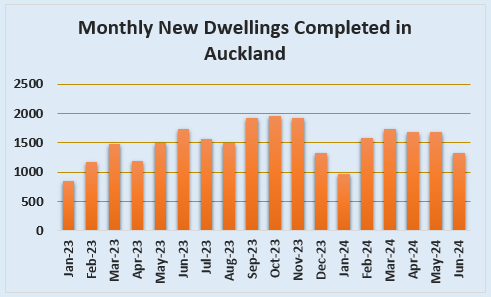

A sharp drop in the number of new dwellings completed in Auckland in June suggests the residential construction downturn in the region is starting to bite hard.

Auckland Council issued 1332 Code Compliance Certificates (CCCs) for new dwellings in June, down from more than 1600 in each of the previous three months, and down from 1742 in June last year. (See the graph below).

CCCs are issued when a building is completed and so are the best indicator of new housing supply, unlike building consents which are issued before construction starts and are an indicator of potential construction activity.

The downturn in June completions signals an end to a stunning run of growth in residential construction in Auckland that has long been signaled by the slide in residential building consents in the region.

June was also the first time Since July 2022 that the number of homes completed in any 12 month period declined.

Fewer consents means fewer starts of new building projects, but many builders have been kept busy by the large amount of work already in the pipeline. However, the latest figures suggest much of that work is now also coming to an end as well, with fewer homes being built and fewer new building projects getting underway.

That means builders may struggle to find work as existing projects come to an end.

However, June was just one month's figures, so we will need to wait and see how the rate of completions plays out over the next few months to get a reliable indication of where residential construction activity in Auckland is likely to settle. But the latest figures are not looking good.

- The comment stream on this article is now closed.

•You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

96 Comments

Still a few new builds being completed in our area but things have changed slightly, one place looks massive but it is symmetrical so I suspect its two houses joined on the one section but is designed as to not look like a townhouse. Not many sections left here now and the few that are look very steep so they would be very expensive to retain and build on these days.

Fairly unhelpul anecdote. As Sam Stubbs has said - there is no shortage of land, even in Auckland. It is hoever very expensive and complex for the average landholder to build anything.

The seemingly less glamorous news/trends that support the bigger picture in the property cycle along with interest rates trends. Will still take time but it’s all happened before and will repeat. Consents were dropping, now new build completions are dropping, rates are dropping. Go figure what will eventually gradually happen.

Again none of this has been happening or will continue to happen overnight.

1330 completions in a month in just Auckland is still very high. Based on consent numbers that implies about 3300 completions nationally, or about 39,000 annualised, which can absorb about 100k population growth (edit: may be more like 33k / 85k after accounting for demolitions, thanks jfoe). That's already roughly in line with the actual population growth of 93k in the last year. But that 93k growth is an anomaly due to borders reopening, and right now population growth is slowing much more dramatically than home completions (7k population growth in 2024Q2 compared to 37k growth in 2023Q2 - whereas home completions only fell from 1700 to 1300).

Keep dreaming.

1330 completions in a month in just Auckland is still very high. Based on consent numbers that implies about 3300 completions nationally, or about 39,000 annualised, which can absorb about 100k population growth. That's already more than the actual population growth of 93k in the last year.

This has to assume though that previous supply was keeping pace.

Well it has done, dwellings per 1000 population are currently sitting at 391, which is actually above the 25-yr average of 389. In fact since 2000 the only period where there has been higher housing supply to population than right now was the 2006-2014 period where ratios stayed above 390 with a peak at 395 in late 2008. At current growth rates we'll exceed that peak within the next 12 months.

From 2016 to 2021 the ratio was very low, continually below 385, with a nadir of 378 at the start of the pandemic when returning kiwis boosted the population. So it's been a very quick reversal.

Is the average house size the same as it was 25 years ago. Where's it heading? Do we have some areas emptying while others are growing?

Are you assuming gross completions rather than completions net of demolitions?

Yes, because I don't think any data exists on demolitions. My guess was that they would run at quite a small fraction of the completions - maybe 10% - so it wouldn't substantially affect the analysis.

Digging around, Statistics NZ has a total dwellings estimate which I assume makes some attempt to account for attrition of existing properties. That's showing +8.3k in 2024Q2, which annualised would extrapolate to 33.2k houses / 85k people. The actual growth in dwellings over the last 12 months was apparently 36.8k / 94k. A little lower than my estimate but basically the story is the same - housing supply and population have been growing at roughly similar rates in the last year, but the population growth is slowing far more drastically.

How about the last 10-15 years.

See comment above. Houses per 1000 people is virtually no change from 10 years ago. Much better than 5 years ago. Better than 20 or 25 years ago. Worse than 15 years ago, but likely to catch up within 12 months if current trends hold.

Based on our household sizes, and vacancy rate (because there can't not be vacancy rates) we are short around 20-25 houses per 1000 people.

You are just inventing numbers now. Perhaps our housing stock is smaller in terms of floor area, but I suspect the average capacity for occupants is as good as before. Townhouses are not spacious but pack plenty of bedrooms and bathrooms.

Average household size is 2.6. for for every 1000 people, you need 386 houses. Add in 5% vacancy (and that's an average between the private sector, with lower vacancy, and the public sector, who have more vacant properties), we are short.

I suppose “this time it’s different” for you isn’t it?

Keep dreaming.

No, I expect house prices to revert to fundamentals sooner or later, like they always have. You're the one who seems to be expecting something magical, and in denial about what the fundamentals are saying.

If I gave you a piece of land for free, it's still going to be expensive making it into a house.

That's one fundamental that's not going to significantly change anytime soon.

For house prices to go low and stay low, you also need other fundamentals to change. Lost incomes that won't return. The population to fall and never come back. That sort of thing.

If land was free house prices would be about half what they are and very nicely affordable. And land doesn't cost anything to make, it's already there. Its value relies on house prices significantly exceeding construction costs, or being expected to do so in the foreseeable future.

I'm not sure I agree that construction costs won't fall rapidly - they rose pretty rapidly in the boom period - but house prices can fall a long way even if the costs don't.

If land was free house prices would be about half what they are and very nicely affordable. And land doesn't cost anything to make, it's already there

It is at least $100k to make a piece of land a legal title to build a house on. Then about $400k minimum to put a modest house on it.

I'm not sure I agree that construction costs won't fall rapidly - they rose pretty rapidly in the boom period

I'll almost bet money square meter costs won't fall by more than 5-10%. There's not a huge amount of margin in building a new house. Labour isn't getting cheaper, nor are the regulatory costs dropping.

Cost increase then a plateau type of trend?

If I had to take a punt, subdued demand for new construction will see prices plateau, likely for at least a couple of years.

But if someone thought they'd drop by 1/4 or more, they're dreaming.

Back to the future?

"Since 2021, there has been an increase in the number of investors buying new builds.... Mortgaged investors' share of new build purchases increased from 25% in 2020 to about 31% now, according to CoreLogic analysis.... Back in 2012 it was only 8%."

https://www.stuff.co.nz/business/property/132738453/why-dont-property-i…

Too many new townhouse developments in undesirable areas

They were never designed to be Desirable. They were designed to be an Investment.

That's how we pump the Lifeblood of The Economy, liquidity, into a System that needs more Debt as each day passes.

If the Auckland townhouse situation is anything like the Chch one, outside of a select few "premium" developments these townhouse developments only made sense on the basis that you could a) borrow easily against an existing home to buy one, and b) that some mug punter would always be willing to pay more than you paid.

Take those two points away - particularly the second one - and why on earth would you buy some Williams Corp $hitter, with terrible workmanship and materials. Also other considerations like how do you get the other owners in the development to help chip in for maintenance that might be needed across the development (this is actually a genuine question - do these things have body corporates or whatever?)

Sounds pretty different to the Auckland experience then. I've been in one over a year, no dramas, built by a reasonably well-known outfit and it gave us access to amenity that met our needs at an affordable price. Standalones in the same area would have been several hundred thousand more and would not have given us the location we have now.

Interesting to know. Funnily enough, we live in a townhouse as well - but built post-quake yet well before the boom of Williams Corp, Wolfbrook etc. So it's a good sized townhouse in a very small development, plenty of on and off-street parking, nice finishing etc. There is a company here that does old style houses in typically small developments, and they seem to be nice properties albeit unusual layouts to modern tastes ... in other words you can find nice townhouses.

However, from what I see most of the new developments - particularly the larger scale ones (e.g. for anybody familiar the massive Williams Corp development on Wharenui Road) are built for investors to leverage into. And so you wind up with this weird blend of many units being Air BnBs, some being longer term rentals, and then the occasional FHB. I fear these developments will age quickly, particularly if investors are left holding the bag with neggy equity.

E.g. one of my clients borrowed against his home in Tauranga to buy a Wolfbrook place in Christchurch - at the peak of the market I might add. Don't think he's ever seen the place in person (I had to explain to him where it was, relative to Chch landmarks he knows). It was just an easy route to use paper equity, and he didn't want to miss out.

Those crappy townhouses are replacing decent family homes, so as the number of larger family homes diminish, the value of the ones remaining sky rockets. Meanwhile, the replacement dogboxes sit unsold on the market, falling in value, unable to attract investors thanks to them no longer having any tax benefit, and being designed to only house people who just got off a plane with a suitcase, their rental pool is rapidly diminishing as well. That's what's happening in my area at least.

You live in Chch too, don't you? Based of what I see in my area, I'd agree.

Correct KW, most people on here cannot see the big picture, too focused on just the numbers. Decent stand alone builds in good locations will continue to rise.

Decent stand alone builds in good locations will continue to rise.

Like this one in Devonport? Which has risen from *checks notes $2.6M at peak to $1.3M asking price now. Or did you mean will continue to negatively grow?

https://www.trademe.co.nz/a/property/residential/sale/auckland/north-sh…

Devonport is a joke, I helped with a reno there a very long time ago and got to see how they were built all those years ago. No I mean stuff bult in the last 10 years with double glazing and insulation that meets the modern building code. North facing, loads of sun and elevated with privacy on a decent size section like 550sqm plus.

All of New Zealand is a joke, Devonport just happens to be one of the most desirable, expensive, premium suburbs in the whole of New Zealand.

So yes I agree, housing in New Zealand is crashing big time when even one of the richest, best suburbs in the whole country prices are dropping vertiginously.

The programme is called location, location, location for a reason.

Those nicely built houses out in the wop wops are about to follow Auckland prices down the pan, if the regions follow as they have previously. Oh hang on, is this time different?

Decent family homes - you mean asbestos laden, draughty, wooden joinery, uninsulated old homes…..

But old homes have good bones, so that trump everything?

Earlier in the year, we were doing work on an old motel complex. Would've been cheap as cheap to build back in the 60s/70s. Concrete block walls everywhere.

The skirting that came out, was Rimu clears. The stuff that went back in, compressed sawdust.

I’d take one of those any day than living wall to wall with a 4mx4m patch out the back along with your other 3/4/5 neighbours coronation street style.

Your two sentences sum up why we have this shambles perfectly

Auckland City should encourage more low rise unit blocks like those in Australia cities, the common six-pack units.

They have more space, we don’t. Our geography doesn’t support that too. Our previous and existing planning is just shit.

We have plenty of space. What we don't have is a) anyone prepared to go to war over those in central suburbs who have access to gold-plated services like frequent bus routes but fight tooth and nail against any intensification, and yet insanely b) when we do open up land on the fringes, it takes forever to connect them to anything that makes driving or using a car (even at peak hour) viable, so you end up with huge congestion and parking pressure.

It's like we're actively trying to get the worst of both worlds and succeeding only so we can feel good at not failing at literally everything.

What are you on about?

Auckland doesn’t have the flat vast space centrally speaking compared to any of the big Aussie cities. Besides, mostly all our central areas are zoned for intensification.

Aussie cities also have massive urban sprawl, the difference is they put in the infrastructure and plan ahead before putting in the houses.

Massive difference.

Correct. For Example:

Nelson - Pulled out the railway in the 1950's which would have the region looking very differently today had they not, and continued to connect it to Blenheim and the West Coast

Christchurch - Post quake they could have put in a Melbourne-style spider train network which would have changed the CBD for the better and afforded a different lifestyle without the need to drive, while still building local hubs around the train stations

Wellington - Probably the best the country has to offer but there's always room to tweak things for improvement

Picton - New ferries and terminals cancelled so no increase in capacity to come for future planning

Auckland - Light Rail, they should have just got it done and continue to look for other rail opportunities such as Sydney did

Nelson - Pulled out the railway in the 1950's which would have the region looking very differently today had they not, and continued to connect it to Blenheim and the West Coast

You can barely justify cars/trucks on these roads.

Agreed, and the maintenance for the roads due to this is frequent.

Iceman, I can think of 20 places in Auckland for these six packs; just to name a few:

Mt Wellington, Panmure, part of Ellerslie - Onehunga, Papatoetoe, Glen innes, Grey lynn, Blockhouse Bay, Windsor - the list is endless. All one needs is about 800sqm of vacant land to build a block of 24-30 units (as they are doing where I am in Brisbane)

Just get people to get rid of their NIMBY mentality.

No chance in Auckland with the urban designers having so much influence.

btw I am surprised if that’s happening in Brizzie, as I thought the urban designers wielded lots of power there too

Is there about to be a tidal wave of distressed property hit the market at unbelievably reduced prices? And are others going to be taken down by the Du Val contagion? But given the Statutory Receivership, maybe it all just becomes State Housing. I know! Call it Northern Response to compliment the AMI property insurance débâcle down, south. Time will tell.

"Du Val leaves at least quarter-billion in debts, Govt steps in"

Rinse and repeat. The cycle continues....

We will be back to lower rates, higher demand and shortage on houses in the years to come. And around and around we go!

Yes but DTIs, so will be quite muted and slow IMO.

Worse. As % rates fall, investors don't buy more, they use the respite to pay down existing Debt. So New Stuff sits on the shelf, unbought. We aren't ready for that. We assume that lower % rates will encourage investors to gallop down to the Bank and borrow-and-buy more. But many have now had a glimpse of what can happen. And Debt retirement; lower Risk, makes absolute sense.

There may be a little of that, but low rates will def entice people back in. FHB share will continue to rise too, overall theme will be Confidence.

FHBer share should rise. That's how it's supposed to work - new family formation requiring a home, etc.

Many on here, and in fact wider New Zealand, have probably never seen a real property route. It's personally and economically frightening. Bank just plain stop lending to most applicants. And % rate keep falling, even as rents keep rising, and yet fear stops buyer, seller and lenders for moving. Household start disintegrating, feeding even more property distress. How we've put ourselves into this sitaution, when we've had so may chances to change direction, amazes me. But it is what it is. And I guess we'll all know the result in due course.

Many on here, and in fact wider New Zealand, have probably never seen a real property route. It's personally and economically frightening. Bank just plain stop lending to most applicants.

We have been seeing this for quite some time now. It's just slow, and biforcated.

As we tighten up on lending, the number of eligible FHB lenders is going to fall. It can't not.

Its only money, not the end of the world.... negative equity in the UK in the early 1990's is a good template for how banks here will deal with this. The banks will do EVERYTHING to try and keep you in the house (ie paying), because once you stop their loss is crystalised.

They even let people move negative equity to a different property in the UK.... how does that work?

I guess the same way they can give you a loan on a car that you're upside-down on the second you're off the lot?

Agree, me and my friends (all investors) have no intention now (or in the foreseeable future) to add to our portfolios. Plan is to just wait out the current downturn, wait for the prices to start rising again and once we hit our magic number wrt capital gains, sell up and divest into hassle free (albeit not without risk) investment funds to enjoy (hopefully) an early retirement.

The last few years have shown us that with changes to regulation, climate concerns, worse inequality and worsening social fabric of NZ, property is not going to be the safe and hassle free investment it used to be. Meanwhile our aggressive funds are doing ~20% YoY atm..

Massive construction unemployment is here. Backlog has been cleared out and there’s very little in the pipeline. It’s going to be a rough ride for many for the remainder of 2024. Hoping for rebound in 2025.

Will be end of 2025 for interest rates relief to pass through, so 2025 itself is not going to look that flash, 2026 H2 if things go well... and their is a global economic pulse to help us up off the canvas... rule one , get a knee to canvas, wait for count to 8 then get and and start dancing till the bell rings.

If only we had been able to see this coming.

Also, a plasterer just quoted me $95/hr + materials + travel + GST.

That is pretty high.

Then again, no one wants to be a plasterer.

How much are you getting plastered? If it's a whole house, you can do a lot better. If you're talking about a few small areas, then the nature of having to make 3-4 trips for only a few hours at a time means they have to charge a higher rate than if they were working on a larger area.

Couple of rooms. So it's sort of in between. Happy to pay extra for smaller jobs. I don't mind them getting trade price and charging a retail, but they add 20% to materials on top of retail.

I'm usually charging a mid point between my trade price and retail. But never more - otherwise I'd just tell a client to supply it. At least it's only plaster though, which doesn't cost much. Unless you have some fancy coving or something going on.

They do sound a little bit rogue-ish. My suspicion is they're more accustomed to pumping out volume, and if they're any good then this probably nets them around that $95/hr figure, working to a meter rate. On the potential plus side, if that were to be the case, they're potentially going to be more efficient at their time - I.e., someone charging less, might spend more time swanning about so you end up paying the same amount anyway.

Many investors are just paying down their loans. They want to see Labour campaign at the next election to get an idea of what tax rules they will one day have thrown at them.

Surely they added to their portfolio yesterday, last week and last month! Definitely before Xmas!

They don't seem to be in any hurry, after all prices keep falling.

Prices are not falling where I am!

Great opportunities to get ahead financially at the moment tho as less competition.

Where will the TD money go? Maybe to Australia - the exodus continues. 14% drop in European births this last year, 5000 future families have already gone.

Personally, I've moved into listed property trusts. Locking in 7-8% dividend yields, with capital gains on the horizon as interest rate drops feed through into cap rates and debt refinancing. Money for jam really, and no crappy tenants to deal with.

Interesting - Care to mention those property trusts you speak of?

Like Tina, they are everywhere

https://www.eqt.com.au/corporates-and-fund-managers/fund-managers/insti…

Anyone with enough to buy a house with no mortgage should really talk to a wealth manager... hard to avoid concentration risk doing things yourself.

Yes, the REITs look much better value and less hassle than residential.

That's the benefit of half the population being scared of anything sold on the share market, good deals left for the rest of us.

Cant complain, have a 15% TSR for the year to date, and another 4 months to go. Last time I owned REITs I got a 30% TSR per annum for 5 years. Hoping to repeat that this cycle.

Interesting KW.

If you live in ChCh you will be aware that prices for family homes have not dropped in ChCh at all really.

reality is that the prices are going to be going north very shortly in the low to medium range .

Established investors are going to enjoy the next few years as rents increase and prices of homes increase again.

‘fewer consents means fewer starts’

It’s not that simple. It’s why I was saying mid-late last year, when consent numbers were very high, that it wouldn’t necessarily flow through into housing starts.

Since then consent numbers have dropped a lot, and will drop further. They won’t be great over the coming year. Yet, I predict starts will increase significantly later in 2025.

Too bad we don’t see articles from Rodney Dickens these days. He’s one of the very few economists and commentators who gets all this stuff.

That will probably send the house prices up....so will this....

https://www.oneroof.co.nz/news/return-of-the-land-grabbers-millions-on-…

Unexpected things happen all the time in all things property!

"the owners purchased it in 2021". Top of the Market stuff?

"Unfortunately, in the last year, they received notification from Auckland Transport that the Penlink will go right through the property."

"Land-banking is a long game, though, and it can take years or even decades for purchases to turn a profit." And sometimes, never.

"....land-bankers who think it might be lucrative. Farhi advised such buyers to be careful, especially if they have to borrow to buy. Where the risk comes in is, if the zoning, the availability of infrastructure, or the timing doesn’t pan out the way you expect it to"

It's a risky business.

Do ya homework, you can make a fortune. Most see obstacles, winners see opportunity.

I'll suggest that it's because most don't see the obstacles that we find ourselves in the precarious situation we do today.

Many, if not most, relied on any obstacle being minimised by the mantra of "Property always goes up!" - and it doesn't, as the vendors in your link might find out.

Property doesn't always go up, but when it goes down, it's the time to buy.

Which is what they're doing. When stock markets tank, most sell, the smart traders buy, because they know the stock market will eventually rise and exceed its previous high.

Property, like shares, is not a uniform asset. Those who bought Pumpkin Patch after it had fallen by 75%, then saw 100% of their new investment wiped out. As did any number of 'famous' names in the late 80's, and many since.

Prices fall for a reason. And just because they have, being 'low' doesn't magically transform that reason into "It must be time to buy!". And the biggest reason to be cautious? As you write - TIME. It took 25 years odd to get back to break-even after the 1929 market adjustment for anyone who did hang on that long. And what's different about anything we've had before now, to what we've had in the past? Time - We have the largest cohort of ageing asset owner in history knocking on the gravedigger front door. And asset of all kind are going to be liquidated to meet both current and future living costs. Those ageing buyers have done their buying. Now they are going to turn into sellers. But the obvious buyers, the next generations(s) can't afford to pay the prices being asked. So.....

The Great Depression is irrelevant.

Tell me when was the last time in NZ's recent history property prices fell for more than a couple of years. They didn't.

Posters here will look back in a few years as the greatest opportunity they missed.

Here's the thing about investing in anything. Being able to survive be wrong. That involves the price paid, the time needed to see it through, and the ability to pay the running cost in the meantime.

And you're right. Recent history gives us no guide as to what can happen. Perhaps looking back at what happened the last time 'free money' ran out; Dunedin, the wealthiest town on the planet in its day, saw the gold rush end. And with that came property devastation there unseen since. And what do we have in abundance today? Free Money. But it's not gold - it's Debt. And that is what makes what we have today far more dangerous than what we've had in our recent history.

Why are you restricting your analysis to one country? Plenty of worldwide examples of prolonged property crashes.

You're restricting your sample size to a handful of bear markets and trying to draw conclusions from this tiny sample.

The average recession length in NZ is 2.5 years. We're about 18 months into this one, so maybe a year to go, which will coincide with the approach of the next election.

Politicians like prices to rise as elections near.

For possibly the first time, we have a housing minister calling for lower prices. It does remain to be seen whether he overpowers the bulk of the party who likely want to see their portfolios increase.

I also (rather cynically) think he’s just trying to ride the wave of prices declining 😂

Why are you restricting your analysis to one country? Plenty of worldwide examples of prolonged property crashes.

The ones that do also have permanent economic decline.

If we're looking to turn into Greece, Italy, or Japan, house prices are the least of everyone's concern.

I was actually thinking of the UK in the 1980s, and Ireland post-GFC. Plenty of people scarred by negative equity in the UK when I was growing up - it was pretty high on their list of concerns.

Similar to older NZers who got stung in the stock market crash in the late 80s.

Ah so we're talking a decade give or take.

Yes, something like that. Enough to put a serious dampener on a narrow investment strategy.

The idea that this is impossible because it hasn't happened in this particularly country for a few decades seems like hopeful logic.

I remember the 87 stock market crash, I made a fortune out of it.

I had a floating mortgage on my house which I could run up to $100k. There was $30k on it so I borrowed another $70k and put it into the local stock market.

But after a few months, I visited the stock exchange in Queen St and saw the mania that was unfolding, so I sold it all and took my profits.

A lot of kiwis lost the lot, some of them lost their houses.

Buy in gloom, sell in boom.

You're amazing.

NZ in the 1970's had a prolonged property slump in real terms.

New Zealand 1974-80

I guess if everyone sold, and sold all at once, we could be in for big problems.

I actually think one of the best assets to pick up this coming downturn is an existing business owned by a boomer who wants to retire.

Especially if they specialise in goods or services in demand by said generation :D

I have a friend who had just sold a local tourism business, been going for 20yrs and is successful, cruise ship trade, selling due to health reasons.

Only 2 inquiries after listing 4 months ago.

Was accessed to list at $320k, dropped to $235k, selling for $150

The imigrants from Asia are getting a bargain.

Smells fishy. If it’s 1 hectare there won’t be much left once penlink goes through it.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.