It would have been better to have had four nice family houses built.

It's easy to improve the yields on all types of rental housing simply by admitting that you overpaid their true value by at least 1/3, which everyone has.

It would be best if you also used net figures and a full ROI.

I don't think that "admitting that one has overpaid, improves the yield".

Of course it does, it's simple maths.

You pay $1,000,000 with revenue of $50,000 equals 5% yield.

But is only worth $660,000. Revenue is still $50,000 so yield is 7.57%.

It's the easiest way to improve yield.

Go on, admit it.

who in their right mind would pay $1K a week to live in a $660K house?

I'm sure there's plenty of good places for that down southland way

You totally missed the point 1) it was an example with numbers rounded for simplicity, but if take the interest.co.nz figures above with Akl at 4.6% then you have people paying $46,000 on a house that someone has paid $1,000,000 for yet is only worth $660,000 once the non-value added speculative gains are removed 2) and on how the yield is calculated, especially in jurisdictions where you have to earn your return based on the yield, not speculative capital gains like NZ does.

It's the same house, but just because the investor overpays for it, which all in NZ do, does not automatically mean the revenue should be less, but it could be if the investor had purchased it without the monopolistic speculative gain extra, which also means it's more of a free market and there is more competition.

eg $660,000 (same house remember) @ 6% Gross is $39,600. Yield is better for investor and rent is cheaper for tenant.

There seems to be this wilful ignorance amongst many investors, both rookie and experienced, of expecting a status quo return to speculative capital gain rentier returns.

The Govts. policies to free up land to equal demand as not even kicked in yet.

It’s Cognitive Dissonance in full display.

”Tell him you disagree and he turns away. Show him facts or figures and he questions your sources. Appeal to logic and he fails to see your point.”

- Leon Festinger

Likely we will see more of the likes of Simplicity in this market.

My view is this might be better all round than amateur investors.

Unless you are a Simplicity fund unit holder, in which case investing your money in low yielding residential returns is an idiot idea. The only way that makes sense is if BTR rents are much higher than normal rents - which you currently see with the existing BTR projects charging $600 for a studio unit (and targeting overseas immigrants who cant get normal rentals).

Would love to know how successful they are at renting those studios out (at $600 pw)

One btr is listed, perhaps look at their books and report back.

Let's be real. Most "investors" are only in it for the speculative tax free capital gain. Little to no capital gain in appartment type dwelling so most are not interested. With today's stupid house prices and normalizing interest rates, there is little in the way of capital gain on a normal house either.

Ergo, little interest from "investors".

Yeah, we all now that these 'investors' were following the model of buy anything, don't maintain it, spend as little on it as you can get away with and then flip the run down liability to the next sucker or apartment builder.

Now they face reality.

Need more one bedroom places built. So hard to find place to yourself if you're a single or below median earner couple. Nationals simplification of balcony requirements etc will help a lot. Often councils have drafted these rules to (intentionally or otherwise) to disincentivise 1 bedroom or studio apartments.

The market wants that product, landlords can provide the capital. Only missing link is being able to build them profitably.

Agreed, Wellington is a prime opportunity in that space as os many couples and singles would be happy to have their own place if it weren't so expensive due to lack of options.

Like I've been saying, do the maths (and forget the mythical un-taxed capital gains which aren't going to be like the last 30 years.)

I might add a granny flat to my backyard.

Probably one of the only ways someone could hope to crack 10%.

These figures don't even include rates, insurance and maintenance which is likely another $200/week for many properties. Then there's the opportunity cost: you could have stuck your 40% deposit in a TD and be making $200+ per week, after tax.

Who are these unicorn investors paying for house deposits with cash you speak of?

yeah who was not already balls deep Nov 2021... clearly not aggressive enough or P.....s

The article fails to mention South Taranaki where gross yields for 3 bedroom houses are regularly 7+% Plenty of large subdividable/second-dwelling-able sections where transporting on another dwelling could easily result in double figure gross yields. There are possibly other unmentioned markets where this is also the case?

Greg,

Just checking that rental yields for Waitemata and Gulf Ward are correct.

Rental yields for 1BDRM and 2BDRM apartments look a little high at 24.8% and 22.1% respectively? And potentially impacting yields for entire NZ?

The particularly great yield on "Waitemata and Gulf Ward" stand out.

However, this is where leasehold properties are concentrated. You can't look at rental income and ignore the ground rental expense.

A real house with privacy and room to move for me please.

They don't compare lifestyle blocks here sorry.

I swapped 800 sq m for 150k sq m

agree but land does need maintenance

many recent landlords would not understand that this traditional effort brings financial reward

The government's goal seems to be to increase rental supply, at the exclusion of all else. It was unbridled investor demand that pushed house prices up to their ungodly peak in 2021. If anything, we should be trying to grow home ownership, rather than grow rental supply. A lady I work told me that without interest deductibility her two rental properties did not make 'financial sense'. That's a bit of a worry, because if they don't back make financial sense without generous tax treatment, then we probably should let the creative destruction of capitalism do it's work. Some investors aren't wearing the true cost of borrowing, and it's leading to sub-optimal outcomes for everyone.

Most businesses wouldn’t make financial sense without interest deductibility. Not just property businesses.

Exactly. Hardly anything would exist if companies had to pay income tax on their gross revenue at 30%, and individual tax rates are even higher. Its not a "tax break" its the application of generally accepted accounting and business principles that apply the world over.

"Most businesses wouldn’t make financial sense without interest deductibility. Not just property businesses."

Most businesses? Seriously? What total bollocks.

Capitalism's "creative destruction" is an oxymoron, another fallacy. Where have we had optimal results for the benefit of all?

Any creative destruction usually benefits those with the biggest pockets.

and the foresight to see it coming, funny they often have deep pockets i wonder why?

"Low rental yields and negative cash flows a feature of three bedroom houses as rental properties - multi-unit properties the way to go for investors."

As far as I know, it's always been a balancing act between capital gain (well-located houses) and yield (apartments, units, commercial property). At least, that's been the case since I first started investing in property in 1995.

Though yields used to be high and capital gains low for free-standing houses in crappy little towns - not sure if that's still so.

Yeah crappy little towns have a hiding coming

locals cannot buy afford to buy since 2005 , the investors are bag holders.... 8)

other investors will buy .... but lower, I am waiting

1/2 a million for Turangi?

"locals cannot buy afford to buy since 2005 "

Non owner occupier buyers from out of town have outbid local owner occupier buyers on local incomes making them unaffordable for local owner occupier buyers. This has resulted in the lowest rates of home ownership in NZ in over 70 years.

https://www.nzherald.co.nz/business/nzs-latest-property-hotspots/EF3SJK…

https://www.stats.govt.nz/news/homeownership-rate-lowest-in-almost-70-y…

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.